- Processed Food

- Dairy-free Yogurt Market

Dairy-free Yogurt Market Size, Share, and Growth Forecast 2026 - 2033

Dairy-free Yogurt Market by Source (Soy, Almond, Coconut, Oat, Others), by Flavor (Plain, Strawberry, Vanilla, Mango, Mixed flavors), by Sales Channel (B2B, B2C), by Regional Analysis, 2026 - 2033

Dairy-free Yogurt Market Share and Trends Analysis

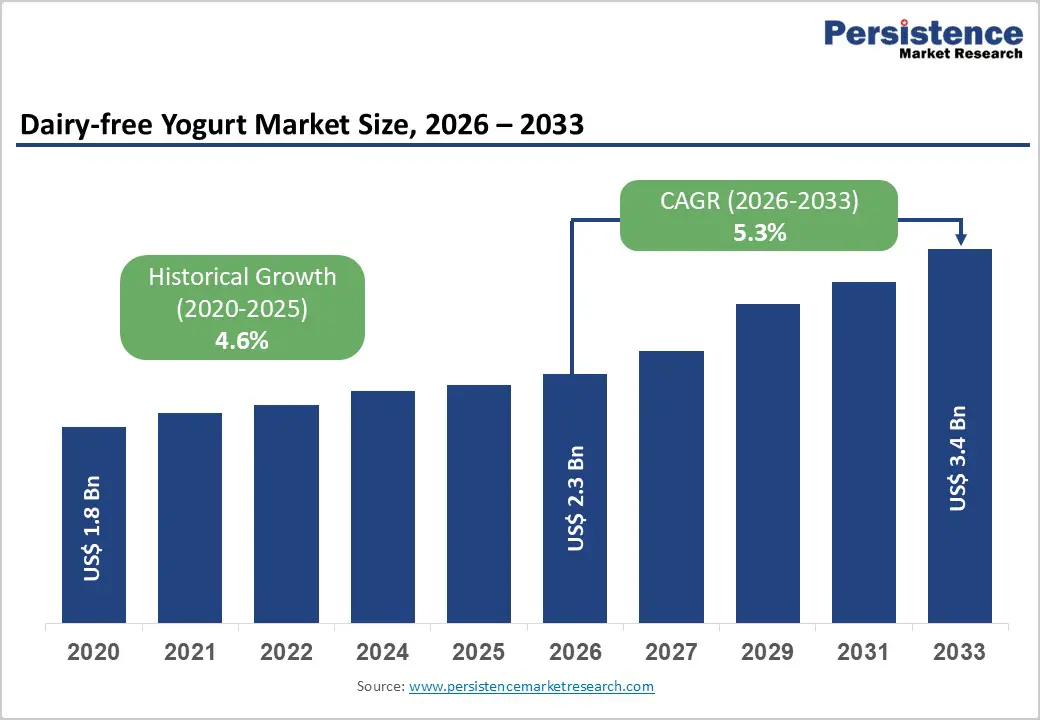

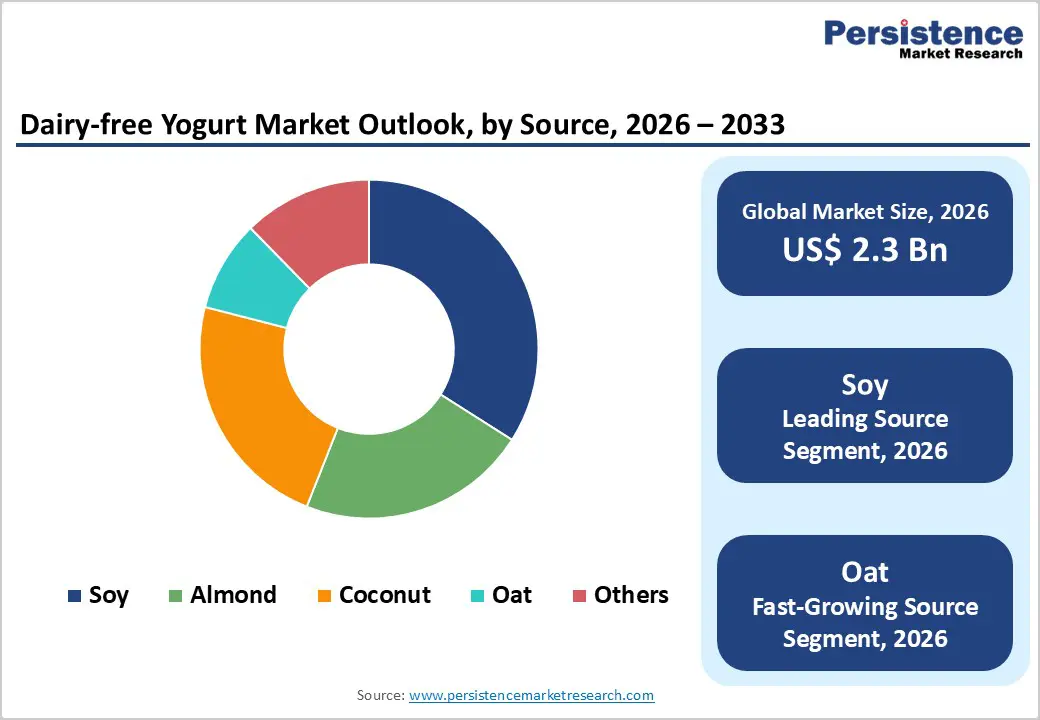

The global dairy-free yogurt market size is expected to be valued at US$ 2.3 billion in 2026 and projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. Strong momentum comes from rising lactose intolerance and dairy allergy prevalence, the rapid adoption of vegan and flexitarian diets, and increasing scrutiny of the environmental footprint of conventional dairy.

High lactose malabsorption rates across Asia, Africa, and Latin America, often exceeding 70% of the population, are structurally shifting consumers toward dairy alternatives. At the same time, nutrition research showing that plant-based yogurts offer lower sugar and sodium with higher fiber than dairy has reinforced their “better-for-you” positioning, encouraging repeat purchases and premium line extensions.

Key Industry Highlights:

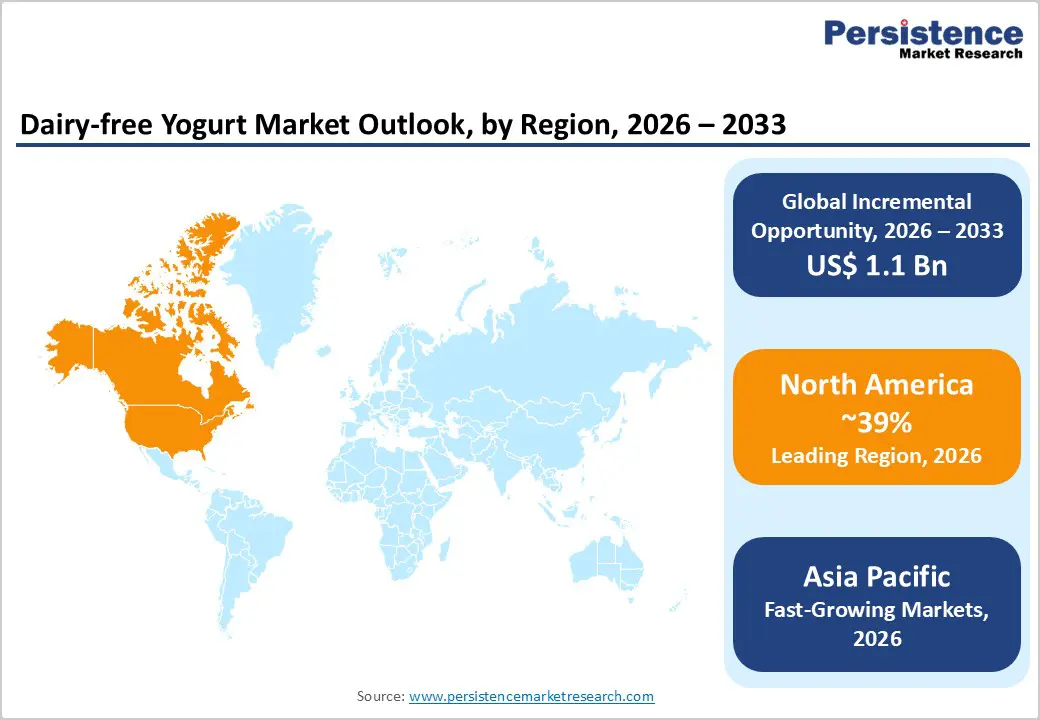

- North America remains the leading region in the dairy-free yogurt market, accounting for 39% share in 2025, supported by high health awareness, strong retail infrastructure, and continuous innovation from mainstream brands and start-ups in flavored cups and drinkable formats.

- Asia Pacific is the fastest-growing region, driven by lactose intolerance levels approaching 90% in several East Asian markets, rapid urbanization, and expanding cold-chain and e-commerce networks that facilitate access to dairy-free yogurts across income segments.

- Soy-based dairy-free yogurt is the dominant source segment with roughly 34% share in 2025, owing to its higher protein content, long-standing consumer familiarity, and efficient global supply chains that support both mainstream and value-focused product positioning.

- Oat-based dairy-free yogurt represents a standout growth segment as studies show oat yogurts closely mirror the nutrient profiles of low- and nonfat dairy yogurts, supporting premium, health-focused launches that address fiber, heart health, and sustainability concerns.

- A key market opportunity lies in fortified almond- and oat-based dairy-free yogurts, where nutrient-density research supports the addition of protein, calcium, and vitamins D and B12, enabling brands to target children, sports-oriented consumers, and older adults seeking complete dairy alternatives.

| Key Insights | Details |

|---|---|

| Dairy-free Yogurt Market Size (2026E) | US$ 2.3 billion |

| Market Value Forecast (2033F) | US$ 3.4 billion |

| Projected Growth CAGR (2026 - 2033) | 5.3% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Rising lactose intolerance and flexitarian dietary shifts

One of the strongest demand drivers for dairy-free yogurt is the high and regionally concentrated prevalence of lactose intolerance and lactose malabsorption. Meta-analyses through online studies show lactose malabsorption affecting around 90% of adults in East Asian countries and over 70% in many Middle Eastern and African populations, compared with roughly 28% in Northern, Southern, and Western Europe and around 42% in North America. Country-level data similarly indicate rates of 90% in China and Japan, around 50% in India, and 60-80% or higher in markets such as Brazil, Mexico, and Saudi Arabia, underscoring the scale of demand for dairy-free options. As consumers in these regions gain purchasing power and exposure to Western-style chilled snacks, dairy-free yogurt becomes a convenient format to access probiotics and snack-style nutrition without gastrointestinal discomfort, amplifying growth beyond traditional lactose-free dairy.

Perceived health and sustainability benefits of plant-based yogurt

Clinical and nutritional evaluations of plant-based yogurts have strengthened their health halo, supporting both premium pricing and mainstream penetration. A 2023 study in Frontiers in Nutrition comparing dairy and plant-based yogurts found that plant-based products contain significantly less total sugar and sodium, while providing substantially more dietary fiber, though typically with lower protein and calcium than dairy yogurt. Complementary work published in Nutrients that assessed 249 non-dairy yogurt alternatives reported that at least one-third of products delivered ≥5 g of protein per serving, while 93% were low in sodium, reinforcing their appeal to health-conscious consumers.

Market Restraints

Nutrient gaps versus dairy and inconsistent fortification

Despite strong demand, nutrient profile gaps relative to dairy yogurt remain a key restraint for some consumers and health professionals. The Nutrients cross-sectional review of 249 plant-based yogurt alternatives found that only about 45% of products were fortified to at least 10% of the daily value for calcium per serving, and roughly 20% achieved similar levels for Vitamins D and B12, nutrients typically abundant in dairy. While at least one-third of products contained ≥5 g of protein per serving and most were low in sodium, the combination of lower protein density and patchy fortification means many offerings still fall short of replicating the full micronutrient package of conventional yogurt, constraining adoption among families, older adults, and clinical nutrition stakeholders.

Price premiums and sensory challenges in some bases

Price and sensory performance are additional barriers to faster penetration. Ongoing academic and trade analyses show that coconut-based yogurts, while popular for their indulgent texture, tend to have the poorest nutrient density and the highest energy density among plant-based options, raising concerns for calorie-conscious consumers. Achieving a creamy texture and a familiar tang while maintaining clean labels, low sugar, and stable emulsification can increase formulation and ingredient costs, often resulting in shelf prices above those of conventional dairy yogurt. In price-sensitive markets, this premium, combined with lingering perceptions that some non-dairy yogurts have off-flavors or chalky textures, can limit trial and repeat purchase relative to other plant-based categories like milk or beverages.

Market Opportunities

Oat- and almond-based formulations with enhanced nutrition and functionality

Oat and almond bases represent particularly attractive opportunity areas, aligning nutrient density, taste, and sustainability narratives. A Frontiers in Nutrition analysis showed that almond-based yogurts scored the highest on nutrient density among evaluated plant-based and dairy yogurts, while oat-based yogurts were nutritionally closest to low- and nonfat dairy in terms of macro- and micronutrient balance. Another report noted that plant-based yogurts overall contained less sugar and sodium, but more fiber, than dairy yogurts, suggesting that fortification strategies can be layered on top of this inherently favorable profile. For market participants, this creates headroom to position almond and oat formulations as “next-generation” dairy-free yogurts with added protein, calcium, vitamins D and B12, and functional ingredients (probiotics, prebiotics, omega fats) tailored to digestive health, immunity, sports recovery, and women’s health, particularly in premium retail and online channels.

Category-wise Analysis

Flavor Insights

Within the flavor segment, strawberry typically emerges as the leading dairy-free yogurt flavor thanks to its broad cross-age appeal, strong association with fruit-based snacking, and adaptability across coconut, soy, almond, and oat bases. Analyses of the broader US yogurt market highlight strawberries and mixed berries as among the most popular flavors in both dairy and non-dairy portfolios, suggesting strong consumer preference continuity as shoppers migrate toward dairy-free options. For manufacturers, strawberry offers a familiar, low-risk profile that pairs easily with clean-label sweeteners and inclusions like real fruit pieces or granola, helping brands position products as both indulgent and wholesome. The flavor also works effectively in drinkable yogurts and multipacks, sustaining high rotation in mass retail, club formats, and convenience channels where decision time is short, and consumers gravitate toward known favorites.

Sales Channel Insights

The dairy-free yogurt market is predominantly driven by B2C sales through modern retail, online grocery, and specialty natural stores, with B2B channels (foodservice, institutional catering, industrial use) playing a supportive but smaller role. Evidence from the European plant-based milk category shows that off-trade channels, primarily supermarkets and hypermarkets, command the overwhelming majority of sales, while on-trade channels represent less than 3% of value, underscoring the dominance of retail-led distribution in dairy alternatives. This pattern carries over to dairy-free yogurt, where chilled shelf placement alongside dairy yogurt, cross-merchandising with granola and smoothies, and growing e-commerce visibility via subscription and direct-to-consumer models underpin the B2C segment’s leadership. As retailers expand plant-based sets and introduce dairy-free private labels, B2C will remain the core growth engine, with B2B gaining importance through menu innovations in cafés, quick-service restaurants, and corporate catering.

Regional Insights

North America Dairy-free Yogurt Market Trends and Insights

North America continues to lead the dairy-free yogurt market with strong and sustained momentum driven by evolving consumer preferences and robust industry dynamics. The region accounts for a significant share of the global market due to high awareness of lactose intolerance, rising adoption of plant-based diets among millennials and Gen Z, and growing demand for clean-label, sustainable food options. Product innovation is a key trend, with manufacturers expanding portfolios across soy, almond, oat and coconut bases, enhancing texture, flavor variety and nutritional profiles such as probiotics and added protein to meet diverse consumer needs. Retail penetration through supermarkets, hypermarkets and online channels further supports widespread availability and convenience. The United States dominates the regional scene, while Canada registers notable growth as plant-based procurement mandates and health trends strengthen demand. Additionally, consumer focus on health benefits, ethical eating and environmental sustainability continues to fuel the shift from traditional dairy to dairy-free alternatives, keeping North America at the forefront of market growth and product leadership in this category.

Asia Pacific Dairy-free Yogurt Market Trends and Insights

The Asia Pacific dairy-free yogurt market is emerging rapidly as a significant growth region, driven by shifting consumer preferences and broader lifestyle changes. Rising health consciousness and increasing awareness of lactose intolerance are encouraging more consumers to seek plant-based alternatives like soy, almond, oat and coconut yogurts, especially in urban and younger demographics. Countries such as China, India, Japan and Australia are witnessing wider availability of non-dairy options through supermarkets, specialty stores and e-commerce platforms, which is expanding market reach and trial. Functional benefits such as gut-health probiotics and low-sugar formulations are also gaining traction, aligning with a growing demand for wellness-oriented foods. Additionally, the rising trend toward vegan and flexitarian diets, partly influenced by sustainability and environmental concerns, is contributing to the adoption of dairy-free yogurts as lifestyle products. With plant-based alternatives projected to grow faster than traditional dairy variants in the region, Asia Pacific is expected to remain one of the fastest-growing markets globally for dairy-free yogurt in the coming years.

Competitive Landscape

The dairy-free yogurt market is highly competitive, with both large established food companies and agile plant-based specialists vying for consumer attention. Rivalry centers on product innovation, especially improvements in taste, texture, flavors, and nutritional benefits like probiotics and high protein, to differentiate offerings. Companies also compete through brand positioning, sustainability claims, clean-label ingredients, and broadening distribution across retail and digital channels. Strategic partnerships, mergers, and private label entries further intensify competition, while regional and niche players tap local tastes and premium segments to carve out market share.

Key Developments:

- In January 2026, King International launched its dairy-free yogurt range in Hong Kong as part of its Asia-Pacific expansion, introducing Greek-style and fruit-flavored plant-based yogurts into selected premium and mainstream retail outlets in the market.

Companies Covered in Dairy-free Yogurt Market

- Danone

- Chobani

- Kite Hill

- Silk

- So Delicious Dairy Free

- Forager Project

- COYO

- The Coconut Collaborative

- Califia Farms

- Ripple Foods

- Lavva

- Good Karma Foods

Frequently Asked Questions

The global dairy-free yogurt market is expected to reach approximately US$ 2.3 billion in 2026, reflecting solid expansion from 2020 levels as lactose-intolerant, vegan, and flexitarian consumers increasingly adopt plant-based yogurt as a mainstream staple.

Key demand drivers include high and regionally concentrated lactose intolerance rates, often exceeding 70-90% in parts of Asia and Africa, alongside the growth of vegan and flexitarian diets and evidence that plant-based yogurts generally contain less sugar and sodium and more fiber than dairy yogurt.

North America is the leading regional market, accounting for around 39% of global dairy-free yogurt sales in 2025, supported by strong health and wellness trends, advanced chilled retail infrastructure, and continuous innovation from brands such as Danone and Chobani.

A major opportunity lies in premium, fortified almond- and oat-based dairy-free yogurts that leverage strong nutrient-density profiles and fortification with protein, calcium, and vitamins D and B12 to address needs in children’s nutrition, active lifestyles, and healthy aging segments.

Prominent players include Danone, Chobani, Kite Hill Silk, So Delicious Dairy Free, Forager Project, COYO, The Coconut Collaborative, Califia Farms, Ripple Foods, Lavva, Good Karma Foods, as well as regional and private-label brands expanding their dairy-free portfolios.