- Processed Food

- Low-fat Cheese Market

Low-fat Cheese Market Size, Share, and Growth Forecast 2026 - 2033

Low-fat Cheese Market by Product Type (Feta, Ricotta, Mozzarella Sticks, Hard Cheese), Application (Biscuits, Snacks, Soups, Sauces, Others), Distribution Channel (Foodservice, Hypermarkets/Supermarkets, Online, Convenience Stores, Others), and Regional Analysis, 2026 - 2033

Low-fat Cheese Market Share and Trends Analysis

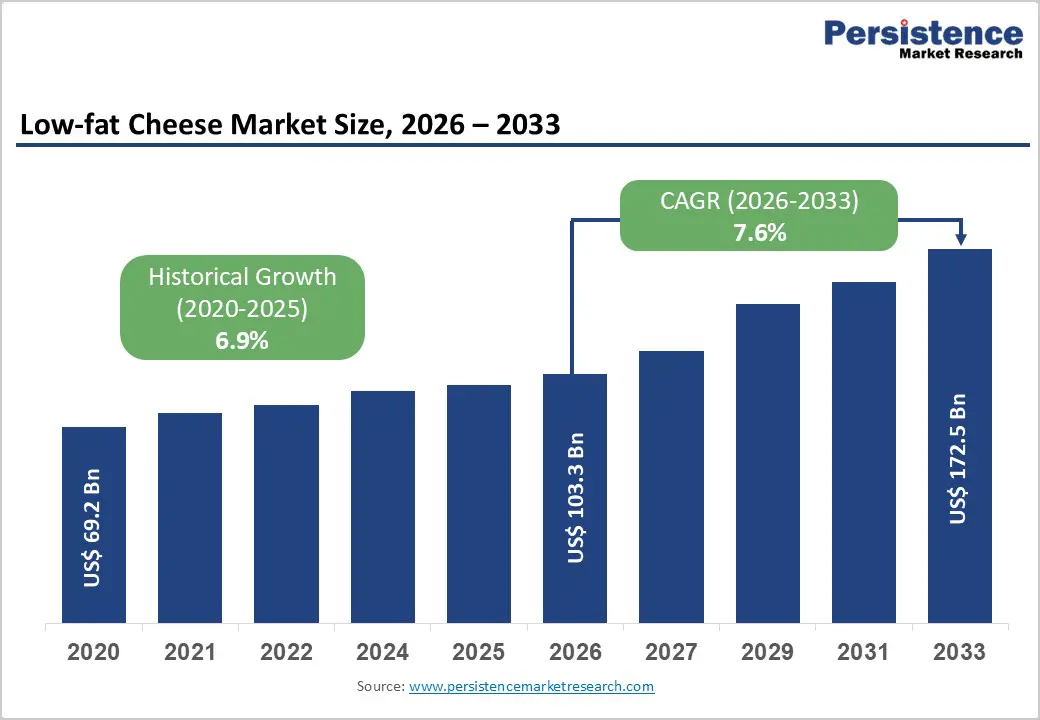

The global Low-fat Cheese market size is expected to be valued at US$ 103.3 billion in 2026 and projected to reach US$ 172.5 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. The increasing health consciousness, rising cases of obesity, and a shift toward healthier dietary habits has encouraged the need for low-fat cheese products.

Consumers are actively seeking reduced-fat dairy alternatives without compromising taste and texture, boosting demand across retail and foodservice channels. Low-fat cheese is widely used in salads, sandwiches, pizzas, and processed foods, supporting its strong adoption in everyday diets. Product innovation focusing on improved flavor, protein enrichment, and clean-label ingredients is further enhancing market appeal. Growth is also supported by expanding fitness trends and nutritional awareness across urban populations in both developed and emerging regions.

Key Industry Highlights:

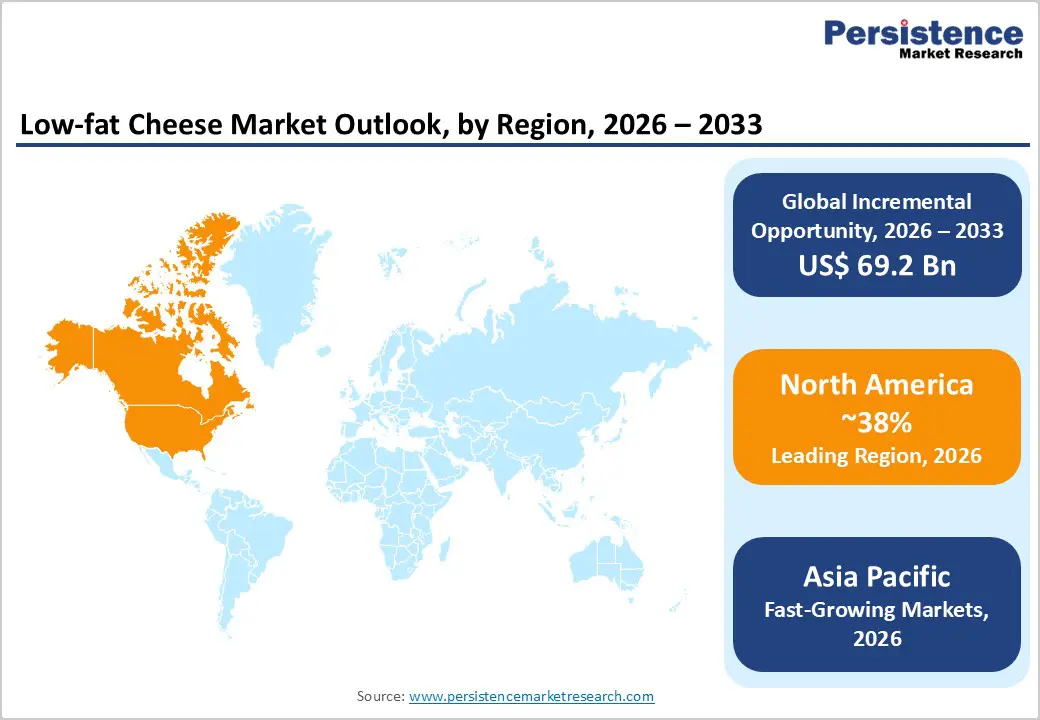

- Leading Region: North America holds approximately 38% of the global low-fat cheese market share in 2025, driven by USDA-mandated low-fat dairy requirements in school nutrition programs serving 30 million+ students daily and strong AHA dietary guidance endorsing reduced-fat dairy consumption.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, propelled by the rapid Westernization of food culture among urban consumers in China, India, and Southeast Asia, expanding QSR penetration, and growing health-conscious dairy adoption across the region's young middle-class population.

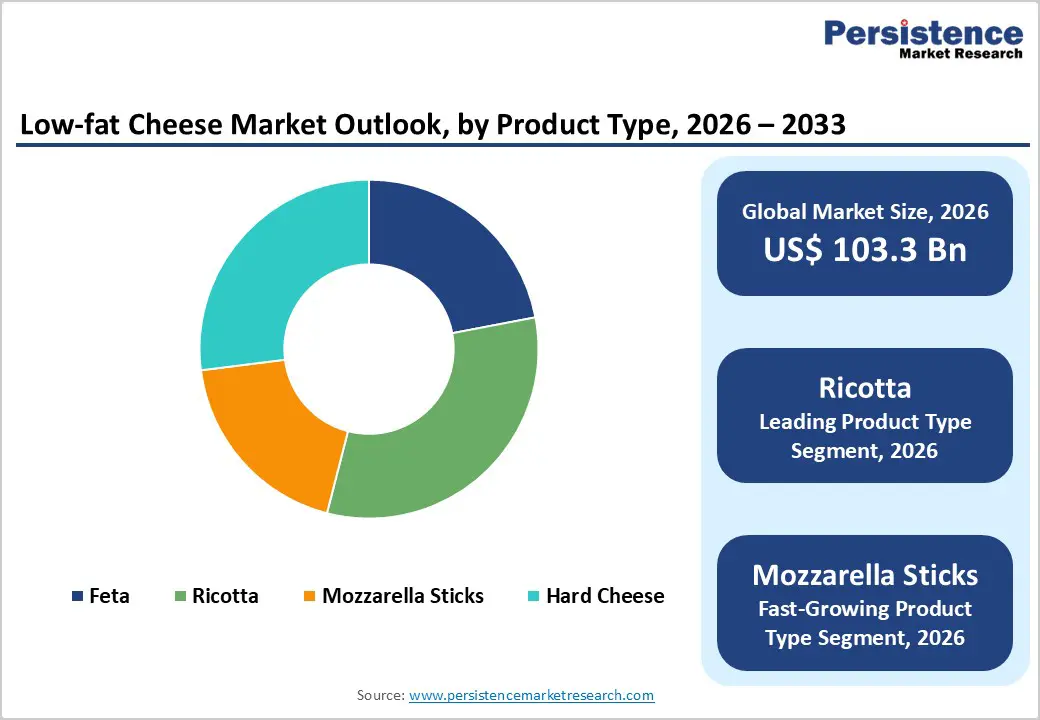

- Dominant Segment: Ricotta leads the product type category with approximately 32% of the global low-fat cheese market share in 2025, driven by its naturally lower fat profile, broad culinary versatility across savory and sweet applications, and strong institutional procurement for school nutrition programs globally.

- Fastest Growing Segment: Low-fat Mozzarella Sticks are the fastest-growing product type, driven by explosive growth in better-for-you snacking, QSR menu reformulation toward healthier options, and school nutrition program adoption, creating large-volume institutional and retail demand for reduced-fat breaded cheese snack formats.

- Key Market Opportunity: Manufacturers investing in fat-reduction technology innovation, particularly advanced enzyme and protein technologies that close the taste-texture gap between low-fat and full-fat cheese, stand to capture premium market positioning and accelerate category adoption among the large consumer segment that prioritizes flavor parity over health alone.

Market Dynamics

Drivers - Rising Vegan and Flexitarian Population Seeking Healthier Options

The rising vegan and flexitarian population is significantly influencing the growth of the low-fat cheese market as consumers increasingly shift toward healthier and more sustainable dietary choices. Vegans avoid animal-based products entirely, while flexitarians reduce their intake of dairy and meat, creating strong demand for healthier dairy alternatives. Low-fat cheese fits well into this trend as it offers reduced calorie and fat content while still providing familiar taste and nutritional benefits. Growing awareness about animal welfare, environmental sustainability, and lifestyle-related health issues is further accelerating this shift. Food manufacturers are responding by developing innovative low-fat and plant-based cheese variants with improved flavor, texture, and nutritional profiles. Retail availability and foodservice adoption are also expanding, making these products more accessible. As a result, the growing vegan and flexitarian movement is becoming a key driver reshaping consumer preferences and supporting long-term market expansion.

Restraints - Higher production cost due to processing and formulation

Higher production costs due to processing and formulation are a significant restraint in the low-fat cheese market. Producing low-fat cheese requires advanced manufacturing techniques to replicate the taste, texture, and mouthfeel of full-fat cheese while removing or reducing fat content. This often involves specialized ingredients, stabilizers, and protein enhancers, which increase raw material expenses. Additionally, precise processing methods such as controlled fermentation, emulsification, and moisture management require sophisticated equipment and higher energy consumption.

Maintaining product consistency and quality further adds to operational complexity and cost. Manufacturers also invest heavily in research and development to improve flavor and consumer acceptance, which increases overall expenditure. Smaller producers face greater challenges in absorbing these costs, limiting their ability to compete with large-scale players. As a result, elevated production and formulation expenses directly impact pricing strategies, profit margins, and market penetration, especially in price-sensitive and emerging markets.

Premium Pricing and Manufacturing Complexity of Low-fat Cheese Production

Producing low-fat cheese that achieves acceptable consumer palatability requires advanced manufacturing processes, including modified starter cultures, fat replacers, texture-modifying enzymes, and protein concentration technologies that add meaningful cost complexity compared to conventional full-fat cheese production. According to the International Dairy Foods Association (IDFA), reduced-fat dairy product formulation typically increases per-unit manufacturing cost by 8–15%, translating into retail price premiums that create adoption friction among price-sensitive consumer segments, particularly in emerging markets where premium dairy categories remain aspirational rather than mainstream purchases.

Opportunities - Mozzarella Sticks: Fastest-Growing Low-fat Cheese Format in Snack and QSR Applications

Low-fat Mozzarella Sticks represent the fastest-growing product type segment within the low-fat cheese market, driven by the explosive growth of the global savory snack segment and the rapid adoption of healthier QSR menu innovation. The Snack Food Association (SFA) reports that the U.S. savory snack category generates over US$ 40 billion in annual retail sales, with better-for-you snack options capturing a growing share.

Low-fat mozzarella sticks are well-positioned at the intersection of indulgence and health providing the tactile snacking experience of a traditionally high-fat item in a clinically validated reduced-fat format. Major QSR chains and school lunch programs are actively incorporating low-fat mozzarella sticks as menu items, creating bulk institutional demand. Manufacturers investing in breaded coating innovation and superior melt profiles for low-fat mozzarella formulations will capture the premium positioning and volume scale this growing category demands.

Digital Retail and Subscription Dairy Box Models Enabling Premium Low-fat Cheese Discovery

The rapid growth of online grocery and specialty food subscription services represents a structurally advantaged distribution opportunity for premium low-fat cheese brands seeking to reach health-conscious consumers who would be difficult to access through traditional retail shelf space constraints. Amazon Fresh, Whole Foods Market's digital platform, and specialty cheese subscription services are enabling the discovery of premium low-fat feta, ricotta, and artisan reduced-fat cheese varieties among consumers who actively seek diet-aligned dairy products. According to FMI – The Food Industry Association, over 52% of U.S. consumers purchased groceries online in 2023, a permanently elevated penetration rate that creates scalable e-commerce infrastructure for brands like Arla Foods and FrieslandCampina to build direct brand relationships with health-motivated low-fat dairy consumers globally.

Category-wise Analysis

Product Type Insights

Ricotta leads the low-fat cheese market by product type with approximately 32% of global market share in 2025, sustained by its naturally lower fat content profile compared to aged hard cheeses, exceptional versatility across cooking applications from baked goods and pasta dishes to desserts and dips and strong institutional demand from school nutrition programs and healthcare food service operators that prioritize low-fat dairy options.

Ricotta's gentle flavor and smooth, spreadable texture make it uniquely compatible with both savory and sweet applications, giving it the broadest application coverage of any low-fat cheese variety. The USDA Agricultural Marketing Service documents ricotta as a key dairy product in NSLP procurement, reinforcing institutional demand. Mozzarella Sticks are the fastest-growing product type, propelled by QSR adoption and snack innovation.

Application Insights

The snacks application segment leads low-fat cheese demand by application with approximately 34% of global market share in 2025, driven by the structural growth of the global better-for-you snack category and the active reformulation of traditional high-fat cheese snack products, such as cheese crackers, cheese puffs, portion-controlled string cheese, and cheese-filled baked snacks, toward low-fat formulations by major manufacturers.

The Snack Food Association (SFA) confirms snacking now constitutes a primary eating occasion for 94% of adults globally. Sauces is the fastest-growing application, driven by the rapid expansion of low-fat cheese-based pasta sauces, dips, and ready-meal sauce components as food manufacturers reduce saturated fat content to meet evolving EU nutrition labeling and FDA nutrition facts standards for front-of-pack health claim eligibility.

Distribution Channel Insights

Hypermarkets and Supermarkets retain the dominant distribution channel position with approximately 46% of global low-fat cheese retail sales in 2025, reflecting their role as the primary destination for weekly dairy category shopping globally and their ability to merchandise a comprehensive low-fat cheese assortment from private-label reduced-fat blocks to premium branded ricotta and specialty reduced-fat feta with strong promotional support.

Major chains, including Walmart, Kroger, Tesco, and Carrefour, maintain dedicated reduced-fat dairy sections. Online channels are the fastest-growing distribution segment, with specialty cheese e-commerce, subscription dairy boxes, and Amazon Fresh enabling premium low-fat cheese brands to build direct consumer relationships.

Regional Insights

North America Low-fat Cheese Market Trends and Insights

North America leads the global low-fat cheese market with approximately 38% of global share in 2025, driven by strong institutional demand from USDA-mandated low-fat dairy requirements in school nutrition programs, high consumer health awareness, and dominant retail presence of major brands, including Kraft Heinz Company and General Mills Inc. The region's QSR sector is a key growth driver as chains reformulate with low-fat mozzarella and ricotta-based menu innovations.

U.S. Low-fat Cheese Market Size

The United States accounts for approximately 83% of North American low-fat cheese revenue, backed by the National School Lunch Program (NSLP) serving over 30 million students daily with mandated low-fat dairy. Per-capita low-fat cheese consumption is among the highest globally. Dairy Farmers of America and Lactalis Group are key supply-side anchors sustaining robust U.S. market growth through 2033.

Europe Low-fat Cheese Market Trends and Insights

Europe is the second-largest low-fat cheese market, holding approximately 28% of global share, with demand shaped by strong regulatory focus on nutrition labeling transparency under EU Regulation (EU) No 1169/2011 on food information to consumers, which mandates per-100g saturated fat disclosures. Arla Foods and FrieslandCampina lead the European market with extensive low-fat cheese portfolios across retail and foodservice channels, with organic and clean-label low-fat variants gaining significant premium traction.

Germany Low-fat Cheese Market Size

Germany is Europe's largest low-fat cheese market, contributing approximately 18–20% of regional revenue, driven by high per-capita dairy consumption and strong consumer preference for Quark a naturally low-fat fresh cheese alongside reduced-fat feta and ricotta. The Deutsche Gesellschaft für Ernährung (DGE) dietary guidelines support low-fat dairy consumption, reinforcing sustained household demand for low-fat cheese variants through 2033.

U.K. Low-fat Cheese Market Size

The United Kingdom accounts for approximately 16–18% of the European low-fat cheese market revenue, with strong demand for reduced-fat Cheddar, the U.K.'s most consumed cheese variety, and growing low-fat cottage cheese and ricotta segments. NHS dietary guidelines actively promote low-fat dairy, while major retailers Tesco and Sainsbury's have expanded private-label reduced-fat cheese assortments significantly, sustaining robust growth.

France Low-fat Cheese Market Size

France contributes approximately 15% of the European low-fat cheese market, with the Programme National Nutrition Santé (PNNS) promoting reduced-fat dairy across the population. Despite France's deep full-fat cheese culture, urban health-conscious consumers are increasingly purchasing low-fat fromage blanc, reduced-fat brie, and light ricotta variants. Lactalis Group and Danone S.A. lead the French reduced-fat dairy segment through their extensive retail distribution networks.

Asia Pacific Low-fat Cheese Market Trends and Insights

Asia Pacific is the fastest-growing regional low-fat cheese market, fueled by the rapid Westernization of food culture among young urban consumers, growing health awareness driving low-fat dairy adoption, and expanding modern retail infrastructure. China's urban middle class is discovering low-fat cheese through international QSR chains and premium imported dairy brands, with growing demand for low-fat mozzarella in the booming Chinese pizza and fast-casual dining segment supported by platforms like Meituan and Ele.me.

India Low-fat Cheese Market Size

India represents approximately 12% of the Asia Pacific low-fat cheese market revenue, with demand anchored by Amul Limited and GCMMF India's dairy cooperative giants, which have introduced low-fat cheese variants across urban supermarkets and online platforms. Rising health consciousness among Indian urban professionals and the growing QSR sector, including Domino's India and McDonald's India, using low-fat mozzarella, support sustained market growth.

Japan Low-fat Cheese Market Size

Japan accounts for approximately 16–18% of Asia Pacific low-fat cheese revenue, with a health-conscious aging population actively seeking reduced-fat dairy protein sources. The Ministry of Health, Labour and Welfare dietary guidelines encourage low-fat dairy consumption among adults over 50. Snow Brand Milk Products and Meiji Holdings lead the Japanese reduced-fat cheese segment, with portioned low-fat mozzarella and ricotta gaining traction in convenience store formats.

Competitive Landscape

The low-fat cheese market is highly competitive, supported by rising health awareness, growing demand for protein-rich dairy products, and increasing preference for reduced-calorie diets. Market participants focus on product innovation through improved taste, texture, and clean-label formulations to attract health-conscious consumers. Expansion of lactose-free, organic, and fortified variants is strengthening portfolio diversification. Companies are also investing in advanced processing technologies to maintain flavor while reducing fat content. Strong retail distribution through supermarkets, specialty stores, and e-commerce platforms enhances market reach, while premiumization and functional nutrition trends continue to shape long-term competitive positioning globally.

Key Developments

- In March 2025, Lactalis UK & Ireland introduced a new protein range under the Lindahls brand to cater to the rising consumer demand for dairy protein. The range includes low-fat, high-protein cheeses such as Quark, Greek Cheese, Gouda Slices, and Cottage Cheese.

- In September 2024, Cathedral City launched a new high-protein, half-fat cheddar range in the U.K. It aims to cater to the surging demand for nutritious and low-fat dairy products. The new product range includes mini, grated, sliced, and block formats.

Global Low-fat Cheese Market - Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 69.2 billion |

|

Current Market Value (2026) |

US$ 103.3 billion |

|

Projected Market Value (2033) |

US$ 172.5 billion |

|

CAGR (2026–2033) |

7.6% |

|

Leading Region |

North America, ~38% market share (2025) |

|

Dominant Product Type |

Ricotta, ~32% market share (2025) |

|

Top-Ranking Application |

Snacks, ~34% market share (2025) |

|

Incremental Opportunity |

US$ 69.2 billion (Absolute Dollar Opportunity, 2026–2033) |

Companies Covered in Low-fat Cheese Market

- Kraft Heinz Company

- Nestlé S.A.

- Unilever N.V.

- Dairy Farmers of America

- Amul Limited (GCMMF)

- FrieslandCampina

- Arla Foods Inc.

- Danone S.A.

- Lactalis Group

- GCMMF

- Lactosan A/S

- Kanegrade Limited

- Aarkay Food Products Ltd.

- General Mills Inc.

- Saputo Inc.

- Fonterra Co-operative Group

Frequently Asked Questions

The global Low-fat Cheese market is valued at US$ 103.3 billion in 2026.

The primary demand drivers include government dietary guidelines from the USDA, WHO, and American Heart Association (AHA) recommending low-fat dairy for cardiovascular health, and mandatory low-fat dairy procurement under the National School Lunch Program (NSLP) serving 30 million+ students daily in the U.S., creating large, policy-backed institutional demand channels for low-fat ricotta, mozzarella, and feta products.

North America leads the global Low-fat Cheese market with approximately 38% of global share in 2025, driven by strong institutional demand from USDA school nutrition mandates.

The most significant near-term opportunities are in Low-fat Mozzarella Sticks, the fastest-growing product segment driven by snack sector growth and QSR menu innovation, and in online and e-commerce distribution channels.

The leading companies in the global Low-fat Cheese market include Lactalis Group, Arla Foods, Inc., FrieslandCampina, Kraft Heinz Company, and Danone S.A.