- Pharmaceuticals

- Neuropathic Pain Market

Neuropathic Pain Market Size, Share, and Growth Forecast 2026 - 2033

Neuropathic Pain Market by Drug Class (Tricyclic Anti-Depressants, Anticonvulsants, SNRIs, Topical Anesthetics, Opioids, Others), Indication (Diabetic Neuropathy, Chemotherapy-Induced Peripheral Neuropathy (CIPN), Post-Herpetic Neuralgia (PHN), Trigeminal Neuralgia, Spinal Cord Injury-Associated Neuropathy, Phantom Limb Pain, Multiple Sclerosis-Associated Neuropathy, Others), Route of Administration, Distribution Channel and Regional Analysis, 2026 - 2033

Neuropathic Pain Market Size and Trend Analysis

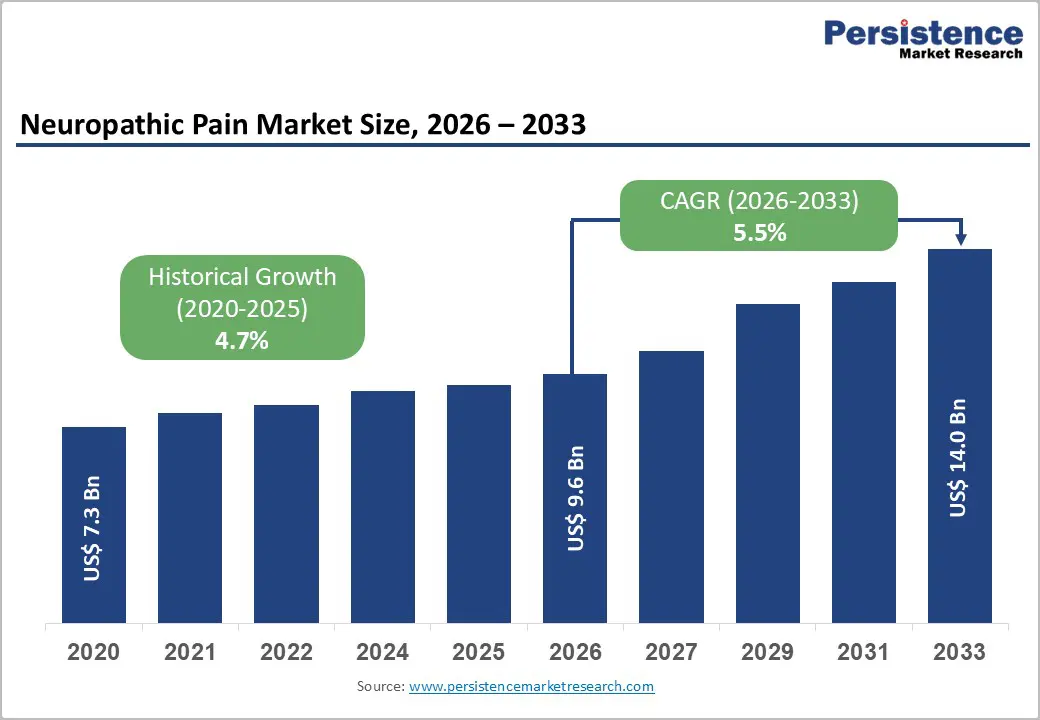

The global neuropathic pain market size is expected to be valued at US$ 9.6 billion in 2026 and projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033. This steady growth trajectory is primarily driven by the rise in global prevalence of conditions that directly cause neuropathic pain most notably diabetes mellitus, cancer, and herpes zoster combined with the progressive aging of the global population.

According to the International Diabetes Federation (IDF), approximately 537 million adults worldwide were living with diabetes in 2021, projected at 783 million by 2045. Also, diabetic peripheral neuropathy affects an estimated 50% of this population over the course of their illness.

Simultaneously, advances in oncology treatment have expanded the population of cancer survivors experiencing chemotherapy-induced peripheral neuropathy (CIPN), while pipeline innovation in non-opioid analgesics, novel anticonvulsant formulations, and targeted topical delivery systems is broadening treatment options and extending market revenue opportunities through the forecast horizon.

Key Industry Highlights:

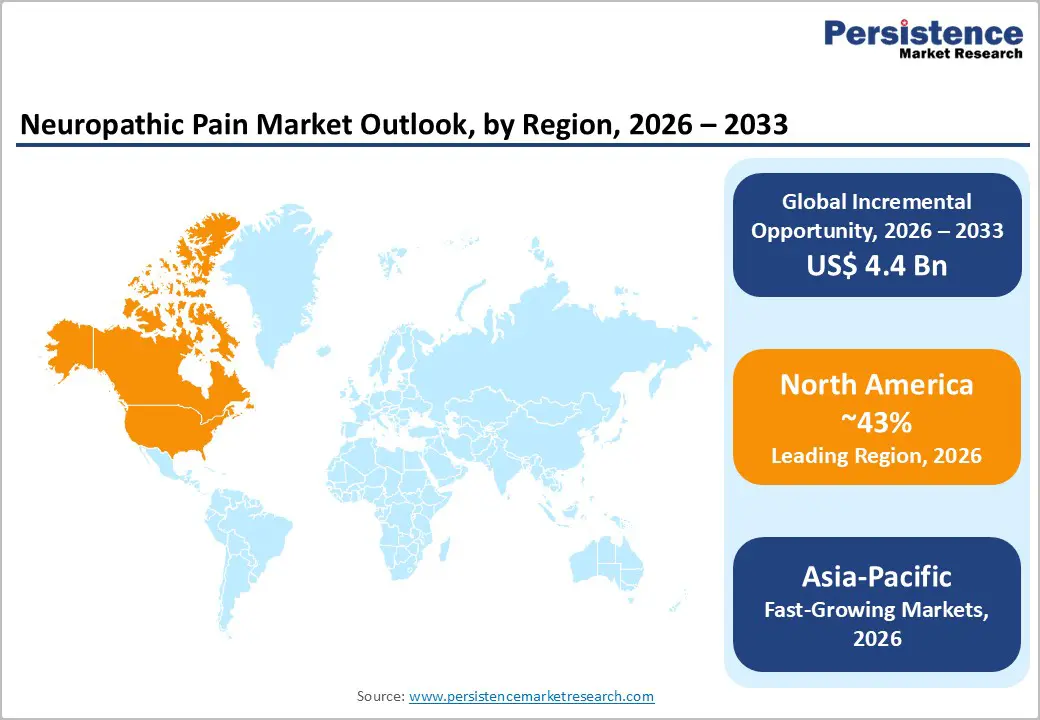

- Regional Leadership: North America leads the global Neuropathic Pain market with approximately 43% revenue share in 2025, driven by high diabetes and cancer survivor prevalence, FDA approval pipelines, and robust insurance reimbursement for anticonvulsant and SNRI therapies.

- Fast-growing Market: Asia Pacific is the fast-growing regional market, propelled by China's 140 million+ diabetic population, Japan's aging demographics, India's expanding generic pharmaceutical access, and rapidly improving healthcare infrastructure across ASEAN nations.

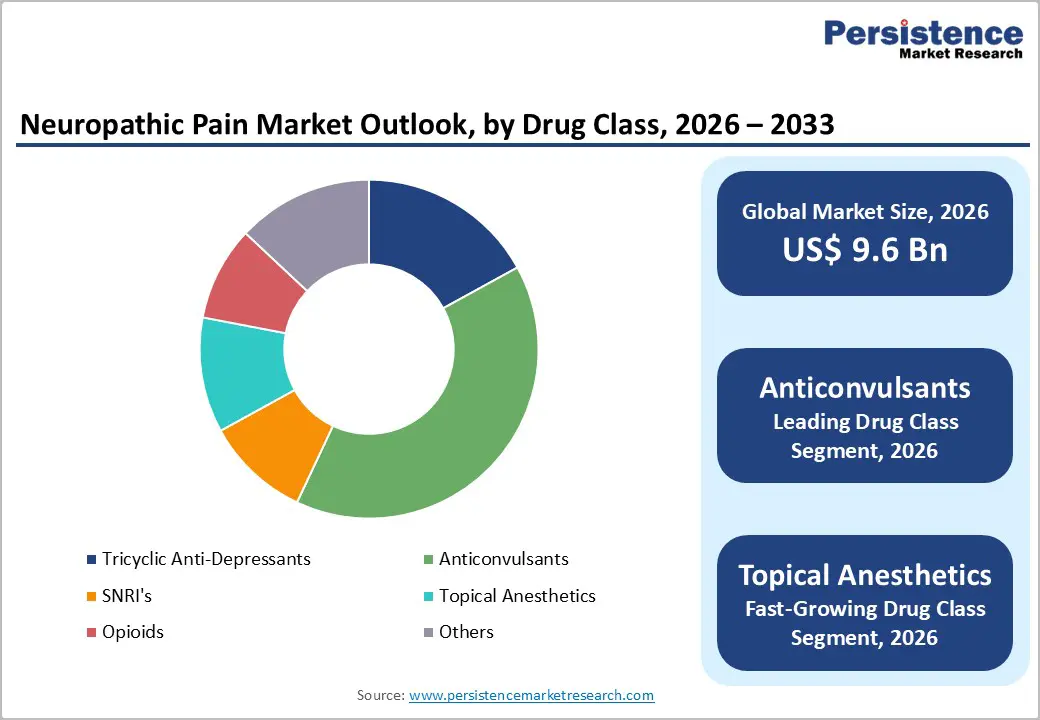

- Dominant Drug Class Category: Anticonvulsants lead the drug class category with approximately 40% market share in 2025, anchored by the broad clinical adoption of pregabalin and gabapentin as IASP- and EFNS-endorsed first-line therapies for multiple neuropathic pain indications.

- Fast-Growing Segment: Topical Anesthetics represent the fastest growing drug class during 2026 - 2033, fueled by increasing preference for targeted, systemic-side-effect-free delivery; EMA- and FDA-approved lidocaine and capsaicin patches; and growing guideline endorsement for localized neuropathic pain indications.

- Key Opportunity: The significant unmet need in CIPN management with no FDA-approved preventive therapy combined with pipeline innovation in selective NaV1.8 inhibitors such as Vertex Pharmaceuticals' suzetrigine, represents the most compelling near-term revenue and first-mover opportunity in the neuropathic pain space.

Market Dynamics

Is the Rising Global Burden of Diabetes and Diabetic Peripheral Neuropathy Drive Growth?

Diabetic peripheral neuropathy (DPN) is the single most prevalent indication driving demand in the neuropathic pain market, affecting an estimated 30-50% of all individuals with diabetes according to the American Diabetes Association (ADA). With the International Diabetes Federation (IDF) projecting global diabetes prevalence to reach 783 million by 2045, up from 537 million in 2021 the DPN patient population will expand dramatically in parallel.

DPN is frequently undertreated; a study published in Diabetes Care found that fewer than 40% of DPN patients receive pharmacological pain management. This substantial treatment gap, combined with the chronic and progressive nature of the condition, creates durable, high-volume demand for anticonvulsants, SNRIs, and topical agents across hospital and retail pharmacy channels, particularly in North America, Europe, and rapidly urbanizing Asia Pacific markets.

Is the Inadequate Efficacy of Existing Pharmacotherapies and High Discontinuation Rates Affecting Market Dynamics?

A fundamental challenge constraining the neuropathic pain market is the limited and often incomplete efficacy of current standard-of-care pharmacotherapies. Clinical guidelines from the International Association for the Study of Pain (IASP) and the European Federation of Neurological Societies (EFNS) acknowledge that first-line agents, including gabapentin, pregabalin, and duloxetine, achieve pain relief in only 30-50% of patients.

High rates of treatment discontinuation due to adverse effects, including sedation, dizziness, and weight gain, limit long-term adherence and reduce per-patient lifetime revenue for manufacturers, creating a persistent efficacy ceiling that constrains organic volume growth for established drug classes.

How Does Innovation in Topical Anesthetic Formulations Pose as the Fastest Growing Drug Class Segment and Fuel More Opportunities?

Topical anesthetics represent the fast-growing drug class in the neuropathic pain market, driven by increasing preference for targeted delivery systems that minimize systemic adverse effects. Products such as lidocaine 5% patches (Versatis, Grünenthal) and capsaicin 8% patches (Qutenza, Averitas Pharma) are gaining clinical acceptance backed by EMA and FDA approvals for post-herpetic neuralgia and diabetic neuropathy.

The EFNS and IASP guidelines increasingly recommend topical agents as first- or second-line options for localized neuropathic pain, reducing systemic drug burden. Pharmaceutical companies investing in novel topical formulations, including extended-release patches, nanoparticle-enhanced penetration systems, and combination products, are well-positioned to capture premium pricing and growing formulary inclusion, particularly in outpatient and homecare settings across both developed and emerging markets.

Category-wise Analysis

Drug Class Insights

The anticonvulsants segment dominates the neuropathic pain market by drug class, accounting for approximately 40% of total drug class revenue in 2025. This leadership is anchored by the widespread clinical adoption of pregabalin (Lyrica, Pfizer) and gabapentin as first-line therapies for diabetic peripheral neuropathy, post-herpetic neuralgia, and spinal cord injury-associated pain, as endorsed by IASP and EFNS clinical guidelines.

Pregabalin's FDA approval spans multiple neuropathic pain indications, and its broad prescriber familiarity across neurology and primary care establishes durable prescribing inertia. Generic entry following patent expiration has significantly expanded formulary accessibility, driving volume growth even as per-unit pricing declines. The combined branded and generic anticonvulsant market remains substantial, with Pfizer, Viatris, and Teva Pharmaceutical Industries among the key revenue contributors to this leading segment.

Indication Insights

The diabetic neuropathy indication leads the neuropathic pain market by disease area, representing approximately 36% of indication-based market revenue in 2025. This dominance directly reflects the global diabetes epidemic: with 537 million diabetic adults worldwide (IDF, 2021) and diabetic peripheral neuropathy affecting up to 50% of long-duration diabetic patients, the patient population for diabetic neuropathy treatment is the largest single addressable indication in the market. First-line therapies, including duloxetine (Cymbalta), pregabalin (Lyrica), and gabapentin are each explicitly FDA-approved or guideline-recommended for this indication.

The chronic, progressive nature of diabetic neuropathy requires long-term pharmacological management, ensuring high prescription persistency and recurring pharmacy dispensing volumes that reinforce this indication's revenue leadership through the forecast period.

Regional Insights

North America Neuropathic Pain Market Trends and Insights

North America is expected to account for approximately 43% of the global neuropathic pain market value in 2026, making it the leading regional contributor, with the United States serving as the primary growth engine. The region’s dominance is driven by a high burden of diabetes, cancer, and spinal cord injuries, all of which significantly contribute to neuropathic pain prevalence. Strong clinical awareness and early diagnosis rates further support sustained treatment uptake across outpatient and hospital settings.

The market benefits from well-established pharmaceutical penetration of therapies such as gabapentinoids, SNRIs, and topical analgesics, alongside increasing adoption of neuromodulation devices. The presence of leading companies and robust R&D pipelines ensures the continuous introduction of improved pain management solutions. Advanced healthcare infrastructure, widespread insurance coverage, and structured pain management guidelines further strengthen treatment access. Additionally, a strong shift toward non-opioid and multimodal pain management strategies is accelerating demand, driven by regulatory scrutiny on opioid prescriptions.

U.S. Neuropathic Pain Market Trends and Insights

The United States dominated the North American neuropathic pain market and was expected to reach nearly US$ 3.6 billion by 2026 due to high diabetes prevalence, strong prescription drug utilization, and advanced pain management infrastructure. According to the Centers for Disease Control and Prevention, around 40.1 million

For the American population, diabetic peripheral neuropathy affects nearly 30-50% of diabetic patients, which significantly increases the demand for anticonvulsants, antidepressants, and topical analgesics. The country also reports high chemotherapy utilization, increasing CIPN incidence. Strong reimbursement systems, rapid adoption of branded neuropathic pain drugs, and high healthcare spending further strengthened the U.S. market position.

Canada Neuropathic Pain Market Trends and Insights

Canada is likely to reach a CAGR of around 5.9% during the forecast period due to an increasing elderly population, rising diabetes burden, and expanding neurological care access. The country has witnessed an increasing prevalence of chronic pain disorders and diabetic complications, especially among aging adults above 65 years. Government-supported healthcare coverage and rising awareness regarding early neuropathy diagnosis have increased treatment adoption rates.

Canada is also seeing higher demand for non-opioid pain management therapies due to opioid safety concerns. Increasing oncology treatment volumes have additionally contributed to rising chemotherapy-induced peripheral neuropathy cases, supporting demand for neuropathic pain medications and neuromodulation therapies across hospitals and specialty clinics.

Europe Neuropathic Pain Market Trends and Insights

Europe is expected to account for approximately 27% of the global neuropathic pain market value in 2026, with key contributions from Germany, the UK, and France. The region’s growth is strongly supported by a rapidly aging population and a high incidence of diabetes, cancer survivorship, and post-surgical neuropathic complications. Well-established national healthcare systems and favorable reimbursement frameworks enable broad access to prescription neuropathic pain therapies, including gabapentinoids, SNRIs, and topical agents.

The market is also influenced by strict opioid regulations across most European countries, driving a sustained shift toward non-opioid and multimodal pain management strategies. Increasing adoption of neuromodulation devices and multidisciplinary pain clinics is further strengthening treatment penetration. Strong clinical guideline adherence and early intervention practices enhance diagnosis and long-term disease management. Continuous innovation by regional and global pharmaceutical companies ensures steady therapeutic advancement.

Germany Neuropathic Pain Market Trends and Insights

Germany led the European neuropathic pain market and was expected to reach nearly US$ 1.1 billion by 2026, owing to strong healthcare infrastructure, high diabetes prevalence, and increasing elderly population. Europe reports painful diabetic peripheral neuropathy prevalence ranging from 6% to 34% among diabetic patients. Germany has one of Europe’s largest aging populations, increasing susceptibility to neuropathic disorders and post-herpetic neuralgia. The country also demonstrates high healthcare expenditure and strong access to prescription neuropathic pain drugs.

Increased adoption of guideline-based pain therapies, along with expanding neurological treatment centers, has strengthened market growth. Germany additionally benefits from high diagnosis rates and reimbursement support for chronic pain management therapies.

UK Neuropathic Pain Market Trends and Insights

The United Kingdom was expected to grow at a CAGR of approximately 5.7% due to increasing diabetic neuropathy incidence and expanding chronic pain management programs. A large U.K. community study involving over 15,000 diabetic patients reported a prevalence of painful diabetic neuropathy of nearly 21%. Rising awareness campaigns by public healthcare organizations and improved access to neurological diagnostics are increasing treatment uptake. The country is also experiencing rising chemotherapy utilization and aging demographics, which are contributing to a higher neuropathic pain burden.

Increased focus on reducing opioid dependency has accelerated demand for alternative therapies, including SNRIs, anticonvulsants, and topical analgesics. Expanding NHS support for chronic pain management further supports market growth.

Asia Pacific Neuropathic Pain Market Trends and Insights

Asia Pacific is expected to account for approximately 18% of the global neuropathic pain market value in 2026, with China, India, and Japan acting as the primary growth engines. The region is witnessing rapid expansion due to a large and rising diabetic population, increasing cancer burden, and improving awareness of chronic pain disorders. Japan leads in advanced pain management adoption, while India and China are major contributors to volume growth driven by expanding access to affordable generics.

Healthcare infrastructure development, growing neurology specialization, and rising healthcare expenditure are significantly improving diagnosis and treatment rates. However, underdiagnosis and limited access to pain specialists in rural areas continue to restrain optimal market penetration. Increasing adoption of cost-effective pharmacological therapies, along with the gradual penetration of neuromodulation technologies in urban hospitals, is supporting steady growth.

China Neuropathic Pain Market Trends and Insights

China dominated the Asia-Pacific neuropathic pain market and is likely to reach US$ 1.4 billion by 2026 due to its massive diabetic population and rapidly expanding healthcare infrastructure. Studies indicate diabetic peripheral neuropathy prevalence in Chinese type 2 diabetes cohorts reached nearly 67.6%, among the highest globally. Rising urbanization, sedentary lifestyles, and increasing obesity rates are driving diabetes incidence significantly. China is also witnessing rapid expansion in oncology treatment volumes, contributing to increased chemotherapy-induced peripheral neuropathy cases.

Government healthcare reforms, expanding insurance access, and increasing domestic pharmaceutical production are supporting wider availability of neuropathic pain therapies across urban and semi-urban healthcare facilities.

India Neuropathic Pain Market Trends and Insights

India is likely to achieve fast-growth with a CAGR of 7.2% owing to rapidly rising diabetes prevalence, improving healthcare access, and increasing awareness regarding neuropathic disorders. Studies reported diabetic peripheral neuropathy prevalence in India ranging between 19.1% and 52.9% among diabetic patients. India’s large diabetic population, increasing geriatric demographics, and growing cancer burden are significantly increasing the demand for neuropathic pain treatment.

Expansion of specialty neurology centers, greater availability of generic medications, and government healthcare initiatives are improving treatment accessibility. Rising healthcare expenditure and increasing diagnosis of diabetic neuropathy in urban populations are further supporting rapid market expansion across the country.

Competitive Landscape

The global neuropathic pain market exhibits a moderately consolidated structure, with a handful of large multinational pharmaceutical companies, including Pfizer Inc., Novartis AG, Teva Pharmaceutical Industries, and Abbott, holding significant branded and generic revenue positions across major indications.

Market leaders differentiate through branded product lifecycle extension strategies (e.g., extended-release reformulations, new indication filings), extensive pain specialty sales forces, and strategic co-promotion partnerships. Generic manufacturers, including Viatris, Amneal Pharmaceuticals, and Accord Healthcare, compete aggressively on price in post-patent anticonvulsant segments. An emerging trend is investment in pipeline NaV1.7 sodium channel blockers and novel topical delivery platforms to address the significant unmet need and establish non-opioid differentiation in the market.

Key Developments:

- March 2026: Vertex Pharmaceuticals Incorporated announced new clinical data for JOURNAVX demonstrating effective pain management following aesthetic and reconstructive surgical procedures. The company presented the findings at a medical conference, highlighting that the non-opioid pain therapy showed meaningful reductions in post-operative pain while supporting recovery outcomes.

- June 2025: Azurity Pharmaceuticals, Inc. announced that the U.S. Food and Drug Administration approved XIFYRM (meloxicam injection) for the management of moderate-to-severe pain in adults. The approval expanded Azurity’s pain management portfolio and provided healthcare professionals with a non-opioid injectable treatment option for acute pain care.

Companies Covered in Neuropathic Pain Market

- Almatica

- Vertex Pharmaceuticals Incorporated

- Azurity Pharmaceuticals, Inc.

- Pfizer Inc.

- Viatris Inc.

- Supernus Pharmaceuticals, Inc.

- Novartis AG

- Accord Healthcare

- Focus Health Group

- Amneal Pharmaceuticals LLC

- Abbott

- Teva Pharmaceutical Industries Ltd.

- Others

Frequently Asked Questions

The global neuropathic pain market is estimated to be valued at US$ 9.6 billion in 2026.

Rising diabetes prevalence, aging populations, cancer therapies, chronic pain incidence, and increasing neuropathy diagnosis rates.

North America is the leading regional market, accounting for approximately 43% of global revenue in 2025.

Development of non-opioid therapies, topical treatments, precision medicines, and expanding healthcare access in emerging markets.

The market is led by Pfizer Inc. (pregabalin/Lyrica franchise), Eli Lilly and Company (duloxetine/Cymbalta), Novartis AG, Abbott (spinal cord stimulation), Teva Pharmaceutical Industries, and Viatris in generics.