- Automotive Components & Materials

- Automotive Coatings Market

Automotive Coatings Market Size, Share, Trends, Growth, and Forecasts

Automotive Coatings Market By Product (Primer, E-Coat, Basecoat, Clearcoat), Technology (Waterborne Coatings, Solventborne Coatings, Powder Coatings, UV-Cured Coatings), End-Use (OEM, Refinish), and Regional Analysis for 2025 - 2032

Automotive Coatings Market Size and Forecast

Market Overview

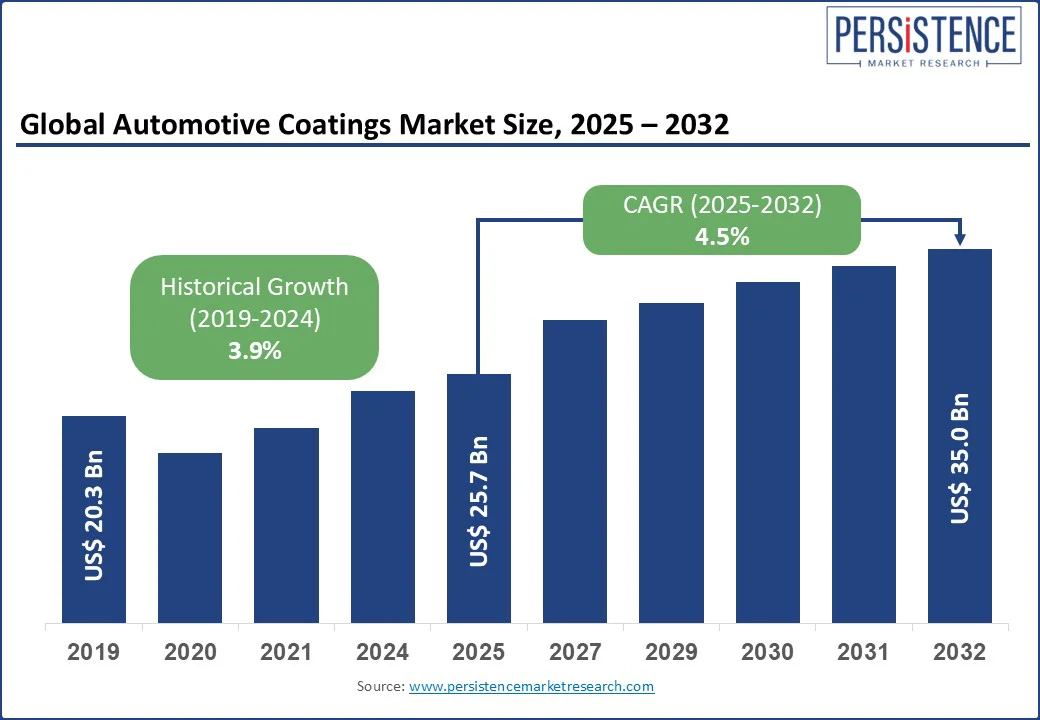

The global automotive coatings market size is likely to be valued US$ 25.7 Bn in 2025 and is projected to grow to US$ 35.0 Bn by 2032, achieving a CAGR of 4.5% from 2025 to 2032. This critical segment of the automotive industry provides protective and aesthetic finishes through automotive surface treatment and vehicle finish solutions.

Growth is driven by rising global vehicle production, increasing demand for advanced car paint coatings with enhanced durability and aesthetics, and a shift toward eco-friendly automotive paint. These Automotive coatings serve automotive OEM applications and the automotive refinish coatings sector, with applications extending to lightweight material coatings for modern vehicles. The market’s expansion is supported by technological advancements, regulatory pressures for sustainable solutions, and growing consumer demand for vehicle customization coatings.

Market Dynamics

Drivers

- Rising Global Vehicle Production Fuels Automotive Coatings Market Growth: The automotive coatings market is experiencing significant growth due to rising vehicle production worldwide. In 2023, global vehicle production reached approximately 80 million units, with projections estimating an increase to 85 million units by 2025, driven by robust demand in emerging markets such as China and India. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), vehicle production in China alone hit 30.16 million units in 2023, reflecting strong market expansion. This surge directly increases demand for high-quality car coatings and vehicle coatings for automotive OEM applications, essential for enhancing durability, aesthetics, and corrosion resistance through advanced automotive surface treatment.

- Electric Vehicle Boom Drives Automotive Coatings Market Expansion: The global surge in electric vehicle (EV) adoption is a key driver for the automotive coatings market. In 2023, the EV market grew by 35%, with 14 million units sold worldwide, according to the International Energy Agency (IEA). This rapid growth increases demand for electric vehicle coating solutions tailored to EV-specific components, such as battery systems and lightweight material coatings for plastics and composites. Notably, car paint coatings for plastic parts in EVs saw a 6% demand increase, enhancing durability, thermal management, and corrosion resistance. For instance, battery enclosures require advanced thermal and dielectric auto body coatings to ensure safety and efficiency. Government initiatives, such as the U.S. Department of Energy’s $7 billion investment in EV battery supply chains, further accelerate EV production, boosting demand for vehicle finish solutions.

Restraints

- Volatility in Raw Material Prices: Fluctuations in the prices of key raw materials, such as titanium dioxide and resins, impact profitability. Smaller players struggled to absorb these increases, leading to reduced competitiveness and delayed product innovation. This cost volatility creates uncertainty and challenges in long-term pricing and contract planning for coatings producers, particularly in emerging markets.

Opportunities

- Smart and Functional Coatings for EVs: The Automotive coatings market is experiencing an increasing adoption of smart and functional coatings for electric vehicles (EVs). Governments worldwide are incentivizing EV production— for instance, China aims for EVs to account for 50% of new car sales by 2035. These coatings offer benefits such as thermal management, corrosion resistance, and EMI shielding essential for EV battery safety and efficiency. This demand drives innovation and expands the automotive coatings market for advanced coatings aligned with government clean energy policies.

- Advancements in Eco-Friendly Coatings: Stringent regulations and consumer demand for sustainability drive innovation in waterborne and powder coatings. BASF’s 2022 Glasurit Eco Balance reduced emissions by 50%, gaining traction in Europe. These coatings align with global VOC reduction goals, offering growth potential as regulations tighten.

Category-wise Insights

Product Type Insights

- Basecoats hold the largest share at 44% in 2025, as they provide the primary color and aesthetic appeal for vehicles through vehicle customization coatings. They provide the vehicle’s color and aesthetic appeal, critical for consumer satisfaction. Their widespread use in OEM and refinish applications, supported by innovations such as Axalta’s advanced basecoat systems, ensures market leadership. Basecoats’ versatility in offering metallic, pearlescent, and matte finishes drives their demand across passenger and commercial vehicles.

- E-coats are the fastest-growing segment in car coatings. Their growth is driven by their corrosion-resistant properties, essential for EVs and lightweight material coatings in vehicle components. The segment’s growth is fueled by increasing EV production, requiring durable coatings for battery components, and eco-friendly cathodic epoxy e-coats, adopted by BMW in 2022, reducing waste by 20%, per BASF data.

Technology Insights

- Water-borne coatings for cars lead the leading market segment, driven by regulatory mandates and their eco-friendly automotive paint profile. They are widely adopted in North America and Europe due to stringent emission standards for VOC-compliant coatings. Increasing demand for sustainable coatings in EV and refinish applications further accelerates growth.

- UV-cured coatings are the fastest-growing technology in auto body coatings. Their rapid curing and energy efficiency make them ideal for high-speed automotive OEM applications.

End-Use Insights

- The OEM segment dominates, accounting for 71% of the market in 2025, driven by high vehicle production volumes. With 84.5 million vehicles produced globally in 2022 (OICA), OEMs require large quantities of primers, e-coats, basecoats, and clearcoats. Long-term contracts with suppliers such as AkzoNobel ensure stable demand, particularly in Asia Pacific, where production is concentrated.

- The refinish segment is the fastest-growing segment. Rising vehicle ownership, with global urbanization projected at 68% by 2050 (World Bank), increases repair and customization demand. Axalta’s fast-drying refinish solutions, launched in 2025, cater to urban repair shops, boosting efficiency by 25%. The growing middle class in emerging markets further drives this segment.

Regional Insights

North America Automotive Coatings Market Trends

North America accounts for 22% of the global automotive coatings market in 2025, with the U.S. leading due to its robust automotive industry. The U.S. produced 10.5 million vehicles in 2023, with a projected increase to 11 million by 2025. The Key drivers include:

- EV Adoption: The U.S. EV market grew by 40% in 2023, increasing demand for electric vehicle coating solutions for battery components and lightweight material coatings.

- Regulatory Push: The EPA’s stringent VOC regulations have driven a 50% adoption rate of water-borne coatings for cars in U.S. automotive OEM applications.

- Refinish Demand: The U.S. automotive refinish coatings market is growing, fueled by an aging vehicle fleet and consumer preference for vehicle customization coatings.

Europe Automotive Coatings Market Trends

Europe holds a 25% market share in 2025, led by Germany, the UK, and France.

- Germany: As Europe’s largest automotive hub, Germany produced 4.1 million vehicles in 2023. The country’s focus on EV production and eco-friendly automotive paint, driven by EU regulations, boosts demand for water-borne coatings for cars and UV-cured car coatings.

- UK: The UK’s automotive sector emphasizes lightweight material coatings for EVs, increasing demand for e-coats and primers in vehicle finish solutions.

- France: France’s focus on luxury vehicles drives demand for high-quality basecoats and clearcoats, with a 6% increase in premium vehicle production in 2023, supported by vehicle customization coatings.

Asia Pacific Automotive Coating Market Trends

Asia Pacific accounts for a significant market share in 2025, led by China, India, and Japan.

- China: As the world’s largest vehicle producer, China manufactured 27 million vehicles in 2023. Rapid EV adoption and government incentives for green technologies drive demand for water-borne coatings for cars and powder auto body coatings.

- India: India’s automotive market is fueled by rising middle-class demand and infrastructure investments. The automotive refinish coatings segment is expanding due to increased vehicle ownership and demand for vehicle customization coatings.

- Japan: Japan’s focus on high-performance vehicles and technological innovation drives demand for UV-cured car coatings, with a 7% growth in their adoption in 2023.

Competitive Landscape

The global automotive coatings market is highly competitive. Companies such as Sherwin-Williams and Axalta invest heavily in R&D, with budgets exceeding US$300 million annually, to develop eco-friendly automotive paint and high-performance auto body coatings. Collaborations with OEMs, such as BASF’s partnership with BMW, ensure tailored automotive OEM applications and market expansion. Firms such as PPG and Akzo Nobel prioritize VOC-compliant coatings to comply with regulations and meet consumer demand for green car coatings.

Key Developments

2023: PPG Industries launched a new line of water-borne coatings for cars, reducing VOC emissions by 20% and gaining traction in Europe and North America.

2024: BASF introduced a bio-based primer, enhancing sustainability in eco-friendly automotive paint and securing contracts with major EV manufacturers.

2024: Akzo Nobel partnered with Tesla to supply electric vehicle coating solutions for its Gigafactory in China, boosting its market share in the Asia Pacific.

Companies Covered in Automotive Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- NIPSEA Group

- RPM International Inc.

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints

- Berger Paints India Axalta Coating Systems, LLC

- FUJIKURA KASEI CO., LTD. KCC Corporation.

Frequently Asked Questions

The automotive coatings market is projected to reach US$25.7 billion in 2025.

Rising global vehicle production, growth in electric vehicles, and increasing consumer demand for vehicle customization coatings and eco-friendly automotive paint are the key market drivers.

The automotive coatings market is poised to witness a CAGR of 4.5% from 2025 to 2032 for the Automotive Coatings Market.

The development of eco-friendly automotive paint and advancements in smart auto body coatings are the key market opportunities.

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., NIPSEA Group, RPM International Inc., BASF SE, Kansai Paint Co., Ltd., Asian Paints, Berger Paints India, Axalta Coating Systems, LLC, FUJIKURA KASEI CO., LTD., and KCC Corporation are among the key market players in the Automotive Coatings Market.