- Beverages

- Mead Beverages Market

Mead Beverages Market Size, Share, and Growth Forecast 2026 - 2033

Mead Beverages Market by Flavor (Traditional, Fruit, Spice & Herb, Floral), by ABV (<3.5%, 3.5% - 7.5%, >7.5%), by Packaging Type (Bottles, Cans, Kegs), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Mead Beverages Market Size and Trend Analysis

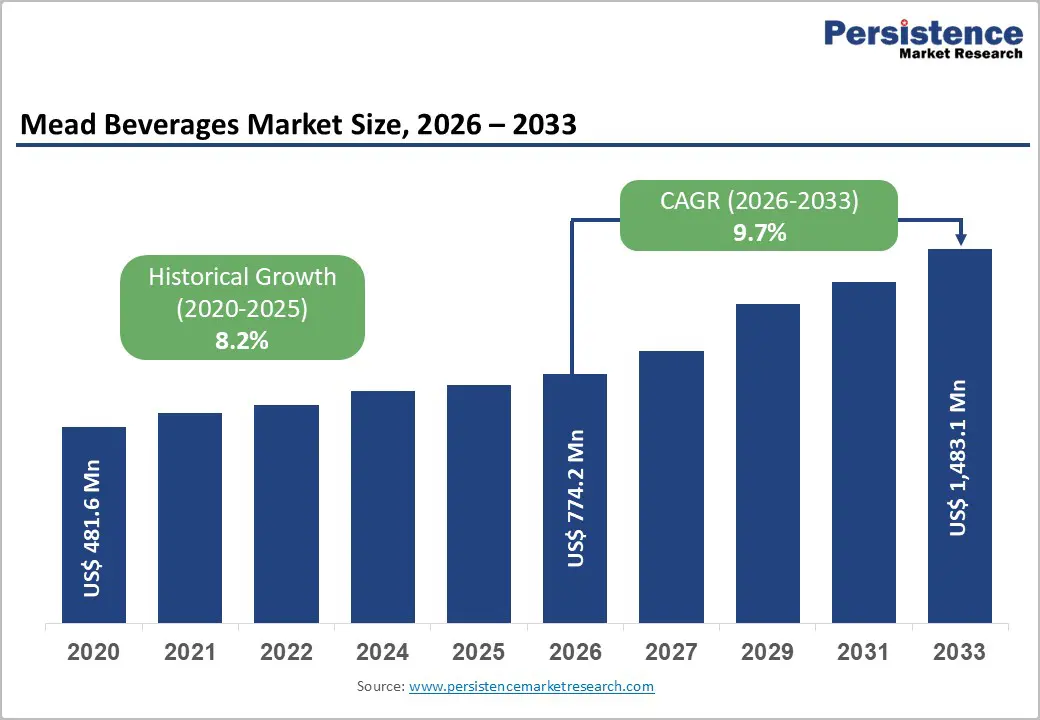

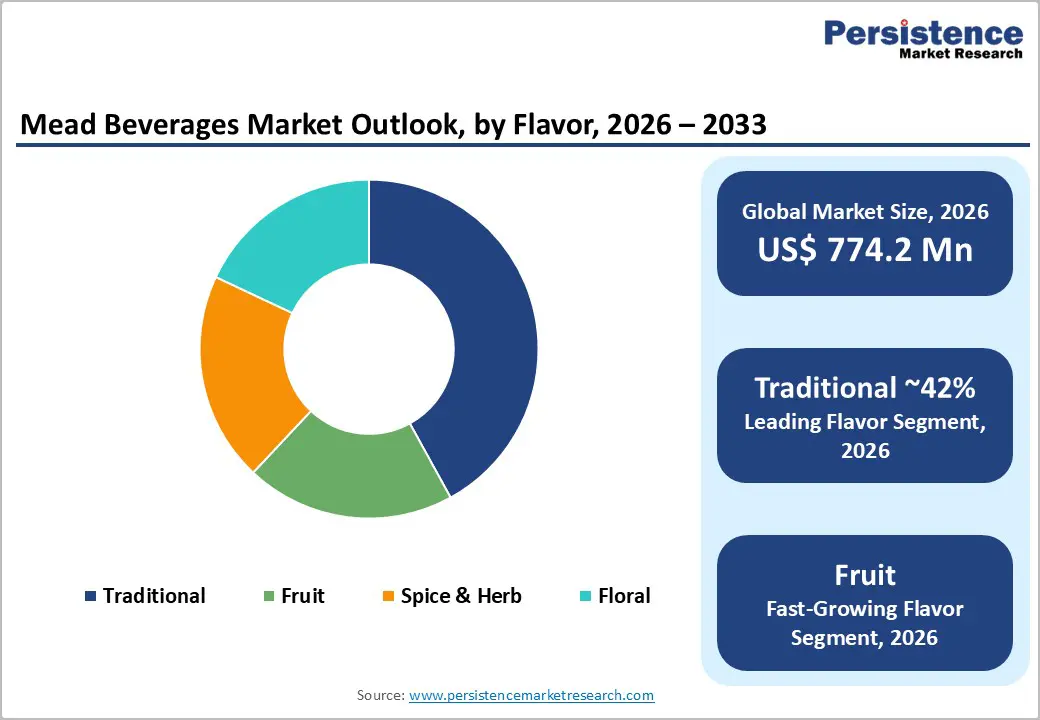

The global mead beverages market size is expected to reach US$ 774.2 million in 2026 and is projected to reach US$ 1,483.1 million by 2033, growing at a CAGR of 9.7% between 2026 and 2033. Mead, also known as honey wine, is a beverage made from honey, water, and yeast, with the occasional addition of fruits.

Mead is considered one of the oldest alcoholic beverages; mead is making a steady comeback in the modern alcohol industry, propelled by growing consumer interest in libations with a rich heritage. Its resurgence in the modern era is also attributable to the rising demand for craft beverages, especially among the young. The mead beverage market is poised to make significant gains in this scenario, as mead offers a diverse flavor profile and aligns with current health trends.

Key Industry Highlights:

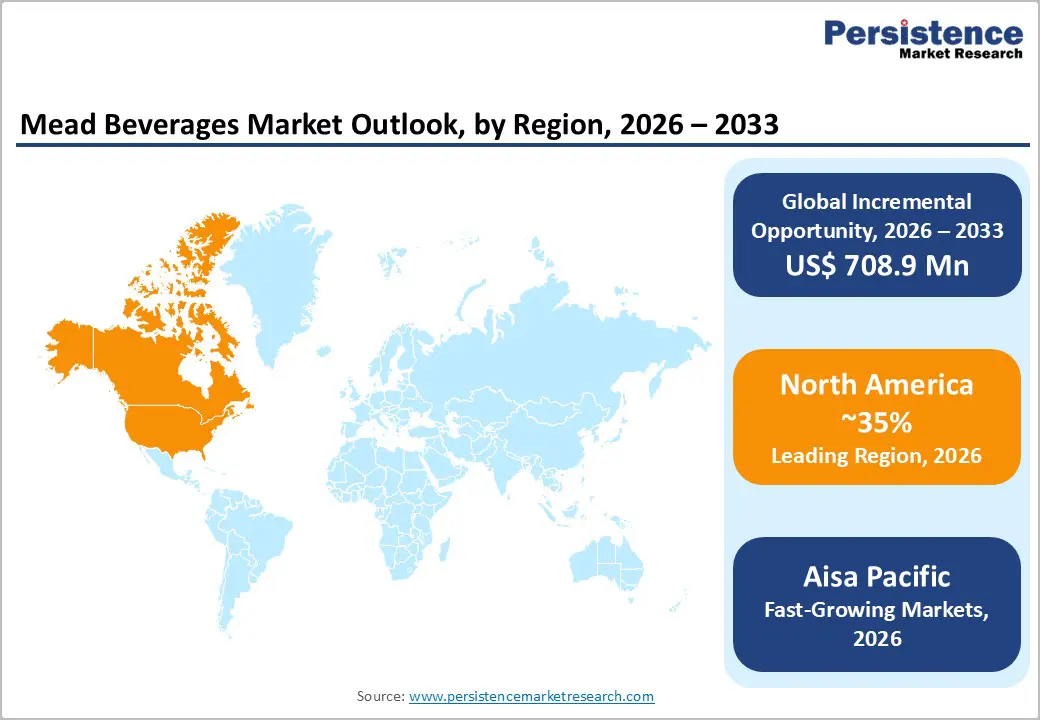

- Leading Region: North America dominates with ~35% share, driven by a well-established craft alcohol ecosystem, an increasing number of meaderies, and strong consumer demand for heritage-inspired, gluten-free, and artisanal alcoholic beverages across the U.S. and Canada.

- Fastest Growing Region: Asia Pacific is the fastest-growing region due to rising disposable incomes, increasing exposure to global craft beverages, and the emergence of local meaderies utilizing regional honey, fruits, and innovative flavor profiles to attract new consumers.

- Dominant Flavor Segment: Traditional mead holds the largest share at 42%, supported by its authenticity and classic appeal, while fruit-flavored meads are rapidly gaining traction among younger consumers seeking diverse, approachable, and innovative taste experiences.

- Dominant Packaging Type Segment: Bottled mead dominates with 62% share, as glass packaging preserves flavor, aroma, and quality while reinforcing premium positioning and appealing strongly to traditional consumers who value authenticity and presentation.

- Key Opportunity: Rising demand for traditional and artisanal alcoholic beverages presents strong growth opportunities, as consumers increasingly seek natural, heritage-based drinks, encouraging innovation in flavors, formulations, and premium product positioning in the mead market.

| Key Insights | Details |

|---|---|

|

Mead Beverages Market Size (2026E) |

US$ 774.2 million |

|

Market Value Forecast (2033F) |

US$ 1,483.1 million |

|

Projected Growth CAGR (2026-2033) |

9.7% |

|

Historical Market Growth (2020-2025) |

8.2% |

Market Dynamics

Drivers - Rising Consumer Preference for Craft, Heritage, and Gluten-Free Alcoholic Beverages

A key growth driver for the mead beverages market is the broader shift toward craft and artisanal alcoholic drinks, where authenticity, provenance, and experimentation are highly valued. Industry reports and expert commentary note that mead is benefiting from the same forces that propelled craft beer, as consumers search out small-batch products that tell a story and showcase local ingredients.

Mead’s positioning as a honey-based, often naturally gluten-free “honey wine” appeals to drinkers who have wheat intolerance or who are seeking alternatives to beer, while its broad flavor spectrum from dry to sweet and still to sparkling allows producers to target wine, cider, and cocktail consumers alike. According to the 2024 Brewers Association report, the craft brewing sector in North America and Europe remains robust, with over 9,700 U.S. craft breweries in 2023, rising to nearly 9,800 in 2024, creating retail and on-premise ecosystems that are comfortable promoting niche categories such as mead alongside beer, cider, and hard seltzer.

Cultural Renaissance of Mead as an Ancient yet Contemporary Beverage

Mead’s historical and cultural resonance is another powerful driver, especially among younger adult consumers influenced by popular culture and interest in traditional foodways. Educational features from institutions such as Encyclopedia Britannica and the UC Davis Honey and Pollination Center describe mead as one of the world’s oldest alcoholic beverages, with evidence of honey-based fermentation dating back thousands of years and deep roots in Celtic, Norse, and Anglo-Saxon cultures.

Modern storytelling around “Viking” drinks and fantasy franchises such as Game of Thrones® has helped raise awareness of mead, triggering curiosity-driven trial among consumers seeking something different from mainstream wine or beer. Producers are leveraging this by emphasizing traditional methods, single-origin honeys, and regional botanicals while also creating sessionable, lower-ABV formats that fit contemporary drinking habits and tasting-room flight experiences.

Restraints - Regulatory Complexity and Intense Competition Within Craft Alcohol

Mead producers often face regulatory ambiguity because mead can be classified as wine, beer, or a specialty product depending on jurisdiction, composition, and alcohol content, leading to differing requirements for licensing, taxation, and distribution. In the U.S., state-level variations in rules on direct-to-consumer shipping, on-premise sales, and self-distribution can constrain smaller meaderies’ ability to reach consumers beyond their local markets, even as interest in e-commerce rises.

Mead competes with a crowded landscape of craft beers, hard seltzers, flavored malt beverages, and ready-to-drink cocktails in a beer market where overall volume declined by around 1–2% in 2024, suggesting pressure on discretionary alcohol spending. These structural challenges can temper the speed at which mead scales, particularly for brands without strong distribution partnerships or marketing resources.

Opportunities - Formulation of Low-Sugar and Probiotic Meads to Push Market Scope

The growing shift toward healthier lifestyles is creating significant opportunities for mead producers to innovate with low-sugar and functional formulations. Increasing awareness around lifestyle-related conditions such as diabetes and obesity has encouraged consumers to reduce intake of high-sugar and processed beverages. In response, meaderies are exploring low-sugar variants that retain the natural appeal of honey while offering improved nutritional profiles.

The incorporation of probiotics into mead is gaining traction, aligning with rising consumer interest in gut health and functional beverages. These innovations position mead as a more health-conscious alternative within the alcoholic drinks category. Another opportunity lies in flavor innovation, particularly using exotic fruits and botanicals. Infusions of berries, tropical fruits, and citrus can enhance taste complexity and attract younger, experimental consumers.

Furthermore, incorporating spices such as ginger, cinnamon, and herbs enables producers to create distinctive, premium offerings. These diverse flavor combinations not only broaden consumer appeal but also support product differentiation in a competitive market. Together, health-focused formulations and flavor innovation are expected to significantly expand the scope and growth potential of the mead beverages market.

Category-wise Analysis

Flavor Insights

By flavor, the mead beverages market is segmented into traditional, fruit, spice & herb, and floral varieties. Traditional mead is expected to dominate, accounting for around 42% of the market in 2025, driven by its authenticity and strong appeal among consumers seeking classic, heritage-inspired beverages. Made primarily from fermented honey and water, traditional mead reflects historical roots and craftsmanship, making it highly attractive to purists and premium beverage consumers who value simplicity and originality.

Fruit-based meads are gaining significant traction, particularly among younger consumers, due to their diverse and approachable flavor profiles. Variants infused with berries, apples, and other fruits offer a balance of sweetness and acidity, enhancing drinkability. Meaderies are increasingly experimenting with innovative flavor combinations to attract new audiences and expand their market reach, contributing to the segment’s steady growth.

Packaging Type Insights

By packaging type, the mead beverages market is segmented into bottles, cans, and kegs. Bottles are expected to dominate the segment, accounting for approximately 62% of the market share, as glass packaging is widely preferred for preserving mead's flavor, aroma, and quality. Bottled formats also align with mead's premium positioning, appealing to consumers who associate glass packaging with authenticity, tradition, and superior product presentation.

However, alternative packaging formats, such as cans and kegs, are gradually gaining popularity, particularly for casual and on-the-go consumption. Cans offer convenience, portability, and suitability for modern retail channels, while kegs are widely used in bars and taprooms. Despite this, bottles continue to maintain a stronghold due to their ability to enhance shelf appeal and support premium branding in the mead beverages market.

Regional Insights

North America Mead Beverages Market Trends and Insights

North America is expected to lead the global mead beverages market, accounting for around 35% share and maintaining its dominance through 2033. This leadership is driven by a well-established craft beverage industry and strong consumer preference for artisanal, small-batch products. Consumers in the U.S. and Canada are increasingly open to experimenting with unique and heritage-inspired drinks, making mead an attractive option due to its diverse flavor profiles and historical appeal. The rapid growth of craft meaderies, mirroring trends seen in breweries and distilleries, further supports market expansion across the region.

Additionally, North America benefits from a robust retail and distribution infrastructure, including a well-developed e-commerce ecosystem for alcoholic beverages. Mead is becoming more accessible through restaurants, specialty liquor stores, and online platforms, enhancing consumer awareness and trial. This improved availability, combined with growing interest in premium and differentiated beverages, continues to drive demand and strengthens the region’s position as a key market for mead.

Europe Mead Beverages Market Trends and Insights

Europe is projected to witness steady growth in the mead beverages market, supported by strong consumer appreciation for premium, artisanal products. The region’s sophisticated consumer base values craftsmanship and authenticity, which has led to the rise of boutique meaderies focused on high-quality, small-batch production. These producers often emphasize traditional techniques and locally sourced ingredients, aligning with Europe’s deep-rooted culture of artisanal food and beverage consumption.

Mead’s diverse flavor offerings, including varieties infused with fruits, herbs, and spices, resonate well with European consumers who prioritize terroir and regional authenticity. Additionally, the growing popularity of mead festivals and cultural events across the region plays a crucial role in increasing awareness and educating consumers about the product. These events celebrate heritage and craftsmanship, fostering stronger consumer engagement and driving demand. As a result, Europe continues to emerge as a stable and culturally significant market for mead beverages.

Asia Pacific Mead Beverages Market Trends and Insights

Asia Pacific is expected to be the fastest-growing regional market for mead, driven by rising disposable incomes and greater exposure to international craft beverages. The region has historical roots in honey-based fermented drinks, particularly in China, which supports cultural acceptance of such products. Today, consumers in markets like Japan, India, and Southeast Asia are becoming more familiar with mead through travel, digital platforms, and specialty retailers. Emerging domestic producers are also introducing modern variations, contributing to growing market awareness.

The region benefits from diverse honey resources and established beverage production infrastructure that can be leveraged for mead production. Urban centers such as Tokyo, Shanghai, Bengaluru, and Singapore are developing vibrant craft beverage ecosystems, supporting niche product adoption. While regulatory challenges remain, especially regarding alcohol distribution and e-commerce, increasing collaborations between international brands and local distributors are expanding market reach. These dynamics, combined with innovation in flavors and formats, position the Asia Pacific as a key growth engine for the global mead beverages market.

Competitive Landscape

The global mead beverages market is a niche yet a rapidly growing segment. Branding and marketing are essential in the mead market's highly competitive environment. Manufacturers are investing in eye-catching packaging, imaginative label designs, and captivating brand narratives that accentuate the distinctive features and historical significance of their products. Many meaderies also use digital marketing and social media to interact with customers directly, sharing their mead stories and creating a community among drinkers.

Key Developments:

- In February 2026, UK-based mead producer Lyme Bay expanded its portfolio by launching two low-alcohol sparkling meads, aiming to tap into the growing demand for lighter, ready-to-drink (RTD) beverage options.

- In October 2025, an Abington High School graduate launched a new mead brand called MerMead, making it available for purchase through select local outlets.

- In March 2025, the Virginia Mead Guild launched the Virginia Mead Trail, offering enthusiasts a curated experience across regional meaderies, aiming to boost tourism and capitalize on the growing resurgence of mead beverages in the U.S.

- In March 2024, Cerana Meads launched its taproom in Nashik, Maharashtra, offering a wide range of meads on tap, including unique flavors such as pomegranate vanilla, Chenin blanc, and blue pea lavender.

Companies Covered in Mead Beverages Market

- Lyme Bay Cider Co Ltd

- Queens Reward Meadery, LLC

- Maxwell Wines

- High Seas

- Brimming Horn Meadery

- Moonshine Meadery

- Pasieka Jaros Sp. z o.o

- Redstone Meadery

- Magic Mead

- Nidhoggr Mead Co.

- Batch Mead

- Charm City Meadworks

- Moonlight Meadery

- Others

Frequently Asked Questions

The global market is expected to be valued at approximately US$ 774.2 million in 2026.

Increasing consumer interest in craft beverages and growing demand for low-sugar alcohol options are key market drivers.

North America currently leads the mead beverages market, accounting for about 35% of global value in 2025.

Key market opportunities include the integration of probiotics and the infusion of fruit and spice flavors in meads.

The key players in the global mead beverages market include Lyme Bay Winery, Queen’s Reward Meadery, and Maxwell Wines.