- Processed Food

- Libya Dairy Products Market

Libya Dairy Products Market Size, Share, and Growth Forecast 2026 - 2033

Libya Dairy Products market by Product Type (Milk, Cheese, Butter & Cream, Milk Powders, Yogurt, Others), by Flavor (Flavored, Unflavored), by Sales Channel (B2B, B2C), and by Regional Analysis, 2026-2033

Libya Dairy Products Market Size and Trend Analysis

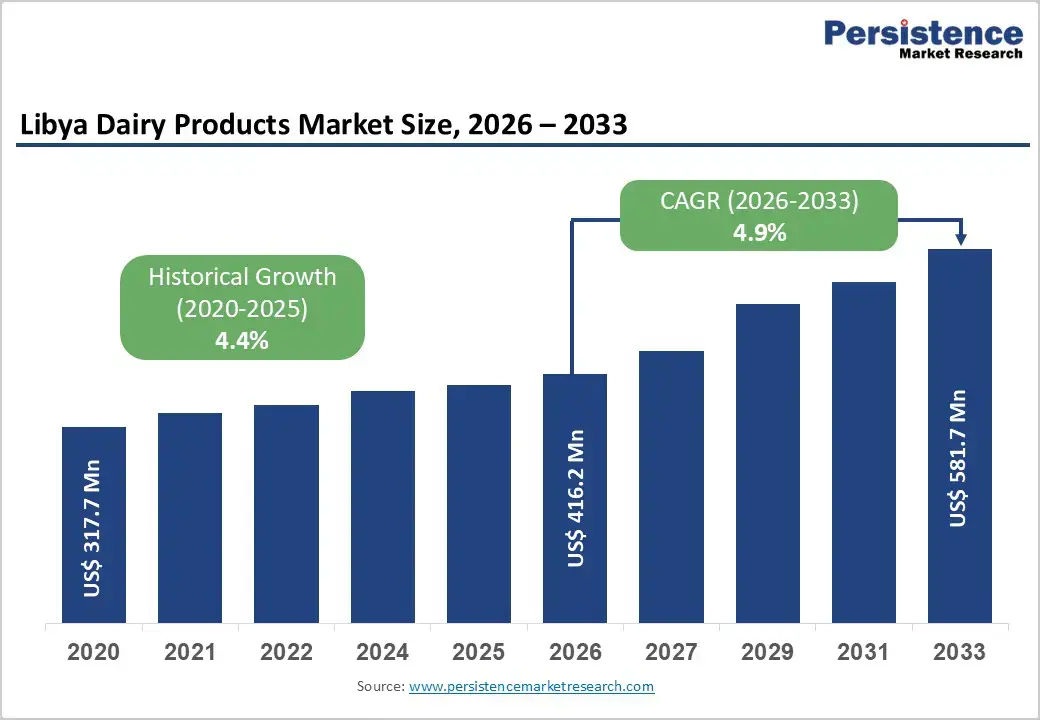

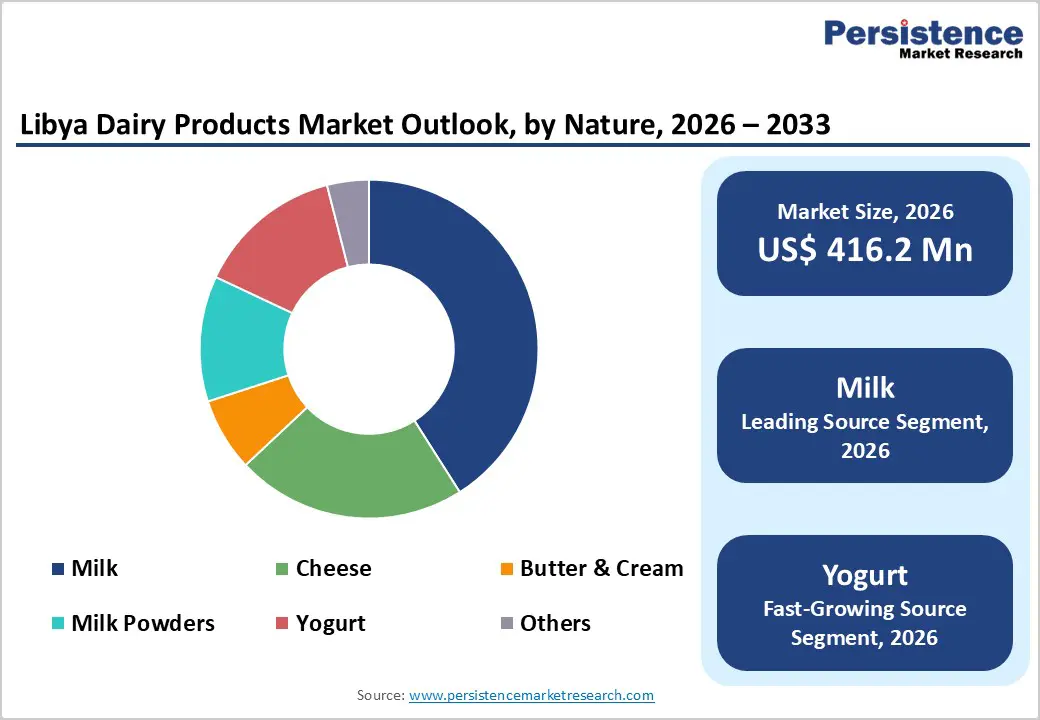

The global Libya Dairy Products market size is expected to be valued at US$ 416.2 million in 2026 and projected to reach US$ 581.7 million by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

Libya’s dairy products market is transitioning from basic supply-driven consumption toward a more structured, urban-centric food system. Population growth, retail modernization, and gradual product diversification are reshaping demand patterns while exposing structural gaps in domestic production.

Key Industry Highlights

- Dominant Product Type Segment: Milk leads the Libya dairy products market with approximately 42% share, supported by its affordability, nutritional value, cultural acceptance, and widespread use across households, foodservice, and institutional nutrition programs.

- Fastest-Growing Segment: Flavored dairy products are projected to grow at a CAGR of around 8.9%, driven by rising demand among children and youth for chocolate, vanilla, fruit-flavored milk, and dessert-style yogurts that combine indulgence with familiarity.

- Market Drivers: Rapid population growth and urbanization are increasing daily dairy consumption, supported by expanding modern retail access, improved cold-chain distribution, and the perception of dairy as a core source of protein, calcium, and child nutrition.

- Opportunities: Growing awareness of digestive health and ingredient transparency is creating opportunities for lactose-free, low-fat, and organic dairy products, allowing local processors and new entrants to pursue premium positioning beyond price-based competition.

- Key Developments: In July 2025, Tetra Pak partnered with Zulfa on a US$16 million greenfield project to strengthen Libya’s food and beverage processing infrastructure; in March 2025, Al Naseem won Libya’s Best Local Product Award, reinforcing confidence in domestic dairy manufacturing; in June 2024, Al Ameed Coffee entered the dairy indulgence space with limited-edition coffee-based ice cream flavors.

| Key Insights | Details |

|---|---|

| Libya Dairy Products Market Size (2026E) | US$ 416.2 Mn |

| Market Value Forecast (2033F) | US$ 581.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver – Growing population and urbanization are increasing dairy consumption demand

Libya’s evolving demographic structure is reshaping everyday food consumption patterns, placing dairy products firmly at the center of household nutrition. Rapid population growth, combined with steady migration toward urban centers such as Tripoli, Benghazi, and Misrata, is increasing reliance on packaged, standardized dairy products. Urban consumers prioritize convenience, food safety, and consistent quality, driving higher intake of pasteurized milk, yogurt, and processed cheese. Smaller family units and rising female workforce participation further accelerate demand for ready-to-consume dairy formats that reduce preparation time while delivering essential nutrients.

Urban expansion is also strengthening modern retail penetration, allowing chilled dairy products to reach a broader consumer base. Supermarkets and neighborhood stores now stock a wider variety of locally produced and imported dairy, increasing consumption frequency. As urban lifestyles intensify, dairy is increasingly viewed as a daily staple supporting protein intake, bone health, and child nutrition across Libyan households.

Restraints – Limited domestic dairy production capacity requiring heavy import dependency

Structural constraints within Libya’s domestic dairy ecosystem continue to limit the market’s self-sufficiency. Local milk production remains challenged by arid climatic conditions, limited fodder availability, and fragmented farm infrastructure. Small-scale dairy farms often struggle with inconsistent yields, animal health management, and access to modern milking technology. These limitations restrict the availability of raw milk required for large-scale processing, making it difficult for domestic producers to meet growing national demand reliably.

As a result, Libya relies heavily on imported milk powders, cheese, butter, and value-added dairy products to stabilize supply. Import dependence exposes the market to foreign currency fluctuations, logistics disruptions, and global price volatility. Extended supply chains also raise costs for processors and consumers. This dependency constrains pricing flexibility, limits innovation cycles, and slows the development of a resilient, locally integrated dairy value chain.

Opportunity – Growing demand for specialized products like lactose-free and organic dairy alternatives

Changing dietary awareness is opening a premium opportunity space within Libya’s dairy products market. Urban consumers are increasingly attentive to digestive health, ingredient transparency, and perceived product purity. This shift is stimulating interest in lactose-free milk, low-fat yogurt, and organic dairy variants designed for sensitive consumers. Families with children and elderly members are driving demand for gentler formulations that support digestion without compromising nutritional intake or taste expectations.

For key players and emerging startups, specialized dairy represents a margin-rich expansion path. Smaller production runs, targeted branding, and health-oriented positioning allow differentiation beyond price competition. Local processors can partner with ingredient suppliers to introduce enzyme-treated lactose-free milk or certified organic lines for niche retail channels. As consumer education improves, demand for functional and clean-label dairy alternatives is expected to strengthen, enabling innovation-led growth within Libya’s evolving dairy landscape.

Category-wise Analysis

Product Type Analysis

Milk holds approximately 42% market share in Libya’s dairy products market as of 2025, reflecting its role as a daily dietary essential. Fresh and reconstituted milk is widely consumed across all income groups due to its affordability, nutritional density, and cultural acceptance. It serves as a foundational food for children, adults, and elderly populations, reinforcing stable baseline demand regardless of economic fluctuations or seasonal shifts.

Milk’s dominance is further supported by its versatility across household and commercial applications. It is consumed directly, used in tea and coffee preparation, and incorporated into cooking and baking. Government-backed nutrition programs and school feeding initiatives also reinforce regular milk consumption. Compared to cheese or butter, milk requires lower consumer spending per purchase, encouraging higher purchase frequency. These structural consumption patterns firmly anchor milk as the leading product category within Libya’s dairy market.

Source Analysis

Flavored dairy products are expected to show a CAGR growth of 8.9% in the forecast period, driven by evolving taste preferences among younger consumers. Sweetened milk, fruit-flavored yogurt, and dessert-style dairy beverages are gaining visibility across urban retail outlets. Flavor innovation enhances product appeal, particularly for children and teenagers, transforming dairy from a functional staple into an enjoyable consumption experience.

Growth is also supported by lifestyle changes favoring indulgent yet familiar foods. Flavored dairy bridges traditional consumption habits with modern snacking behavior, offering variety without deviating from trusted dairy formats. Manufacturers are experimenting with chocolate, vanilla, strawberry, and regionally inspired flavors to increase shelf differentiation. Attractive packaging and single-serve formats further support impulse purchases. As disposable incomes gradually stabilize, flavored dairy is positioned to capture incremental consumption occasions across Libya’s expanding urban population.

Market Competitive Landscape

The Libya dairy products market exhibits a moderately fragmented structure, combining domestic processors with imported brands competing across price and quality tiers. Local companies focus on essential dairy categories such as milk, yogurt, and soft cheese, prioritizing supply continuity and affordability. Leading players invest in cold-chain logistics, improved packaging, and compliance with national food safety standards to strengthen consumer trust and retail reach.

Product innovation is gradually gaining momentum, particularly in flavored milk and extended-shelf-life formats suited to Libya’s climate. Sustainability efforts emphasize efficient water usage, waste reduction, and recyclable packaging. Certifications related to hygiene, halal compliance, and quality management enhance brand credibility. Government oversight on food imports and labeling supports market stability, while consumer education campaigns are improving awareness around nutrition, storage practices, and product differentiation within the dairy segment.

Key Developments:

- In July 2025, Tetra Pak has partnered with Zulfa to launch a US$16 million greenfield project in Libya, marking a strategic move to strengthen food and beverage processing infrastructure in the country.

- In March 2025, Al Naseem secured first place in Libya’s Best Local Product Award, highlighting its strong commitment to quality and local manufacturing excellence.

- In June 2024, Al Ameed Coffee expanded its product portfolio with the launch of two limited-edition ice cream flavors, combining its signature coffee with caramel and coffee with cardamom.

Companies Covered in Libya Dairy Products Market

- Nestlé S.A.

- Al Naseem

- Lactalis Group

- Ghalia

- Aljaied

- Arab Dairy

- Alnour Company

- Others

Frequently Asked Questions

The market is expected to be valued at US$ 416.2 million in 2026, following a steady growth trajectory from its 2020 valuation.

A growing population and urbanization are key drivers in the Libya dairy products market.

Growing demand for specialized products like lactose-free and organic dairy alternatives is a key opportunity for key players and startups in the Libya Dairy Products market.

Key players include Nestlé S.A., Al Naseem, Lactalis Group, Ghalia , Aljaied , Arab Dairy and others