- Power Generation, Transmission, & Distribution

- U.S. Thermal Management Technologies Market

U.S. Thermal Management Technologies Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Thermal Management Technologies Market by Device Type (Conduction Cooling Devices, Air Cooling Devices, Liquid Cooling Devices, Hybrid Cooling Devices, Thermoelectric Cooling Devices, Substrate & Interface Materials, Misc..), By Industry (Data Centers & Servers, Consumer Electronics, Automotive & EVs, Aerospace & Defense, Healthcare, Industrial / Enterprise), By Material Type (Metal-Based Materials, Non-Metal Materials, Polymer-Based, Phase Change Materials (PCM), Composites, Miscellaneous / Others), and Regional Analysis for 2026 - 2033

U.S. Thermal Management Technologies Market Size and Trends Analysis

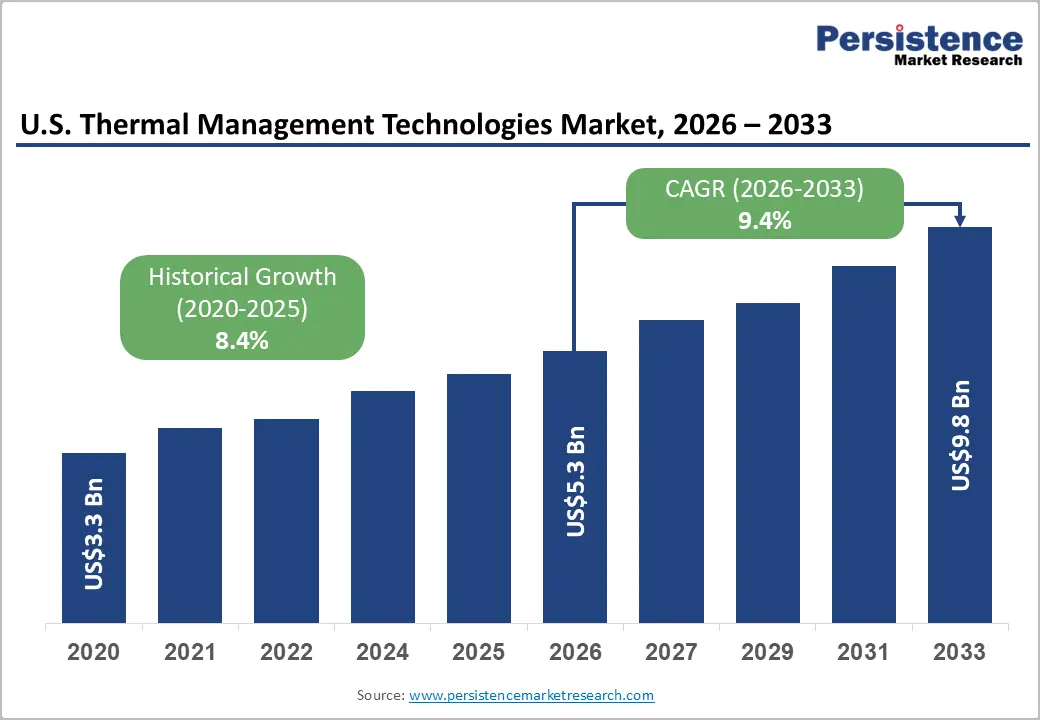

The U.S. thermal management technologies market size is likely to be valued at US$5.8 billion in 2026 and is projected to reach US$9.8 billion by 2033, growing at a CAGR of 9.4% between 2026 and 2033.

The market's robust historical trajectory reflects structural demand driven by the proliferation of AI-accelerated data centers, accelerating electric vehicle adoption, and the escalating thermal loads imposed by advanced semiconductor architectures.

The convergence of hyperscale computing expansion, federal electrification mandates, and aerospace modernization programs has established thermal management as a mission-critical engineering discipline rather than a peripheral input cost. As the U.S. data center ecosystem reached approximately 43.4 GW of operational capacity with vacancy rates near historic lows of 4.2%, and with EV adoption accounting for more than 1 in 10 new cars sold in 2024 according to the International Energy Agency (IEA), heat dissipation solutions are increasingly foundational to infrastructure performance, product reliability, and regulatory compliance across all major end-use verticals.

Key Industry Highlights

- Data Centers Lead Demand: Data Centers & Servers dominate with 30% market share in 2026, driven by AI-driven rack densities exceeding 40-100 kW and hyperscale construction pipelines across the United States.

- Advanced Liquid Cooling Dominance: Advanced & Liquid Cooling Devices hold 28% of the market, reflecting large-scale adoption of cold plates, immersion systems, and microchannel heat exchangers in AI infrastructure.

- Fastest-Growing Segment: Automotive & EV Thermal Management is the fastest-growing segment, with battery cooling systems accounting for 42.35% of EV thermal revenue and enabling up to 20% driving range optimization.

- Aerospace & Defense as Stability Anchor: Mission-critical platforms such as Honeywell’s upgraded 80 kW F-35 PTMS and one million flight-hour milestone reinforce aerospace as a high-value, long-cycle demand engine.

- Strategic Consolidation Momentum: Eaton’s US$ 9.5 billion acquisition of Boyd Thermal (November 2025) signals accelerating consolidation and integration of liquid cooling with intelligent power management.

- Regulatory & Sustainability Drivers: EPA low-GWP refrigerant mandates and federal backing through the Liquid Cooling for AI Act of 2025 are reshaping product development and accelerating liquid cooling deployment.

| Key Insights | Details |

|---|---|

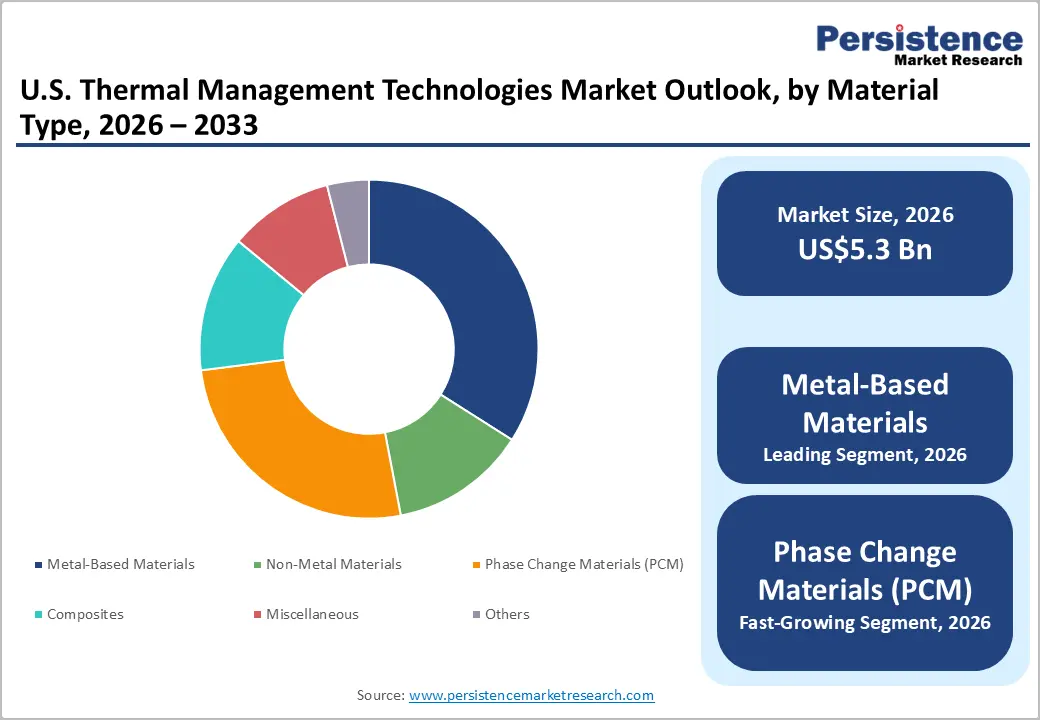

| U.S. Thermal Management Technologies Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 9.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.4% |

Market Dynamics

Drivers - Exponential Data Center Power Density and AI Infrastructure Demands Creating Critical Thermal Engineering Requirements

The structural shift toward AI-optimized data centers is placing unprecedented thermal loads on facility infrastructure, establishing high-performance cooling as a non-negotiable operational requirement. As AI training and inferencing workloads deploy high-density GPU clusters with per-rack power levels routinely exceeding 40-100 kW compared to conventional server racks averaging 5-10 kW conventional air-cooling architectures are reaching thermodynamic limits, necessitating advanced liquid and hybrid cooling solutions.

According to research, the U.S. accounts for approximately 94% of total Americas data center operational capacity, with 25.3 GW of active construction and 89% of this pipeline pre-committed prior to deliver a supply-demand imbalance that signals durable demand for advanced thermal infrastructure. Bipartisan legislative momentum reinforces this imperative: the Liquid Cooling for AI Act of 2025, sponsored by Senators Coons and McCormick, directs the Government Accountability Office (GAO) to conduct a formal R&D assessment of liquid cooling deployment in AI compute clusters, while mandating the Department of Energy (DOE) to develop policy recommendations for liquid cooling and heat reuse at the federal level. This legislative engagement within the U.S. Thermal Management Technologies Market confirms that thermal engineering has transitioned from a facilities management consideration to a strategic national infrastructure priority.

Electric Vehicle Adoption and Battery Thermal Management Imperatives Driving Automotive Sector Demand

Battery thermal management systems (BTMS) represent one of the most technically demanding and commercially consequential applications within the U.S. Thermal Management Technologies Market, driven by the electrochemical sensitivity of lithium-ion and emerging solid-state battery architectures to temperature excursions.

According to the International Energy Agency (IEA), U.S. EV sales exceeded 1 in 10 new cars sold in 2024, with first-quarter 2025 sales tracking approximately 10% above the prior-year period, and full-year 2025 EV penetration projected to reach approximately 11% of total car sales. Despite this adoption momentum, battery electric vehicles (BEVs) in the United States remain approximately 30% more expensive on average than comparable internal combustion engine vehicles a differential that makes thermal efficiency improvements, driving range extension, and battery longevity all commercially decisive factors.

Battery cooling systems accounted for 42.35% of EV thermal management revenue in 2024 per industry estimates, with optimized cooling architectures demonstrated to deliver up to 20% driving range extension by reducing temperature differentials across battery cells. The Inflation Reduction Act allocates US$ 7.5 Billion for EV charging infrastructure, creating downstream demand for integrated thermal management solutions across commercial charging corridors, supporting continued adoption of advanced BTMS technologies.

U.S. Aerospace and Defense Modernization Programs Sustaining Demand for High-Performance Thermal Solutions

The U.S. aerospace and defense sector represents a structurally resilient demand anchor for the Thermal Management Technologies Market, characterized by mission-critical reliability requirements and sustained public investment that is insulated from commercial economic cycles. According to the Aerospace Industries Association (AIA) Facts and Figures 2025, using 2024 data, the U.S. aerospace and defense industry generated nearly US$ 995 Billion in total business activity, contributing US$ 443 Billion in economic value equivalent to 1.5% of U.S. nominal GDP, while supporting over 2.2 million workers with average wages of US$ 115,000 56% above the national average.

The sector exported US$ 138.6 Billion in 2024, up from US$ 135.9 Billion in 2023, generating a trade surplus of US$ 73.9 Billion. Honeywell's Power and Thermal Management System (PTMS) for the F-35 Lightning II surpassed one million flight hours across more than 1,100 aircraft in March 2025, underscoring the maturity and scale of deployed thermal management technology in advanced defense platforms. Ongoing investments in digital transformation, AI-driven maintenance, and next-generation combat aircraft further reinforce aerospace and defense as a sustained and high-value end-use sector for precision thermal engineering solutions.

Restraint - High Capital Costs and System Integration Complexity of Advanced Liquid and Immersion Cooling Solutions

Advanced liquid cooling architectures including direct immersion, microchannel, and cold plate systems carry substantially higher upfront capital costs and installation complexity compared to conventional air-cooled infrastructure, creating adoption friction particularly among mid-tier enterprise and colocation operators. Custom liquid distribution unit (CDU) installations, waterproof facility, coolant management systems, and specialized maintenance protocols collectively elevate total cost of ownership well beyond standard HVAC-based cooling deployments.

For organizations operating legacy data center facilities, the retrofitting cost and operational disruption of transitioning to liquid cooling represent material financial and business continuity risks that delay procurement decisions, dampening near-term adoption within the U.S. Thermal Management Technologies Market.

Refrigerant Regulatory Transitions Imposing Compliance Costs and Product Reformulation Requirements

Upcoming regulatory mandates from the U.S. Environmental Protection Agency (EPA) governing high global warming potential (GWP) refrigerants are compelling manufacturers to reformulate cooling systems ahead of compliance deadlines. Vertiv's proactive launch in October 2025 of low-GWP refrigerant versions utilizing R-454B and R-32 of its CoolPhase data center cooling systems, specifically in anticipation of EPA regulations effective January 2027, illustrates the breadth of reformulation activity underway across the industry. These transitions impose R&D costs, supply chain qualification burdens, and product line management complexity that disproportionately affect smaller manufacturers lacking the engineering resources and capital to accelerate reformulation timelines.

Opportunity - Liquid Cooling for Hyperscale and AI Infrastructure: Policy-Backed Commercial Acceleration

Federal legislative and executive engagement with liquid cooling as a strategic technology is creating a policy-backed commercial acceleration opportunity for participants in the U.S. Thermal Management Technologies Market. The Liquid Cooling for AI Act of 2025 explicitly identifies liquid cooling as essential to maintaining U.S. AI infrastructure leadership, with Senator McCormick articulating that "innovative cooling systems capable of supporting advanced chips" are a national competitiveness imperative.

The U.S. Administration's AI Action Plan has simultaneously emphasized streamlined permitting for data center construction and the potential availability of federal lands for AI computing infrastructure, compressing development timelines for new hyperscale facilities that require advanced thermal management from the ground up.

The DOE's mandated assessment of liquid cooling heat reuse opportunities creates additional long-term demand visibility for integrated thermal recovery systems. For manufacturers of cold plates, microchannel cooling modules, immersion cooling systems, and associated thermal interface materials, the convergence of policy mandate, hyperscale pre-commitment pipelines, and legislative R&D investment frameworks provide a uniquely de-risked commercial environment.

EV Thermal Management Innovation: Solid-State Batteries, Heat Pumps, and Predictive Thermal Architectures

The technical evolution of EV powertrains is creating differentiated demand for next-generation thermal management solutions well beyond the current generation of liquid-cooled BTMS, representing a high-value product development opportunity for U.S. Thermal Management Technologies Market participants. The transition toward solid-state battery chemistries which operate within narrower temperature windows requiring temperature maintenance within ±2°C of optimal operating conditions demands fundamentally more precise and responsive thermal management than existing lithium-ion architectures.

Phase change materials and two-phase cooling system deployments have demonstrated efficiency gains of 15 to 25% compared to conventional liquid cooling approaches, creating technology differentiation opportunities for material and systems innovators. Heat pump integration is further advancing EV thermal efficiency, reducing reliance on resistive positive temperature coefficient heaters that account for up to 30% of energy consumption in cold climates, directly extending driving range in winter operating conditions.

Smart algorithms leveraging vehicle-to-cloud connectivity are enabling predictive thermal management that adjusts cooling strategies in real time based on driving conditions, opening software-enabled product revenue streams that complement traditional hardware offerings.

Aerospace and Defense Thermal Management: Hybrid-Electric Aircraft and Next-Generation Defense Platforms

Thermal management innovation requirements for next-generation aerospace programs represent a structurally compelling long-duration opportunity within the U.S. Thermal Management Technologies Market, driven by the electrification of propulsion architectures and the growing power electronics loads of advanced avionics.

Honeywell demonstrated an 80 kW cooling capability for the F-35 PTMS in March 2024 significantly exceeding the current 32 kW operational requirement validated using a Digital Twin model backed by over 2,500 hours of performance testing and 750,000 flight hours of operational data, establishing the technical and commercial precedent for scalable high-capacity cooling in next-generation defense platforms.

The Clean Aviation Project TheMa4HERA, initiated in February 2023 with a 24-partner consortium across 10 European countries and led by Honeywell, focuses on thermal management architectures for hybrid-electric regional aircraft reflecting the multinational collaborative framework through which next-generation aerospace thermal standards are being set, with direct implications for U.S. manufacturers seeking to influence global platform certification requirements. The Honeywell and Reaction Engines Limited MoU for microtube heat exchangers capable of reducing system weight by over 30% further illustrates the weight-efficiency frontier driving aerospace thermal innovation.

Category-wise Analysis

Device Type Insights

Data Centers and Servers represent the dominant device type application within the U.S. Thermal Management Technologies Market, accounting for approximately 30% of total device type revenue in 2026. This leadership position reflects the convergence of unprecedented AI-driven power density escalation, hyperscale construction pipelines with near-zero vacancy rates, and the structural inadequacy of conventional air cooling to manage rack thermal loads at modern computing densities. The U.S. data center ecosystem's 43.4 GW of operational capacity with 93.6% concentrated domestically creates an enormous installed base requiring continuous thermal management upgrades.

Advanced liquid cooling, cold plates, and direct immersion cooling devices are progressively displacing legacy CRAC-based air cooling across high-performance compute deployments, with AI inferencing, financial trading, and streaming workloads demanding always-on, precision-controlled thermal environments. The competitive intensity of cloud service providers on power usage effectiveness (PUE) metrics further drives procurement of best-in-class thermal solutions.

The Automotive and EVs segment is the fastest-growing device type application within the U.S. Thermal Management Technologies Market, propelled by federal electrification incentives, expanding OEM EV program commitments, and the escalating thermal engineering demands of next-generation battery and power electronics architectures. U.S.

Battery thermal management systems specifically liquid-cooled battery modules, waste heat recovery systems, brake and suspension cooling architectures, and cabin seat heating and cooling systems are collectively expanding the per-vehicle thermal management content value. The introduction of 800V fast-charging architectures and higher-nickel cathode battery chemistries further intensifies thermal management requirements, as rapid charge cycles generate heat profiles that demand real-time active cooling responses to preserve cell longevity and safety margins.

Industry Insights

Advanced and Liquid Cooling Devices hold the leading position within the End-Use Industry segmentation of the U.S. Thermal Management Technologies Market, capturing approximately 28% of total end-use industry revenue in 2026. This leadership reflects the fundamental shift in enterprise and hyperscale data center design philosophy away from ambient air management toward precision direct-liquid cooling architectures that can manage rack densities economically unmanageable with air.

Cold plate systems, microchannel heat exchangers, and single- and two-phase direct immersion technologies collectively constitute this segment, with demand underpinned by the sustained pre-commitment of 89% of the U.S. data center construction pipeline.

Eaton's US$ 9.5 Billion acquisition agreement for Boyd Corporation's Thermal business expected to close in Q2 2026 and incorporating Boyd Thermal's projected US$ 1.5 Billion in liquid cooling revenue directly validates the commercial scale and investor confidence defining this segment's leadership position.

Convection and Air-Cooling Devices represent the fastest-growing segment within the end-use industry classification, driven by their cost-effective scalability, established manufacturing ecosystem, and continued relevance in enterprise, industrial, and consumer electronics applications where rack densities remain below the threshold requiring liquid cooling conversion. Heat sink innovations, advanced forced-air systems, heat spreaders, and vapor chamber hybrids are delivering performance improvements that extend air cooling's viability in moderate-density computing environments.

Parker Chomerics' October 2024 launch of the THERM-A-FORM CIP 60 thermal interface material with 6.0 W/m-K thermal conductivity exemplifies the material's innovation, enabling convective systems to meet evolving electronics performance requirements.

Competitive Landscape

The U.S. Thermal Management Technologies market exhibits a moderately consolidated and innovation-driven structure, where a mix of diversified industrial conglomerates and specialized thermal solution providers compete across aerospace, data centers, electronics, automotive, and medical applications. While large players dominate high-value segments such as liquid cooling and defense-grade systems, niche specialists maintain strong positions in thermoelectrics, interface materials, and precision cooling components, creating a semi-oligopolistic environment in advanced applications.

Leading companies shaping the competitive landscape include Honeywell, Eaton, Vertiv, Parker Hannifin (through Parker Chomerics), Boyd Corporation, and Laird Thermal Systems. These firms compete on technological innovation, liquid cooling capabilities, system integration expertise, and long-term defense and hyperscale data center contracts. Strategic acquisitions, digital twin-enabled product upgrades, and expansion in AI-driven cooling infrastructure are intensifying competition, gradually strengthening consolidation in high-growth segments such as liquid cooling and integrated power-thermal platforms.

Key Industry Developments

- In November 2025, Boyd Corporation announced a definitive agreement to sell its Thermal business to Eaton for $9.5 billion, with the transaction expected to close in the second quarter of 2026 pending regulatory approvals. The deal represents a significant consolidation move within the U.S. Thermal Management Technologies market, transferring Boyd’s advanced thermal solutions portfolio to Eaton’s power management platform. This transaction is poised to strengthen Eaton’s capabilities in integrated thermal and power solutions across high-growth sectors including data centers, electrification, and industrial applications.

- In July 2025, Oklo Inc. and Vertiv announced a collaboration to co-develop integrated power and thermal management solutions for hyperscale and colocation data centers in the United States. The partnership will leverage steam and electricity from Oklo’s Aurora advanced nuclear power plant to drive Vertiv’s cooling systems, enhancing energy efficiency and resilience for AI and high-performance computing facilities. This strategic initiative represents a significant advancement in the U.S. Thermal Management Technologies market, aligning next-generation cooling innovation with clean energy deployment to address rising data center power demands.

- In March 2024, Honeywell announced the successful demonstration of an upgraded 80kW cooling capability for the F-35 Lightning II Power and Thermal Management System (PTMS), significantly exceeding the current 32kW requirement. Using a Digital Twin model backed by over 2,500 hours of performance testing and 750,000 flight hours of operational data, Honeywell validated a low-risk enhancement to existing heat exchanger and control systems. This development marks a major advancement for the U.S. Thermal Management Technologies market, reinforcing scalable, high-capacity cooling solutions to support next-generation avionics and defense modernization programs.

Companies Covered in U.S. Thermal Management Technologies Market

- Honeywell International Inc.

- Liard Thermal System

- Vertiv Co.

- Parker Chomerics

- Boyd Corporation

- Advanced Cooling Technologies, Inc.

- Aavid Thermalloy, LLC

- Wakefield-Vette, Inc

- Siemens AG

- STMicroelectronics

- Gentherm Incorporated

- Parker-Hannifin Corporation

Frequently Asked Questions

The U.S. Thermal Management Technologies Market is projected to be valued at US$ 5.3 Bn in 2026.

The Liquid Cooling Devices segment is expected to account for approximately 28% of the U.S. Thermal Management Technologies Market by Device Type in 2026.

The Market is expected to witness a CAGR of 9.4% from 2026 to 2033.

The U.S. Thermal Management Technologies Market growth is driven by AI-driven hyperscale data center power density requiring advanced liquid cooling, accelerating EV adoption demanding high-performance battery thermal management, and sustained aerospace & defense modernization programs requiring mission-critical precision cooling solutions.

Key market opportunities in the U.S. Thermal Management Technologies Market include policy-backed acceleration of liquid cooling for AI hyperscale data centers, next-generation EV thermal innovations such as solid-state battery cooling and predictive heat management, and advanced aerospace & defense thermal systems for hybrid-electric aircraft and high-power avionics platforms.

Key players in the Thermal Management Technologies Market include Honeywell, Eaton, Vertiv, Parker Hannifin (through Parker Chomerics), Boyd Corporation, and Laird Thermal Systems.