- Beverages

- U.S. Instant Coffee Market

U.S. Instant Coffee Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

U.S. Instant Coffee Market by Flavoring (Flavored, Unflavored), by Coffee Type (Liquid, Soluble/Powder), by Packaging (Sachet, Pouches, Jars), by Distribution Channel (Supermarkets/Hypermarkets, Online Retail Stores), and Analysis for 2025 - 2032

U.S. Instant Coffee Market Size and Trends

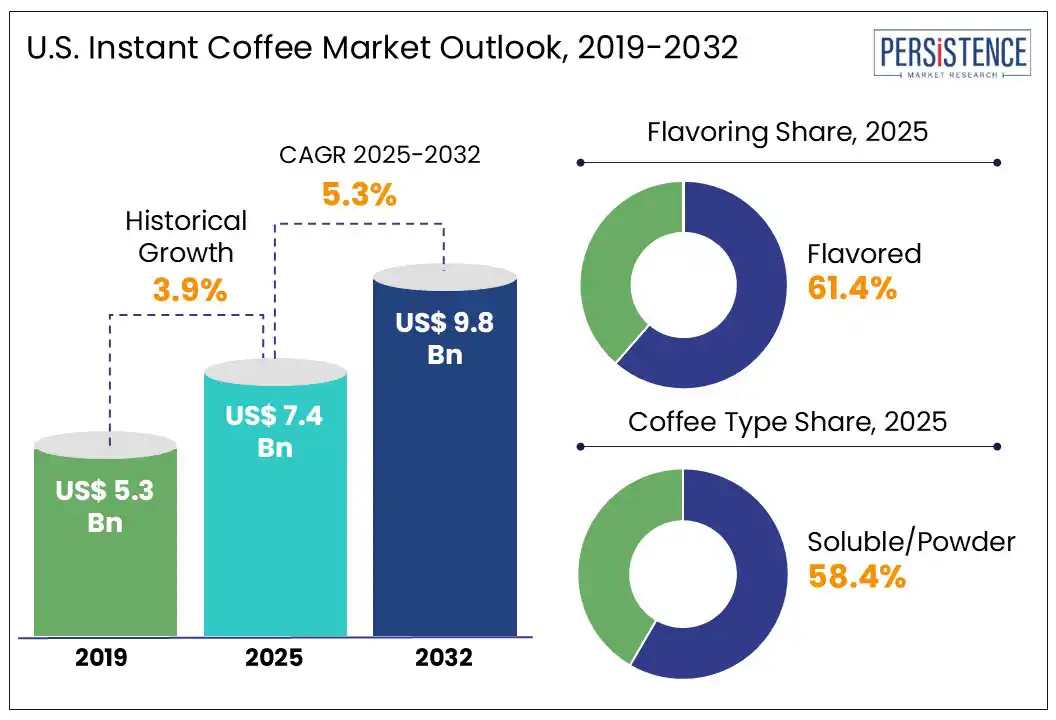

The U.S. instant coffee market size is likely to be valued at US$ 7.4 Bn in 2025 and is estimated to reach US$ 9.8 Bn in 2032, growing at a CAGR of 5.3% during the forecast period 2025-2032.

Instant coffee, long valued for its convenience and ease of preparation, is now experiencing a remarkable resurgence in the U.S. market. This revival aligns with evolving consumer preferences that demand both speed and quality in their coffee experience. The category is being transformed through premium sourcing and specialty-grade innovations, elevating instant coffee’s status among discerning consumers. Robust growth is being observed across both flavored and unflavored segments, with particular strength in convenient formats such as sachets and liquid concentrates. These developments signal a dynamic shift, establishing it as a rapidly expanding and influential segment within the U.S. coffee market.

Key Industry Highlights:

- Increased work-from-home culture is boosting at-home caffeinated beverage consumption and instant coffee uptake.

- Instant coffee brands are predicted to target multicultural markets with 3-in-1 and sweetened regional blends.

- Key companies are estimated to collaborate with wellness influencers and fitness brands to position instant coffee as a healthy product.

- Flavored instant coffee variants such as vanilla and mocha are attracting non-traditional coffee drinkers.

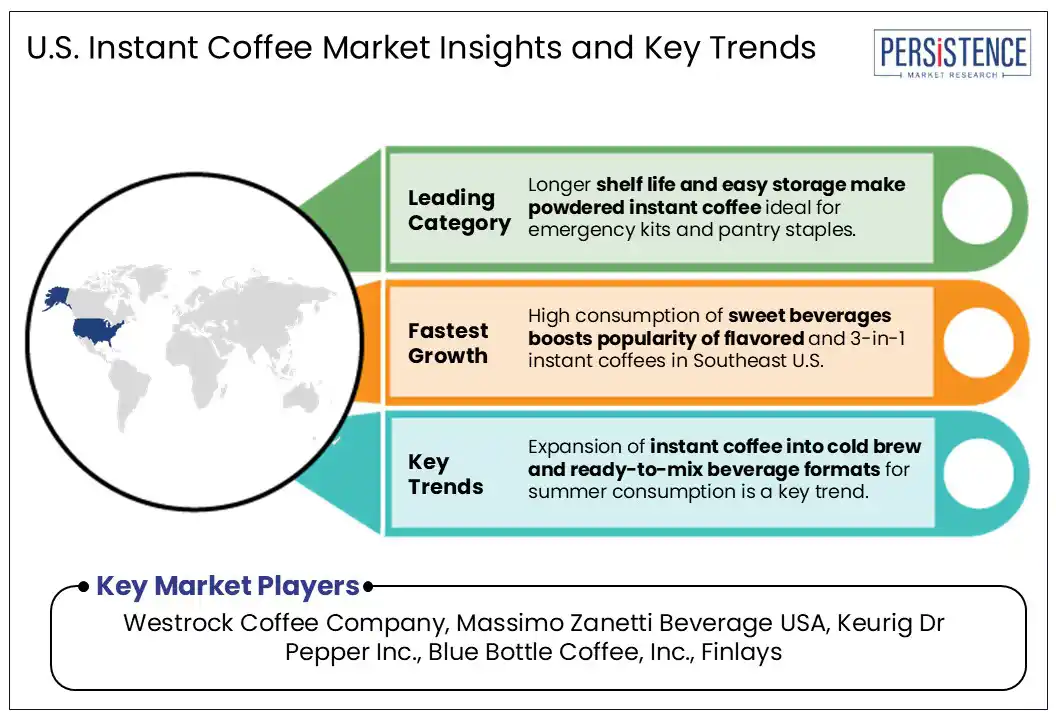

- Powdered coffee will likely hold around 58.4% of the share in 2025 due to its ability to easily blend into recipes, shakes, and baking.

- The Southeast U.S. is witnessing steady growth owing to the increased adoption of premium sachets and liquid concentrates in urban hubs such as Atlanta and Miami.

|

Market Attribute |

Key Insights |

|

U.S. Instant Coffee Market Size (2025E) |

US$ 7.4 Bn |

|

Market Value Forecast (2032F) |

US$ 9.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.9% |

Market Dynamics

Driver - Hybrid Lifestyles and Equipment-free Brewing to Fuel Demand

Accessibility and ease of preparation are pushing the U.S. instant coffee market growth, mainly among demographics that prioritize convenience. With the shift toward hybrid work and on-the-go lifestyles, consumers are increasingly valuing the speed and minimal equipment required for preparing instant coffee. A 2024 survey by the National Coffee Association revealed that 43% of Gen Z and millennial consumers prefer formats that require no brewing equipment. It has spurred demand for instant sachets, which only require hot water and are ideal for busy mornings, office desks, travel kits, and dorm rooms.

Expansion of portable and single-serve instant coffee formats is particularly impactful in urban areas where kitchen space is limited and time constraints are high. Brands such as Starbucks VIA have seen significant adoption among city dwellers who lack access to full brewing setups. Instant coffee is also proving to be an inclusive format across socioeconomic tiers. In underserved or rural areas where cafés or coffee equipment are less accessible, it serves as a primary source of caffeine.

Restraint - Hefty Coffee Tariffs Force Brands to Raise Instant Coffee Prices

U.S. tariffs on instant coffee, primarily hefty duties on robusta from Vietnam and agrarian pressures on Brazil and Colombia, are significantly inflating costs for importers and manufacturers. A baseline 10% tariff on Brazilian arabica and a 46% levy on Vietnamese robusta sharply raise the landed price of green beans. Industry leaders such as Royal Coffee note that these added import taxes, especially for coffee concentrate and commercial-grade robusta, are disrupting supply, squeezing profit margins and driving input costs higher.

With U.S. instant coffee imports already under price pressure due to global climate events, the added tariffs mean retailers and brands are hiking shelf prices. The National Coffee Association warns that even a universal 10% tariff on Brazil-imported coffee, amounting to over US$2.1 Bn in annual U.S. sourcing, will likely compound record-high consumer prices. As instant coffee becomes less affordable, consumers are anticipated to trade down to private-label or forego instant entirely.

Opportunity - Rise of Specialty Instant Coffee in Retail and Travel Segments

Increasing demand for specialty coffee in the U.S. has pushed the boundaries of what consumers expect from instant coffee. It has created new opportunities for premiumization, innovation, and niche market expansion. As third-wave coffee culture continues to spread, consumers are becoming more discerning about flavor, origin, and processing methods. It has created a viable space for specialty instant coffee, mainly freeze-dried single-origin varieties that promise barista-level flavor in seconds. Several brands are capitalizing on this trend by offering specialty-grade instant coffee made from 100% arabica beans sourced from specific regions such as Ethiopia or Colombia.

Retailers are responding to this shift by allocating shelf space to gourmet instant offerings. Whole Foods and Trader Joe’s, for instance, have started stocking premium instant options that highlight ethical sourcing and complex flavor profiles. The sachet format is witnessing rapid growth among instant coffee packaging types. Specialty instant brands are using this to target not just at-home consumers but also hikers, travelers, and digital nomads who want high-quality coffee without single-serve coffee makers.

Category-wise Analysis

Flavoring Insights

Based on flavoring, the market is divided into flavored and unflavored. Among these, the flavored segment is predicted to lead with nearly 61.4% of the U.S. instant coffee market share in 2025 due to its ability to meet the evolving taste preferences among younger consumers who often seek indulgent profiles over traditional bitter notes. A 2024 report from Kerry Group highlighted that about 54% of Gen Z and millennial coffee drinkers in North America prefer flavored coffee options with vanilla, mocha, hazelnut, and caramel among the most favored. Instant coffee brands have responded by introducing a wide range of flavors, such as turmeric coffee to cater to this segment, often in portable sachets or pods that emphasize both variety and convenience.

Unflavored instant coffee is experiencing decent growth owing to the rising preference for customization and control over additives. Several health-conscious consumers are opting for base coffee options that allow them to regulate sugar, dairy, and flavoring levels according to personal dietary requirements. This trend is evident in the increasing popularity of clean-label products, with unflavored instant coffee often perceived as a ‘blank canvas’ free from hidden sweeteners or artificial ingredients.

Coffee Type Insights

By coffee type, the U.S. instant coffee market is bifurcated into liquid and soluble/powder. Out of these, the soluble/powder segment is expected to account for approximately 58.4% of the share in 2025, with its adaptability across both conventional and emerging use cases. Rapid expansion of at-home consumption post-pandemic has normalized the use of powdered coffee for everyday routines. These formats offer a long shelf life, require no equipment, and allow flexible portion control. These properties make them highly attractive for households balancing budget and convenience.

The U.S. liquid coffee market is seeing steady growth due to increased consumer preference for ultra-convenience and precision in beverage preparation. Unlike powder-based formats that require stirring and can leave residue, liquid coffee offers a mess-free and consistent cup that resonates with busy urban consumers. This demand has been particularly notable in foodservice and commercial beverage sectors. Brands such as Douwe Egberts and Nestlé Professional, for example, supply liquid coffee concentrates to hotel chains, corporate offices, and healthcare facilities for consistent brewing in high-volume settings.

Zone Insights

Southwest U.S. Instant Coffee Market Trends

In the Southwest, especially Arizona and neighboring states, the market is increasingly influenced by regional dynamics and shifting consumer trends. In Arizona, both instant and drip coffee commands a premium price relative to the national average, with regular cups running around US$3.51, which is 14% above the U.S. average. This pricing backdrop affects ready-to-drink coffee positioning. It becomes a cost-saving alternative even when cafés are marginally more affordable, pushing domestic consumption mainly among budget-conscious urban households.

Across the Southwest, convenience-driven consumers such as commuters, remote workers, military personnel, and travelers are spurring demand for portable sachets and freeze-dried options. National data shows sachets are the fastest-growing packaging segment. This trend is mirrored regionally via Phoenix, Tucson, El Paso, and Albuquerque, where on-the-go lifestyles are gaining momentum. Brands are pushing high-end freeze-dried blends marketed for superior aroma and taste. In addition, the expansion of Caffenio, a Mexico-based chain opening its first U.S. location in Mesa, shows growing interest in culturally authentic coffee formats.

Southeast U.S. Instant Coffee Market Trends

The stronghold of legacy players such as Community Coffee, which dominates markets in Louisiana and parts of Mississippi, is a key market driver in the Southeast. These deeply rooted domestic companies maintain loyal followings with customized offerings, including chicory-infused instant blends and organic coffee that reflect regional taste profiles. Unlike the Pacific Northwest or Northeast, where black coffee and specialty roasts are more common, the Southeast leans toward sweeter and milkier instant coffee products.

It is partly cultural, shaped by the zone’s long-standing affinity for sweet tea and flavored beverages. Instant coffee formats that mimic this sweetness, including 3-in-1 sachets containing coffee, sugar, and creamer, have seen a surging acceptance across Birmingham and Jackson. These pre-mixed formats also appeal to lower-income households seeking convenience and consistency at a low cost. Additionally, recent U.S. tariffs on Brazil, Colombia, and Vietnam, which are the source of robusta beans used in instant coffee, have added up to 46% in import duties. In the Southeast, where shipping routes funnel through Gulf ports, small regional roasters are affected, squeezing margins in a cost-sensitive market.

Midwest U.S. Instant Coffee Market Trends

The Midwest is experiencing a subtle but significant transformation. While the zone has traditionally leaned toward brewed drip coffee, increasing inflation and bean shortages have prompted more consumers to explore instant alternatives. It has seen a measurable uptick in demand for instant coffee sachets, primarily in Illinois and Minnesota. In these states, urban centers such as Chicago and Minneapolis house a large population of commuters and officegoers looking for quick caffeine solutions. These consumers are increasingly turning to single-serve, freeze-dried sachets due to their portability and improved taste profiles.

Local roasters are also starting to integrate instant coffee into their offerings. Dunn Brothers Coffee, a chain rooted in Minnesota, for example, has begun experimenting with selling house-blended instant formats. These products are positioned as high-quality alternatives to mainstream instant coffee, using the same beans as their regular roasts. It reflects a shift in consumer trust toward local brands and signals a surging acceptance of instant coffee beyond its former budget-only image.

Competitive Landscape

The U.S. instant coffee market is witnessing a dynamic shift augmented by both legacy brands and a surge of specialty entrants. Nestlé, through its Nescafé and Starbucks VIA lines, maintains a dominant position, leveraging vast distribution networks and consistent innovation. However, its dominance is increasingly challenged by premium-focused start-ups such as Waka Coffee and Sudden Coffee that cater to millennials and Gen Z with ethical sourcing and flavor integrity. Private-label instant coffees from grocery chains, including Costco, have gained impetus as consumers seek affordable alternatives without sacrificing taste.

Key Industry Developments

- In August 2024, Diamond Brew officially launched in the U.S. as the country's first brewless coffee. It is considered a new generation of instant coffee that offers a barista experience without any equipment.

- In April 2024, NESCAFÉ launched NESCAFÉ Gold Espresso and NESCAFÉ Ice Roast in the U.S. NESCAFÉ's Gold Espresso does not require any machine and can be instantly prepared. Ice Roast is the brand’s first-ever cold-liquid-dissolvable coffee made to be mixed with cold water or milk.

Companies Covered in U.S. Instant Coffee Market

- Westrock Coffee Company

- Massimo Zanetti Beverage USA

- Keurig Dr Pepper Inc.

- Blue Bottle Coffee, Inc.

- Finlays

- Bkon

- Nestle S.A.

- The Kraft Heinz Company

- The J.M. Smucker Company

- Kerry Group plc

- Boston’s Best Coffee Roasters

- Others

Frequently Asked Questions

The U.S. instant coffee market is projected to reach US$ 7.4 Bn in 2025.

DIY coffee hacks using instant coffee and the growth of online grocery platforms are the key market drivers.

The market is poised to witness a CAGR of 5.3% from 2025 to 2032.

The emergence of store-brand instant coffees and product diversification into travel kits are the key market opportunities.

Westrock Coffee Company, Massimo Zanetti Beverage USA, and Keurig Dr Pepper Inc. are a few key market players.