- Processed Food

- Non-dairy Cheese Market

Non-dairy Cheese Market Size, Share, and Growth Forecast, 2026 - 2033

Non-dairy Cheese Market by Product Type (Mozzarella, Parmesan, Cheddar, Others), Source (Soy Milk, Others), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others), and Regional Analysis for 2026 – 2033

Non-dairy Cheese Market Size and Trends Analysis

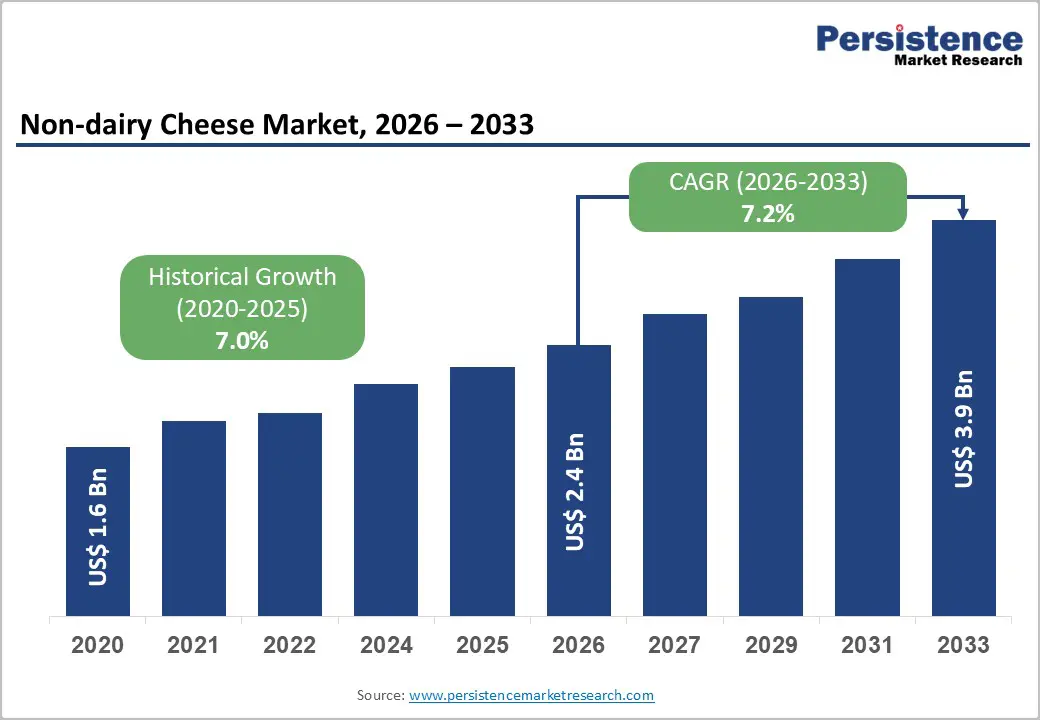

The global non-dairy cheese market size is likely to be valued at US$2.4 billion in 2026, and is expected to reach US$3.9 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of vegan and flexitarian diets, rising lactose intolerance and dairy allergy awareness, and advancements in plant-based formulations delivering improved melt, stretch and flavor profiles.

The growing demand for sustainable, allergen-free non-dairy cheese, particularly mozzarella and cheddar made from coconut milk, is driving adoption across food applications. Advances in fermentation-based textures and clean-label ingredients are further boosting uptake by offering dairy-like sensory experiences. The increasing recognition of non-dairy cheese as critical to inclusive, environmentally friendly food options in emerging health-conscious markets remains a major driver of market growth.

Key Industry Highlights:

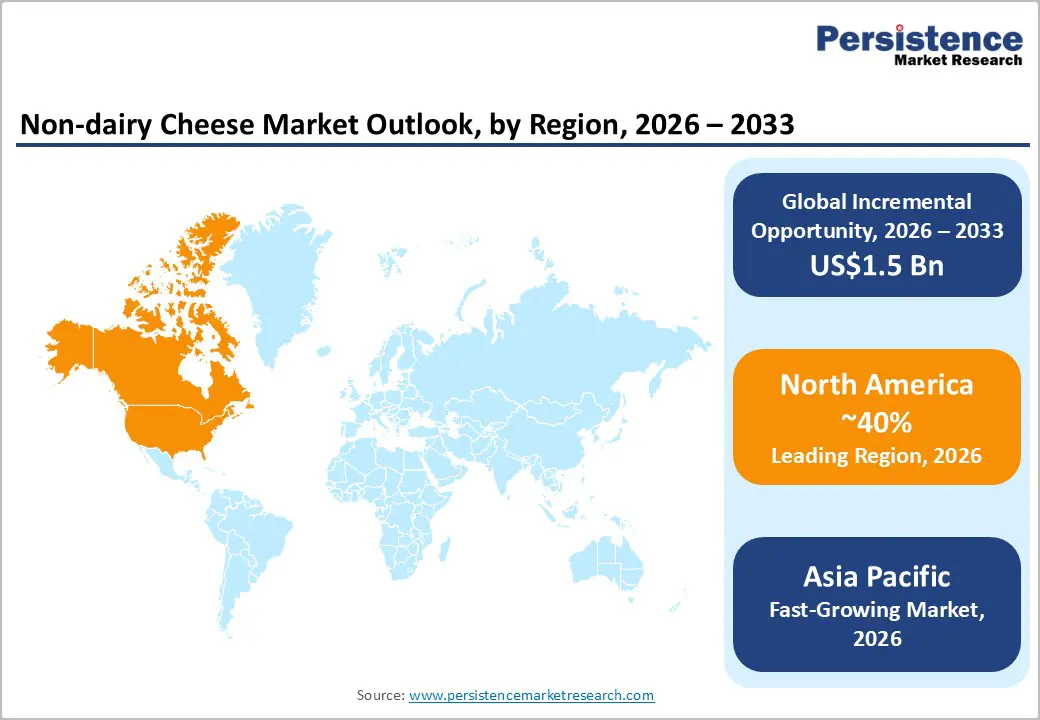

- Leading Region: North America, to account for a 40% market share in 2026, driven by high vegan adoption, strong retail presence, and premium demand in the U.S.

- Fastest-growing Region: Asia Pacific, to be fueled by rising lactose intolerance, expanding middle-class, and growing investments in plant-based foods in China and India.

- Dominant Product Type: Mozzarella, to hold approximately 35% of the market share, as it dominates pizza and Italian cuisine applications.

- Leading Source: Coconut milk, to account for over 40% of the market revenue, due to its superior meltability and creaminess.

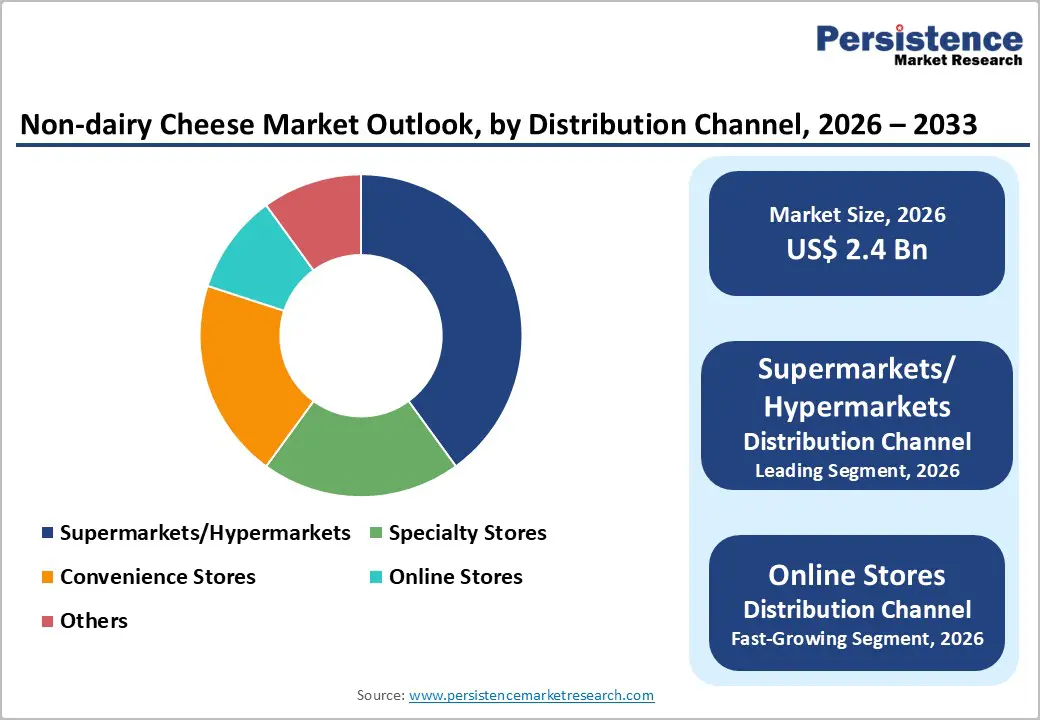

- Leading Distribution Channel: Supermarkets/Hypermarkets, to contribute nearly 35% of the market revenue, due to broad accessibility and in-store promotions.

| Report Attribute | Details |

|---|---|

|

Non-dairy Cheese Market Size (2026E) |

US$2.4 Bn |

|

Market Value Forecast (2033F) |

US$3.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Vegan & Flexitarian Diets and Allergen-Free Cheese Alternatives

The rising prevalence of vegan and flexitarian diets is significantly accelerating the demand for allergen-free cheese alternatives, reshaping the global food and beverage landscape. Consumers are increasingly shifting away from traditional dairy products due to health concerns, ethical considerations, and environmental awareness. Vegan consumers seek completely plant-based options, while flexitarians aim to reduce animal-derived food intake without fully eliminating it, creating a large and diverse customer base for dairy-free cheese.

Allergen awareness is also playing a critical role in market growth. Lactose intolerance, milk protein allergies, and soy or nut sensitivities are encouraging manufacturers to develop allergen-free cheese alternatives made from ingredients such as oats, rice, chickpeas, peas, and coconut, formulated without common allergens. These products offer safer options for sensitive consumers while maintaining taste, texture, and melting performance. Food innovation has further strengthened the adoption. Advances in fermentation, protein extraction, and emulsification technologies are enabling brands to create plant-based cheeses that closely replicate the flavor and functionality of traditional cheese.

High Production Costs and Sensory Performance Gaps

High production costs and sensory performance gaps remain major challenges restraining the growth of the allergen-free and plant-based cheese alternatives market. Developing dairy-free cheese that matches the taste, texture, and melting behavior of traditional cheese requires complex formulations, advanced processing technologies, and specialized ingredients. Proteins extracted from peas, chickpeas, oats, or other plants often require extensive purification and modification to achieve the desired functional properties, significantly increasing manufacturing costs. Allergen-free formulations must avoid common allergens such as dairy, soy, and nuts, which limits ingredient choices and increases R&D and sourcing costs.

Sensory performance is another critical barrier. Replicating the creamy mouthfeel, stretch, and rich flavor of dairy cheese is technically difficult without casein and milk fat, which naturally provide structure and taste. Many plant-based cheeses still struggle with issues such as poor meltability, graininess, and off-flavors, which can reduce consumer satisfaction and repeat purchases. To close this gap, manufacturers must invest heavily in fermentation, enzyme technology, and flavor science, further raising development costs.

Growing Vegan and Flexitarian Diets Boost Demand

The growing adoption of vegan and flexitarian diets is one of the strongest demand drivers for the non-dairy cheese market. Consumers are increasingly reducing or eliminating animal-based foods due to health concerns, ethical considerations related to animal welfare, and environmental awareness. Vegan consumers require completely dairy-free alternatives, while flexitarians seek to limit dairy intake without giving up familiar foods such as pizza, burgers, and sandwiches. This creates a large and diverse customer base that actively looks for plant-based cheese products that fit into everyday meals.

Health awareness is playing a major role in this shift. Many consumers associate plant-based diets with lower cholesterol, easier digestion, and improved gut health, which encourages them to replace traditional cheese with non-dairy options. The rise in lactose intolerance and milk protein sensitivity makes dairy-free cheese a practical solution for people who want to enjoy cheese without discomfort or allergic reactions. Foodservice operators and retailers are responding quickly by expanding vegan menus and stocking a wider range of plant-based cheeses, thereby increasing visibility and accessibility.

Category-wise Analysis

Product Type Insights

Mozzarella is expected to dominate the market, accounting for approximately 35% of the market share in 2026. Its dominance is driven by pizza category dominance, melt performance improvements, and widespread Italian cuisine usage, making it preferred for food service. Mozzarella provides stretch, ensures browning, and contributes to versatility, making it suitable for large-scale QSR campaigns. Daiya Foods Inc. focuses on plant-based mozzarella shreds known for their meltability on pizza and other dishes, helping food-service operators offer dairy-free alternatives without compromising sensory quality. Violife Foods also offers a range of vegan mozzarella products used by restaurants and quick-service outlets that cater to vegan or lactose-free preferences.

Cheddar is likely to be the fastest-growing segment, due to its expanding use in snacking, sandwiches, and burgers. Its sharp profile makes it ideal for targeted flavor, reducing dairy dependency. Continuous innovations in aging and shredding are further strengthening its appeal, driving rapid adoption across North America and Europe, where demand for versatile slices is accelerating. Violife launched a new aged cheddar-style vegan cheese, expanding its premium lineup and shelf presence across key retail channels. This product targets consumers seeking plant-based cheddar for sandwiches, burgers, and snacking, where its sharper flavor profile appeals to mainstream tastes and reduces dependency on traditional dairy.

Source Insights

Coconut milk is expected to lead the market, accounting for approximately 40% of the market in 2026, driven by its superior creaminess, melt performance, and neutral flavor base, making it preferred for premium products. Their dominance persists as the demand for diverse textures increases. The growing popularity of clean-label almond milk and expanded soy campaigns emphasizes the shift towards a wider range of alternatives. U.K.-based plant-based company Cocos Organic has introduced a coconut-milk-based soft cheese alternative made with 92% coconut milk and fermented with live vegan cultures. This product offers a creamy texture and improved meltability, making it ideal for sandwiches, baked dishes, and everyday use.

Almond milk is likely to be the fastest-growing segment, driven by strong momentum in nutty flavors and increasing inclusion in clean-label products. The growing shift toward allergen-friendly platforms, along with improved perception, is accelerating adoption. Advancements in blending and the continued progress of high-protein entering consumer trials drive market growth. Armored Fresh Inc. developed a range of almond milk–based plant-based cheeses that include cheese cubes, spreadable cheeses, slices, and shredded formats made from almond milk and almond protein. These products were introduced into the U.S. market via retail stores and online platforms, expanding consumer access beyond niche health food shops.

Distribution Channel Insights

Supermarkets and hypermarkets are expected to dominate the market, accounting for nearly 35% of revenue by 2026, owing to their role as central hubs for impulse purchases, large-scale retail programs, and the management of a variety of non-dairy cheese options that benefit from in-store sampling. Their wide reach, trained staff, and the ability to manage high volumes or promotional blends drive greater consumption. Supermarkets are also at the forefront of mozzarella rollouts and running trials for emerging cheddar varieties. Brands such as Cathedral City Plant-Based Cheese and Violife vegan cheeses are available in major supermarkets, including Sainsbury’s, Tesco, ASDA, and Waitrose, providing consumers with easy access to both familiar and innovative non-dairy options.

Online stores represent the fastest-growing segment, driven by their strong digital presence and expanding role in subscription models. They offer a convenient, quick, and accessible variety, attracting buyers who prefer detailed reviews and home delivery settings. Increased outreach programs, e-commerce focus, and wider availability of routine and premium cheese further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Vegan Dukan sells a wide range of plant-based cheese products directly to consumers through its e-commerce platform. It offers customers the ability to select products, choose subscription plans, and receive regular doorstep delivery of vegan cheese such as Plan B Mozzarella, Parmesan, and Cheddar slices, making shopping convenient and accessible across urban and semi-urban areas.

Regional Insights

North America Non-dairy Cheese Market Trends

North America is expected to lead the market, accounting for nearly 40% share in 2026, driven by the region’s high rate of vegan adoption, a strong food innovation ecosystem, and high public awareness of allergen-free benefits. Distribution systems in the U.S. and Canada provide extensive support for cheese programs, ensuring wide accessibility of non-dairy cheese across mozzarella, cheddar, and pizza populations. Increasing demand for coconut-based, convenient, and easy-to-melt forms is further accelerating adoption, as these formats improve taste and reduce barriers associated with dairy.

Innovation in non-dairy cheese technology, including stable fermentation, improved meltability, and targeted flavor enhancement, is attracting significant investment from both the public and private sectors. Government initiatives and sustainability campaigns continue to promote use against lactose risks, environmental concerns, and emerging dietary threats, creating sustained market demand. The growing focus on cheddar grades and specialty uses, particularly for snacking and others, is expanding the target applications for non-dairy cheese.

Europe Non-dairy Cheese Market Trends

Europe is likely to witness steady growth, driven by the increasing awareness of plant-based benefits, strong regulatory systems, and government-led sustainability programs. Countries such as Germany, France, and the U.K. have well-established food frameworks that support routine non-dairy use and encourage adoption of innovative cheese delivery methods, including non-dairy cheese. These sustainable formulations are particularly appealing to pizza consumers, regulation-conscious consumers, and flexitarian users, thereby improving acceptance and coverage rates.

Technological advancements in non-dairy cheese development, such as enhanced meltability, application-specific delivery, and improved clean-label grades, are further enhancing market potential. European authorities are increasingly supporting research and trials on cheese to address both routine and specialized needs, thereby strengthening market confidence. The growing emphasis on convenient, allergen-free options aligns with the region’s focus on preventive health and on reducing dairy intake. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in fermentation and novel variants to increase efficacy.

Asia Pacific Non-dairy Cheese Market Trends

Asia Pacific is likely to be the fastest-growing region, driven by rising health awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting cheese campaigns to address lactose growth and emerging vegan needs. Non-dairy cheese is particularly attractive in these regions due to its scalable administration, ease of use, and suitability for large-scale food drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-melt non-dairy cheese that withstands challenging climatic conditions and minimizes flavor dependence. These innovations are critical for reaching remote facilities and improving overall taste coverage. Growing demand for mozzarella, cheddar, and pizza applications is contributing to market expansion. Public-private partnerships, increased plant-based expenditure, and rising investment in cheese research and manufacturing capacity are further accelerating growth. The convenience of cheese delivery, combined with improved texture and reduced risk of allergies, positions non-dairy cheese as a preferred choice.

Competitive Landscape

The global non-dairy cheese market is competitive, with established vegan brands and dairy giants entering the plant-based market. In North America and Europe, Daiya Foods and Violife lead through strong R&D, distribution networks, and retail ties, bolstered by innovative mozzarella and cheddar programs. In Asia Pacific, local brands advance with localized solutions, enhancing accessibility. Fermentation delivery boosts melt, cuts dairy risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Clean-label formulations address perception issues, aiding penetration into mainstream markets.

Key Industry Developments

- In January 2025, RIND launched ALPINE SVVISS, a cashew-based artisan vegan cheese in the U.S. The product’s introduction at major food shows coincided with digital sales support via online specialty retailers and direct-to-consumer channels, reflecting strong e-commerce uptake.

Companies Covered in Non-dairy Cheese Market

- Daiya Foods

- Miyoko's Creamery

- Violife

- Follow Your Heart

- Kite Hill

- Treeline

- Tofutti

- Bel Group

- Good Planet Foods

- Saputo Inc.

- Bega Cheese

- Parmela Creamery

Frequently Asked Questions

The global non-dairy cheese market is projected to reach US$2.4 billion in 2026.

The rising prevalence of vegan and flexitarian diets and lactose intolerance awareness are the key drivers.

The non-dairy cheese market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Rapid expansion of e-commerce and direct-to-consumer platforms is creating a major growth opportunity for non-dairy cheese brands to reach wider audiences, offer subscriptions, and launch innovative products faster with lower distribution barriers.