- Sensors & Controls

- Surface Inspection Market

Surface Inspection Market Size, Share, and Growth Forecast 2026 - 2033

Surface Inspection Market by Surface Type (2D, 3D), by Component (Hardware, Software, Services), Technology (Machine Vision, AI & Deep Learning-Based Inspection, Optical Inspection, Ultrasonic Inspection, Laser Scanning & Profilometry, Others), Industry (Automotive, Semiconductors & Electronics, Metals & Steel, Glass & Ceramics, Aerospace & Defense, Food & Beverages, Paper & Wood, Others), Regional Analysis, 2026 - 2033

Surface Inspection Market Size and Trend Analysis

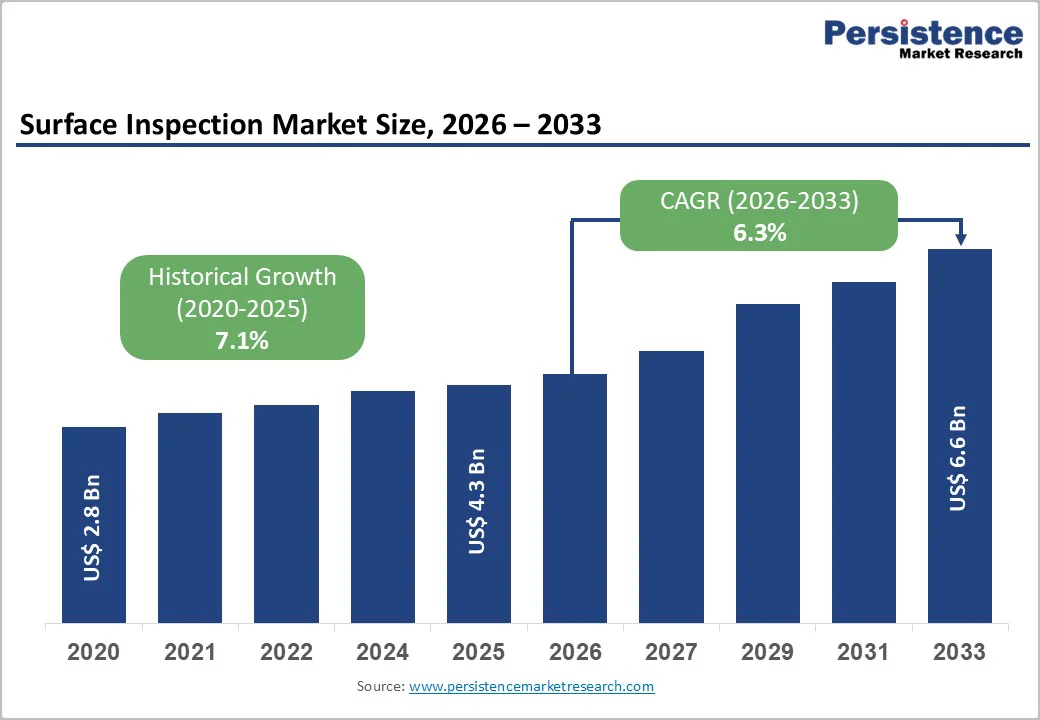

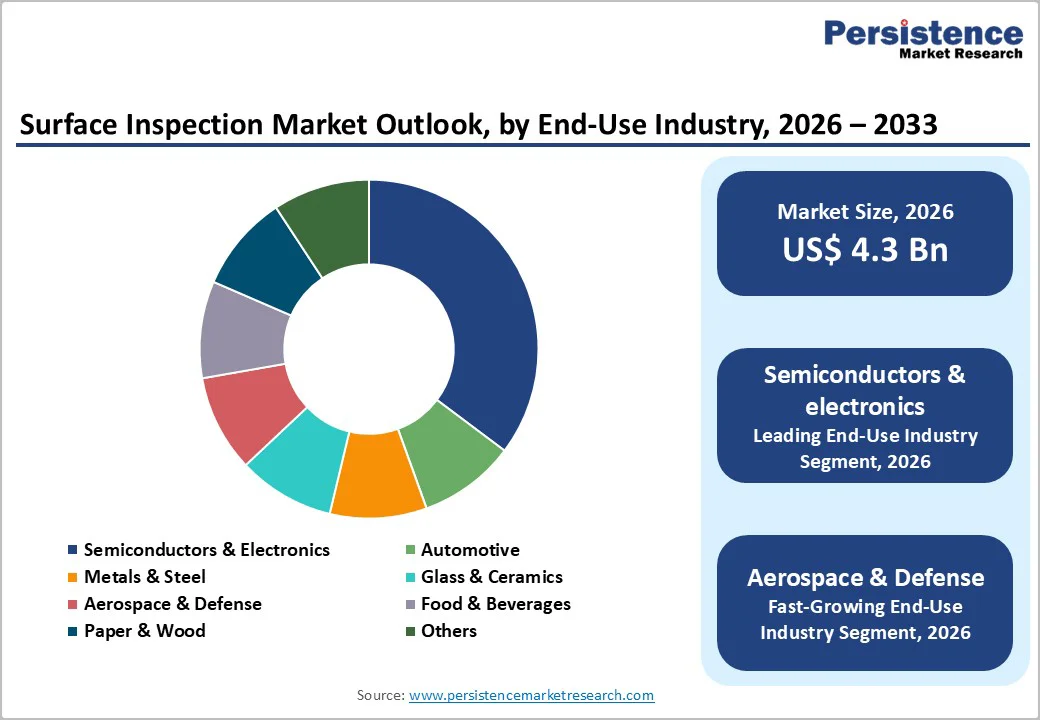

The global surface inspection market size is projected to be valued at US$ 4.3 billion in 2026 and projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market is experiencing robust acceleration due to escalating demand for automation in manufacturing processes driven by labor cost inflation, rapid adoption of artificial intelligence and deep learning algorithms enabling detection of sub-pixel defects, and stringent regulatory compliance requirements in safety-critical industries such as automotive and aerospace. Industries are investing heavily in surface inspection systems to reduce defect rates, which can reach 10-15% in traditional manual inspection environments, and achieve yield improvements of 10-20% through the implementation of advanced vision-based quality control systems.

Key Market Highlights

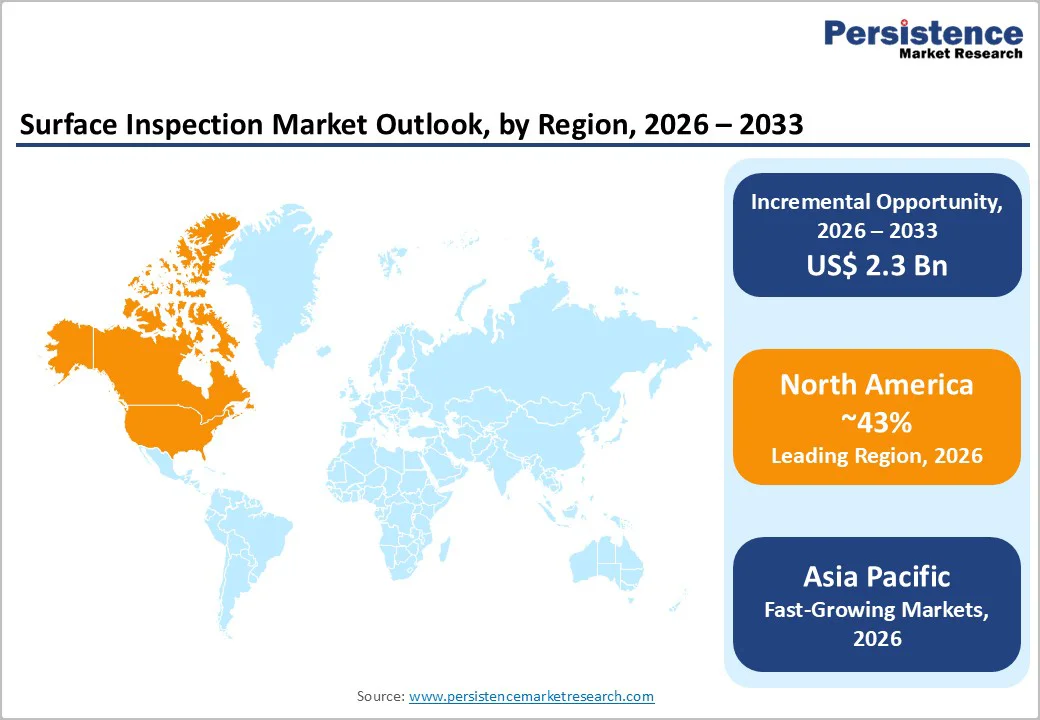

- Leading Region: North America dominates the surface inspection market with 43-45% market share in 2025, driven by advanced manufacturing infrastructure, technology innovation leadership, stringent quality regulations, and substantial government investments in semiconductor domestic production through initiatives like the Chips Act.

- Fastest Growing Region: Asia Pacific exhibits the highest growth trajectory at 10.5-11.2% CAGR through 2032, led by China’s 11.6% CAGR, driven by rapid industrialization, expanding electronics manufacturing capacity, and aggressive adoption of Industry 4.0 technologies across manufacturing sectors.

- Dominant Segment: 3D surface inspection technology leads all segments with 52% market share in 2025, delivering superior capabilities for detecting complex surface defects, measuring topology, and enabling volumetric analysis essential for precision industries including aerospace and semiconductors.

- Fastest Growing Segment: AI & Deep Learning-Based Inspection technology represents the fastest-growing technology segment at 11.5% CAGR through 2032, enabling autonomous defect pattern recognition achieving 97-99% accuracy and reducing false positive rates by 60-70% compared to conventional approaches.

- Key Market Opportunity: Aerospace & Defense industry expansion represents a significant growth opportunity, projected to grow at 8.5% CAGR through 2032, driven by escalating component complexity, stringent regulatory compliance requirements, and critical safety implications necessitating comprehensive defect elimination before component deployment.

| Key Insights | Details |

|---|---|

|

Surface Inspection Market Size (2026E) |

US$ 4.3 Billion |

|

Market Value Forecast (2033F) |

US$ 6.6 Billion |

|

Projected Growth CAGR(2026-2033) |

6.3% |

|

Historical Market Growth (2020-2025) |

7.1% |

Market Dynamics

Market Growth Drivers

Increasing Demand for Automation and Quality Control in Manufacturing

The global manufacturing sector is experiencing unprecedented pressure to implement automated quality control solutions to combat rising labor costs and human inspection inconsistencies. According to the International Federation of Robotics 2023 report, the majority of world manufacturers are prioritizing automation implementation by 2024-2025, representing a critical inflection point for surface inspection technology adoption. Machine vision systems can inspect 300-500 units per minute with 97-99% accuracy compared to human inspectors achieving 85-90% accuracy over the same time period. The U.S. Bureau of Labor Statistics projects that automation sectors, including machine vision systems, will expand by 9% from 2026 to 2033, indicating the transformative role these technologies play across industrial landscapes. Manufacturers across automotive, semiconductors, electronics, and food & beverages are increasingly deploying these systems to maintain product consistency, reduce rework costs, and meet customer quality expectations, creating substantial recurring revenue opportunities for system providers.

Technological Advancements in AI and Deep Learning Integration

Recent breakthroughs in artificial intelligence and deep learning algorithms are fundamentally reshaping surface inspection capabilities and accuracy benchmarks. AI-powered optical inspection systems have achieved detection accuracy rates up to 99% compared to approximately 85% accuracy using traditional rule-based techniques, representing a transformative 16-percentage-point improvement. Taiwan’s TSMC reported a 30% improvement in defect detection rates after integrating deep neural networks into their inspection workflows, while Samsung’s AI-driven inspection systems have achieved 99% accuracy in identifying even subtle gray-level anomalies that conventional methods previously struggled to detect. The integration of convolutional neural networks (CNNs) with high-resolution imaging enables identification of defects smaller than a single pixel, detection speeds exceeding 67,000 profiles per second using blue laser technology, and comprehensive three-dimensional surface analysis. These technological advances are driving adoption across diverse industrial sectors where precision and throughput directly correlate with profitability and competitive positioning.

Market Restraints

High Initial Capital Investment and Implementation Complexity

A significant adoption barrier remains the substantial upfront capital expenditure required for deploying advanced surface inspection systems, with complete system costs ranging from US$ 10,000 to US$ 200,000+, depending on technological sophistication and application requirements. Small and medium-sized enterprises (SMEs) face particular challenges securing adequate financial support and justifying return-on-investment timelines that often exceed 18-36 months for payback periods. Additionally, system integration complexity requires specialized technical expertise, custom calibration procedures for specific production environments, and ongoing maintenance protocols that increase total cost of ownership. The necessity for skilled workforce training, implementation of custom software configurations, and potential production line disruptions during installation create substantial barriers preventing an estimated 40-50% of manufacturing facilities worldwide from implementing advanced inspection solutions.

Data Security and Standardization Challenges in Vision Systems

The expanding connectivity of inspection systems through Industrial Internet of Things (IIoT) networks and cloud-based data analytics platforms introduces significant cybersecurity vulnerabilities and regulatory compliance complexities. Absence of comprehensive international standardization frameworks for machine vision systems creates interoperability challenges when integrating inspection equipment with existing production automation systems and robotic platforms. Organizations must navigate fragmented data privacy regulations across geographic regions, including GDPR in Europe, CCPA in California, and varying national cybersecurity standards, requiring substantial compliance investments. Environmental factors, including ambient lighting conditions, reflective surface properties, and temperature fluctuations, can significantly degrade system performance, with environmental sensitivities causing false positive rates exceeding 20-30% in certain industrial settings.

Market Opportunity

Explosive Growth Potential in AI-Driven Defect Detection and Industry 4.0 Integration

The convergence of machine learning algorithms, Industry 4.0 implementation initiatives, and real-time analytics is creating unprecedented growth opportunities for next-generation surface inspection solutions. The AI industrial defect detection market is projected to reach US$ 5 billion by 2033, representing a 2.2x growth trajectory with particularly robust adoption in electronics manufacturing, where defects represent one third of AI-based inspection demand. Unsupervised learning algorithms and adaptive anomaly detection systems are reducing training data requirements by 60-70%, enabling manufacturers to deploy intelligent defect detection without extensive manual feature engineering. Integration of Internet of Things (IoT) sensors with predictive maintenance algorithms enables manufacturers to predict equipment failures before they occur, reducing unplanned downtime by 35-50% and optimizing resource utilization. Leading industrial enterprises are establishing AI deployment centers and investing heavily in digital transformation initiatives, creating substantial revenue opportunities for solution providers capable of delivering integrated systems combining visual inspection with thermal imaging, ultrasonic analysis, and X-ray inspection modalities.

Category-wise Analysis

Surface Type Insights

3D surface inspection holds the leading position with around 52% market share in 2025, supported by its ability to capture depth, contour, and volumetric details that 2D systems cannot resolve. Using technologies such as laser triangulation and structured light, 3D systems deliver sub-micron point-cloud accuracy essential for components requiring tight geometric tolerances. Industries including aerospace, automotive, semiconductors, and medical devices rely on 3D inspection to identify micro-voids, subsurface cracks, and dimensional deviations with high reliability. Its expanding role in advanced manufacturing, particularly in precision machining and 3D-stacked semiconductor architectures, continues to sustain strong adoption levels.

Component Insights

Hardware constitutes the largest component category with nearly 60% share in 2025, reflecting its central role in establishing the physical inspection architecture. High-resolution cameras, advanced optics, specialized lighting modules, and high-speed processors account for the bulk of system investment, with camera units alone ranging widely in cost based on resolution and frame rate requirements. Hardware demand is reinforced by manufacturers’ reliance on durable, high-performance components capable of supporting continuous, high-speed production environments. As inspection accuracy expectations increase, system builders are investing in next-generation sensors, multi-camera configurations, and edge-processing modules to enhance throughput and defect-detection reliability.

Technology Insights

Machine vision remains the dominant technology with about 45% share in 2025, driven by its ability to deliver high-speed, high-accuracy inspection across diverse industrial workflows. Leveraging sophisticated illumination, high-resolution imaging, and advanced rule-based algorithms, machine vision systems routinely achieve 97–99% detection accuracy while processing images at over 1,000 frames per second. This combination of speed and consistency makes it ideal for applications such as packaging verification, electronics assembly, and automotive finishing. Its scalability-from simple 2D checks to multi-parameter inspection stations-has cemented its position as the industry’s most established technology, supported by continual improvements in imaging hardware and analytical software.

Industry Insights

Semiconductors & electronics represent the largest end-use segment with roughly 38% share in 2025, driven by rapid advancements in chip miniaturization and increasing wafer production volumes. Fabrication processes for sub-10nm nodes demand inspection systems capable of identifying particle contamination, pattern defects, and lithography inconsistencies with near-perfect sensitivity. Automated optical inspection and AI-enhanced defect classification are now integral to yield-management strategies. As device architectures become more complex-particularly with 3D stacking, heterogeneous integration, and advanced packaging-the reliance on high-precision surface and subsurface inspection continues to intensify, reinforcing this segment’s leadership in global market demand.

Regional Insights

North America Surface Inspection Trends

North America commands the leading regional position with approximately 43% market share in 2025, sustained by technological innovation leadership, substantial manufacturing infrastructure, and stringent quality control regulations across automotive, aerospace, pharmaceutical, and electronics sectors. The United States represents the primary growth engine within the region, driven by advanced manufacturing capabilities in precision industries, significant research and development investments by leading technology companies, and government initiatives including the Chips and Science Act promoting domestic semiconductor manufacturing competitiveness.

Major automotive manufacturers including General Motors, Ford, and Tesla have implemented comprehensive surface inspection systems across production facilities, while semiconductor manufacturers based in Arizona and California deploy cutting-edge inspection equipment for next-generation chip production. The region’s innovation ecosystem includes leading solution providers such as Cognex Corporation headquartered in Massachusetts, establishing North America as the global technology innovation center. Companies are investing heavily in AI-powered inspection capabilities, with machine learning algorithms increasingly integrated into existing production automation systems to enhance defect detection accuracy and reduce false positive rates.

Europe Surface Inspection Trends

Europe ranks as the second-largest regional market with approximately 28% market share in 2025, characterized by exceptionally stringent quality standards, rigorous regulatory frameworks, and manufacturing excellence focus particularly in Germany, United Kingdom, and France. Germany emerges as the regional technology leader, home to precision engineering enterprises including ISRA Vision AG (now part of Atlas Copco), Basler AG, and numerous machine vision integrators supporting automotive and semiconductor industries. The region’s manufacturing competitiveness depends on superior product quality differentiation, driving widespread adoption of advanced inspection technologies to maintain competitive advantage against lower-cost manufacturing regions.

European Union regulatory requirements including CE marking compliance, automotive safety standards, and pharmaceutical manufacturing regulations create substantial demand for reliable inspection systems ensuring compliance verification. The region demonstrates the fastest growth trajectory at 9.2% CAGR through 2032, driven by continued industrial modernization initiatives, increasing demand for sustainable manufacturing practices minimizing waste and defects, and government funding supporting Industry 4.0 and advanced manufacturing competitiveness. United Kingdom manufacturers are increasingly deploying surface inspection systems for precision component manufacturing, while France is experiencing rapid automation adoption driven by government incentives and industrial modernization funding supporting technology investment by manufacturing enterprises.

Asia Pacific Surface Inspection Trends

Asia Pacific represents the highest-growth regional market, projected to expand at 10.5% CAGR through 2032, driven by rapid industrialization, expanding electronics and semiconductor manufacturing capacity, and accelerating adoption of automation and Industry 4.0 technologies across manufacturing sectors. China emerges as the regional growth engine, demonstrating exceptional adoption momentum for surface inspection systems with 11.6% CAGR through 2035, supported by government initiatives promoting domestic manufacturing capability, expanding domestic consumer electronics production, and growing semiconductor self-sufficiency priorities. Japan maintains its position as an advanced manufacturing hub with early adoption of 3D surface inspection systems and robotics integration, while South Korea is rapidly expanding semiconductor and display manufacturing capacity, creating substantial demand for precision inspection technologies. India represents an emerging growth opportunity with manufacturing sector digitalization accelerating, rising demand for inspection systems from automotive suppliers and electronics assembly operations, and cost-effective manufacturing capabilities attracting foreign direct investment.

The region benefits from substantially lower labor costs compared to developed markets, enabling price-competitive system deployment while achieving superior quality outcomes compared to traditional manual inspection approaches. ASEAN countries including Vietnam, Thailand, and Indonesia are establishing manufacturing presence attracting investment from global automotive and electronics companies, driving growing demand for surface inspection systems across high-volume production facilities.

Competitive Landscape

Market Structure Analysis

The surface inspection market is moderately consolidated, with a relatively small group of technology leaders shaping overall competitive dynamics while numerous mid-tier and niche providers contribute to a diverse supply base. The market structure is defined by companies that offer fully integrated ecosystems—combining imaging hardware, advanced software, and lifecycle services—enabling them to secure long-term customer relationships and higher switching costs. Business strategies increasingly emphasize AI-driven software differentiation, expansion of cloud-connected analytics, and the development of modular platforms that can be scaled across different production environments. Vendors are also pursuing vertical integration to gain stronger control over component quality and enhance system performance reliability. Partnerships with automation and robotics providers remain central to strengthening turnkey inspection solutions for high-throughput manufacturing lines. Additionally, ongoing consolidation through mergers and acquisitions reflects the industry’s shift toward broader technology portfolios and expanded service capabilities, allowing firms to compete more effectively in global markets.

Key Developments:

- February 2025: TASMIT Inc. launched the INSPECTRA series novel inspection system for glass substrates, representing significant advancement in semiconductor wafer visual inspection technology with enhanced detection capabilities for substrate defects and contamination.

- March 2024: Hitachi High-Tech Corporation introduced the LS9300AD system for inspecting front and backside non-patterned wafer surfaces, equipped with innovative DIC (Differential Interference Contrast) inspection function enabling superior detection of irregular defects on semiconductor wafers.

Companies Covered in Surface Inspection Market

- Omron Corporation

- Panasonic Corporation

- Keyence Corporation

- Cognex Corporation

- Teledyne Technologies, Inc.

- Basler AG

- ISRA Vision AG (Atlas Copco)

- Ametek, Inc.

- VITRONIC Machine Vision

- Matrox Electronic Systems Ltd.

- Baumer Inspection GmbH

- Edmund Optics

- IMS Messsysteme GmbH

- Zebra Technologies Corporation

- SICK AG

- National Instruments Corporation

Frequently Asked Questions

The market is expected to reach US$ 6.6 billion by 2033, up from US$ 4.3 billion in 2026 at a CAGR of 6.3%.

Demand is driven by rising automation needs, higher labor costs, stricter quality regulations, product complexity, and advancements in AI-based defect detection.

3D surface inspection leads with a 52% market share due to its superior defect-detection and topology-measurement capabilities.

North America leads with 43–45% market share, supported by advanced manufacturing, strong R&D, and policy-driven semiconductor expansion.

Major opportunities include AI-enabled inspection, Industry 4.0-based predictive maintenance, rapid Aerospace & Defense growth, and strong Asia Pacific expansion.