- Automotive Components & Materials

- Automotive Steering System Market

Automotive Steering System Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Steering System Market by Component (Hydraulic Pump, Steering Column/Rack, Sensors, Electric Motor and Others), Mechanism (Electronic Power Steering (EPS), Hydraulic Power Steering (HPS) and Electrically Assisted Hydraulic Power Steering), Vehicle Type (Passenger Car, LCV and HCV)) and Regional Analysis for 2025 - 2032

Automotive Steering System Market Size and Trends Analysis

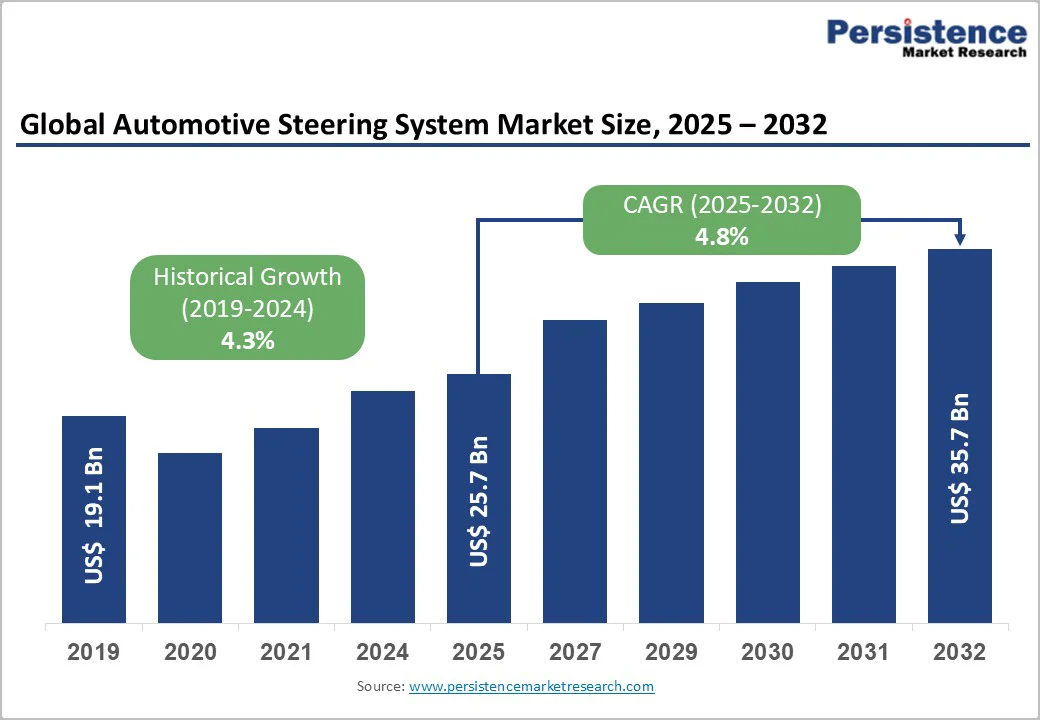

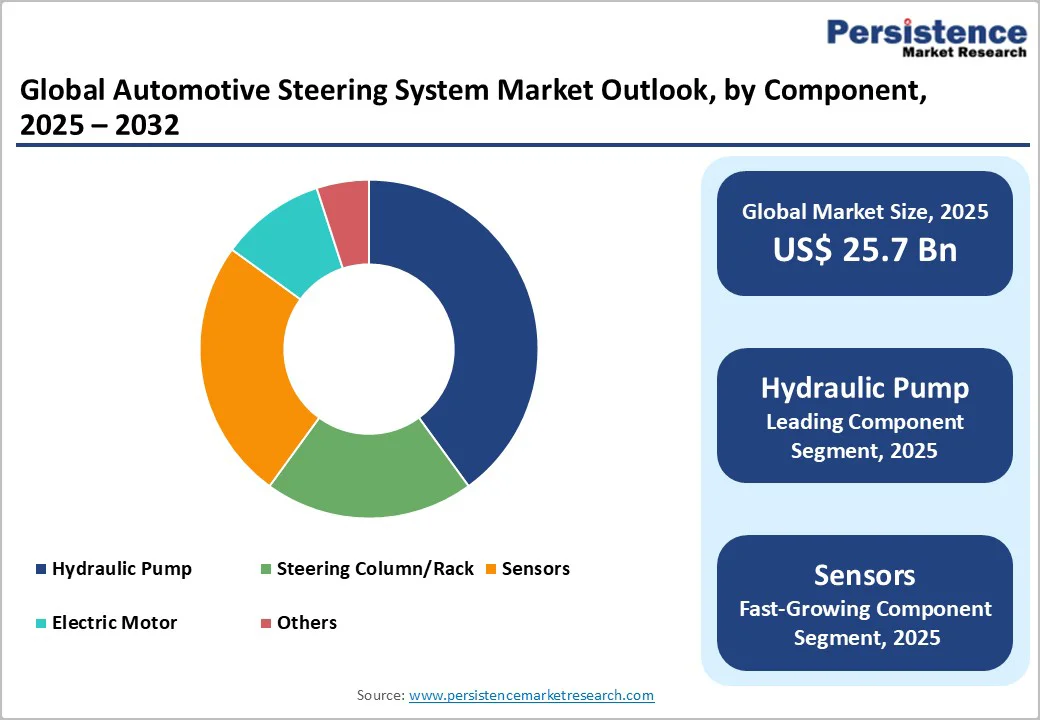

The global automotive steering system market size is valued at US$ 25.7 billion in 2025 and is projected to reach US$ 35.7 billion by 2032, growing at a CAGR of 4.8% between 2025 and 2032. The market for automotive steering systems comprises the manufacturing, distribution, and development of steering mechanisms utilized in motor vehicles. This critical element plays a pivotal role in regulating the trajectory of an automobile, thereby guaranteeing driver command and road safety.

Key Industry Highlights:

- Product Segments: Electronic Power Steering (EPS) dominates with 69.3% market share, driven by near-universal OEM adoption, improved energy efficiency, and seamless integration with ADAS and autonomous driving systems. Electrically assisted hydraulic steering represents the fastest-growing product segment.

- Component Segments: Hydraulic pumps command 38.4% share, sustained by strong usage in commercial and heavy-duty vehicle platforms requiring high steering loads. Sensors are the fastest-growing component segment, rising at 8–12% CAGR, driven by advanced torque sensor integration for ADAS, and combination sensor modules that reduce component count by 30–40%, lowering system cost and improving reliability

- Vehicle Type Segments: Passenger cars lead with 64.3% market share, supported by the world’s largest production base and rapid shift toward fully electronic steering systems. Light commercial vehicles (LCVs) represent the fastest-growing segment, expanding at 6–9% CAGR, fueled by e-commerce logistics growth, fleet electrification, and increasing adoption of EPS for efficiency gains and lower maintenance.

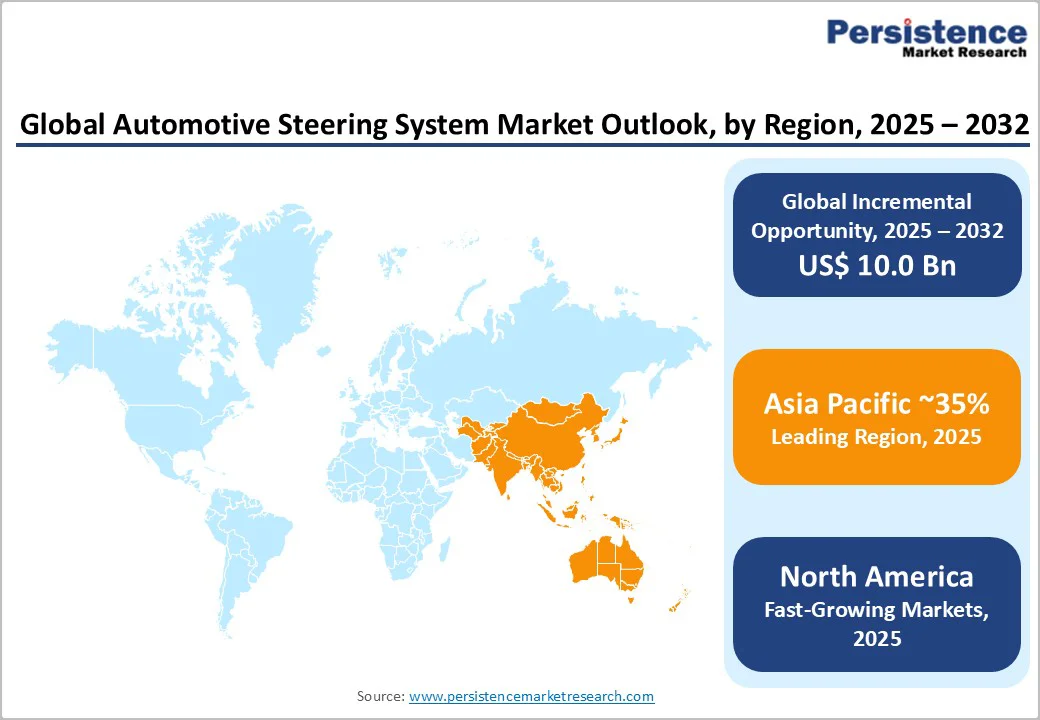

- Regional Leaders: Asia-Pacific dominates with 35% market share and 8.5% CAGR, driven by China’s commanding 45% regional contribution and India’s rapid 10% growth. North America holds a 25% share at 5.2% CAGR, while Europe accounts for 23% share growing at 4.5% CAGR, supported by premium vehicle production and early adoption of advanced steering technologies.

- Strategic Market Developments: Bosch leads with 16% global share, anchored by its EPS technology portfolio, while JTEKT, Nexteer, and ZF remain strong competitors. Steer-by-wire deployments by ZF and Nexteer (2024–2025) enable autonomous driving platforms, representing a US$2.4B opportunity by 2032. Emerging-market EPS penetration creates an additional US$3.7 B opportunity as developing countries transition from hydraulic to electronic systems.

| Key Insights | Details |

|---|---|

|

Automotive Steering System Market Size (2025E) |

US$ 25.7 Bn |

|

Market Value Forecast (2032F) |

US$ 35.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Drivers - Increasing International Focus on Vehicle Safety Standards

The substantial increase in demand for electric vehicles (EVs) emerges as a notable catalyst propelling the expansion of the worldwide automotive steering system market. In the current paradigm shift towards sustainability within the automotive sector, electric vehicles have emerged as a significant contributor to the reduction of carbon emissions and the advancement of environmental awareness. The current paradigm shift is having a substantial influence on the market dynamics of automotive steering systems.

The increasing prevalence of electric vehicles is exerting a multifaceted impact on the automotive steering system market. Electric vehicles, which are distinguished by their use of electric motors as opposed to conventional internal combustion engines, require sophisticated and effective steering systems to complement their unique powertrain properties.

As an alternative to conventional hydraulic systems, electric power steering (EPS) has gained prominence due to its compatibility with the energy-efficient philosophy of electric vehicles. Expanding pedal placement offers improved manoeuvrability, reduced power consumption, and the potential to interface with advanced driver-assistance systems (ADAS), demonstrating the industry's commitment to all-encompassing technological advancement.

Restraints - Complexities in ADAS Integration Process

One significant factor that restricts the growth of the worldwide automotive steering system industry is the ongoing difficulties that arise during the integration process of advanced driver-assistance systems. Although ADAS technologies can significantly improve vehicle safety and decrease accidents, manufacturers face complex challenges in achieving a seamless integration with steering systems.

The requirement for precise coordination between the steering system and numerous ADAS components, including automated emergency braking and lane-keeping assistance, contributes to the complexity. The simultaneous pursuit of optimal integration, reliability, and safety continues to pose a substantial technical challenge.

Difficulties in calibration and compatibility concerns among various ADAS functionalities and steering mechanisms necessitate thorough engineering and testing, which in turn contribute to escalated development expenses and schedules.

Mounting Demand to Address Concerns Around Environmental Sustainability

An area of difficulty for the worldwide automotive steering system industry is the mounting demand to address issues of environmental sustainability. Regarding environmental impact, the automotive industry, including manufacturers of steering systems, is confronted with stringent regulations and increased consumer expectations.

Steering systems, including hydraulic components, frequently necessitate resource-intensive manufacturing processes and utilize materials that contribute to environmental degradation. Achieving sustainability objectives poses a complex and multifaceted dilemma for the market of automotive steering systems.

Opportunity - Increasing Prevalence of Autonomous and Connected Vehicles

The increasing prevalence of autonomous and connected vehicles offers a substantial opportunity for growth in the worldwide automotive steering system market. With the advancement of the automotive sector toward an era of intelligent transportation, steering systems are positioned to have a significant impact on the future driving experience. By incorporating cutting-edge technologies such as artificial intelligence (AI) and sensor-based systems, novel opportunities arise to guide advancements that address the changing requirements of autonomous and connected vehicles.

Autonomous and connected vehicles are dependent on advanced steering systems that surpass conventional capabilities. The introduction of autonomous driving brings about the implementation of steer-by-wire technology, which substitutes electronic signals for the physical connection between the steering wheel and the wheels. This fundamental change not only improves the accuracy and promptness of steering but also corresponds with the overarching objective of developing automobiles that can execute decisions in real-time.

By integrating sensors, cameras, and AI algorithms into steering systems, vehicles are empowered to navigate intricate environments, adapt to dynamic road conditions, and establish communication with other vehicles. This significantly enhances the overall safety and efficiency of connected and autonomous driving.

Category-wise Analysis

Component Insights

Hydraulic pumps command 38.4% component market share in 2025 through continuing deployment in heavy commercial vehicles requiring high steering torque capacity and legacy passenger vehicle production in emerging markets. Commercial vehicle applications including Class 8 trucks, construction equipment, and agricultural machinery requiring steering torque exceeding 2,000 Nm maintain hydraulic power steering prevalence where electric motor sizing constraints limit EPS deployment.

Sensors represent fastest-growing component at approximately 8% CAGR, expanding through ADAS integration requirements, steer-by-wire deployment, and enhanced steering system intelligence demanding torque sensors, angle sensors, and force feedback transducers. Torque sensors measuring driver steering input with 0.1 Nm resolution enable sophisticated EPS control algorithms, ADAS steering intervention, and driver monitoring capabilities essential for Level 2-3 autonomous functionality.

Mechanism Insights

EPS systems command 69.3% mechanism market share through near-universal adoption achieving 85%+ penetration of global new vehicle production driven by fuel efficiency advantages, ADAS integration capability, and regulatory compliance benefits. Column-assist EPS dominating compact and mid-size passenger cars provides cost-effective implementation at $400-600 per unit, while rack-assist and pinion-assist configurations supporting larger vehicles and performance applications command $600-800 pricing reflecting higher torque requirements.

Electrically assisted hydraulic systems represent fastest-growing mechanism at approximately 7-10% CAGR, serving transitional role for heavy-duty applications requiring hydraulic torque capacity combined with electronic control capability and on-demand pump operation. Commercial vehicle applications and performance vehicles maintaining hydraulic actuation while adopting electric pump drive eliminate parasitic engine loads achieving 15% energy savings versus engine-driven pumps.

Vehicle Type Insights

Passenger cars command 64.3% market share through largest production volumes exceeding 70 million units globally and near-universal EPS adoption supporting fuel efficiency, ADAS integration, and consumer comfort expectations. Premium vehicle segment including BMW, Mercedes-Benz, and Audi deploying advanced EPS with variable steering ratios, adaptive damping, and steer-by-wire readiness command 40-60% pricing premiums justifying technology investment.

LCV segment represents fastest-growing vehicle type at approximately 6-9% CAGR, driven by e-commerce expansion, electric commercial vehicle adoption, and fleet management integration creating specialized steering requirements. Electric LCV platforms including delivery vans and last-mile vehicles transitioning to EPS for weight reduction and energy efficiency create incremental demand growing 20% annually.

Regional Market Insights

North America Automotive Steering System Market Trends

North America generates approximately US$7.8 billion market value in 2025 representing 25% global market share growing at 5.2% CAGR through 2032, driven by established automotive manufacturing, regulatory framework supporting fuel efficiency, and autonomous vehicle development ecosystem. The United States dominates regional market with 78% North American share through domestic OEM presence including Ford, General Motors, and Tesla deploying advanced EPS systems, NHTSA safety regulations supporting ADAS integration, and Silicon Valley autonomous vehicle development. Light truck and SUV market dominance commanding 80% U.S. production drives rack-assist and pinion-assist EPS deployment versus column-assist systems typical of compact cars. Canadian automotive sector contributing 10-12% regional share through integrated North American manufacturing.

Europe Steering System Market Trends

Europe represents US$7.2 billion market in 2025 capturing 23% global market share growing at 4.5% CAGR through 2032, characterized by stringest emissions regulations, premium automotive positioning, and steer-by-wire technology leadership. Germany leads European market with 34-40% regional share through automotive manufacturing dominance including BMW, Mercedes-Benz, Volkswagen, and ZF steering system leadership deploying production steer-by-wire systems. Euro 6d emissions standards and CO2 fleet targets mandating EPS adoption across European production create regulatory compliance drivers. United Kingdom, France, Italy, and Spain demonstrating steady growth through automotive manufacturing presence.

Asia Pacific Steering System Market Trends

Asia Pacific represents dominant region at approximately 35% global market share with estimated market value of US$9.5 billion by 2025 growing at 8.5% CAGR through 2032, driven by automotive manufacturing leadership, expanding vehicle production, and EV adoption acceleration. China dominates Asia Pacific with 44-50% regional share through automotive production exceeding 26 million vehicles annually, comprehensive EV manufacturer presence, and domestic steering system suppliers including Shenyang Jinbei, CAAS, and China Automotive Systems. Japan representing 14% regional share maintains technology leadership through JTEKT, NSK, and Showa Corporation steering system manufacturing excellence. India emerging as high-growth market at 10-14% CAGR through expanding automotive production and EPS adoption acceleration.

Competitive Landscape

Prominent entities in the worldwide automotive steering system industry, such as JTEKT Corporation, ZF Friedrichshafen, and Bosch, utilize strategic initiatives to maintain and expand their market dominance. These sector frontrunners are perpetually investing in research and development to provide state-of-the-art steering solutions that address the ever-changing requirements of the automotive industry. As a result, they are constantly at the vanguard of innovation.

Bosch, a market leader, employs a comprehensive strategy to attain the greatest possible market share. The organization implements Artificial Intelligence (AI) strategically into its steering systems with the aim of improving accuracy, promptness, and security. Bosch's market dominance is a result of its dedication to ADAS development, which is in line with the industry's trend toward safer and more automated driving encounters.

Key Industry Developments

- In April 2025, Nexteer Automotive Corporation announced the launch of high-output column-assist electric power steering (HO CEPS), a powerful addition to its steering portfolio that delivers up to 110 Nm of assist torque, compared to the standard 40-95 Nm range. This advancement enables the system to support larger, heavier vehicles such as SUVs and entry-level EVs, while preserving steering precision, efficiency, and cost-effectiveness.

- In September 2022, Hyundai Mobis CO., Ltd launched its advanced dual actuator rear wheel steering system to enhance vehicle maneuverability and driving dynamics. The system delivers a 25% reduction in turning radius, significantly improving urban drivability, particularly in tight spaces and congested parking environments.

Companies Covered in Automotive Steering System Market

- Robert Bosch GmbH

- JTEKT Corporation

- ZF Friedrichshafen AG

- Nexteer Automotive

- NSK Ltd.

- Thyssenkrupp AG

- Mando Corporation

- Showa Corporation

- Hyundai Mobis Co., Ltd.

- Other Market Players

Frequently Asked Questions

The Automotive Steering System market is estimated to be valued at US$ 25.7 Bn in 2025.

The primary demand driver for the Automotive Steering System market is the rapid adoption of Electronic Power Steering (EPS) systems, supported by vehicle electrification, advanced safety requirements, and the growing integration of ADAS and autonomous driving features.

In 2025, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Automotive Steering System market.

Among the Component Type, Hydraulic Pump hold the highest preference, capturing beyond 38.4% of the market revenue share in 2025, surpassing other Component Type.

The key players in the Automotive Steering System market are Robert Bosch GmbH, JTEKT Corporation, ZF Friedrichshafen AG and Nexteer Automotive