- Food Ingredients & Additives

- Dairy Replacer Market

Dairy Replacer Market Size, Share, and Growth Forecast, 2026 - 2033

Dairy Replacer Market by Nature (Organic, Conventional), End-User (Food & Beverages, Infant Nutrition, Food Service Industry, Households), Source (Plant-Based, Oat-Based), and Regional Analysis for 2026-2033

Dairy Replacer Market Share and Trends Analysis

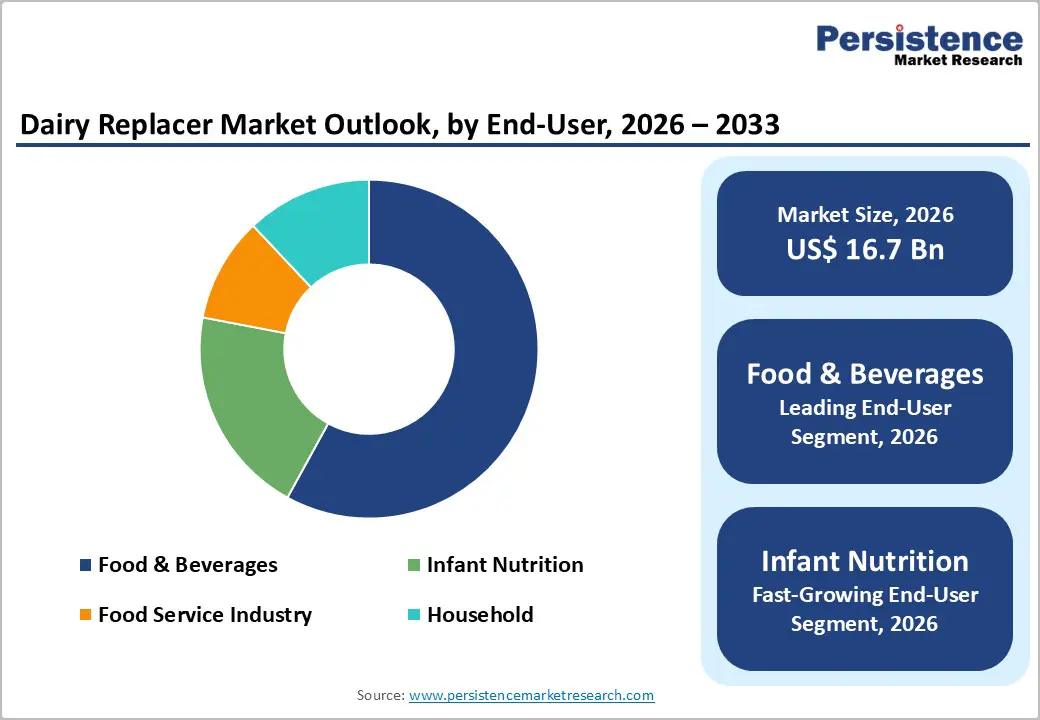

The global dairy replacer market size is likely to be valued at US$ 16.7 billion in 2026, and is projected to reach US$ 29.3 billion by 2033, growing at a CAGR of 8.6% during the forecast period 2026−2033. Demand is increasing as consumers are adopting plant-based nutrition alternatives across beverages, infant nutrition, bakery, and animal feed applications. Rising prevalence of lactose intolerance is influencing dietary preferences, particularly in Asia Pacific and parts of Africa. Environmental sustainability concerns are shaping purchasing decisions, as consumers are evaluating carbon footprint and water usage associated with traditional dairy production. Higher disposable income levels in emerging economies are enabling experimentation with value-added nutritional products.

Companies are responding by expanding product portfolios that replicate taste, texture, and nutritional functionality of conventional dairy. Technological advancement in formulation science is strengthening product performance and improving protein digestibility and micronutrient fortification. Manufacturers are investing in enzyme processing, fermentation techniques, and protein isolation methods to enhance sensory quality and shelf stability. Distribution networks are expanding through organized retail, food service chains, and electronic commerce platforms, and this expansion is improving accessibility across urban and semi-urban markets. Regulatory authorities are establishing clearer labeling guidelines for plant-based alternatives, which is reducing compliance ambiguity. Strategic partnerships between ingredient suppliers and food producers are accelerating product innovation cycles.

Key Industry Highlights

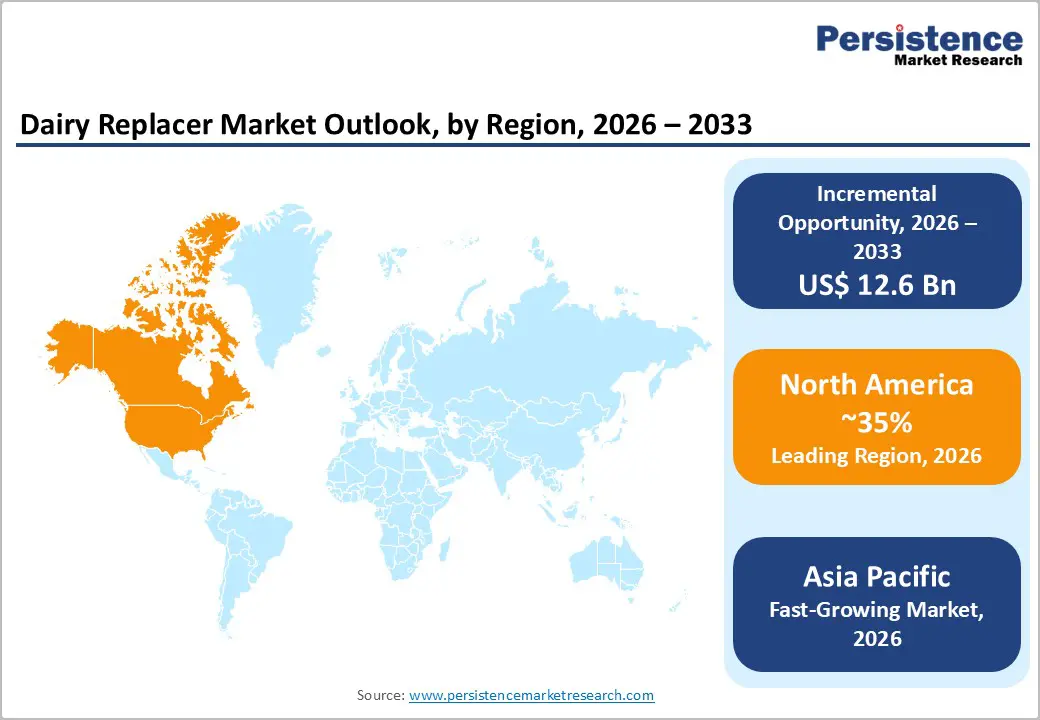

- Dominant Region: North America is expected to hold around 35% of the market share in 2026, on the back of an established plant-based food culture and widespread consumer awareness.

- Fastest-growing Market: The Asia Pacific market is anticipated to emerge as the fastest-growing through 2033, fueled by government initiatives promoting plant-based protein development and food security diversification.

- Source Dynamics: Plant-based sources are slated to dominate with an estimated 2026 share exceeding 62%, while oat-based sources are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- End-User Leadership: Food & beverages are poised to hold an estimated 58% revenue share in 2026, with infant nutrition expected to be the fastest-growing segment from 2026 to 2033.

- July 2025: Premier Protein introduced a new line of Almondmilk non-dairy protein shakes made with real almond milk, each offering 20 g of plant-based protein, and available in Chocolate, Vanilla, and Coffee flavors.

| Key Insights | Details |

|---|---|

| Dairy Replacer Market Size (2026E) | US$ 55.2 Bn |

| Market Value Forecast (2033F) | US$ 70.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Lactose Intolerance and Dairy Allergies

Growing prevalence of lactose intolerance and dairy allergies are affecting populations across both developed and emerging markets, and this trend is increasing demand for dairy replacement products. Consumers who are experiencing digestive discomfort from conventional dairy are actively seeking alternatives that deliver comparable protein, calcium, and vitamin content. Manufacturers are developing specialized formulations that replicate the nutritional profile of traditional milk while eliminating lactose and allergenic proteins. Companies are targeting defined consumer segments such as children, adolescents, and adults with sensitivity conditions to expand penetration beyond niche health categories. Product development teams are focusing on protein fortification, micronutrient balance, and improved digestibility to ensure functional equivalence. As awareness of gastrointestinal health is growing, dairy replacers are becoming part of routine dietary planning rather than occasional substitutes.

Health-conscious households are increasingly selecting dairy alternatives for preventive nutrition and long-term wellness management. Parents are evaluating ingredient transparency and allergen-free positioning when choosing products for children. Food manufacturers are gaining competitive advantage by designing age-specific and condition-specific offerings that address unique dietary requirements. Market leaders are emphasizing digestibility studies, clinical validation, and nutritional benchmarking to reinforce credibility. By aligning innovation strategy with evolving health awareness, dairy replacer producers are converting widespread physiological concerns into durable growth pathways supported by clear functional value propositions.

Regulatory Fragmentation and Labeling Restrictions

Regulatory frameworks for dairy replacers differ significantly between regions. Manufacturers face complex compliance requirements when they operate across multiple markets. Some jurisdictions restrict terminology usage. They prohibit words such as "milk" or "dairy" for plant-based products. These limitations affect how consumers recognize and purchase alternatives. The European Parliament actively debates plant-based product naming rules. Such discussions create uncertainty around future standards. Companies must develop region-specific communication strategies. They balance brand consistency with local regulatory demands. This process complicates product positioning and market entry planning for global participants.

Diverse nutritional labeling rules add further operational challenges. Different markets enforce unique fortification standards and health claim approvals. Manufacturers adjust formulations to meet each region's specific requirements. These variations increase research and development expenses. Smaller competitors struggle most with these compliance burdens. Established firms gain advantage through their regulatory expertise and infrastructure. Companies succeed by building integrated regulatory affairs teams. They anticipate policy changes and create flexible product platforms. Such proactive approaches enable manufacturers to navigate fragmentation effectively and maintain competitive positioning across diverse markets.

Strategic Partnerships between Food Technology Companies and Agricultural Producers

Biotechnology companies, food processors, and agricultural input suppliers are forming integrated collaboration networks that are accelerating innovation across the dairy replacer sector. These partnerships are improving supply chain coordination and are shortening product development cycles. Vertical integration strategies are strengthening cost management and quality oversight from raw material sourcing to final formulation. Large food corporations are acquiring plant-based startups to access specialized fermentation technologies and protein extraction capabilities. Many are also establishing dedicated research centers focused on alternative dairy development. These strategic initiatives are enabling firms to secure intellectual property rights and to commercialize new formulations more rapidly.

Technology transfer is moving efficiently through these structured alliances, and participants are scaling production capacity while expanding geographic distribution. Agricultural biotechnology expertise is integrating with food science research to improve protein functionality, taste, and nutritional density. Consumer-facing brands are contributing market intelligence that is guiding formulation priorities and packaging strategies. This cross-sector convergence is creating value beyond traditional supply chain relationships. Organizations that are coordinating ecosystem partnerships effectively are strengthening operational efficiency and accelerating category growth. Clear governance frameworks and intellectual property management systems are sustaining collaboration benefits over time. Firms that are institutionalizing partnership management practices are positioning themselves to capture a larger share of incremental revenue as the dairy replacer market continues expanding.

Category-wise Analysis

Nature Insights

The organic segment is projected to account for approximately 55% of the dairy replacer market revenue share in 2026. Consumers are associating plant-based nutrition with organic agricultural practices, and this perception is strengthening demand for certified formulations. Organic variants are aligning with preferences for natural, minimally processed foods that exclude synthetic additives and genetically modified organisms (GMO). Certification frameworks such as United States Department of Agriculture Organic (USDA Organic) and European Union Organic (EU Organic) standards are providing structured quality assurance. These regulatory certifications are reinforcing consumer confidence and are supporting premium pricing strategies. Health-focused demographics are demonstrating willingness to pay higher prices for traceable sourcing and verified production practices.

The conventional segment is set to become the fastest-growing between 2026 and 2033 as production efficiency and cost optimization are improving competitiveness against traditional dairy. Manufacturers are enhancing processing methods and securing scalable ingredient sourcing, and these measures are enabling more affordable pricing structures. Conventional products are benefiting from wider retail penetration across supermarkets, discount chains, and value-oriented outlets, which is expanding addressable consumer reach. As awareness of dairy replacers is increasing among mainstream households, demand is extending beyond niche organic buyers. Volume growth is also being driven by price-sensitive consumers who are prioritizing functional nutrition and affordability.

End-User Insights

Food and beverages are projected to command an estimated 58% of the dairy replacer market share in terms of revenue in 2026. Dairy alternatives are being widely incorporated into bakery products, confectionery, ready-to-eat meals, and beverage formulations. Industrial food manufacturers are actively reformulating recipes to reduce allergens, meet clean label expectations, and manage input costs more effectively. Dairy replacers are performing reliably under demanding processing conditions such as high-temperature baking, emulsification, and extended shelf-life packaging. This functional stability is enabling deployment across multiple product categories without compromising taste, texture, or nutritional integrity. Companies are achieving greater formulation flexibility while maintaining consumer-acceptable sensory characteristics comparable to traditional dairy ingredients.

Infant nutrition is likely to register the highest CAGR through 2033, powered by widening awareness of dairy allergies in newborns. Parents are seeking plant-based infant formulas that address intolerance concerns while maintaining nutritional adequacy. Regulatory authorities are granting approvals for specialized formulations that incorporate advanced plant protein blends and fortified micronutrient profiles. The infant nutrition category is sustaining premium pricing due to strict quality standards and heightened parental scrutiny. Manufacturers that are investing in clinical validation, safety testing, and pediatric compliance documentation are strengthening trust with healthcare providers and caregivers. Medical professionals are recommending dairy replacers for infants diagnosed with allergies or sensitivities, and this endorsement is accelerating adoption. Companies that are focusing on research-driven formulation and transparent labeling practices are positioning themselves to capture high-margin growth within pediatric nutrition applications.

Source Insights

Plant-based dairy replacers are expected to capture 62% of market revenues in 2026. Soy, almond, oat, and coconut are serving as primary plant sources within this category. Soy-based formulations are holding a leading share due to their high protein concentration and established processing infrastructure, particularly in Asia Pacific where soy consumption traditions are deeply rooted. Soy protein is delivering a complete amino acid profile that closely matches conventional dairy protein quality, which is supporting nutritional equivalence in fortified products. Mature supply chains, strong agricultural output, and widespread consumer familiarity are reinforcing soy’s commercial resilience. Manufacturers are continuing to optimize extraction efficiency and flavor refinement to enhance acceptance across beverage and infant nutrition segments. This foundation is enabling soy to retain leadership despite intensifying competition from emerging plant sources.

Oat-based dairy replacers are slated to be the fastest-growing segment between 2026 and 2033, on account of shifting consumer preferences toward improved taste and texture performance. Oat formulations are offering a naturally creamy mouthfeel and balanced flavor profile, which is strengthening repeat purchase rates in beverages and ready-to-drink products. Oats are containing beta glucan, a soluble fiber associated with cholesterol management benefits, and this attribute is supporting differentiated health positioning. Environmental considerations are influencing purchasing behavior, and oat cultivation is generally requiring lower water input compared to several tree nut alternatives. Manufacturers are scaling production capacity to meet rising demand while maintaining supply chain stability. As sustainability metrics and sensory quality are becoming central to brand differentiation, oat-based dairy replacers are gaining traction across retail and food service channels.

Regional Insights

North America Dairy Replacer Market Trends

North America is likely to represent approximately 35% of the dairy replacer market value in 2026. The United States leads regional consumption patterns through established plant-based food culture and widespread consumer awareness. Urban centers in Canada show strong growth potential, particularly among diverse immigrant communities with varied dietary needs. Advanced retail distribution networks ensure broad product availability across grocery chains and specialty stores. Strong consumer purchasing power supports premium product adoption among health-conscious demographics. Robust food innovation ecosystems in California and Northeast regions drive continuous product development and market differentiation.

The United States Food and Drug Administration (FDA) provides supportive regulatory frameworks that facilitate market entry for new dairy replacer formulations. Major retailers actively expand shelf space dedicated to plant-based alternatives, significantly improving consumer access. The competitive landscape balances established multinational corporations with dynamic startup innovators, creating vibrant market dynamics. Foodservice channels represent strategic growth opportunities, particularly coffee shops, quick-service restaurants, and institutional catering operations. Companies succeed by targeting these high-volume channels where dairy replacer penetration accelerates most rapidly. Investment flows support technology development while distribution partnerships drive scale across retail and foodservice applications.

Europe Dairy Replacer Market Trends

Europe is anticipated to play an instrumental role within the global market for dairy replacers through 2033. Germany leads regional consumption patterns through its mature organic food sector and advanced retail infrastructure for specialty dietary products. The United Kingdom, France, and Spain follow as key markets with established consumer bases. Northern European countries demonstrate particular strength due to widespread environmental consciousness that favors sustainable food alternatives. Mature distribution networks ensure consistent product availability across urban and suburban retail channels. Well-developed cold chain logistics support premium fresh and refrigerated dairy replacer categories.

The EU Farm to Fork Strategy and Green Deal initiatives establish supportive policy frameworks that accelerate plant-based food adoption. Regulatory harmonization across member states enables efficient cross-border trade and facilitates market scale-up for compliant manufacturers. Labeling restrictions on plant-based terminology present marketing challenges in select jurisdictions, requiring region-specific communication strategies. Investment activity concentrates in food technology hubs such as Berlin, Amsterdam, and London, were corporate venture capital from major food conglomerates fuels innovation. Eastern European markets offer expansion potential as rising disposable incomes and westernized dietary patterns drive dairy replacer penetration in countries including Poland, Czech Republic, and Romania. Companies can achieve competitive advantage through sustainability positioning, clean label formulations, and alignment with local consumer values.

Asia Pacific Dairy Replacer Market Trends

Asia Pacific is poised to emerge as the fastest-growing market for dairy replacers during the 2026-2033 forecast period. China leads consumption patterns through government initiatives that promote plant-based protein development and food security diversification. Japan follows with sophisticated consumer preferences for premium, health-focused formulations, particularly in functional beverage categories. India benefits from cultural familiarity with plant-based proteins and large vegetarian populations. ASEAN nations including Indonesia, Thailand, and Vietnam demonstrate strong expansion potential driven by youthful demographics and growing exposure to global dietary trends. Manufacturing proximity to raw materials such as soy and rice creates cost advantages and enhances supply chain performance.

High lactose intolerance prevalence generates inherent demand across East Asian populations. Rapid urbanization and expanding middle-class segments accelerate market penetration in urban centers. Companies achieve competitive positioning through localized production facilities that reduce logistics costs and improve delivery reliability. Cold chain infrastructure investments support premium fresh product categories while distribution network optimization addresses geographic diversity. Strategic success requires tailored marketing approaches that accommodate varying regulatory frameworks and consumer expectations across fragmented markets. Manufacturers prioritize price-competitive formulations for mass-market segments alongside premium offerings for health-conscious urban consumers to maximize regional growth opportunities.

Competitive Landscape

The global dairy replacer market showcases a moderately fragmented structure, with leading multinational companies collectively accounting for approximately 35-40% of total revenues. Prominent participants such as Danone, Nestlé, Oatly Group AB, and Ripple Foods are maintaining significant influence through diversified product portfolios and strong brand recognition. These organizations are competing to address rising demand for plant-based nutrition and sustainable ingredient sourcing while differentiating offerings in an increasingly competitive landscape. They are prioritizing formulation innovation, nutritional optimization, and strict quality assurance standards to meet evolving consumer expectations. Strategic collaborations with agricultural technology providers are strengthening raw material traceability and supply consistency. Companies that are leveraging scale advantages in procurement and global distribution are reinforcing market leadership in premium and mainstream segments.

Competitive intensity is increasing as firms are adopting advanced manufacturing technologies and environmentally responsible production practices. Investment in energy-efficient processing, sustainable packaging, and transparent sourcing frameworks is becoming central to brand positioning. Market leaders are integrating research capabilities with commercialization expertise to accelerate product launches across infant nutrition, beverages, and functional foods. At the same time, emerging players are targeting niche applications and region-specific taste preferences to capture incremental share. This balance between established multinational operators and agile innovators is sustaining moderate fragmentation while driving continuous technological and sustainability-focused advancement.

Key Industry Developments

- In January 2026, MÖ Foods raised US$ 2.4 million in funding to scale its oat-based cheese technology, aiming to expand production capacity and accelerate commercial launches of dairy-alternative cheese products. The investment will support R&D, manufacturing scale-up, and broader market distribution in plant-based dairy segments.

- In November 2025, Remilk partnered with Gad Dairies to launch “New Milk”, a lactose-free, low-sugar milk made using precision fermentation to produce recombinant beta-lactoglobulin, positioned as conventional milk rather than an alternative product. The company stated that high-efficiency yeast fermentation and strong titers are enabling competitive unit economics, with plans to scale through co-manufacturing partnerships in North America and Asia.

- In September 2025, Ecotone launched Kallo Alt Milks, a new oat milk line under its Kallo brand in the United Kingdom, aimed at expanding its presence in the growing dairy alternative category with products made from oat and pea to meet rising consumer demand for sustainable and allergen-friendly beverage options.

Companies Covered in Dairy Replacer Market

- Danone S.A.

- Nestlé S.A.

- The Coca-Cola Company

- Oatly Group AB

- Califia Farms

- Ripple Foods

- Blue Diamond Growers

- Sanitarium Health & Wellbeing

- Kikkoman Corporation

- Vitasoy International Holdings

- Elmhurst 1925

- Chobani LLC

- Archer Daniels Midland Company

- Triballat Noyal

- Earth's Own Food Company

Frequently Asked Questions

The global dairy replacer market is projected to reach US$ 16.7 billion in 2026.

Livestock production intensification, animal welfare regulations, and nutritional technology advancements are propelling market growth.

The dairy replacer market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Sustainability certifications and specialized formulations for alternative livestock species are opening lucrative market opportunities.

Danone S.A., Nestlé S.A., Oatly Group AB, and Ripple Foods.are some of the key players in the market.