- Beverages

- U.S. Liquid Coffee Market

U.S. Liquid Coffee Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Liquid Coffee Market by Coffee Type (Espresso, Cappuccino, Americano, Latte, Others), Serving Type (Hot Coffee, Cold Coffee), Flavor (Flavored, Unflavored), End-use (Coffeehouses and Beverage Shops, Bakeries and Restaurants, Others), by Zone Analysis, 2026 - 2033

U.S. Liquid Coffee Market Size and Trend Analysis

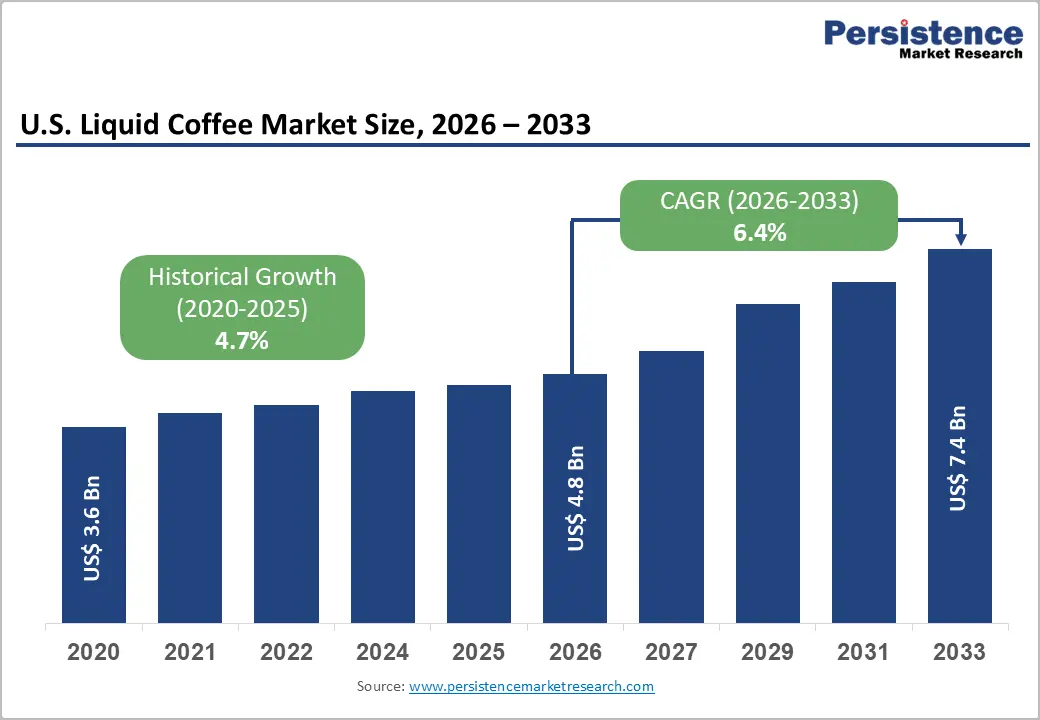

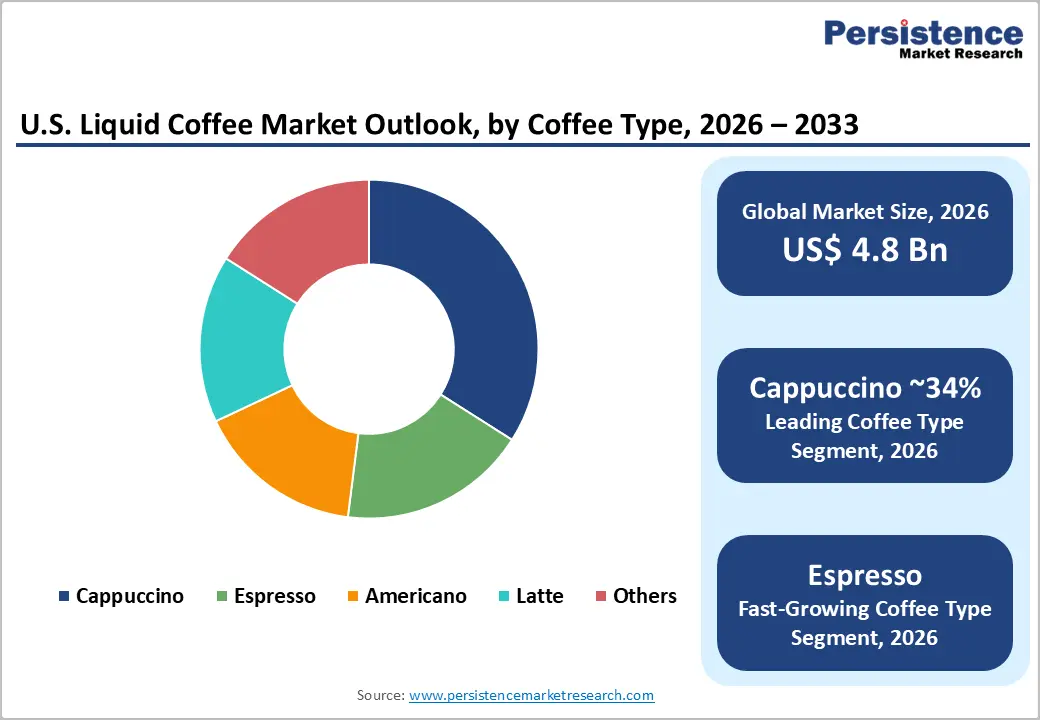

The U.S. liquid coffee market size is expected to be valued at US$ 4.8 billion in 2026 and projected to reach US$ 7.4 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. Rising demand for convenient, ready-to-drink, and premium coffee beverages, increasing urban lifestyles, busy consumer routines, and the expansion of café culture are supporting higher consumption of liquid coffee across households and foodservice channels.

According to the National Coffee Association, nearly 195 million American adults drink coffee each week, with 66% consuming coffee daily, making it the most popular beverage in the country. Growing preference for specialty coffee, cold brew, flavored variants, and at-home coffee preparation further strengthens market demand. Additionally, innovation in packaging, health-focused formulations, and premium product offerings is driving expansion, while strong retail distribution and foodservice adoption continue to support long-term market growth.

Key Industry Highlights:

- Leading Region - The West U.S. leads the national Liquid Coffee market with approximately 33% revenue share in 2025, anchored by California, Oregon, and Washington's specialty coffee culture, the highest coffeehouse density per capita, and the birthplace of Starbucks Corporation.

- Fast-Growing Market - The Southwest U.S. is the fastest-growing liquid coffee market, driven by Texas and Arizona recording among the highest U.S. population growth rates per the U.S. Census Bureau, expanding specialty coffeehouse penetration, and young demographics with strong cold coffee affinity.

- Dominant Coffee Type - Cappuccino leads the Coffee Type segment with approximately 34% U.S. market share in 2025, driven by its premium positioning, versatility across hot and iced formats, plant-based milk adaptability, and consistent menu prominence at Starbucks, Dunkin', and independent specialty operators.

- Fastest Growing Coffee Type - Espresso is the fastest-growing coffee type, growing at nearly double the overall category rate among Gen Z consumers per the NCA. Seasonal innovation, iced espresso formats, and premium positioning at both national chains and specialty independents are propelling this high-margin segment's rapid expansion.

Market Dynamics

Driver - Rising Per-Capita Coffee Consumption and Premiumisation Trend Across U.S. Demographics

The U.S. maintains the highest absolute coffee consumption volumes globally, and a powerful premiumisation trend is driving revenue growth well above volume growth rates. The National Coffee Association's (NCA) 2024 National Coffee Data Trends Report confirms that specialty coffee consumption encompassing espresso drinks, cappuccinos, lattes, and cold brew has reached an all-time high, with 51% of U.S. coffee drinkers consuming specialty beverages daily.

The Specialty Coffee Association (SCA) notes that the average transaction value at specialty coffee outlets has increased by over 18% between 2020 and 2024, reflecting consumer willingness to pay premiums for quality-differentiated liquid coffee products. This premiumisation dynamic is benefiting established chains including Starbucks Corporation and Caffè Nero as well as independent specialty operators across all five U.S. regions.

Restraints - Rising Coffee Bean Prices and Supply Chain Cost Pressures

Green coffee bean price volatility represents a persistent structural challenge for U.S. liquid coffee operators. The International Coffee Organization (ICO) reported that global arabica coffee prices reached 30-year highs in 2024, surpassing US$ 3.00 per pound on the ICE Futures Exchange, driven by persistent drought conditions in Brazil and Vietnam and logistics disruptions. These commodity price increases translate directly into higher menu prices and margin compression for liquid coffee operators, potentially dampening consumer visit frequency and transaction volume, particularly among price-sensitive mid-market consumers who represent a significant portion of coffeehouse and quick-service restaurant foot traffic.

Opportunities - Espresso - Fastest Growing Coffee Type and Menu Innovation Frontier

Espresso is the fastest-growing coffee type segment within the U.S. Liquid Coffee market and represents a compelling product innovation and margin expansion opportunity for operators. The SCA identifies espresso-based drinks, including lattes, cappuccinos, macchiatos, and flat whites, as the category with the highest innovation velocity in U.S. coffeehouse menus, with seasonal and limited-edition espresso beverage launches becoming a core traffic-driving strategy for chains including Starbucks Corporation and McCafé USA.

The NCA's 2024 Data Trends Report notes that espresso drink consumption among Gen Z (aged 18-26) consumers is growing at nearly double the rate of overall coffee consumption, creating a long-runway demand trend as this demographic cohort has matured into high disposable income brackets. Investment in barista training, equipment upgrades, and seasonal flavour innovation positions operators to capitalise on this high-growth segment.

Category-wise Analysis

Coffee Type Insights

Cappuccino leads the U.S. Liquid Coffee market by coffee type, accounting for 34% of total market share in 2025. Cappuccino's market leadership reflects its status as the quintessential espresso-milk beverage, balancing the intensity of espresso with steamed milk and foam in a format that appeals to both experienced and entry-level specialty coffee consumers. The Specialty Coffee Association (SCA) identifies cappuccino as consistently among the top three best-selling espresso drinks at U.S. specialty coffee outlets.

Its versatility with seasonal flavour variations, iced formats, and plant-based milk adaptations enables operators to command premium pricing while sustaining high consumer order frequency. Starbucks, Dunkin', and McCafé USA all feature cappuccino prominently in their core menu architectures. Espresso is the fastest-growing coffee type, owing to rapid adoption by Gen Z’s and attractive coffee menus.

Serving Type Analysis

Hot Coffee remains the leading serving type of segment, accounting for 58% of total U.S. Liquid Coffee market revenue in 2025. The dominance of hot coffee reflects the deeply ingrained morning coffee ritual among U.S. consumers. The NCA reports that over 79% of U.S. coffee drinkers consume coffee in the morning, with hot formats representing the dominant morning occasion beverage. Hot espresso-based drinks, such as cappuccinos, lattes, and Americanos, benefit from higher average selling prices than drip coffee, elevating revenue contribution beyond volume share. Cold Coffee is the fastest-growing serving type, with the NCA documenting a 300%+ surge in cold brew consumption since 2016 and iced espresso drinks becoming the most popular menu innovation format among consumers aged 18-34 across all U.S. regions.

End-user Insights

Coffeehouses and beverage shops represent the dominant end-user segment, accounting for approximately 62% of total U.S. Liquid Coffee market revenues in 2025. The coffeehouse format, anchored by national chains including Starbucks Corporation, Dunkin' Donuts LLC, Costa Coffee, and Caffè Nero, provides the primary out-of-home liquid coffee consumption occasion for U.S. consumers. The National Restaurant Association (NRA) identifies coffee and specialty beverage sales as the fast-growing revenue category within the broader foodservice industry.

The bakeries and restaurants are the fast-growing end-user category, driven by the integration of specialty espresso programmes into non-traditional foodservice environments from artisan bakeries and fast-casual restaurants to hotel lobbies and airport concessions, expanding the accessible occasions for premium liquid coffee consumption beyond the standalone coffeehouse format.

Zone Insights

West U.S. Liquid Coffee Market Trends and Insights

The West U.S. leads the national Liquid Coffee market with approximately 33% of total U.S. revenue share in 2025. The region is the birthplace of the modern U.S. specialty coffee movement, originating in Seattle, Washington, with Starbucks, and maintains the highest per-capita specialty coffee shop density in the country. California, Oregon, and Washington drive premium espresso demand, strong cold brew adoption, and a sophisticated independent coffeehouse culture that commands premium pricing and sustained high visit frequency.

Southwest U.S. Liquid Coffee Market Trends and Insights

The Southwest U.S. is the fastest-growing liquid coffee regional market, supported by Texas and Arizona's position among the five fastest-growing U.S. states per U.S. Census Bureau data. Austin, Dallas, and Phoenix are experiencing rapid specialty coffeehouse expansion, with independent and regional chains filling demand from young, affluent consumer demographics with high specialty coffee affinity. The region's warm climate additionally supports year-round cold coffee consumption growth.

Competitive Landscape

The U.S. liquid coffee market is moderately concentrated, with Starbucks Corporation commanding the largest single share of out-of-home liquid coffee revenues, followed by Dunkin' Donuts LLC and McCafé USA. Strategic priorities among market leaders include menu innovation through seasonal espresso launches, expansion of digital loyalty programmes, cold coffee category investment, and drive-through format growth.

Emerging brands, including Gloria Jean's Coffees and Coffee Beanery compete through specialty positioning and franchise expansion. The Kraft Heinz Company and The J.M. Smucker Company lead the at-home RTD and liquid coffee concentrate segment. DTC e-commerce and subscription coffee models are emerging as competitive vectors.

Key Developments

- In February 2025, Starbucks Corporation announced the national rollout of its expanded cold coffee platform, including new nitro cold brew variants and cold espresso drinks, targeting Gen Z consumers and aiming to achieve 40% of U.S. beverage revenues from cold formats by 2026.

- In January 2025, Nescafé announced its plan to introduce a new range of liquid espresso concentrate in the U.S. in February. The products will be made available in two flavors, namely, sweet vanilla and black. The concentrates are available in 300-ml bottles and are formulated with Arabica beans.

- In October 2024, Dunkin' Donuts LLC launched its revamped espresso programme with new equipment investments across U.S. locations, introducing a premium Cappuccino and Cortado range to compete with specialty coffee operators and capture higher-margin espresso beverage transactions.

- In May 2023, The J.M. Smucker Company expanded its Folgers and Dunkin' branded ready-to-drink liquid coffee concentrate portfolio with new flavored and cold brew variants, targeting the fast-growing U.S. at-home premium liquid coffee segment through major grocery and e-commerce retail channels.

U.S. Liquid Coffee Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.6 Billion |

| Current Market Value (2026) | US$ 4.8 Billion |

| Projected Market Value (2033) | US$ 7.4 Billion |

| CAGR (2026 - 2033) | 6.4% |

| Leading Region | West U.S., 33% market share (2025) |

| Dominant Coffee Type | Cappuccino, 34% market share (2025) |

| Top-ranking Serving Type | Hot Coffee, 58% market share (2025) |

| Incremental Opportunity | US$ 2.6 Billion (2026 - 2033) |

Companies Covered in U.S. Liquid Coffee Market

- Café Amazon

- Café du Monde

- Caffè Nero

- The Kraft Heinz Company

- Costa Coffee

- Dunkin’ Donuts LLC

- Eight O’ Clock Coffee Company

- Four Barrel Coffee

- McCafé USA

- Starbucks Corporation

- All American Coffee LLC

- The J.M. Smucker Company

- Gloria Jean’s Coffees

- Coffee Beanery

- Others

Frequently Asked Questions

The U.S. liquid coffee market is estimated to be valued at US$ 4.8 billion in 2026.

Increasing demand for RTD coffee among millennials and surging preference for on-premise consumption are the key market drivers.

The West U.S. leads with 33% of the national liquid coffee market revenue in 2025.

Rising adoption of kegerator-style cold brew taps in hotels and increasing demand for foam-topped coffee drinks are the key market opportunities.

Café Amazon, Café du Monde, and Caffè Nero are a few key market players.