- Automotive Components & Materials

- Automotive Active Grille Shutter Market

Automotive Active Grille Shutter Market Size, Share, and Growth Forecast for 2025 - 2032

Automotive Active Grille Shutter Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles and Heavy Commercial Vehicles), By Shutter (Visible Automotive Active Grille Shutters and Non-Visible Automotive Active Grille Shutters), Vane, Sales Channel, and Regional Analysis for 2025 - 2032

Automotive Active Grille Shutter Market Size and Trends

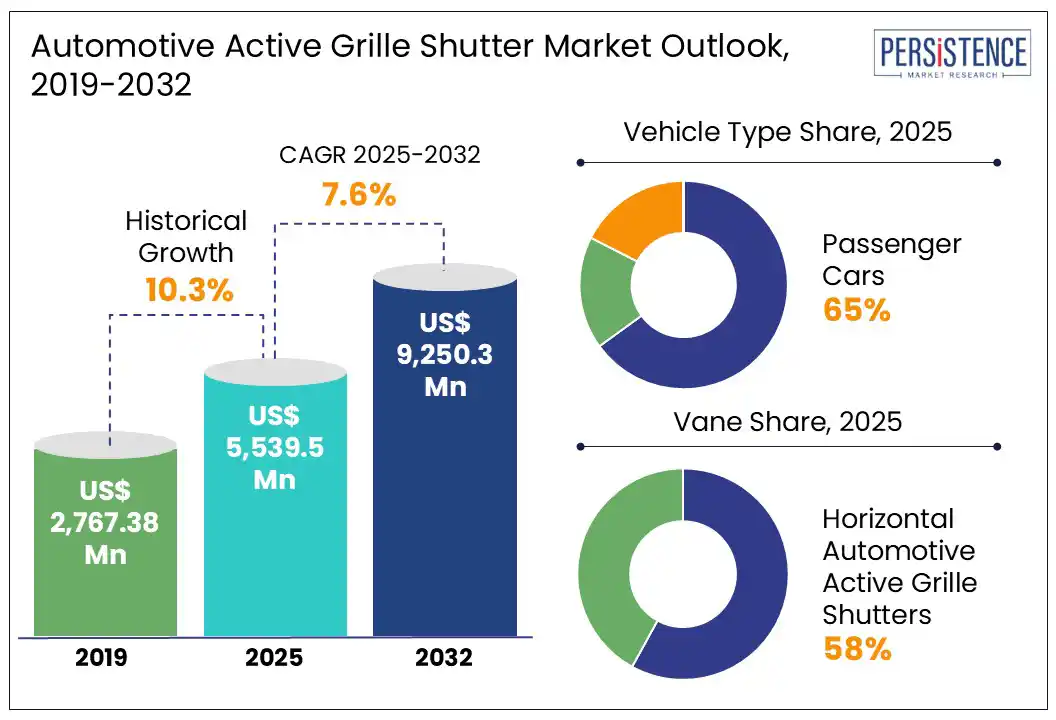

The global Automotive Active Grille Shutter Market size is likely to be valued at US$ 5,539.5 Mn in 2025 and is expected to reach US$ 9,250.3 Mn by 2032, growing at a CAGR of 7.6% from 2025 to 2032.

Active grille shutters are expected to be in high demand amid emerging trends, including thermoacoustic engine encapsulation and the use of sophisticated thermal management to increase engine efficiency. The automotive active grille shutter market is experiencing strong demand across different vehicle segments. Sports, luxury, and light commercial vehicles are the most common types of automobiles with active grille shutters. Compact active grille shutter manufacturers are mainly focused on manufacturing materials that are lightweight.

Key Industry Highlights:

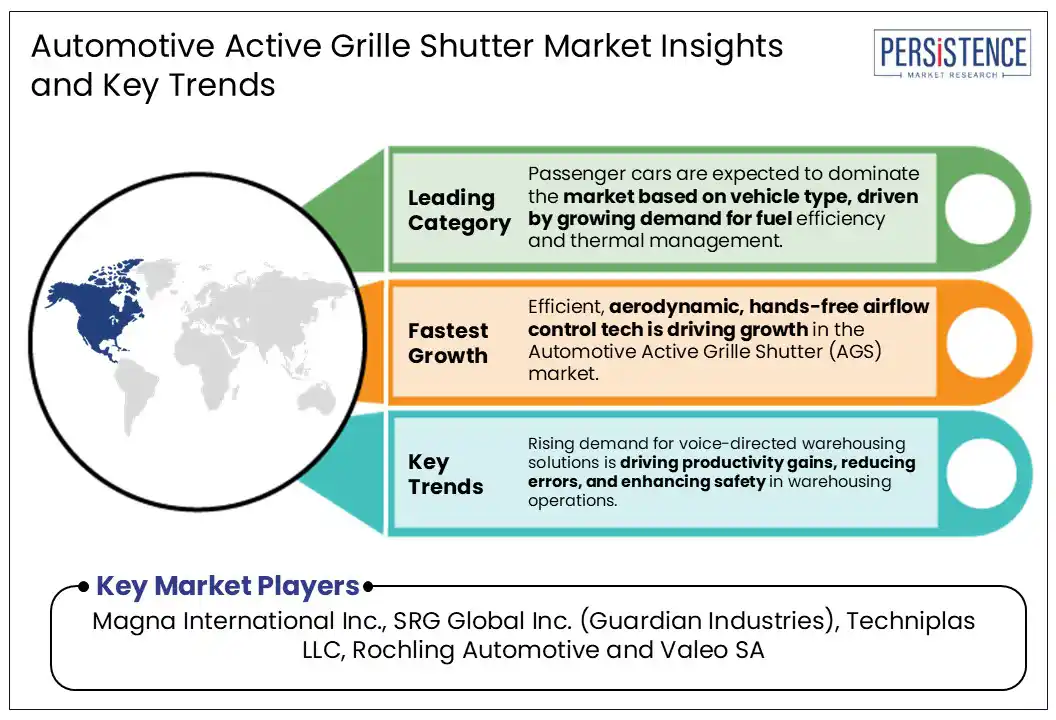

- The development of more efficient, aerodynamic, hands-free airflow-control technologies is fueling growth in the Automotive Active Grille Shutter (AGS) market.

- North America is projected to dominate the market, accounting for 30.1% of global revenue by 2025, driven by early adoption of energy-efficient automotive technologies and strong OEM presence.

- OEM demand is increasing as manufacturers prioritize fuel efficiency and CO emission reduction, especially in SUVs and light-duty vehicles.

- Technological advancements such as AI-driven control systems, lightweight materials, and electromechanical shutters are enhancing performance and durability.

- Based on Vehicle Type, the passenger cars segment is expected to lead the market with a significant share, supported by increasing demand for fuel economy and thermal management.

- The luxury vehicle segment is increasingly integrating AGS to improve performance and reduce drag, contributing to market expansion.

|

Global Market Attribute |

Key Insights |

|

Automotive Active Grille Shutter Market Size (2025E) |

US$ 5,539.5 Mn |

|

Market Value Forecast (2032F) |

US$ 9,250.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.3% |

Market Dynamics

Driver - Efficiency and design advancements are accelerating demand for the automotive active grille shutter market

Driving factors such as end-user concerns about efficiency and design advancements are expected to aid in the growth of the global Automotive Active Grille Shutter market. Luxury, midsize, and sporty vehicles all come equipped with automotive active grille shutter systems. Additionally, the demand for the automobile active grille shutter system is anticipated to rise significantly as more models and new vehicle types are lined up for launches. Additionally, the growth of the middle class, increasing household incomes, and growing urbanization will all contribute to a spike in vehicle sales.

The demand for fuel-efficient automobiles is expected to drive growth in the market for automotive active grille shutter Market. The aerodynamic coefficient can be raised by using AGS systems, which can decrease CO2 emissions by up to 3 grams per kilometer and reduce air drag by an average of 9%, or 25 aerodynamic points. Government-imposed restrictions on emissions push automakers to use technologies that reduce air resistance and cut emissions. In the upcoming years, technology adoption may be boosted by such emission standards and regulations by domestic regulatory bodies.

Restraint - High cost of technology restrains the automotive active grille shutter market growth

A major restraint facing the automotive active grille shutter (AGS) market is the high cost of the technology. AGS systems involve advanced mechatronics and materials, making them expensive to produce and integrate into vehicles. This high cost limits adoption, especially in developing economies where consumers prefer more affordable vehicles without such features. Instead, low-segment vehicles often rely on cheaper aerodynamic solutions, such as diffusers, underbody panels, and spoilers to reduce drag.

Additionally, the premium pricing of AGS-equipped vehicles restricts market penetration primarily to luxury and mid-range segments, slowing broader market growth. The cost barrier also affects manufacturers’ willingness to adopt AGS widely, despite its benefits in improving fuel efficiency and reducing emissions. Thus, affordability remains a significant challenge restraining the global expansion of the automotive active grille shutter market.

Opportunity - Growing demand for fuel efficiency and emissions reduction in ICE vehicles

Despite the rise of EVs, internal combustion engine (ICE) vehicles still account for a significant share of the global vehicle fleet. OEMs are under increasing regulatory pressure to reduce CO emissions and improve fuel efficiency. Active Grille Shutters help reduce aerodynamic drag by up to 9%, translating to fuel savings of 1–2 mpg, a critical advantage in meeting stringent emission norms like Euro 7 and U.S. CAFE standards.

Major automakers such as General Motors, Toyota, and Volkswagen have incorporated AGS into the Chevrolet Malibu, Toyota Camry, and VW Golf. These systems adjust grille openings dynamically, balancing engine cooling with drag reduction, thereby improving mileage and helping meet tightening global emission norms. In 2023, Magna International and Valeo upgraded their AGS offerings with lightweight materials and smart actuators to improve system responsiveness and durability.

Category-wise Analysis

Vehicle Type Insights

The passenger car segment holds the largest share globally in this market and will continue to dominate during the forecast period. Due to rising individual disposable income, the rising production and sales of passenger cars in developing countries will push the segment growth. The passenger car segment accounted for a market share of more than 70.60% in 2020. AGS demand in the passenger car segment is likely to rise as AGS penetration increases in passenger car models.

On the other hand, the commercial vehicle segment will witness steady growth in the forecast period. It is attributed to several governments' worldwide initiatives at reducing Co2 emissions and commercial vehicle consumers opting for fuel-efficient vehicles.

Vane Insights

The horizontal vane type dominates the automotive active grille shutter (AGS) market due to its ease of installation and superior aerodynamic benefits. Positioned horizontally across the vehicle's grille, these vanes efficiently regulate airflow to optimize engine cooling and reduce drag, enhancing fuel efficiency and lowering emissions. Their straightforward design allows for simpler integration into existing vehicle architectures compared to vertical vane systems, reducing manufacturing complexity and costs. This ease of installation makes horizontal vane AGS highly favored by automakers, contributing to its predicted market dominance through 2032 and beyond.

Additionally, horizontal vane systems provide effective energy savings and improved thermal management, aligning with the increasing regulatory demands for fuel economy and environmental compliance.

The vertical vane type segment witnessed high growth and low penetration during 2024. The vertical vane segment accounted for 33.42% share of market in 2024. Due to improved performance/tunning capability and increased preference for high-end automobiles due to their high aesthetic value, the segment will grow during the forecast timeframe.

Regional Insights

Asia Pacific Automotive Active Grille Shutter Market Trends

The Asia Pacific automotive active grille shutter market is poised for strong growth, driven by the region’s rapid vehicle electrification, expanding automotive production, and tightening emission regulations. Countries such as China, Japan, South Korea, and India are investing heavily in fuel-efficient and eco-friendly technologies. In particular, China leads the electric vehicle (EV) boom, with AGS systems playing a crucial role in optimizing thermal management and aerodynamic efficiency in EVs and hybrids. The growing demand for passenger cars and SUVs, especially in India and Southeast Asia, also supports the integration of AGS in ICE vehicles to improve fuel economy and reduce emissions.

Additionally, regional automakers and Tier-1 suppliers are accelerating R&D into lightweight and cost-effective AGS solutions to meet evolving regulatory and consumer demands. As governments continue to enforce stricter fuel economy standards and promote electric mobility, the Asia Pacific AGS market is expected to witness substantial adoption through 2032.

North America Automotive Active Grille Shutter Market Trends

The rising stringent government regulations for CO2 emissions, the fast adoption rate of new technology, high expenditure on product innovation, and increased consumer spending are expected to propel the market in North America. The presence of major radiator shutter assembly manufacturers and their effort to design aesthetic vehicle models contribute to the region's growth. Furthermore, increasing the production of light commercial vehicles in this region is expected to propel the growth of active grille shutter systems.

In North America, the U.S. is a significant end-user market. Factor such as increased sales of premium cars with active grille shutters, including several different RAM 1500 models, Ford cars, and high-end luxury cars from brands such as Cadillac and General Motors, among many others.

Europe Automotive Active Grille Shutter Market

Europe holds a dominant position in the global automotive active grille shutter (AGS) market, accounting for over 25% of the market share. The region’s growth is primarily driven by stringent emission regulations imposed by the European Union and a strong focus on environmentally friendly transportation solutions. Automakers in Europe are increasingly integrating AGS technology into new vehicles to enhance fuel efficiency by reducing aerodynamic drag and improving thermal management. This is crucial for meeting Europe’s ambitious carbon reduction targets.

The Original Equipment Manufacturer (OEM) sector plays a vital role in this expansion, as AGS becomes a standard feature in many passenger and commercial vehicles. Key markets such as Germany, France, and the UK lead in adoption, supported by advances in smart shutter mechanisms and actuation technologies.

Competitive Landscape

The automotive active grille shutter market is moderately competitive on a global scale, with numerous manufacturers competing for market dominance. Over the past few years, the active grill shutter market has seen a variety of growth strategies implemented by market competitors, including acquisitions, mergers, and partnerships. A pull technique is being used by some players by promoting their products at auto shows and exhibitions. The market also observes strong collaborations between automakers and original equipment manufacturers, with a strong emphasis on innovation.

Key Vane Developments:

- In April 2023, Valeo announced the intention to set up a new plant in Fukuoka, Japan, which will concentrate on producing advanced thermal management systems such as active grille shutters.

- In March 2021, Magna International Inc., a leader in automotive component suppliers, introduced two advanced electrified propulsion systems on an ice and snow-filled test track.

Companies Covered in Automotive Active Grille Shutter Market

- Magna International Inc.

- Shape Corporation

- SRG Global Inc. (Guardian Industries)

- Techniplas LLC

- HBPI GmbH

- Rochling Automotive

- Valeo SA

- Mirror Controls International

- Sonceboz SA

- Batz Group

- Aisin Corporation

- Yamaguichi Starlite Co., Ltd.

- Keboda Chongquing Automotive Electronics Co., Ltd

- Johnson Electric

Frequently Asked Questions

The automotive active grille shutter market is set to reach US$ 5,539.5 Mn in 2025.

Demand for Fuel Efficiency and Emission Reduction and Growth in Electric and Hybrid Vehicles are the major growth drivers.

The Vane is estimated to rise at a CAGR of 7.6% through 2032.

Increasing Demand for Fuel Efficiency and Emissions Reduction and Expansion Driven by Electrification and Advanced Vehicle Technologies are the key market opportunities.

Magna International Inc., SRG Global Inc. (Guardian Industries), Techniplas LLC, Rochling Automotive and Valeo SA are a few leading players.