- Home Appliances

- Air Purification Market

Air Purification Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Air Purification Market by Technology (Activated Carbon Filtration, High-Efficiency Particulate Air, Ionizer Purifiers, Ultraviolet Germicidal Irradiation, Others), Application (Residential, Commercial, Industrial), Regional Analysis by 2026 - 2033

Air Purification Market Size and Trend Analysis

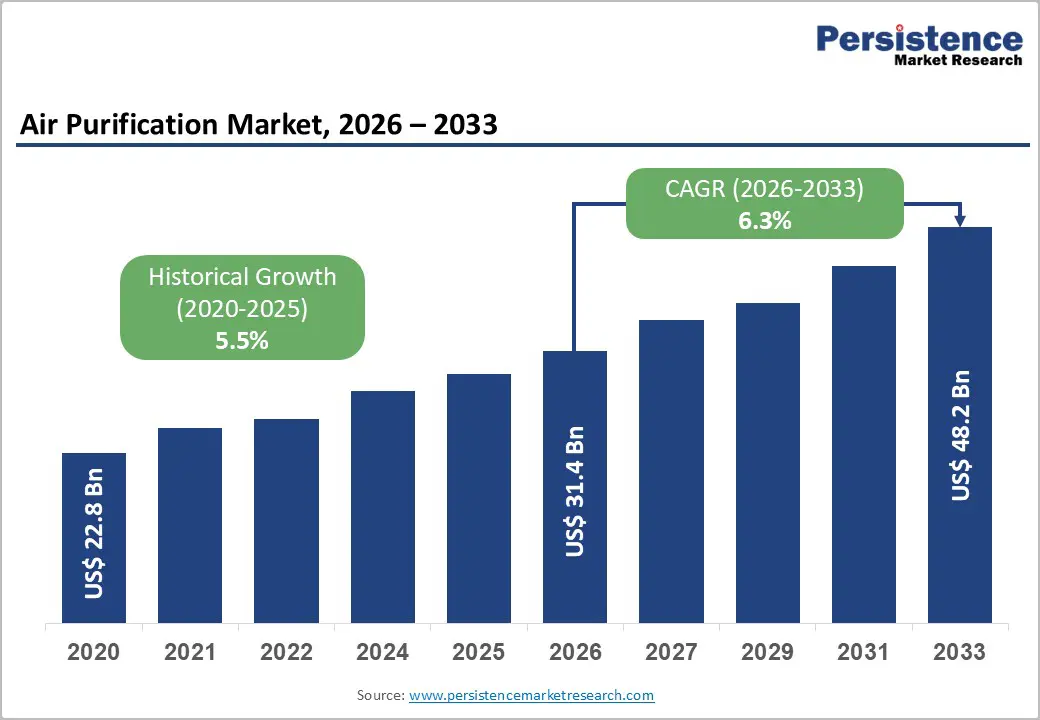

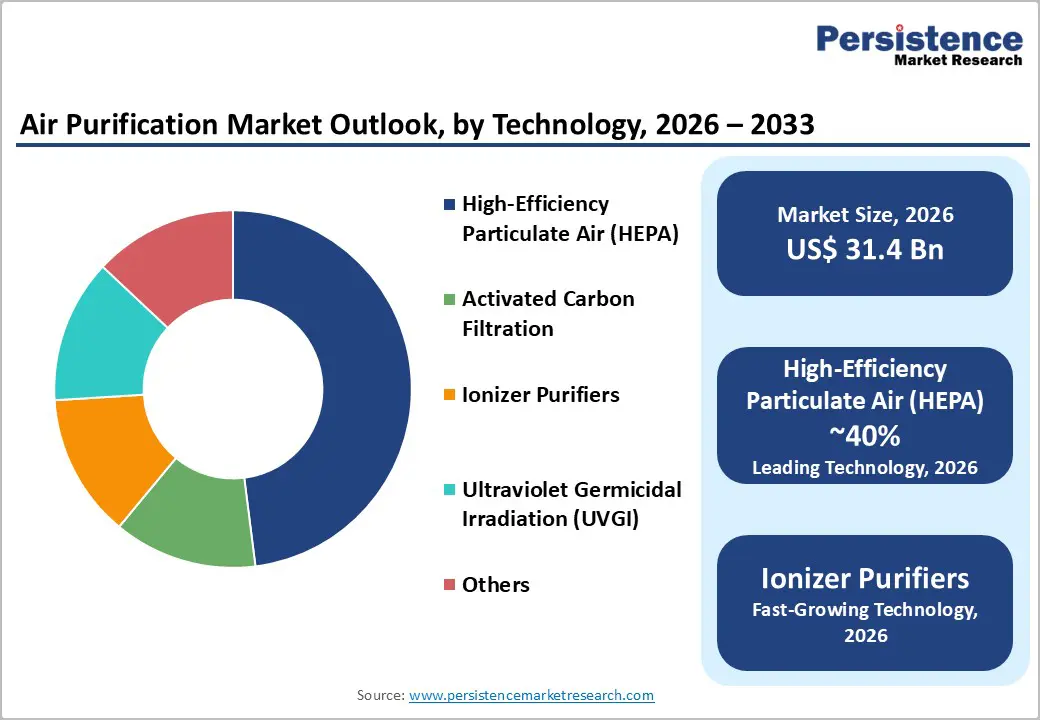

The global air purification market size is likely to be valued at US$31.4 billion in 2026 and is projected to reach US$48.2 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

Rising awareness about indoor air quality represents a critical growth driver as people worldwide spend approximately 90% of their time indoors, where pollutant concentrations are often 2 to 5 times higher than outdoor levels, according to the U.S. Environmental Protection Agency. The World Health Organization reports that combined ambient and household air pollution contributes to 6.7 million premature deaths annually, with household air pollution alone responsible for 3.2 million deaths in 2020, underscoring the urgent need for effective air purification solutions across residential, commercial, and industrial settings.

Key Market highlights

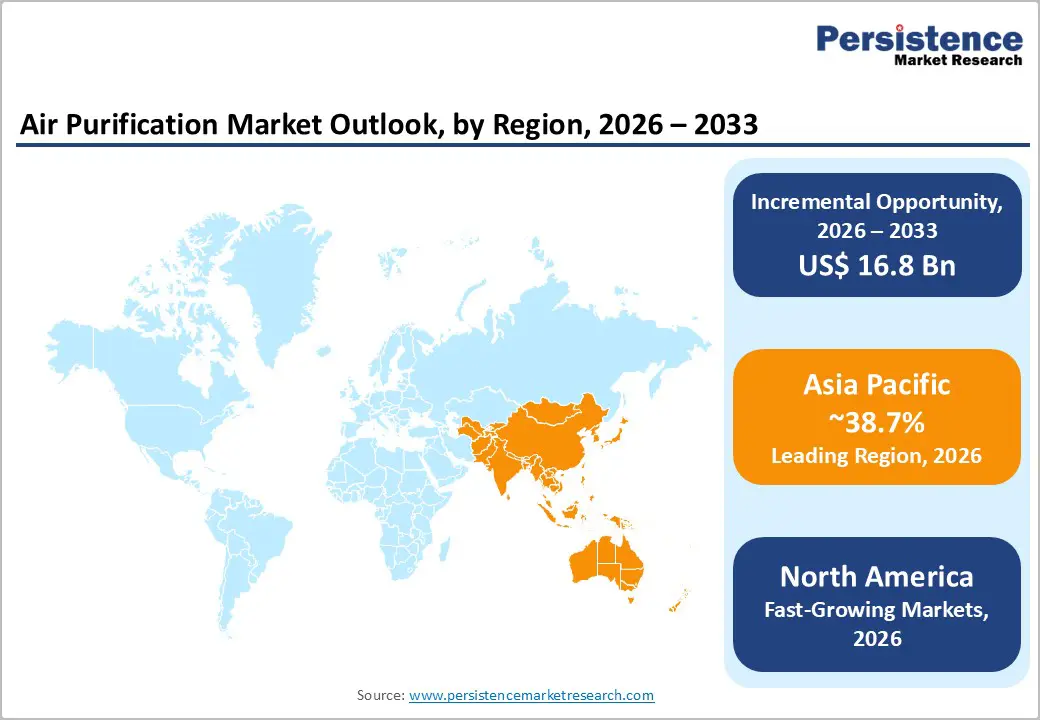

- Regional Leader: Asia Pacific dominates the market with 38.7% share, driven by severe urban air pollution in China and India, rapidly expanding middle-class populations, increasing health awareness, progressive regulatory standards like China's GB 36893-2024, and strong manufacturing capabilities serving both domestic and export markets.

- Fastest Growing Region: North America represents the fastest growing region in the air purification market through stringent EPA and OSHA regulatory frameworks, high consumer awareness about indoor air quality, advanced innovation ecosystems, and strong adoption across residential, commercial, and industrial segments supported by established distribution infrastructure.

- Leading Segment: High-Efficiency Particulate Air (HEPA) technology commands approximately 48% market share due to proven 99.97% particle removal efficiency, widespread consumer trust, and regulatory recognition.

- Fastest Growing Segment: The commercial application segment shows accelerated growth as organizations implement corporate wellness programs, comply with ESG mandates, and meet occupational safety requirements.

- Key Market Opportunity: Smart purifiers present a key opportunity, integrating AI for urban demand.

| Key Insights | Details |

|---|---|

| Air Purifier Market Size (2026E) | US$31.4 Bn |

| Market Value Forecast (2033F) | US$48.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.3% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics

Drivers - Rising Urbanization and Deteriorating Air Quality

The primary catalyst for the Air Purification Market is the rapid rate of global urbanization, which has led to significantly higher concentrations of particulate matter (PM2.5 and PM10) in metropolitan areas. The World Health Organization emphasizes that household air pollution exposure leads to noncommunicable diseases, including stroke, ischemic heart disease, chronic obstructive pulmonary disease, and lung cancer, with 44% of pneumonia deaths in children under 5 years attributed to inhaling particulate matter from polluted indoor air.

The American Lung Association confirms that HEPA filters can remove 99.97% of airborne particles, providing substantial relief to allergy sufferers and those with respiratory sensitivities. Urban areas in Asia and Europe frequently surpass guidelines, boosting HEPA and multi-stage systems for PM2.5 capture. This trend aligns with the Air Purifier Market dynamics, where pollution spikes during wildfires and industrial emissions heighten consumer urgency for continuous purification. Governments reinforce this through standards like China's GB/T 18801-2022, compelling verifiable performance.

Technological Advancements and Integration with Smart Systems

Innovation in filtration technologies and smart connectivity is driving market adoption across various consumer segments. Modern air purifiers often combine High-Efficiency Particulate Air (HEPA) filters with activated carbon, Ultraviolet Germicidal Irradiation (UVGI), and ionization to tackle pollutants like PM2.5, PM10, volatile organic compounds, bacteria, mold spores, and viruses. Hybrid filtration systems that merge HEPA and activated carbon provide effective solutions for particulate and chemical emissions in residential and industrial settings.

Blueair's HEPASilent™ dual-filtration technology captures 99.97% of particles down to 0.1 microns, offering low noise and energy consumption. Its IoT capabilities, real-time air quality monitoring, smart sensors, and mobile app connectivity enhance user experience and efficiency, appealing to tech-savvy consumers. Additionally, the integration of air purification with HVAC systems presents growth opportunities, as companies like Dyson, Honeywell, and Daikin develop advanced multi-stage purification systems.

Market Restraints

High Initial Investment and Recurring Maintenance Costs

The substantial upfront cost of advanced air purification systems, particularly those with HEPA filtration, UV-C sterilization, and smart connectivity features, creates a significant barrier to adoption among price-sensitive consumer segments. High-quality purifiers, especially those equipped with HEPA and Activated Carbon filters, command a premium price point that limits penetration in price-sensitive developing markets.

Furthermore, the recurring cost of filter replacements, which manufacturers recommend every 6 to 12 months, creates a total cost of ownership that discourages lower-income households. This economic friction slows down mass market adoption, particularly in regions where air purification is still considered a discretionary expense rather than an essential utility.

Competition from Integrated HVAC Systems

The rising preference for integrated heating, ventilation, and air conditioning systems that incorporate air purification capabilities poses a competitive challenge to standalone air purifier manufacturers. Many modern central air systems now include HEPA filters or advanced filtration technologies that effectively remove dust, pollen, and allergens, offering consumers a dual-function solution for cooling and air purification. These integrated systems appeal to property owners and facility managers because they provide convenience, potentially lower overall costs compared to purchasing separate devices, improved energy efficiency, and less obtrusive installation in living and working spaces.

The commercial and industrial segments particularly favor such comprehensive HVAC solutions that can maintain consistent air quality across large facilities while meeting OSHA and EPA compliance requirements through validated filter performance and continuous air quality monitoring.

Opportunity - Integration of Smart Technology and IoT Ecosystems

Smart air purifiers with Internet of Things (IoT) capabilities, app controls, and real-time air quality index (AQI) monitoring are increasingly appealing to tech-savvy consumers. Coway's Airmega series uses artificial intelligence (AI) for automatic adjustments during pollution spikes and integrates with Google Home. This feature attracts urban users concerned about volatile organic compounds (VOCs) and particulates. ENERGY STAR efficiency encourages adoption, and hybrid models that combine air purification and humidification are gaining popularity.

A key growth area is the integration of air purifiers into smart home ecosystems. By incorporating IoT features, manufacturers can allow users to monitor indoor air quality (IAQ) via smartphone apps. Devices that adjust fan speeds based on real-time pollution data or work with voice assistants are in high demand. This technology not only enhances convenience but also enables predictive maintenance, notifying users when filters need changing, thus optimizing performance and creating recurring revenue for companies.

Commercial and Institutional Segment Acceleration

The commercial and industrial application segments offer significant untapped potential as organizations prioritize employee wellness, regulatory compliance, and environmental sustainability initiatives. Corporate offices, information technology parks, hospitals, educational institutions, hotels, and shopping malls increasingly install centralized air purification systems as part of workplace safety programs and Environmental, Social, and Governance (ESG) mandates.

Pharmaceutical, semiconductor, and biotechnology manufacturing facilities require specialized HEPA and ULPA filtration systems to maintain contamination-free production environments, achieving ISO cleanroom classifications. The air purifier market is connected to broader trends as awareness about UV Disinfection Equipment grows, particularly in healthcare settings where pathogen control remains critical for infection prevention and patient safety. Air purification system providers can develop tailored solutions addressing specific industry requirements, offer comprehensive maintenance contracts, and leverage data analytics capabilities to demonstrate measurable improvements in indoor air quality metrics and employee health outcomes.

Category-wise Analysis

Technology Insights

The High-Efficiency Particulate Air (HEPA) technology segment dominates the market, accounting for a market share of approximately 48% due to its proven efficacy and regulatory endorsement. This segment leads because HEPA filters are certified to trap 99.97% of particles as small as 0.3 microns, making them the gold standard for removing dust, pollen, mould, and bacteria. The rising incidence of respiratory disorders and airborne infections has increased demand for dependable purification solutions, with HEPA filters consistently selected for their reliable performance over extended operational periods.

Manufacturers increasingly integrate HEPA filtration with complementary technologies, including activated carbon filters for odor and chemical vapor removal and UV sterilization modules for comprehensive air treatment, enhancing overall system effectiveness. The development of hybrid filters combining HEPA and activated carbon addresses both particulate matter and chemical emissions simultaneously, gaining traction in industrial settings, including pharmaceuticals, chemical manufacturing, and laboratories, where multiple contaminant types require management.

Application Insights

The residential application segment leads the air purification market with an estimated 43% share, driven by health consciousness and awareness of indoor air quality's impact on well-being. The U.S. Environmental Protection Agency reports that indoor pollutant levels can be 2 to 5 times higher than outdoor air, prompting homeowners to seek solutions. The rise of allergies, asthma, and respiratory conditions, particularly among children and the elderly, influences purchasing decisions. The World Health Organization indicates that improving indoor air quality can reduce asthma symptoms by up to 40%.

This segment benefits from innovations such as compact designs, quiet operation, smart connectivity, and energy-efficient models that meet Energy Star standards. Manufacturers like Xiaomi, Eureka Forbes, Coway, and Sharp provide affordable options for middle-income consumers, expanding their reach beyond premium brands like Dyson, Philips, and Honeywell.

Regional Insights

North America Air Purifier Market Trends

North America remains a mature and technically advanced region, characterized by high adoption rates of smart and connected devices. The U.S. EPA and OSHA enforce indoor air quality standards to reduce health risks from airborne pollutants like PM2.5, VOCs, and bioaerosols, promoting adoption in residential and commercial spaces. Regulatory requirements are evolving, with agencies enforcing stricter compliance for industrial, commercial, and healthcare facilities through validated filter performance and air quality monitoring.

Furthermore, the region's innovation ecosystem is robust, with frequent launches of medical-grade purifiers catering to the substantial population suffering from seasonal allergies. The emphasis on HEPA-grade filtration to combat allergens ensures steady replacement demand.

Europe Air Purifier Market Trends

The Europe market is shaped by stringent environmental sustainability goals and the European Green Deal, which influences product efficiency standards. In December 2024, the EU introduced new pollution rules under the revised Ambient Air Quality Directive, cutting the allowed annual limit value for fine particulate matter PM2.5 by more than half and updating standards for twelve air pollutants, including PM10, nitrogen dioxide, sulfur dioxide, ozone, and benzene, with compliance required by 2030. These regulatory changes compel commercial facilities, industrial operations, and public institutions to invest in advanced air purification infrastructure, ensuring adherence to health-protective air quality standards.

Germany, the U.K., France, and Spain lead regional market performance through combinations of strong environmental consciousness, well-developed healthcare systems prioritizing preventive health measures, and supportive government policies promoting clean air technologies.

Asia Pacific Air Purifier Market Trends

Asia Pacific dominates the air purification market, with 38.7% of the global market share, propelled by severe urban air pollution, rapid industrialization, expanding middle-class populations, and increasing health awareness. China implements progressive regulatory measures including Standard GB 36893-2024 establishing minimum energy efficiency values and performance grades for air purifiers, with mandatory compliance required for products manufactured or imported after October 1, 2025. This regulatory framework drives market standardization and encourages manufacturers to develop energy-efficient models meeting stringent government requirements while supporting the country's environmental sustainability objectives.

India presents a significant growth opportunity, with major cities like Delhi, Mumbai, Bengaluru, and Kolkata driving around 75% of demand. Delhi NCR alone accounts for 40% of this due to pollution from vehicles, industry, construction, and crop burning. In response to the worsening air quality, Dyson launched the Purifier Hot plus Cool Gen 1 in India in November 2024.

Competitive Landscape

The Air Purification Market is moderately fragmented, characterized by a mix of established global electronics giants and specialized filtration companies. The market structure is evolving towards consolidation as major players like Honeywell and Daikin acquire smaller, niche innovators to expand their technology portfolios. Key differentiators for market leaders include proprietary filtration technologies, energy efficiency ratings, and quiet operation modes. Emerging business models are shifting towards "Air as a Service," where commercial clients pay for guaranteed air quality metrics rather than just hardware, ensuring long-term service contracts. Research and development trends are heavily focused on increasing the Clean Air Delivery Rate (CADR) while minimizing noise and energy consumption.

Key Market Developments

- February 2025: Blueair announced that its new Classic Pro CP7i model achieved the "Asthma & Allergy Friendly" certification, reinforcing its position in the medical-grade segment.

- January 2025: Coway Co., Ltd. was named a CES Innovation Awards Honoree for its "Smart Self-cleaning Air Purifier," highlighting advancements in automated maintenance technology.

- September 2024: Daikin Industries Ltd. signed a memorandum to acquire land for a new manufacturing plant in Southern India to meet the surging demand for air handling units in the region.

Top Companies in the Air Purifier Market

- Honeywell International Inc. (U.S.): A dominant player leveraging its industrial engineering heritage to produce robust HEPA purifiers. Honeywell is widely trusted in the North American market for its "Doctor's Choice" branding and high CADR ratings, making it a leader in the premium residential segment.

- Daikin Industries Ltd. (Japan): A global leader in HVAC and air purification, Daikin distinguishes itself with its patented Streamer technology that decomposes pollutants. The company holds a massive influence in the Asian market and is aggressively expanding its manufacturing footprint in India and Southeast Asia.

- Koninklijke Philips N.V. (Netherlands): Philips focuses on the intersection of healthcare and consumer lifestyle, offering smart purifiers with app-connectivity. Their focus on sensing technology and real-time feedback appeals to health-conscious urban consumers in Europe and Asia, positioning them as a top choice for allergy management.

Companies Covered in Air Purification Market

- Honeywell International Inc.

- Daikin Industries Ltd.

- Koninklijke Philips N.V.

- Camfil

- Donaldson Company, Inc.

- Sumitomo Heavy Industries, Ltd.

- FLSmidth

- Blueair

- Sharp Electronics Corporation

- LG Electronics

- Coway Co., Ltd.

Frequently Asked Questions

The market is projected to reach US$48.2 Bn by 2033, growing at a robust pace due to increasing health awareness.

Deteriorating air quality in urban areas, combined with rising consumer awareness regarding respiratory health issues like asthma.

The HEPA (High-Efficiency Particulate Air) technology segment leads the market, with 48% market share, due to its superior ability to trap 99.97% of airborne particles without harmful by-products.

Asia Pacific is the leading region, driven by severe pollution challenges in countries like China and India and a rapidly expanding middle class.

Integrating IoT and smart features into purifiers, as well as developing wearable air purification devices, presents a significant growth opportunity.

Key players include Honeywell International Inc., Daikin Industries Ltd., Koninklijke Philips N.V., Blueair, and Coway Co., Ltd., among others.