- Automotive Components & Materials

- Automotive Heat Shield Market

Automotive Heat Shield Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Heat Shield Market by Product Type (Single Shell, Double Shell and Sandwich), by Material Type (Metallic and Non-metallic) by Application (Exhaust System, Turbocharger, Under Bonnet, Engine Compartment and Under Chassis), Vehicle Type (Passenger vehicles, Light Commercial Vehicles (LCV), and Heavy Commercial Vehicles (HCV)) and Regional Analysis 2026 2033

Automotive Heat Shield Market Size and Trends Analysis

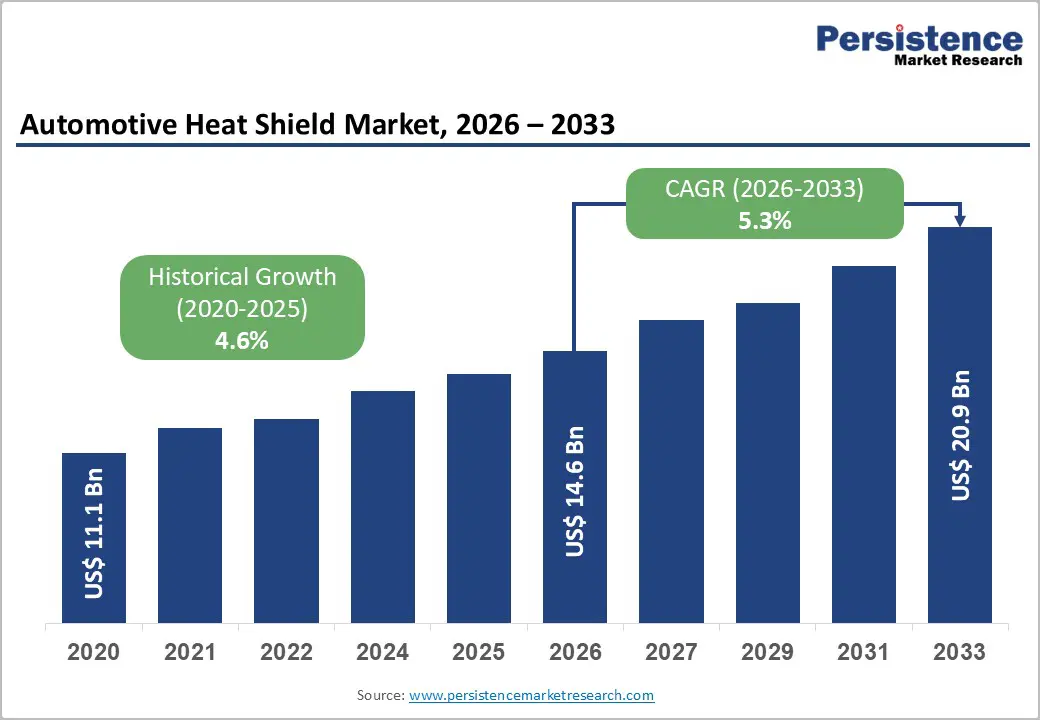

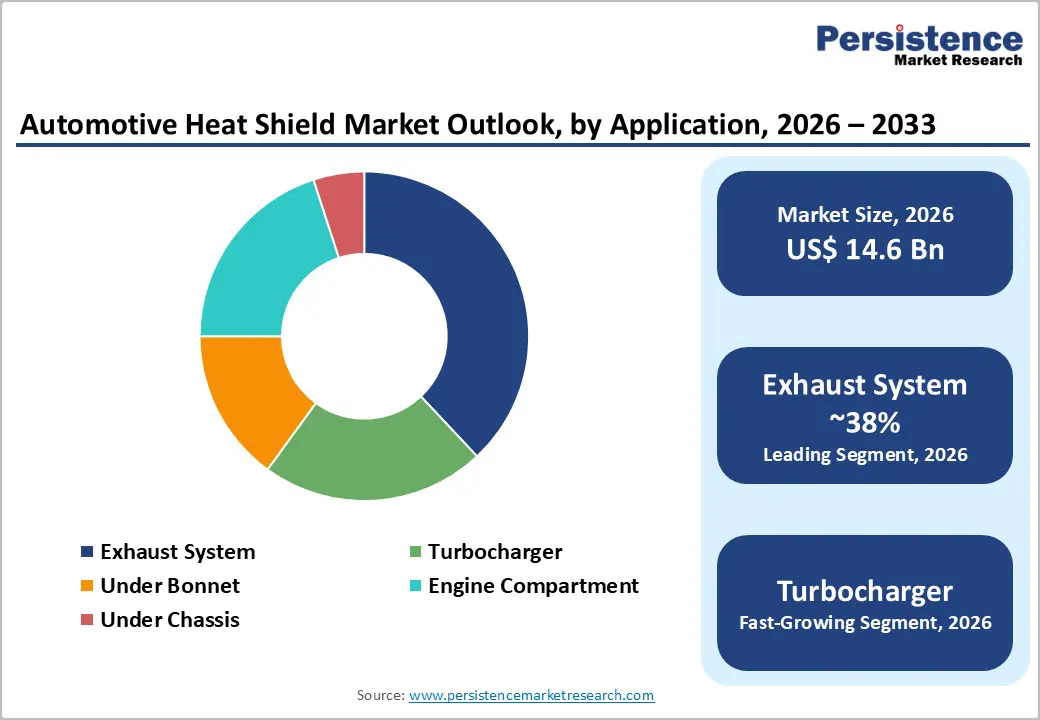

The global Automotive Heat Shield Market size was valued at US$ 14.6 billion in 2026 and is projected to reach US$ 20.9 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The market is experiencing steady expansion driven by rising vehicle electrification trends, increased adoption of turbocharged engines requiring advanced thermal management, stringent emission regulations worldwide, and growing vehicle production particularly in Asia Pacific.

Key Industry Highlights:

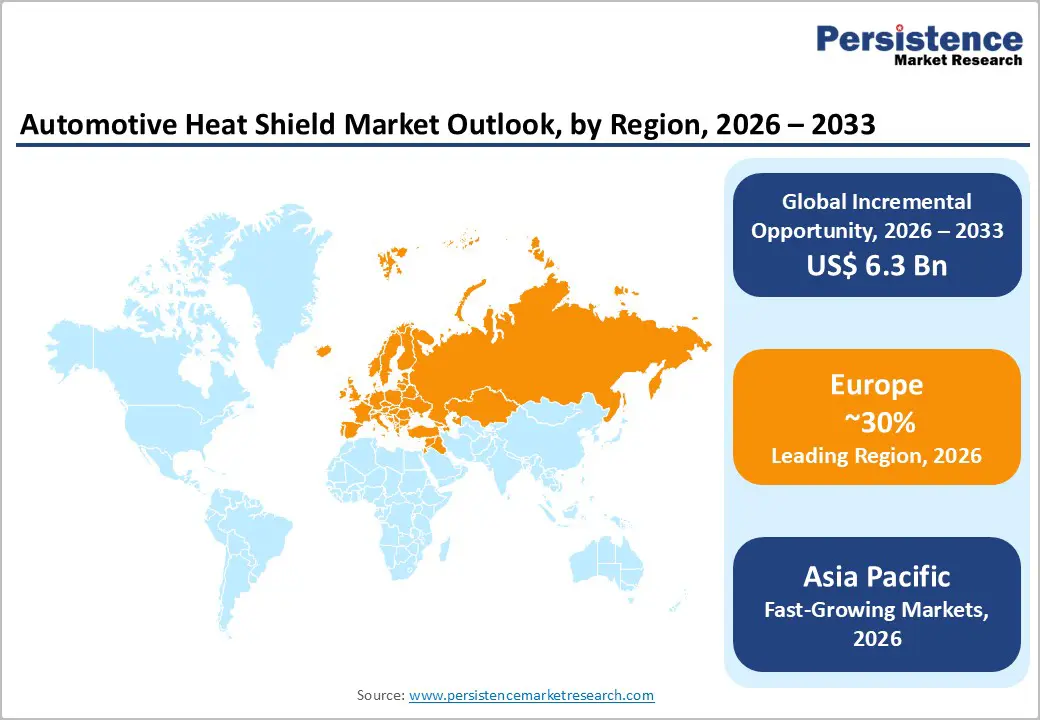

- Leading Region: Europe commands approximately 30% of global Automotive Heat Shield Market revenue, driven by stringent EU emission regulations, accelerating electric vehicle electrification, and premium manufacturing capabilities supporting advanced thermal management solutions in Germany, United Kingdom, France, and Spain.

- Fastest Growing Region: Asia-Pacific exhibits fastest market growth at 7% CAGR through 2033, propelled by explosive vehicle production in China and India, rapid electric vehicle adoption, government manufacturing support initiatives, and emerging market automotive production expansion.

- Dominant Segment: Double-shell heat shields command approximately 46% of market revenue, driven by superior thermal protection in high-temperature applications, proven manufacturing maturity, and widespread adoption across passenger vehicles, commercial vehicles, and specialized turbocharged engine applications.

- Fastest Growing Segment: Non-metallic heat shields expand fastest at 6% CAGR, driven by accelerating electric vehicle adoption requiring lightweight thermal insulation for battery pack protection, electrical insulation properties, and specialized thermal management supporting emerging vehicle platform requirements.

- Key Market Opportunity: Lightweight composite and ceramic-coated heat shield technologies represent the highest-potential opportunity, enabling manufacturers to reduce vehicle weight while enhancing thermal protection, supporting electric vehicle range improvement, fuel efficiency targets, and emerging thermal management requirements for advanced powertrain technologies.

| Key Insights | Details |

|---|---|

| Automotive Heat Shield Market Size (2026E) | US$ 14.6 Bn |

| Market Value Forecast (2033F) | US$ 20.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.6% |

Market Dynamics

Drivers - Rising Adoption of Turbocharged Engines Accelerating Heat Management Requirements Across Global Markets

The widespread adoption of turbocharged engines across passenger vehicles and commercial vehicle segments is driving exceptional demand for advanced automotive heat shield solutions essential for protecting vehicle components from elevated thermal exposure. Turbochargers substantially increase engine combustion temperatures and ambient engine bay temperatures, requiring sophisticated thermal management systems preventing component degradation and maintaining vehicle performance.

Turbocharged engine adoption has accelerated dramatically in response to emission regulations and fuel efficiency mandates, with manufacturers increasingly incorporating turbocharging technologies across diverse vehicle segments to improve power output while reducing overall engine displacement. Heat shields protecting turbochargers, exhaust manifolds, intercoolers, and associated systems represent critical applications where advanced materials and engineering sophistication are essential for managing thermal loads exceeding 900°C in certain applications.

Electric Vehicle Electrification and Advanced Battery Thermal Management Creating Specialized Shield Demand

The accelerating global transition toward electric vehicles is generating substantial demand for specialized heat shield solutions essential for protecting battery packs, electric motors, inverters, and advanced electronic components from thermal stress. Electric vehicles produce concentrated thermal loads from high-capacity battery systems during charging, discharging, and peak acceleration scenarios where innovative thermal management becomes critical for vehicle safety, battery longevity, and component reliability.

Battery thermal runaway prevention represents a critical safety requirement where heat shields utilizing advanced materials including phase-change materials, aerogels, mica sheets, and multi-layer laminates are increasingly deployed to ensure electrical insulation, fire containment, and optimal temperature distribution across battery cells. Non-metallic heat shield materials are gaining momentum in electric vehicle applications, with specialized ceramics, polymers, and composite solutions offering lightweight properties essential for improving vehicle range while providing superior thermal insulation characteristics.

Restraints - High Complexity and Customization Requirements Increasing Manufacturing Costs and Production Challenges

The increasing complexity of modern vehicle platforms, diverse thermal requirements across specialized applications, and stringent integration constraints create substantial manufacturing challenges limiting cost reduction and market accessibility. Custom heat shield design requirements accommodating tight engine compartment spaces, unique vehicle architectures, and application-specific thermal demands necessitate specialized engineering, prototype development, and rigorous testing protocols increasing overall product development costs. Advanced heat shield configurations including multi-layer sandwich designs, ceramic-coated metallic solutions, and composite structures demand sophisticated manufacturing capabilities, specialized equipment, and trained technical expertise that smaller manufacturers struggle to access affordably.

Transition to Active Cooling Systems Potentially Reducing Passive Heat Shield Requirements in Advanced Vehicles

Advanced thermal management technologies including liquid cooling systems, heat exchangers, and active temperature control mechanisms are becoming increasingly effective at managing thermal loads, potentially reducing reliance on traditional passive heat shield protection. Liquid cooling systems employed by leading electric vehicle manufacturers including Tesla, BMW i-Series, and Jaguar i-Pace efficiently circulate coolant through dedicated channels regulating component temperatures, thereby minimizing thermal stress on surrounding components and reducing passive heat shield requirements. Liquid-cooled turbochargers are increasingly gaining adoption in advanced internal combustion engine vehicles, providing superior thermal management efficiency compared to traditional passive heat shield approaches.

Opportunity - Lightweight and Advanced Material Development Supporting Weight Reduction and Performance Enhancement

Emerging opportunities exist for heat shield manufacturers developing innovative lightweight materials including composite structures, ceramic coatings, and advanced polymers that substantially reduce weight while maintaining superior thermal protection characteristics. Lightweight heat shield solutions support vehicle manufacturers' critical objectives of improving fuel efficiency, extending electric vehicle range, and meeting increasingly stringent emission standards requiring comprehensive weight reduction initiatives across vehicle platforms. Ceramic-coated metallic heat shields represent an emerging segment combining superior thermal barrier performance with minimal weight and thickness, offering manufacturers differentiated solutions addressing space-constrained modern vehicle designs. Carbon fiber composites, graphene-enhanced polymers, and nanostructured ceramic materials are establishing next-generation heat shield platforms delivering exceptional thermal protection with significantly reduced weight compared to traditional metallic solutions.

Expansion of Government Support and Emerging Market Opportunities Driving Regional Growth Acceleration

Rapid economic development across emerging markets in Asia-Pacific, Latin America, and Middle East and Africa regions combined with expanding vehicle production capabilities and government support for automotive manufacturing creates substantial growth opportunities for heat shield suppliers. China maintains the world's largest vehicle production base with 30 million vehicles produced annually, establishing exceptional market scale for heat shield suppliers, while India is experiencing accelerating automotive manufacturing growth driven by government Make in India initiatives and expanding domestic consumption.

Government policies emphasizing emissions reduction, vehicle electrification incentives, and manufacturing sector support across emerging markets are creating favorable conditions for heat shield market expansion. Major vehicle manufacturers are accelerating manufacturing facility development across ASEAN nations including Vietnam, Thailand, and Indonesia, establishing emerging markets as critical growth centers requiring localized heat shield manufacturing and supply networks.

Category-wise Analysis

Product Type Insights

Double-shell heat shields commanding approximately 42% of the Automotive Heat Shield Market represent the leading product segment driven by exceptional thermal protection characteristics in high-temperature applications including exhaust systems and turbocharger environments. Double-shell configurations featuring two metallic layers with integrated air gaps provide superior insulation and durability compared to single-shell alternatives, delivering proven thermal protection in demanding engine compartment and under-hood applications. The double-shell segment is projected to maintain dominance through 2033, supported by widespread adoption in passenger vehicles, commercial vehicles, and specialized high-temperature applications where proven performance characteristics and manufacturing maturity support competitive market positioning.

Sandwich-type heat shields capturing approximately 25% of market revenue represent an emerging advanced segment incorporating multi-layer construction with composite materials, ceramic insulation cores, and specialized material combinations delivering superior thermal protection with reduced weight. Sandwich configurations combining metallic outer shells with insulation material cores including ceramic fibers, polymeric foams, and advanced composite matrices enable manufacturers to achieve exceptional thermal resistance while minimizing overall component weight and thickness.

Vehicle Type Insights

Passenger vehicles commanding approximately 55% of Automotive Heat Shield Market revenue represent the dominant vehicle segment driven by exceptional global production volumes exceeding 75.5 million units annually and widespread heat shield applications across diverse thermal management scenarios. Passenger vehicle heat shield applications encompass exhaust systems, turbochargers, engine compartments, under-chassis protection, and emerging electric vehicle battery pack insulation representing comprehensive thermal protection requirements across modern vehicle platforms. The passenger vehicle segment is projected to maintain market dominance through 2033, supported by continued production growth particularly in Asia-Pacific emerging markets where rapid economic development is expanding vehicle ownership.

Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs) collectively represent approximately 38-45% of market revenue, with LCVs capturing larger share at approximately 22-28% while HCVs represent approximately 16-18% of total market revenue. Commercial vehicle heat shields address more demanding thermal management scenarios including higher exhaust temperatures, extended operational periods, and specialized applications in emission control systems and after-treatment technologies.

Material Type Insights

Metallic heat shields commanding approximately 78% of Automotive Heat Shield Market revenue continue dominating through superior thermal conductivity, exceptional durability, and proven compatibility with existing vehicle platforms and manufacturing processes. Metallic heat shields fabricated from aluminum, stainless steel, and specialty steel alloys deliver proven thermal protection in high-temperature applications exceeding 900°C, with material properties offering excellent heat reflection, structural rigidity, and longevity under demanding operational conditions.

Non-metallic heat shields encompassing ceramic composites, polymer-based insulators, fiber composites, and advanced polymer matrices capture approximately 14-20% of market revenue and represent the fastest-expanding segment at 6-7% CAGR. Non-metallic materials including advanced ceramics, polymeric foams, composite structures, and fiber-based insulators provide specialized thermal insulation characteristics, lightweight properties, and electrical insulation capabilities essential for electric vehicle battery pack protection and emerging thermal management applications.

Application Insights

Exhaust system heat shields capturing approximately 38% of Automotive Heat Shield Market revenue represent the largest application segment serving comprehensive thermal protection requirements across mufflers, downpipes, catalytic converters, and main exhaust components. Exhaust system thermal management is essential for protecting vehicle structures from heat damage, improving emission control system performance, and maintaining vehicle occupant safety through effective heat containment and reflection.

Turbocharger heat shields capture approximately 26% of market revenue and represent the fastest-expanding application segment at 6.5% CAGR, driven by exceptional worldwide adoption of turbocharged engines across passenger vehicles and commercial vehicle segments. Turbochargers generate extreme thermal loads with surface temperatures frequently exceeding 900°C, creating critical thermal management requirements where specialized heat shields protect critical engine compartment components, electronic control units, fuel systems, and adjacent mechanical assemblies from thermal degradation.

Regional Insights

North America Automotive Heat Shields Market Trends

North America commands approximately 22% of global Automotive Heat Shield Market revenue, with the United States representing the dominant regional market driven by substantial vehicle production, strict emission regulations, and widespread adoption of advanced thermal management technologies. The U.S. automotive market produces approximately 10-11 million vehicles annually, establishing exceptional scale for heat shield suppliers, with North American manufacturers increasingly adopting advanced heat shield technologies addressing emission compliance and fuel efficiency requirements.

North American vehicle manufacturers are investing substantially in advanced heat shield solutions incorporating ceramic coatings, composite materials, and lightweight designs supporting improved fuel efficiency and compliance with EPA emission standards. The region's emphasis on technological innovation, combined with established supply chain infrastructure and sophisticated manufacturing capabilities, establishes North America as a premium market segment where advanced heat shield solutions command higher valuations.

Europe Automotive Heat Shields Market Trends

Europe represents approximately 30% of global Automotive Heat Shield Market revenue, with Germany maintaining regional dominance through advanced automotive manufacturing capabilities, premium vehicle production, and strict environmental regulations driving technological sophistication. European vehicle manufacturers are experiencing exceptional growth opportunities in heat shield applications through accelerating electric vehicle adoption, stringent Euro 6 and emerging Euro 7 emission standards requiring advanced thermal management, and regulatory harmonization initiatives establishing standardized compliance frameworks.

The European heat shield market is experiencing fastest regional growth trajectories driven by exceptional electric vehicle electrification rates, particularly in Germany, United Kingdom, France, and Spain, where electric vehicle adoption continues accelerating and creating demand for specialized battery pack thermal protection solutions. European manufacturers emphasize sustainability and environmental compliance, driving investments in lightweight materials, recyclable heat shield solutions, and manufacturing processes supporting environmental responsibility objectives.

Asia Pacific Automotive Heat Shields Market Trends

Asia Pacific represents the fastest-growing regional market, commanding approximately 25% of global Automotive Heat Shield Market revenue with exceptional expansion at 7% CAGR through 2033, driven by explosive vehicle production growth and accelerating electric vehicle adoption. China dominates Asia-Pacific automotive production with 30 million vehicles annually, establishing exceptional market scale for heat shield suppliers, while India is experiencing accelerating production growth and emerging as a critical manufacturing center for global automotive suppliers.

India's automotive sector is projected to become the world's third-largest vehicle producer by 2030, with government Make in India initiatives and expanding domestic consumption driving substantial heat shield demand across passenger and commercial vehicle segments. Asia-Pacific's exceptional growth trajectory reflects the region's manufacturing advantages including lower production costs, expanding automotive supply chains, and accelerating electric vehicle adoption particularly in China where government electrification initiatives and consumer demand are driving rapid EV market expansion.

Competitive Landscape

The Automotive Heat Shield Market exhibits moderately fragmented competitive structure with numerous specialized suppliers, established automotive component manufacturers, and emerging innovators competing across diverse market segments. Tier 1 suppliers including Zircotec Ltd., Morgan Advanced Materials, Tenneco Inc., Autoneum, and ElringKlinger AG leverage extensive automotive supply relationships, specialized thermal engineering expertise, and established manufacturing capabilities. Tier 2 and emerging competitors including Lydall, Inc., Dana Limited, UGN Inc., CARCOUSTICS, and Frenzelit GmbH are expanding through specialized material innovation, regional market focus, and customized solution development.

Key Developments:

- In February 2025, Brookfield acquired Chemelex, a leader in electric heat-trace systems, expanding its capabilities in temperature regulation technologies applicable to automotive thermal management.

- In November 2024, Autoneum inaugurated a new Research & Technology (R&T) Center in Shanghai, China, targeting New Mobility and bolstering its foothold in the region. This center is set to aid in the development and production of components and materials tailored for e-mobility.

Companies Covered in Automotive Heat Shield Market

- Zircotec Ltd

- Morgan Advanced Materials

- DuPont

- Dana Limited.

- Lydall, Inc.

- Tenneco Inc.

- CARCOUSTICS

- UGN Inc.

- Autoneum

- ElringKlinger AG

- Frenzelit GmbH

- Others Key Players

Frequently Asked Questions

The Global Automotive Heat Shield Market is projected to reach US$ 20.9 Billion by 2033, expanding from US$ 14.6 Billion in 2026 at a CAGR of 5.3%.

The market is primarily driven by rising adoption of turbocharged engines requiring advanced thermal management, accelerating electric vehicle electrification creating specialized battery pack thermal protection demand.

Double-shell heat shields dominate approximately 42% of market revenue, driven by superior thermal protection in high-temperature exhaust system and turbocharger applications, proven manufacturing maturity, and widespread adoption across diverse vehicle platforms and thermal management scenarios.

Europe commands approximately 30% of global Automotive Heat Shield Market revenue as leading region.

The key players in Backhoe Loader are Morgan Advanced Materials, Superwool Fibres; Zircotec Ltd., Autoneum and Tenneco Inc.