ID: PMRREP3148| 200 Pages | 6 Jan 2026 | Format: PDF, Excel, PPT* | Healthcare

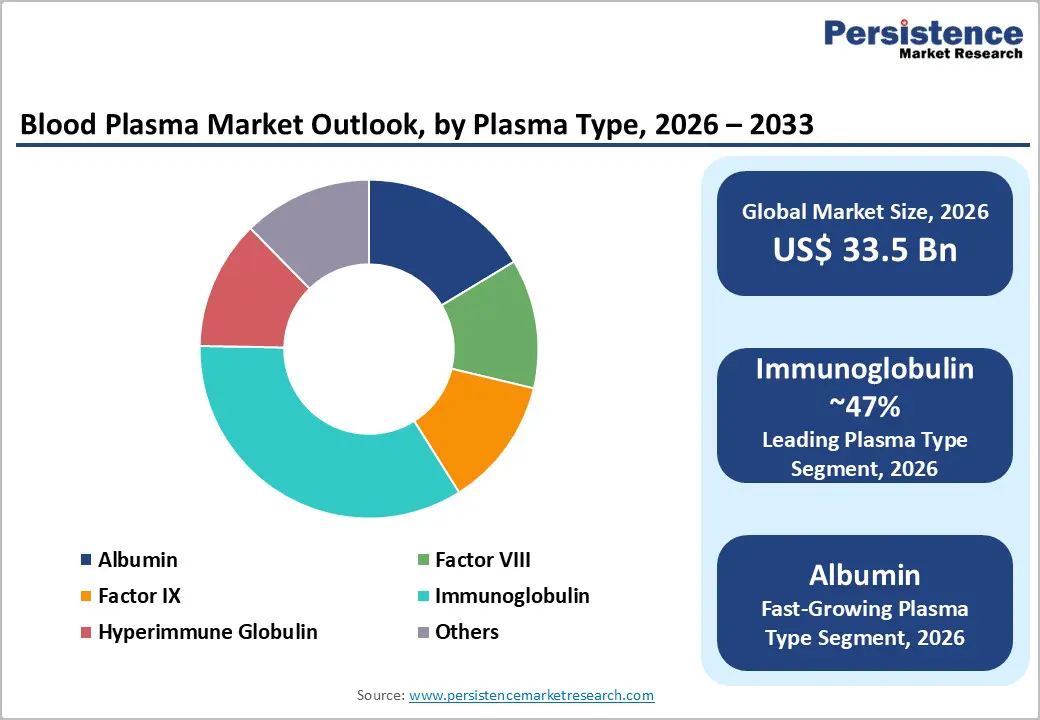

The global blood plasma market size is expected to be valued at US$ 33.5 billion in 2026 and projected to reach US$ 54.2 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Plasma is the liquid portion of the blood. Plasma is the versatile component and makes about 55% of the blood. Plasma is the composite mixture of more than 700 proteins and other substances which are vital for the efficient functioning of the human body. Plasma helps in regulating body temperature and blood pressure.

It serves as a medium for exchange of proteins, nutrients and hormones to the different parts of the body. Clotting factor, albumin and immunoglobulin are some of the major proteins found in plasma. Plasma is extracted as proteins and substances and used as main ingredients in medical products to replace body fluids, clotting factors and antibodies. Plasma is used as a component for the treatment of serious health problems such as hemophilia and autoimmune disorders.

| Global Market Attributes | Key Insights |

|---|---|

| Blood Plasma Market Size (2026E) | US$ 33.5 Bn |

| Market Value Forecast (2033F) | US$ 54.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 6.3% |

Driver – Rising burden of immunodeficiency and autoimmune disorders

Growing prevalence of primary and secondary immunodeficiency disorders is a key demand catalyst for plasma derived immunoglobulin therapies. The World Health Organization (WHO) and clinical registries recognize thousands of patients worldwide with primary immunodeficiency, but improved diagnosis is rapidly expanding identified cases, especially in North America, Europe, and Asia. Intravenous and subcutaneous immunoglobulins are now standard of care for many primary and secondary immune deficiencies, as well as autoimmune conditions such as chronic inflammatory demyelinating polyneuropathy and immune thrombocytopenia, often requiring lifelong, high volume dosing. This chronic therapy profile, combined with expanding indications in neurology and hematology, structurally underpins growing consumption of plasma protein therapeutics and supports the dominance of the immunoglobulin segment within the blood plasma market.

Expansion of plasma collection infrastructure and technology

Global plasma supply has increased significantly over the last decade as major fractionators expand plasmapheresis networks and introduce higher yield collection technologies. In the U.S, which contributes the majority of plasma for fractionation, there are more than 1,200 active plasma collection centers, and the number of facilities has grown by over 50% in recent years, driven by operators such as CSL, Grifols, Takeda (BioLife), and Octapharma. Next generation automated plasmapheresis systems, including the Rika system deployed at CSL centers, can increase donation yield per session by around 10%, lowering cost per liter and improving operational efficiency. These investments boost the availability of starting plasma for albumin, clotting factors, and immunoglobulins, enabling manufacturers to meet rising clinical demand and sustain robust revenue growth across therapeutic segments.

Restraints – Supply–demand imbalance and risk of product shortages

Despite ongoing investments, the balance between global plasma supply and demand for plasmaderived medicinal products remains tight, especially for polyvalent immunoglobulins. Disruptions in donor participation, logistical constraints, or regulatory interventions can trigger shortages, which have been observed periodically in several regions and therapeutic classes. Such shortages force clinicians to prioritize the most critical indications, delay treatment initiation, or switch patients to less preferred alternatives, thereby constraining near term volume growth and exposing the market to volatility.

Stringent regulatory requirements and high manufacturing complexity

Plasma fractionation is heavily regulated due to the biological origin of products and the need to ensure viral safety, traceability, and batch consistency. Authorities such as the European Medicines Agency (EMA) and national regulators enforce rigorous standards for donor selection, pathogen inactivation, and quality control, as outlined in guidelines for plasma derived medicinal products. Compliance with these requirements necessitates large scale investments in manufacturing facilities, validation studies, and pharmacovigilance, which raises barriers for new entrants and increases production costs. These factors can limit pricing flexibility, extend time to market for new products, and deter smaller players from expanding capacity, mildly tempering overall market growth.

Opportunity – High growth potential in albumin and emerging therapeutic uses

The albumin segment is poised to be the fastest growing plasma type, supported by expanding utilization beyond traditional indications such as liver cirrhosis and hypovolemia into critical care and perioperative settings. Clinical data support albumin’s role in fluid resuscitation, sepsis management, and large volume paracentesis, while ongoing research explores benefits in stroke, cardiac surgery, and drug delivery applications. Emerging markets in Asia Pacific are significantly increasing albumin consumption as healthcare infrastructure improves and intensive care services scale up, with China and India displaying rapid adoption in tertiary hospitals. As production yields improve and fractionators optimize product portfolios, albumin offers an attractive revenue growth pocket within the broader blood plasma market.

Growing demand for plasma derived therapies in rare and chronic disorders

Opportunities are expanding in niche indications such as hereditary angioedema, von Willebrand disease, and specific coagulation factor deficiencies where plasma derived factor concentrates remain essential, particularly in countries with limited access to recombinant products. For example, plasma derived Factor VIII and Factor IX continue to play a major role in managing hemophilia in low and middle income markets due to cost advantages and established clinical familiarity. At the same time, hyperimmune globulins targeting pathogens or specific antigens (e.g., for emerging infectious diseases) are under development, offering new therapeutic avenues and premium pricing potential. Collectively, these rare and chronic disease segments provide high margin opportunities for manufacturers that can secure reliable plasma supply, navigate regulatory pathways, and build specialized commercial capabilities.

By Plasma Type Analysis

The immunoglobulin segment accounted for 47% of global blood plasma revenues around 2025 and is expected to remain the leading plasma type in 2025. This dominance reflects its broad label coverage across primary and secondary immunodeficiency, autoimmune neuromuscular disorders, immune thrombocytopenia, and various off label uses, often involving chronic, high dose regimens. Clinical guidelines in North America and Europe increasingly recommend immunoglobulin for a widening spectrum of conditions, while aging populations and rising cancer survivorship further expand the immunocompromised patient base. As a result, immunoglobulins generate the highest revenue per liter of plasma and drive a substantial portion of fractionation economics, cementing their leadership within the plasma type category.

By End-User Analysis

Hospitals are projected to remain the dominant end-user segment in the global blood plasma market, accounting for approximately 55% share in 2025. This dominance is driven by the complex administration protocols, requirement for close patient monitoring, and widespread use of plasma and plasma-derived products in acute care settings. Hospitals are the primary sites for managing major surgeries, trauma cases, liver failure, severe infections, and critical bleeding disorders, where plasma transfusions and high-dose immunoglobulin therapies are routinely required. Advanced tertiary and quaternary care hospitals in developed markets such as the U.S., Germany, and Japan serve as referral centers for rare immunodeficiency and coagulation disorders, leading to concentrated utilization of products including Factor VIII, Factor IX, hyperimmune globulins, and specialized plasma therapies. Although clinics and outpatient infusion centers are gradually expanding their role in long-term immunoglobulin maintenance therapy, hospitals are expected to maintain clear leadership due to their central role in managing complex and emergency cases.

North America Blood Plasma Market Trends

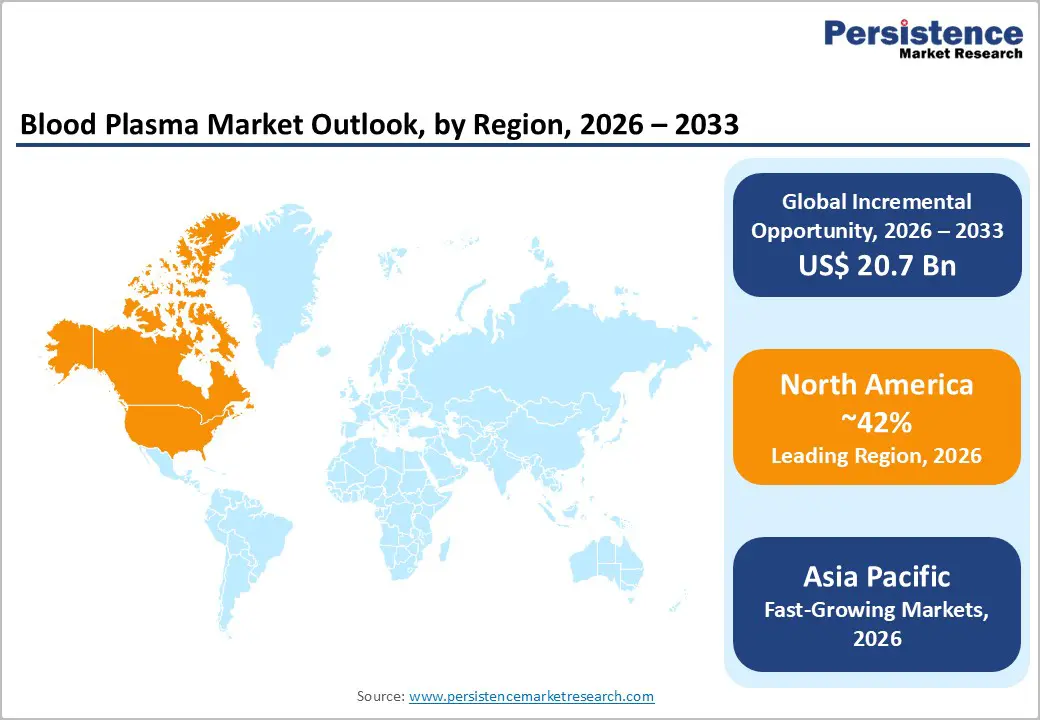

North America, led by the U.S., commands 42% of global blood plasma and plasma derived therapeutics demand, underpinned by high diagnosis rates, advanced reimbursement systems, and a dense network of plasma collection centers. The U.S. alone hosts over 1,200 FDA registered plasma donation centers, and large operators such as Grifols, CSL, Takeda (BioLife), and Octapharma own approximately 80% of these facilities, ensuring robust supply for domestic use and exports. Strong reimbursement for immunoglobulin therapies in neurology, hematology, and immunology, along with established treatment guidelines, sustains premium pricing and high per patient utilization in this region.

Innovation and regulatory oversight in North America are also pivotal. The U.S. Food and Drug Administration (FDA) continuously update standards for donor screening, viral inactivation, and manufacturing controls, which, while stringent, support confidence among clinicians and patients. Companies are piloting new plasmapheresis devices, digital donor engagement tools, and advanced fractionation technologies that reduce cost per liter and enhance product yields. These factors collectively underpin North America’s leading share in the blood plasma market and reinforce its position as a global hub for plasma collection, fractionation, and innovation.

Asia and Pacific Blood Plasma Market Trends

Asia Pacific is projected to be the fastest growing region for blood plasma, supported by rising healthcare expenditure, demographic expansion, and improving diagnosis of hematologic and immunological disorders in China, Japan, India, and ASEAN markets. China has significantly expanded its domestic plasma fractionation capacity under a regulated licensing framework, focusing on albumin and immunoglobulin supply, while Japan maintains a sophisticated market with high per capita utilization of plasma derived products and strong safety standards. India and several Southeast Asian countries are at earlier stages of market development but are witnessing rapid growth as tertiary care hospitals proliferate and clinical guidelines increasingly reference plasma derived therapies.

Manufacturing and cost advantages are also pivotal in Asia Pacific. Several countries are investing in local plasma fractionation plants and public private partnerships to reduce dependence on imports and improve pandemic preparedness. Lower labor costs and supportive industrial policies, particularly in China and India, attract investments in plasma fractionation, packaging, and ancillary technologies. As awareness campaigns, patient registries, and reimbursement programs expand across the region, Asia Pacific is expected to deliver the highest CAGR in the global blood plasma market over the forecast horizon.

The blood plasma market is moderately consolidated, with a handful of large multinational fractionators such as CSL, Grifols, Takeda Pharmaceuticals, Octapharma, and Kedrion controlling a substantial share of global plasma collection and fractionation capacity. These players compete primarily on plasma network scale, product portfolio breadth (immunoglobulins, albumin, clotting factors, hyperimmune globulins), safety record, and global distribution capabilities. Strategic initiatives include acquisitions of plasma centers, capacity expansions, investments in next generation plasmapheresis devices, and development of niche hyperimmune or specialty products, while emerging regional players and public blood establishments focus on selective product lines and domestic self sufficiency

Key Industry Developments:

The global market is projected to be valued at US$ 33.5 Bn in 2026.The global market is projected to be valued at US$ 33.5 Bn in 2026.

Rising immunodeficiency and autoimmune disorders, increased immunoglobulin and albumin use, and expanding plasma collection infrastructure with advanced plasmapheresis technologies.

The global market is poised to witness a CAGR of 7.1% between 2026 and 2033.

Developing plasma-derived therapies for rare chronic disorders like hereditary angioedema, von Willebrand disease, and coagulation factor deficiencies.

Key companies include Biotest AG, CSL, GC Biopharma Corp, Grifols, and Intas Pharmaceuticals Ltd.

| Report Attributes | Details |

|---|---|

| Historical Data/Actuals | 2020 – 2025 |

| Forecast Period | 2026 – 2033 |

| Market Analysis | Value: US$ Bn and Volume (if Available) |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Plasma Type

By Application

By End-User

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author