- Home Care & Utilities

- Air Purifier Market

Air Purifier Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Air Purifier Market by Technology (HEPA, Activated Carbon, Ionic Filters), by Coverage Range (Below 250 Sq. Ft., 250 to 400 Sq. Ft., 401 to 700 Sq. Ft.), by Sales Channel (Online, Offline), by Application (Commercial, Residential), and Regional Analysis for 2025 - 2032

Air Purifier Market Size and Trends Analysis

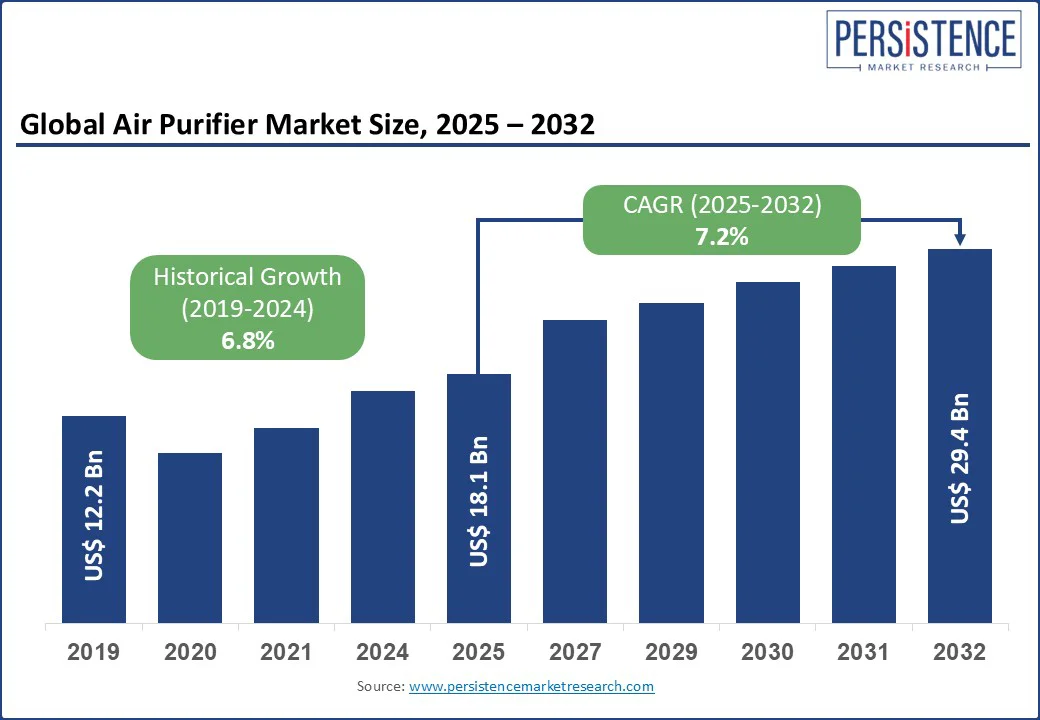

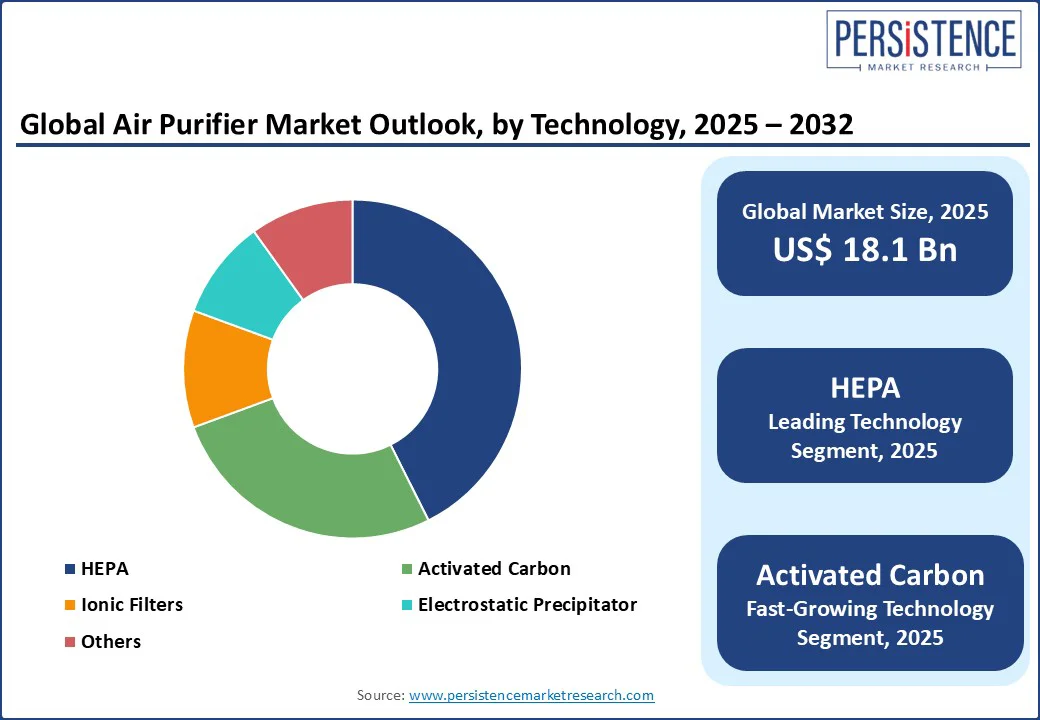

The air purifier market size is likely to be valued at US$ 18.1 Bn in 2025 and is estimated to reach US$ 29.4 Bn in 2032, growing at a CAGR of 7.2% during the forecast period 2025 - 2032.

The air purifier market growth is spurred by increasing concerns over urban pollution, indoor air quality compliance, and airborne disease transmission. Developments in filtration technology have further strengthened the product’s role in tackling VOCs.

Key Industry Highlights

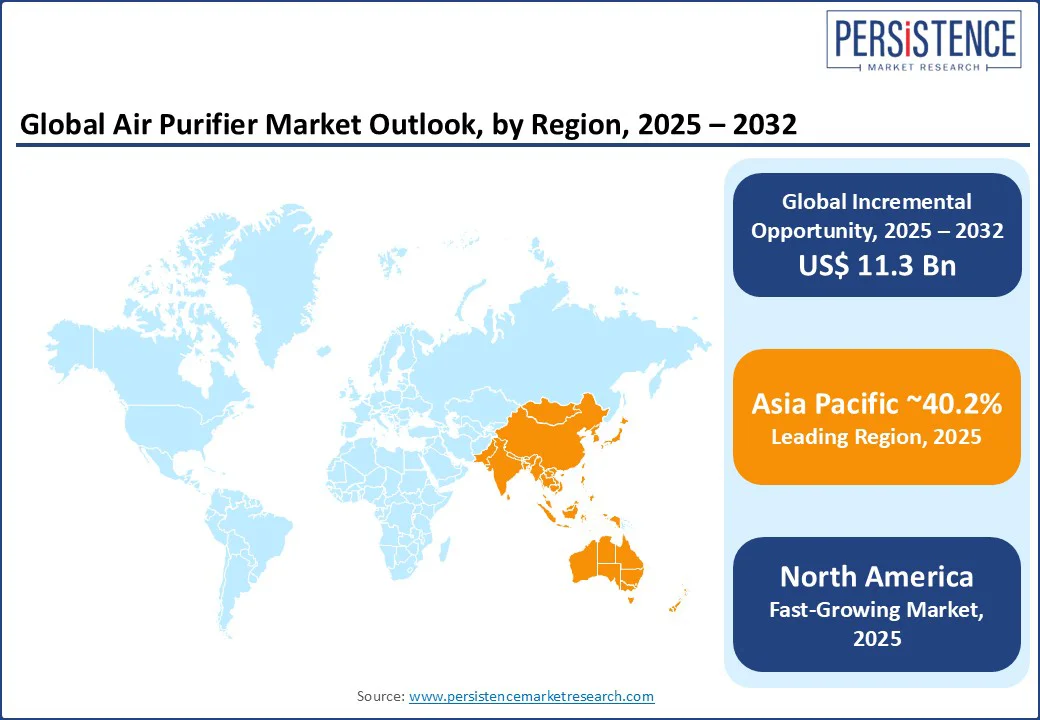

- Leading Region: Asia Pacific with around 40.2% share in 2025, boosted by industrial pollution, urban smog, and government-led clean air programs.

- Fastest-growing Region: North America is likely to witness robust growth because of seasonal wildfire smoke and strict indoor air quality guidelines.

- Legacy Company: In August 2025, Alen celebrated 20 years of creating unique air purifiers that ensure the health and safety of millions of Americans. It has become a trusted name in clean air solutions since its founding in 2005.

- Dominant Technology: HEPA, approximately 42.6% share in 2025, spurred by superior particle capture efficiency and widespread use in healthcare facilities.

- Leading Application: Commercial sectors are expected to witness a leading position due to the rise in employee wellness initiatives are prompting offices to invest in air purification systems.

|

Global Market Attribute |

Key Insights |

|

Air Purifier Market Size (2025E) |

US$ 18.1 Bn |

|

Market Value Forecast (2032F) |

US$ 29.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver - Rising Incidence of Airborne Illnesses Spurs Demand

Surging prevalence of airborne diseases is propelling demand for air purifiers worldwide. Post-pandemic awareness has made households, businesses, and institutions more conscious of how pathogens spread through microscopic aerosol particles. In late 2023 and early 2024, several regions experienced simultaneous surges of flu and COVID-19 cases. It prompted renewed interest in portable HEPA units for offices, classrooms, and waiting rooms. These purchases are no longer seasonal, but they are seen as part of year-round preventive infrastructure.

Healthcare facilities are leading this trend as infection control protocols increasingly incorporate mechanical filtration with proven pathogen removal rates. In commercial settings, the demand is boosted due to liability and operational continuity concerns. Companies in high-density work environments have invested in purifiers with both HEPA and UV-C stages to limit transmission during outbreaks.

Restraint - High Recurring Filter Replacement Costs Deter Buyers

Drawbacks such as dryness and irritation from reduced humidity are hampering adoption to a certain extent, as they affect day-to-day comfort. In cold or arid climates, continuous operation of HEPA-based purifiers can strip additional moisture from already dry indoor air, leading to complaints of dry throat, itchy eyes, or nasal irritation. In Japan, where pollen season often coincides with low humidity, some consumers prefer humidifier-purifier combos to avoid these side effects.

The recurring cost of filter replacement is another barrier, mainly in price-sensitive markets. High-quality HEPA and activated carbon filters can cost 20 to 30% of the purifier’s original price annually. In heavily polluted cities, replacement intervals can be as short as three to six months. This issue is more pronounced for imported brands whose replacement filters are priced higher or have limited local availability.

Opportunity - Smart Home Compatibility Broadens Market Penetration

The launch of smart air purifiers with HEPA filtration, app-based control, and real-time air quality monitoring is creating new avenues. These features transform an air purifier from a passive appliance into an active system that responds to changing indoor and outdoor conditions. For instance, Coway’s Airmega series in South Korea recently began providing AI-based operation modes that adjust fan speeds automatically when outdoor AQI spikes. This level of automation appeals to tech-savvy consumers who want minimal manual intervention without compromising air quality.

The connectivity element is also broadening market reach into ecosystems beyond standalone appliances. App-based control allows integration with smart home platforms such as Google Home, Amazon Alexa, and Apple HomeKit. Real-time air quality monitoring is creating a feedback loop that improves consumer trust and engagement. By displaying particulate levels, VOC concentrations, and filter life in real time, manufacturers are turning abstract health risks into trackable data.

Category-wise Analysis

Technology Insights

By technology, the segmentation comprises High Efficiency Particulate Air (HEPA), activated carbon, ionic filters, electrostatic precipitator, and others. Among these, HEPA is poised to hold nearly 42.6% of the air purifier market share in 2025 as it delivers proven and measurable performance against fine particulate matter, which is the main air quality concern in urban and rural settings.

Certified HEPA filters can capture at least 99.97% of particles as small as 0.3 microns, making them effective against PM2.5, pollen, mold spores, and certain bacteria. This precision is necessary in South Asia and Eastern Europe, where prolonged exposure to high PM levels is associated with respiratory illness.

Activated carbon technology is gaining momentum as it addresses a category of indoor air pollutants that mechanical filters cannot effectively capture. These include Volatile Organic Compounds (VOCs) from paints, cleaning agents, and furnishings, as well as smoke and cooking fumes. As urban living spaces become compact and airtight for energy efficiency, the concentration of such gases is rising. It is prompting increased consumer interest in purifiers with thick and high-quality activated carbon filters.

Application Insights

In terms of application, the market is trifurcated into commercial, residential, and industrial. Out of these, the commercial segment is expected to account for around 59.5% of share in 2025 as businesses and institutions face regulatory pressure and reputational risk if Indoor Air Quality (IAQ) fails to meet acceptable standards.

Offices, schools, hospitals, hotels, and retail spaces are being held accountable for the health and comfort of occupants. High occupancy levels in commercial spaces make consistent air purification important for both particulate and gaseous pollutants. Hospitality venues such as hotels in Dubai and Singapore have adopted multi-stage systems with HEPA and activated carbon filtration to maintain odor-free environments.

Residential application is seeing steady growth because poor outdoor air quality is increasingly intruding into homes. Individuals are becoming more aware of the long-term health risks of indoor pollutants. In Delhi, Jakarta, and Warsaw, seasonal smog events now last weeks rather than days, augmenting homeowners to invest in continuous indoor protection. T

echnology and affordability are also making residential adoption easy. Compact purifiers with verified Clean Air Delivery Rate (CADR) ratings are now available in the sub-US$ 150 range in emerging countries, making them accessible to middle-income households.

Regional Insights

Asia Pacific Air Purifier Market Trends - Prolonged PM2.5 and PM10 Exposure in China and India Fuels Demand

In 2025, Asia Pacific is predicted to account for approximately 40.2% of share due to severe air pollution, recurring seasonal haze, and rising consumer health awareness. China and India are witnessing steady growth with urban residents facing prolonged exposure to PM2.5 and PM10 levels above WHO guidelines.

In 2024, New Delhi recorded multiple severe AQI days even outside the traditional winter smog season. Such scenarios are pushing residential and institutional demand for HEPA systems. Cities such as Beijing and Shanghai are seeing rising sales of smart air purifiers with integrated air quality sensors, allowing real-time monitoring through mobile apps.

Government policies are increasingly steering product development. China’s GB/T 18801-2022 standard has compelled domestic and international brands to refine product performance. India’s Bureau of Indian Standards (BIS) introduced guidelines in 2023 to ensure clear labeling and consumer safety, encouraging the adoption of ozone-free technologies. These norms are prompting manufacturers to focus on verifiable performance metrics rather than marketing claims. It is gaining traction in markets with counterfeit or unregulated devices.

North America Air Purifier Market Trends - Midwest and Northeast Households Invest in HEPA Units

In North America, air cleaner has shifted from being a seasonal or optional purchase to a year-round necessity. It is attributed to recurring wildfire smoke events, post-pandemic awareness of airborne pathogens, and stringent state-level norms. In the U.S. air purifier market, households in the Midwest and Northeast are investing in portable HEPA units with certified CADR to mitigate fine particulate matter (PM2.5) and allergens. Regulatory measures are playing a decisive role in influencing product development.

California’s requirement for portable air purifiers to hold California Air Resources Board (CARB) certification and meet strict ozone emission caps has eliminated ozone-generating devices from mainstream retail shelves. These rules now also apply to in-duct electronic devices, compelling manufacturers to redesign products to meet safety benchmarks. Such compliance measures have influenced national product strategies as brands seek to improve SKUs for multiple states rather than develop separate models.

Europe Air Purifier Market Trends - Urban Smog in High-density Cities Sustains Demand

In Europe, the market is developing owing to the requirement for urban smog control in high-density areas and allergen management in countries with clean outdoor air but rising pollen loads. Warsaw, Milan, and Sofia continue to face particulate matter levels surpassing EU limits during winter heating months.

It is leading to sustained residential demand for portable HEPA units. Seasonal allergen concerns are emerging as a key growth driver in northern and western Europe. Germany, the Netherlands, and the U.K. have reported extended pollen seasons due to climate change.

Birch pollen counts in Hamburg reached record highs in 2024. This has broadened the market beyond pollution-heavy cities to suburban households. Buyers are now demanding units with HEPA-13 filters and activated carbon layers for allergen and odor control. The EU’s Ecodesign Directive, which extends to certain categories of small household appliances, is further encouraging manufacturers to improve energy efficiency without compromising filtration performance.

Competitive Landscape

The global air purifier market consists of global appliance giants, regional specialists, and niche firms targeting specific air quality concerns. Global brands maintain a dominant position through high-performance, design-backed products that integrate smart connectivity and multifunctional features.

Regional manufacturers are focused on customizing products as per local air quality challenges and consumer budgets. In China, brands such as Xiaomi and Blueair compete in the mid-range and smart-connected segment. Xiaomi embraced its IoT ecosystem to deliver app-controlled purification at accessible price points. The market also includes specialized players that focus on high-performance or institutional-grade purification.

Key Industry Developments

- In November 2024, Dyson introduced the Dyson Purifier Hot plus Cool Gen 1, its latest air purifier, in India. It features an intelligent sensor that automatically detects dust, pollen, and other particle pollution.

- In October 2024, Philips, under Versuni India, launched a new line of air purifiers designed to provide both silent and powerful air purification. The new models were developed to deliver clean air while maintaining a quiet and undisturbed environment.

Companies Covered in Air Purifier Market

- IQAir

- LG Electronics

- Honeywell International, Inc.

- Hamilton Beach Brands, Inc.

- Unilever PLC

- Whirlpool Corporation

- Koninklijke Philips N.V.

- Panasonic Corporation

- COWAY Co., Ltd.

- Samsung Electronics Co., Ltd.

- Molekule

- The Camfil Group

- Dyson

- Sharp Electronics Corporation

- Carrier Global Corporation

- Others

Frequently Asked Questions

The air purifier market is projected to reach US$ 18.1 Bn in 2025.

Rising urban air pollution and surging awareness of indoor air quality are the key market drivers.

The air purifier market is poised to witness a CAGR of 7.2% from 2025 to 2032.

Integration of IoT-enabled controls and development of portable air purifiers for cars are key market opportunities.

IQAir, LG Electronics, and Honeywell International, Inc. are a few key market players.