- Processed Food

- Non-Dairy Ice Cream Market

Non-Dairy Ice Cream Market Size, Share, and Growth Forecast, 2026 – 2033

Non-Dairy Ice Cream Market by Source Type (Soy, Oats, Almond, Coconut, Rice), Flavor (Chocolate, Vanilla, Caramel, Fruity), and Regional Analysis for 2026 – 2033

Non-Dairy Ice Cream Market Size and Trends Analysis

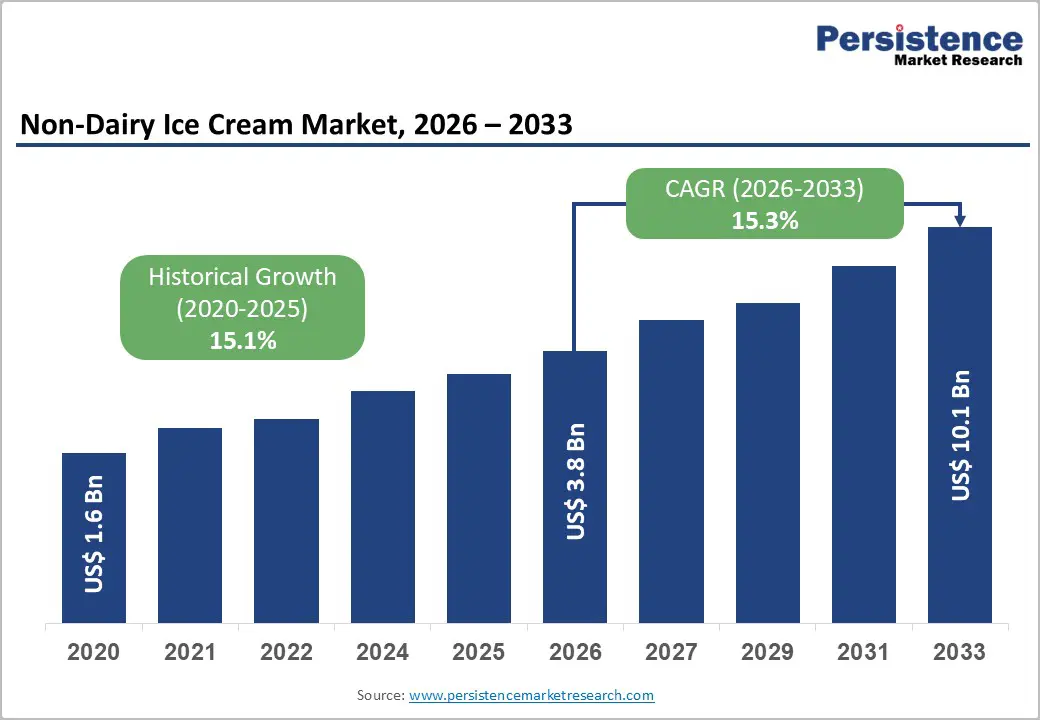

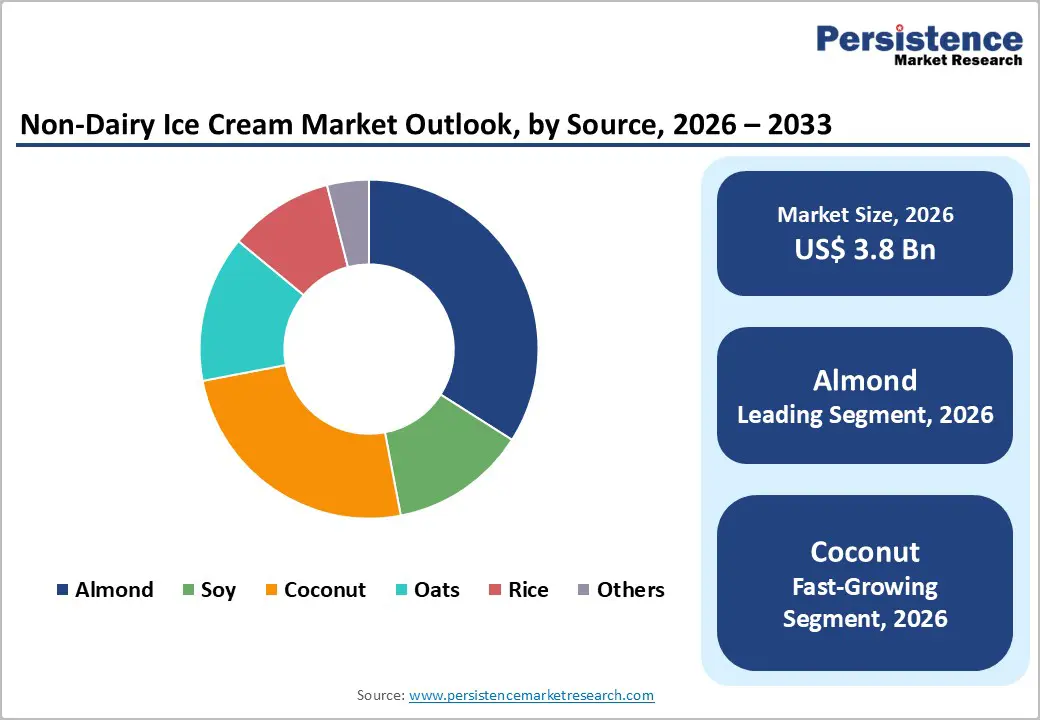

The global non-dairy ice cream market size is likely to be valued at US$3.8 billion in 2026 and is expected to reach US$10.1 billion by 2033, growing at a CAGR of 15.3% during the forecast period from 2026 to 2033, driven by a combination of long-term dietary shifts, health awareness, and sustainability considerations.

Growth builds on steady historical momentum supported by the widespread prevalence of lactose intolerance worldwide, alongside a rising number of consumers adopting vegan, vegetarian, and flexitarian lifestyles. Increasing awareness around cholesterol management, digestive health, and clean-label food consumption is accelerating demand for plant-based frozen desserts as alternatives to conventional dairy ice cream. These advancements are expanding consumer acceptance beyond niche health-focused segments to mainstream audiences.

Key Industry Highlights:

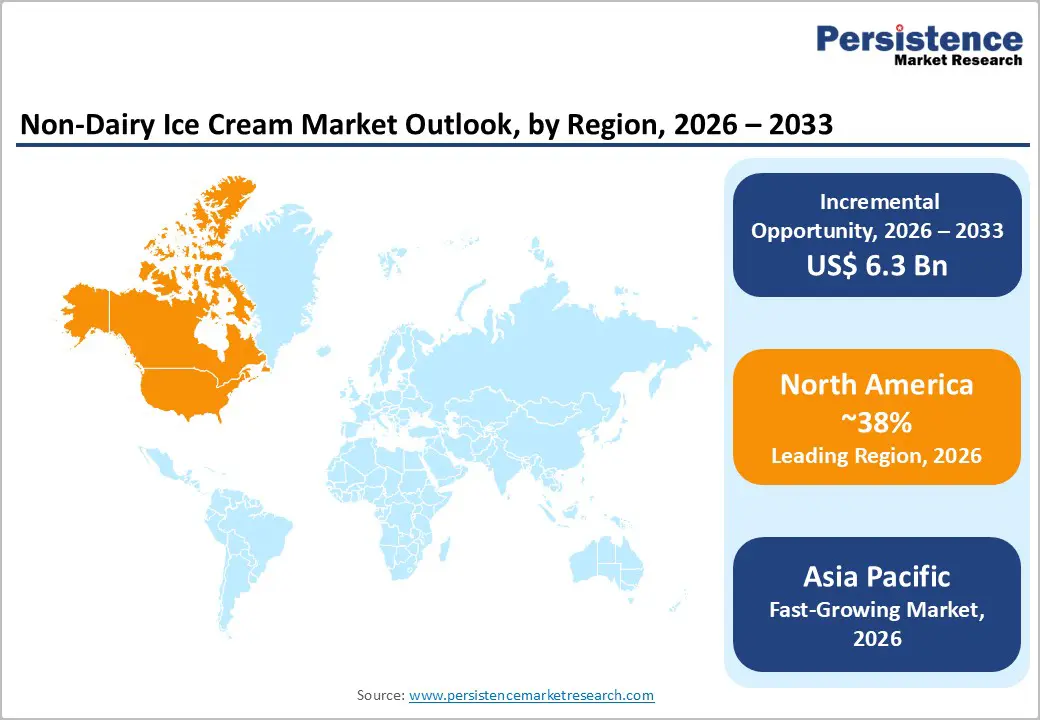

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by U.S. leadership supported by strong retail infrastructure, high vegan adoption, regulatory clarity, and a dynamic innovation ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rising lactose intolerance prevalence, expanding middle-class consumption, rapid urbanization, and strong plant-based raw material availability.

- Leading Source Type: Almond-based products are projected to represent the leading source type in 2026, accounting for 34% of the revenue share, driven by strong consumer preference and premium positioning.

- Leading Flavor: Chocolate is anticipated to be the leading flavor type, accounting for over 36% of the revenue share in 2026, supported by its universal appeal and indulgent positioning.

| Key Insights | Details |

|---|---|

| Non-Dairy Ice Cream Market Size (2026E) | US$ 3.8 Bn |

| Market Value Forecast (2033F) | US$ 10.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Prevalence of Lactose Intolerance and Dairy Allergies

A significant portion of the adult population experiences difficulty digesting lactose, creating sustained demand for plant-based alternatives. Consumers increasingly seek products that eliminate digestive discomfort while maintaining indulgent taste experiences. This shift is particularly visible in regions with high intolerance rates, where dairy-free desserts are transitioning from niche to mainstream categories. Retailers are expanding shelf space for lactose-free frozen desserts, reflecting structural dietary needs rather than short-term trends, strengthening long-term category resilience and consistent consumption growth patterns worldwide.

Beyond intolerance, the rising diagnosis of milk protein allergies among children and young adults accelerates demand. Parents actively search for safe, allergen-friendly dessert options that align with health-conscious household purchasing decisions. Foodservice operators, schools, and hospitality providers are also incorporating dairy-free alternatives to accommodate diverse dietary requirements. Clear labeling, allergen transparency, and plant-based certifications enhance consumer trust and influence buying behavior. As awareness grows through healthcare advocacy and nutritional education, non-dairy ice cream benefits from medically supported demand, reinforcing its position as a necessary alternative rather than merely a lifestyle-driven preference across developed and emerging economies.

Health, Wellness, and Sustainability Trends

Consumers increasingly associate plant-based products with lower cholesterol, cleaner ingredient lists, and improved digestive health. Demand for reduced sugar, organic, non-GMO, and additive-free formulations continues to expand. Many brands now fortify products with probiotics, fiber, and plant proteins to enhance functional appeal. This convergence of indulgence and perceived health benefits allows non-dairy ice cream to attract both health-focused and mainstream consumers. The shift toward mindful consumption patterns supports sustained category expansion, especially among millennial and Gen Z demographics prioritizing balanced lifestyles.

Sustainability concerns amplify market growth as consumers evaluate the environmental footprint of dairy production. Plant-based formulations are often perceived as requiring fewer natural resources and generating lower greenhouse emissions. Ethical considerations surrounding animal welfare also influence purchasing decisions. Brands increasingly highlight sustainable sourcing, recyclable packaging, and transparent supply chains to strengthen environmental credentials. Retailers prioritize eco-conscious product lines, while investors channel funding into sustainable food innovation.

Barrier Analysis - Challenges in Replicating Taste and Texture

Replicating the creamy mouthfeel and richness of traditional dairy ice cream remains a key technical challenge. Dairy fat and milk proteins naturally create smooth texture, stable emulsification, and desirable melting properties that are difficult to duplicate with plant-based ingredients. Some early non-dairy formulations suffered from icy textures or beany aftertastes, limiting repeat purchases. Although ingredient technology has improved significantly, achieving consistent sensory parity across different plant bases requires advanced processing techniques. Texture optimization, fat structuring, and flavor masking add complexity to formulation, increasing research and development demands for manufacturers competing in premium segments.

Consumer expectations for indulgence remain high, and any perceived compromise in flavor or creaminess can restrict broader adoption. Taste remains the primary purchase driver in frozen desserts, making sensory performance critical. Brands must balance clean-label positioning with functional stabilizers to maintain structure and shelf stability. Ingredient variability across almond, oat, coconut, or soy bases complicates standardization. Continuous innovation in emulsifiers, fermentation processes, and fat alternatives is essential to narrow the sensory gap.

Limited Shelf Life and Stability Issues in Plant-Based Formulations

Plant-based ice creams often face stability challenges related to protein structure, fat crystallization, and water binding capacity. Plant proteins do not stabilize mixtures as effectively as dairy proteins, which can cause separation or ice crystals during storage. These issues can impact texture consistency and visual appeal, particularly in fluctuating temperature conditions across supply chains. Maintaining product integrity requires advanced stabilizer systems and strict cold-chain management. Smaller manufacturers may face higher operational costs due to specialized storage requirements, limiting scalability and regional distribution efficiency in emerging markets with underdeveloped infrastructure.

Shelf life can also be influenced by the absence of traditional dairy stabilizing properties, requiring careful formulation adjustments. Oxidation risks in certain plant oils may affect flavor stability over time. Retailers demand extended freezer stability to reduce wastage, pushing producers to invest in improved packaging technologies and moisture barriers. Transportation across long distances increases exposure to temperature variations, heightening product degradation risk. As the category expands, ensuring consistent quality across retail formats becomes critical. Addressing formulation resilience and cold-chain optimization remains essential for sustaining competitive performance.

Opportunity Analysis - Technological Convergence and Functional Innovation

Advances in precision fermentation, plant protein refinement, and fat-structuring technologies enable improved creaminess and flavor authenticity. Companies are leveraging biotechnology to create dairy-identical proteins without animal inputs, enhancing texture performance. Functional innovation also includes incorporating probiotics and added plant proteins to position products as better-for-you indulgences. This fusion of food science and nutrition elevates non-dairy ice cream beyond simple substitution, allowing brands to command premium positioning while meeting evolving wellness expectations.

Digitalization and data-driven product development enhance innovation speed. Consumer insights gathered through online platforms guide rapid flavor experimentation and limited-edition launches. Automation in manufacturing improves consistency and scalability, supporting broader market penetration. Collaboration between food tech startups and established dairy alternatives companies accelerates the commercialization of novel ingredients. Functional claims aligned with digestive health, immunity, or energy support differentiation in competitive retail environments. As consumers increasingly seek indulgent products with added benefits, technological integration creates significant long-term growth opportunities within the category.

Oat and Almond Base Expansion

Almond established a premium perception and mild taste profile, allowing broad compatibility with diverse flavors, from chocolate to fruity blends. Oat-based formulations benefit from creamy texture and sustainable sourcing narratives, resonating strongly with environmentally conscious consumers. Growing agricultural supply chains for both ingredients support scalability. Their adaptability across cuisines enhances cross-regional appeal, making them strategic bases for product diversification in both developed and emerging markets.

Product innovation leveraging oat and almond bases includes hybrid formulations that blend multiple plant sources to optimize taste and texture. Manufacturers are introducing fortified versions with added protein and fiber to strengthen nutritional appeal. Private-label retailers increasingly adopt these bases due to stable sourcing and consumer familiarity. Foodservice operators also prefer oat and almond variants for consistent performance in desserts and beverages. As research improves protein extraction and fat emulsification techniques, these bases are positioned to capture expanding consumer demand, creating sustained opportunities for premiumization and geographic expansion.

Category-wise Analysis

Source Type Insights

The almond-based segment is expected to lead the non-dairy ice cream market, accounting for approximately 34% of revenue in 2026, driven by its strong health positioning and premium consumer perception. Almond milk offers low saturated fat content, natural vitamin E, and a mild flavor profile that blends well with chocolate, vanilla, caramel, and fruit inclusions. Its smooth texture allows manufacturers to deliver a creamy mouthfeel while maintaining clean-label appeal. For example, several leading brands prominently feature almond milk as their core base to support indulgent yet better-for-you positioning.

Coconut-based products are likely to represent the fastest-growing segment in 2026, supported by their rich texture and dairy-like creaminess. Coconut milk’s naturally high fat content helps replicate the smooth mouthfeel traditionally associated with dairy ice cream, reducing the sensory gap for mainstream consumers. Manufacturers increasingly adopt coconut as either a standalone base or part of hybrid blends to enhance stability and creaminess. For example, premium vegan dessert brands often use coconut cream to deliver indulgent textures in chocolate and caramel variants.

Flavor Type Insights

Chocolate is projected to lead the market, capturing around 36% of the revenue share in 2026, supported by its universal appeal and strong indulgence association. Cocoa naturally complements plant-based bases such as almond, oat, and coconut, helping mask any subtle aftertastes while enhancing richness. Dark chocolate options attract health-conscious consumers due to perceived antioxidant benefits and reduced sugar positioning. For example, many leading non-dairy brands prioritize chocolate as a flagship SKU to anchor their product portfolio.

Vanilla is likely to be the fastest-growing flavor type in 2026, driven by versatility and clean-label appeal. Consumers increasingly favor simple ingredient lists and authentic flavors, positioning vanilla as a premium yet approachable choice. Its neutral profile allows manufacturers to highlight the quality of the plant base, whether almond, oat, or coconut. Vanilla also serves as a foundation for mix-ins such as nuts, fruit swirls, and chocolate chips, expanding product customization opportunities. For example, premium non-dairy brands frequently introduce pure vanilla bean variants to emphasize craftsmanship and base quality.

Regional Insights

North America Non-Dairy Ice Cream Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by strong consumer demand for plant-based indulgence, health-consciousness, and sustainability. Health and wellness trends are central, with a growing number of shoppers seeking lactose-free, lower-cholesterol, and clean-label dessert alternatives. This trend is especially strong among millennials and Gen Z consumers, who choose non-dairy options for health, environmental, and ethical reasons. Retailers are responding by expanding freezer aisle space dedicated to plant-based desserts, and mainstream grocery chains now prominently feature non-dairy pints alongside traditional dairy.

Innovation and product differentiation are key competitive trends in the U.S. market, supported by both established players and agile newcomers. Many companies focus on enhancing texture and flavor to narrow the sensory gap with dairy ice cream, often through advanced plant protein and fat technologies. For example, Van Leeuwen Artisan Ice Cream has expanded its non-dairy portfolio using oat and coconut bases, positioning its vegan pints as premium alternatives that deliver rich mouthfeel and bold flavors.

Europe Non-Dairy Ice Cream Market Trends

Europe is likely to be a significant market for non-dairy ice cream in 2026, due to strong consumer awareness of plant-based diets, environmental sustainability, and animal welfare concerns. Countries such as the U.K., Germany, France, and the Netherlands are at the forefront of adoption, driven by high vegan and flexitarian populations. European consumers increasingly demand clean-label, organic, and non-GMO formulations, encouraging manufacturers to innovate with oat, almond, and coconut bases. Retailers across the region have significantly expanded private-label plant-based frozen dessert ranges, improving affordability and mainstream penetration.

Product innovation and premiumization remain defining trends across the European market. Manufacturers are focusing on artisanal flavors, reduced-sugar recipes, and locally-sourced ingredients to align with regional taste preferences. For example, Unilever has expanded its plant-based ice cream portfolio in Europe under well-known brands, introducing dairy-free variants that leverage established brand trust while meeting vegan certification standards. This strategy allows multinational companies to scale distribution quickly through supermarkets and convenience channels.

Asia Pacific Non-Dairy Ice Cream Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the non-dairy ice cream market in 2026, driven by high lactose intolerance prevalence, expanding middle-class populations, and growing urbanization. Countries such as China, Japan, India, and key Southeast Asian nations are witnessing rising awareness of plant-based diets, particularly among younger consumers influenced by food trends. Local availability of raw materials such as coconut, soy, and rice strengthens regional manufacturing advantages and cost efficiency. E-commerce growth and improvements in cold-chain logistics are expanding product accessibility beyond metropolitan cities into tier-two and tier-three urban centers.

Innovation and localization remain central to Asia Pacific market dynamics. Manufacturers are adapting flavor profiles to regional preferences, incorporating tropical fruits, matcha, red bean, and other culturally relevant ingredients to enhance appeal. For example, Häagen-Dazs has expanded plant-based frozen dessert offerings in parts of Asia by leveraging strong distribution networks and tailoring flavors to local tastes. Domestic brands are also strengthening their presence by emphasizing affordability and traditional ingredient familiarity. Investments in production capacity, strategic partnerships, and improved packaging technologies are enhancing scalability.

Competitive Landscape

The global non-dairy ice cream market exhibits a moderately fragmented structure, driven by a mix of multinational food companies and nimble specialty brands catering to diverse consumer preferences worldwide. Market participation ranges from legacy consumer packaged goods firms expanding their plant-based portfolios to vegan-focused startups innovating in texture and flavor. Regional players also contribute to competitive intensity, particularly in Asia Pacific and Europe where localized taste profiles and ingredient sourcing shape product offerings.

With key leaders including Unilever, General Mills, Danone, Bliss Unlimited, Eden Creamery, Swedish Glace, NadaMoo, Tofutti, Happy Cow, Over The Moo, The Booja-Booja, Trader Joe’s, and Van Leeuwen Artisan Ice Cream, the competitive landscape blends heritage brands with emerging innovators. These players compete through ongoing innovation in plant-based bases such as almond, oat, coconut, and hybrid formulations, extensive distribution across supermarkets, specialty stores, and online retail, and strategic marketing that highlights health, sustainability, and sensory quality.

Key Industry Developments:

- In August 2025, Japanese food tech startup Kinish launched a new plant-based ice cream brand, The Rice Creamery, offering rice-based ice creams with 60% less sugar and 62% lower greenhouse gas emissions than traditional dairy options. The initial lineup includes three flavors: The Original (rice with cashew nut paste), Master’s Uji Matcha (with Uji matcha), and Elegant Dutch Chocolate (with Dutch cocoa powder). Launched at Tokyu Store, the brand targets dairy-free demand in Japan due to milk allergies, lactose intolerance, and environmental awareness. Kinish plans to expand distribution to other mass retailers, convenience stores, and internationally to Washington DC, USA, under the brand name The Rice Cream.

- In July 2025, Lidl relaunched its Ben & Jerry’s-style Vemondo vegan ice cream tubs in the UK, just in time for National Ice Cream Month. The returning flavors include Cookie Dough, Choco Fudge Brownie, and Peanut Butter Cookie, previously introduced in 2023. These tubs are available at an RRP of US$2.43 per 500ml and are part of Lidl’s seasonal plant-based offerings, which also include limited-time waffle cones and sorbet ice cream balls. The relaunch reflects growing consumer demand for affordable, indulgent vegan frozen desserts and Lidl’s commitment to expanding its plant-based product range.

Companies Covered in Non-Dairy Ice Cream Market

- Bliss Unlimited

- Danone

- Dream

- Eden Creamery

- General Mills

- Happy Cow

- NadaMoo

- Over The Moo

- Swedish Glace

- The Booja-Booja

- Tofutti Brands

- Trader Joe’s

- Unilever

- Van Leeuwen Artisan Ice Cream

Frequently Asked Questions

The global non-dairy ice cream market is projected to reach US$3.8 billion in 2026.

The non-dairy ice cream market is driven by rising lactose intolerance, growing vegan and flexitarian diets, and increasing demand for healthier, plant-based alternatives.

The non-dairy ice cream market is expected to grow at a CAGR of 15.3% from 2026 to 2033.

Key market opportunities include innovation in plant-based bases, functional ingredients, and expansion of oat and almond-based products in emerging and premium segments.

Bliss Unlimited, Danone, Dream, Eden Creamery, General Mills, Happy Cow, NadaMoo, and Over the Moo are the leading players.