- Beverages

- Chocolate Beer Market

Chocolate Beer Market Size, Share, and Growth Forecast 2026 - 2033

Chocolate Beer Market by Product Type (Chocolate Ale, Chocolate Stout, Chocolate Lager, Others), Packaging Type (Glass Bottles, Cans, Kegs, Others), Distribution Channel (Online Retail, Supermarkets/Hypermarkets, Liquor Stores, Specialty Stores), and Regional Analysis, 2026 - 2033

Chocolate Beer Market Share and Trends Analysis

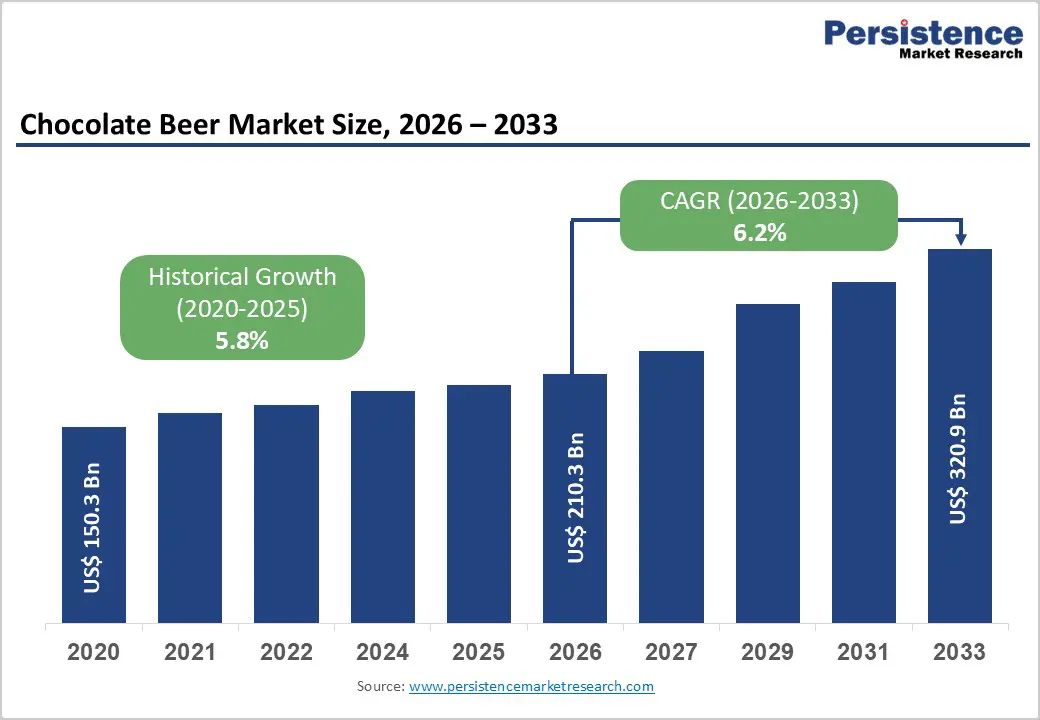

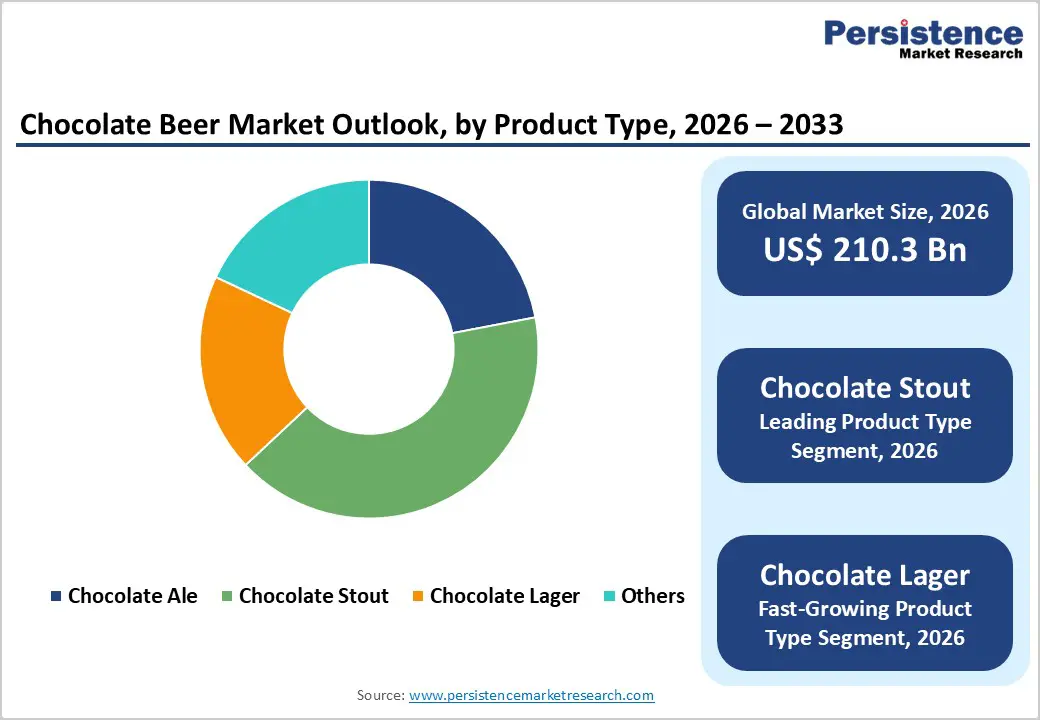

The global Chocolate Beer market size is expected to be valued at US$ 210.3 billion in 2026 and projected to reach US$ 320.9 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. The chocolate beer market is expanding at an accelerating pace, driven by the structural premiumization of the global beer industry, the explosive growth of craft brewing culture, and rising consumer demand for innovative, flavor-forward specialty beer varieties.

The proliferation of independent craft breweries, with the Brewers Association reporting over 9,500 craft breweries operating in the United States alone as of 2023, has created a fertile innovation ecosystem where chocolate-flavored ales, stouts, and lagers are among the highest-demand specialty beer segments. Simultaneously, the convergence of craft beer and artisan chocolate culture is driving premium pricing and brand storytelling that resonates strongly with millennials and affluent consumers globally.

Key Industry Highlights:

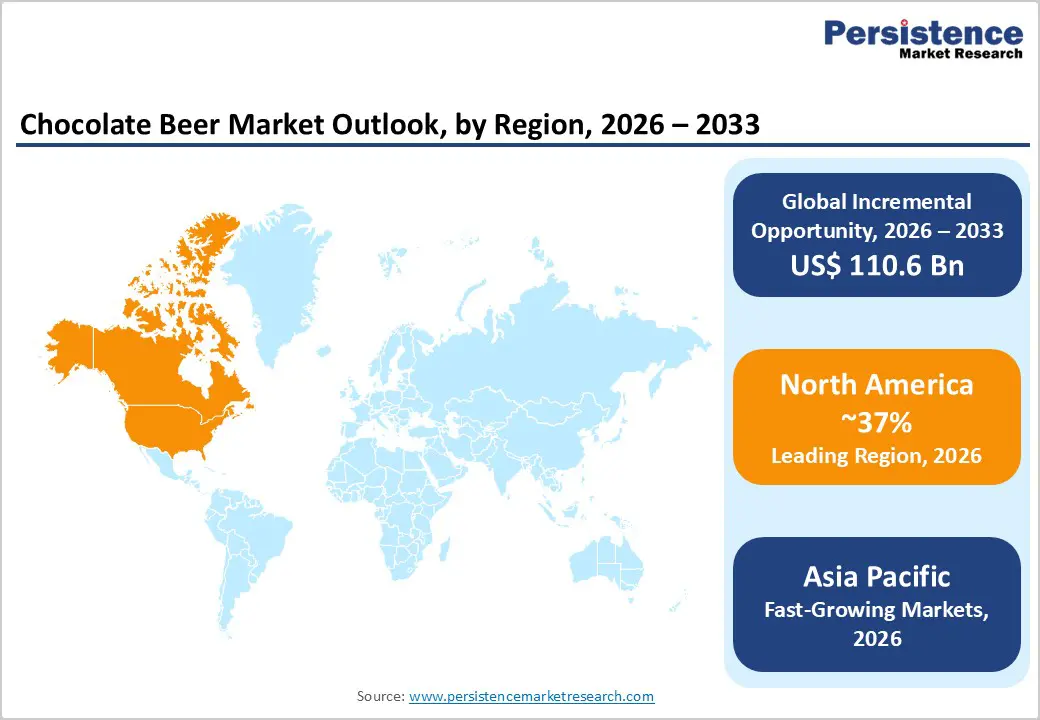

- Leading Region: North America held approximately 37% of global share in 2025, anchored by the world's most mature craft brewery ecosystem of 9,500+ independent breweries, US$ 28.9 billion in craft beer retail sales, and iconic chocolate stout brand leadership.

- Fastest Growing Market: Asia Pacific is the fastest-growing region through 2033, driven by the rise in need for premiumization, and product scaling in the specialty beer bar and retail infrastructure across Japan, South Korea, India, and Southeast Asia.

- Dominant Product: Chocolate stout accounts for approximately 41% of global product share in 2025, established as the archetypal chocolate beer style through iconic brands such as Young's Double Chocolate Stout and consistent Great American Beer Festival recognition, driving global consumer awareness.

- Fast-Growing Product: Chocolate lager is the fast-growing product type, creating the most accessible consumer entry point into the chocolate beer category by combining mainstream lager's approachability with subtle chocolate flavor notes, targeting the global 90% lager-dominant consumer base.

Market Dynamics

Drivers - Craft Beer Revolution and the Rise of Flavor-Forward Specialty Beer Segments

The shift in consumer beer preferences from mainstream lagers toward premium, craft, and specialty beers is the foundational demand driver for the chocolate beer category globally. The Brewers Association reports that U.S. craft beer retail dollar sales exceeded US$ 28.9 billion in 2023, representing approximately 29% of the total U.S. beer market by value.

Chocolate-flavored beer styles, particularly stouts and porters brewed with cocoa nibs, chocolate malt, and cacao extracts, represent some of the most widely celebrated specialty beer categories in craft beer award competitions, including the Great American Beer Festival (GABF) and the World Beer Cup. This award visibility amplifies consumer discovery and drives trial purchase behavior, creating a virtuous cycle of brand building and category growth that benefits independent craft producers.

Premiumization Trend and Consumer Willingness to Pay for Unique Sensory Beer Experiences

Growing consumer willingness to trade up to premium, experience-driven beer products, even as overall beer consumption volumes plateau in mature markets, is structurally supporting chocolate beer's above-average growth trajectory relative to mainstream lager categories. The Brewers Association notes that the average price per case of craft beer is approximately 2.5x higher than that of domestic premium lagers, reflecting strong consumer price tolerance for perceived quality and uniqueness. According to the NielsenIQ data flavored and specialty craft beers consistently outperform category growth rates in off-premise retail. The chocolate beer segment benefits directly from this premiumization dynamic, with brands such as Samuel Adams Chocolate Bock and Young's Double Chocolate Stout commanding significant price premiums that sustain superior margin profiles for manufacturers.

Restraints - Regulatory Restrictions on Alcohol Sales and Distribution in Key Markets

The chocolate beer market faces significant regulatory barriers across multiple high-potential markets where alcohol sales restrictions, including state-controlled distribution monopolies, age-based purchasing restrictions, and outright prohibition in certain jurisdictions, constrain market access and distribution channel development.

In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) mandates compliance with labeling, ingredient, and flavor additive regulations for flavored beers, adding regulatory overhead. In Middle East markets and parts of South Asia, religious and cultural prohibitions on alcohol fundamentally limit addressable market size, diverting potential consumers to non-alcoholic chocolate malt beverage alternatives.

High Production Costs of Premium Chocolate Beer Ingredients Constrain Margin Expansion

The use of high-quality chocolate ingredients, including single-origin cacao nibs, premium dark chocolate malt, and cacao powder, significantly increases ingredient costs relative to conventional beer brewing, compressing profit margins for independent craft producers who lack the purchasing scale of large brewing conglomerates.

The International Cocoa Organization (ICCO) has documented significant cacao price volatility driven by weather events and West African supply disruptions, with cocoa prices reaching multi-decade highs in 2024, creating procurement cost instability that directly impacts chocolate beer ingredient budgets and retail price positioning across the category.

Opportunities - Chocolate Lager is the Fast-Growing Product Expanding the Category's Consumer Base

Chocolate Lager represents the fastest-growing product type within the chocolate beer market, offering a significant market development opportunity by bridging the flavor preferences of mainstream lager consumers with the premium chocolate beer category. Unlike Chocolate Stout, which appeals primarily to seasoned craft beer drinkers, Chocolate Lager's lighter body, lower bitterness, and subtle cocoa flavor notes create a more accessible entry point for consumers transitioning from mainstream beer to premium specialty varieties.

The global lager beer category dominates worldwide beer consumption, representing approximately 90% of global beer volume per Kirin Holdings' annual Beer Consumption Survey. Brands and breweries that develop well-crafted chocolate lager variants, such as Moosehead Brewery and regional craft producers, are well-positioned to convert mainstream lager drinkers into the premium chocolate beer segment, significantly expanding the category's total addressable consumer base.

Category-wise Analysis

Product Type Insights

Chocolate Stout commands the leading product type share of approximately 41% of the global chocolate beer market in 2025, reflecting its status as the archetypal and most celebrated chocolate beer style globally. The stout style's naturally roasty, full-bodied character derived from heavily roasted malts provides a complementary flavor canvas for chocolate additions, producing the complex, dessert-like tasting profiles that define the chocolate beer category's premium positioning.

Iconic brands, including Young's Double Chocolate Stout (brewed by Wells & Young's), Samuel Adams Chocolate Bock, and North Coast Brewing's Old Rasputin, have built decades-long consumer loyalty around this style. The Great American Beer Festival consistently awards chocolate stouts among the most competitive judged categories, amplifying consumer awareness and driving retail discovery.

Packaging Type Analysis

Glass Bottles retain the dominant packaging share of approximately 52% of chocolate beer sales in 2025, reflecting the premium positioning of the chocolate beer category, where glass bottle packaging communicates craft provenance, artisanal quality, and product sophistication that resonates with the target consumer demographic. Specialty and limited-edition chocolate beer releases, such as seasonal chocolate stout offerings from Sierra Nevada Brewing Co. and Deschutes Brewery are almost exclusively packaged in glass bottles that enable collector-grade label designs and gift purchase positioning.

Cans are the fast-growing packaging format, driven by their superior light and oxygen protection properties, convenience advantage in outdoor consumption occasions, and growing craft can adoption led by breweries including BrewDog and New Belgium Brewing.

Distribution Channel Insights

Specialty Stores, including dedicated beer bottle shops, craft beer retailers, and gourmet food stores, lead the chocolate beer distribution channel with approximately 38% of global share in 2025, reflecting the category's premium and specialty positioning that aligns with the curated, knowledgeable retail environment these stores provide. Specialty stores enable educated staff recommendations, tasting events, and exclusive product discovery that are essential for building consumer trial and loyalty for premium chocolate beer styles.

Liquor Stores provide the broadest accessible distribution in North America and Europe. Online Retail is the fastest-growing distribution channel, driven by beer subscription services, direct-to-consumer brewery shipping (where legally permitted), and e-commerce platforms like Drizly (Uber Eats), enabling the discovery of rare and limited-edition chocolate beer releases globally.

Regional Insights

North America Chocolate Beer Market Trends and Insights

North America leads the global chocolate beer market with approximately 37% of global share in 2025, anchored by the world's most mature craft beer ecosystem with over 9,500 independent breweries per the Brewers Association. Strong consumer premiumization behavior, robust specialty retail infrastructure, and a deeply embedded craft beer culture make North America the global innovation hub for chocolate beer styles, including barrel-aged chocolate stouts and experimental chocolate lager variants.

U.S. Chocolate Beer Market Size

The United States represents approximately 85% of North American chocolate beer revenue, backed by craft beer retail dollar sales exceeding US$ 28.9 billion in 2023. Producers, including Sierra Nevada Brewing Co., Samuel Adams, Deschutes Brewery, and Lakewood Brewing Company, maintain strong chocolate beer SKUs. The U.S. leads global chocolate beer product innovation through GABF-recognized seasonal and limited-edition releases.

Europe Chocolate Beer Market Trends and Insights

Europe is the second-largest chocolate beer market, holding approximately 28% of global share in 2025, with the United Kingdom as the category's spiritual home through iconic brands such as Young's Double Chocolate Stout. The region's deep beer culture across Germany, Belgium, and the Netherlands provides fertile ground for specialty chocolate beer innovation, while BrewDog's rapid European expansion is normalizing premium craft beer pricing and creating new chocolate beer consumer segments.

Germany Chocolate Beer Market Size

Germany accounts for approximately 18–20% of the European chocolate beer market value. Despite the Reinheitsgebot (German Beer Purity Law) restricting traditional brewing, the growing craft beer movement and imported specialty beer market are enabling chocolate beer consumption growth. Emelisse Brewery products and international chocolate stout imports are gaining significant specialty retail traction in major German cities, including Berlin and Munich.

U.K. Chocolate Beer Market Size

The United Kingdom contributes approximately 25–27% of European chocolate beer revenue, anchored by its heritage of dark beer and stout brewing tradition. Young's Beers, with its globally recognized Double Chocolate Stout and BrewDog's expanding portfolio, provides strong category leadership. The Society of Independent Brewers (SIBA) reports sustained craft beer consumer premiumization in the U.K., supporting chocolate beer category growth through 2033.

France Chocolate Beer Market Size

France represents approximately 13% of the Europe chocolate beer market, with rising craft beer adoption among young urban French consumers creating growing demand for premium specialty beer styles. France's world-class culinary culture, which celebrates chocolate as a premium ingredient, provides a uniquely favorable consumer perception backdrop for chocolate beer. Ommegang Brewery and imported BrewDog products are finding growing specialty retail distribution in Paris and Lyon.

Asia Pacific Chocolate Beer Market Trends and Insights

Asia Pacific is the fast-growing regional chocolate beer market, propelled by craft beer culture spreading among young urban consumers in China, Japan, Australia, and South Korea. China's craft beer market, growing at over 20% annually per China Alcoholic Drinks Association data, is particularly receptive to imported premium specialty beers, with chocolate stout and ale variants gaining rapid traction in tier-one city craft beer bars and specialty bottle shops.

India Chocolate Beer Market Size

India represents approximately 8–10% of the Asia Pacific chocolate beer market value, with demand concentrated in metro cities where craft beer bars and specialty retail are expanding. India's beer market is growing rapidly, with premium imported brands from BrewDog and Anheuser-Busch InBev's craft portfolio gaining urban distribution. Regulatory harmonization under India's excise framework is gradually expanding licensed premium beer channel access, supporting the trajectory of growth for specialty chocolate beer.

Japan Chocolate Beer Market Size

Japan accounts for approximately 18% of Asia Pacific chocolate beer revenue, reflecting a mature premium beer consumer base with a strong affinity for complex, innovative flavor profiles. Japanese craft breweries are increasingly experimenting with chocolate-infused dark beers, while Kirin Holdings and Sapporo Breweries have launched limited-edition chocolate beer variants. Japan's gift-giving culture creates a natural premium seasonal chocolate beer market during holidays.

Southeast Asia Chocolate Beer Market Size

Southeast Asia contributes approximately 14% of the Asia Pacific chocolate beer market value, emerging as a fast-growing sub-region driven by young, internationally influenced urban consumers in Singapore, Thailand, Vietnam, and Malaysia. Craft beer bar culture is rapidly expanding across the region's major cities, with imported chocolate stouts and ales from BrewDog and Sweetwater Brewing Company gaining growing specialty retail and on-premise distribution.

Competitive Landscape

The chocolate beer market is highly competitive, driven by the rapid growth of craft brewing and rising consumer interest in flavored and specialty alcoholic beverages. Market participants are focusing on product innovation, experimenting with cocoa blends, dark malts, and dessert-inspired profiles to differentiate offerings. Seasonal and limited-edition launches are widely used to create premium appeal and boost demand. Companies are expanding distribution through taprooms, specialty liquor stores, and online channels to improve accessibility.

Key Developments:

- In June 2025, Vault City planned to launch a new luxurious beer inspired by the Dubai chocolate trend. The Dubai-Style Chocolate Pistachio Imperial Stout includes Belgian dark syrup, nut-free pistachio flavoring, brown sugar, and cacao nibs.

- In October 2024, San Miguel Brewery Inc. introduced San Miguel Chocolate Lager to extend its portfolio of brands. The Lager is a full-bodied dark beer that has a rich, dark, chocolate taste, and subtle caramel notes. It is topped with a creamy head that brings out a delectable roasted malt aroma.

Global Chocolate Beer Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 150.3 billion |

|

Current Market Value (2026) |

US$ 210.3 billion |

|

Projected Market Value (2033) |

US$ 320.9 billion |

|

CAGR (2026–2033) |

6.2% |

|

Leading Region |

North America, ~37% market share (2025) |

|

Dominant Product Type |

Chocolate Stout, ~41% market share (2025) |

|

Top-Ranking Packaging Type |

Glass Bottles, ~52% market share (2025) |

|

Incremental Opportunity |

US$ 110.6 billion |

Companies Covered in Chocolate Beer Market

- Anheuser-Busch InBev

- Deschutes Brewery

- BrewDog

- New Belgium Brewing

- North Coast Brewing Company

- Sierra Nevada Brewing Co

- Samuel Adams

- Lakewood Brewing Company

- Anderson Valley Brewing Company

- Young's Beers

- MillerCoors

- Emelisse Brewery

- Moosehead Brewery

- Sweetwater Brewing Company

- Ommegang Brewery

Frequently Asked Questions

The global Chocolate Beer market is likely to be valued at US$ 210.3 billion in 2026.

The primary demand drivers are the structural growth of the global craft beer industry with the Brewers Association reporting U.S. craft beer retail sales.

North America leads the global Chocolate Beer market with approximately 37% of global share in 2025.

The most significant near-term growth opportunities are in the Chocolate Lager segment, which bridges mainstream lager consumers with the premium chocolate beer category, targeting the global 90% lager-dominant consumer base, and in the Asia Pacific market entry, where China's craft beer market is growing at 20% annually, and Japan's premium gift beer culture offers first-mover distribution advantages for international chocolate beer brands.

The leading companies in the global Chocolate Beer market include Anheuser-Busch InBev, BrewDog, Sierra Nevada Brewing Co., Deschutes Brewery, Samuel Adams (Boston Beer Company), Young's Beers, New Belgium Brewing, North Coast Brewing Company, and Ommegang Brewery, among others.