- Specialty & Fine Chemicals

- Concrete Resurfacer Market

Concrete Resurfacer Market Size, Share, and Growth Forecast, 2026 - 2033

Concrete Resurfacer Market by Product Formulation (Fiber-Reinforced, Organic Modification, Hybrid Resurfacing), Application (Concrete Floors, Pool Decks, Sidewalks, Driveways), End-User (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

Concrete Resurfacer Market Share and Trends Analysis

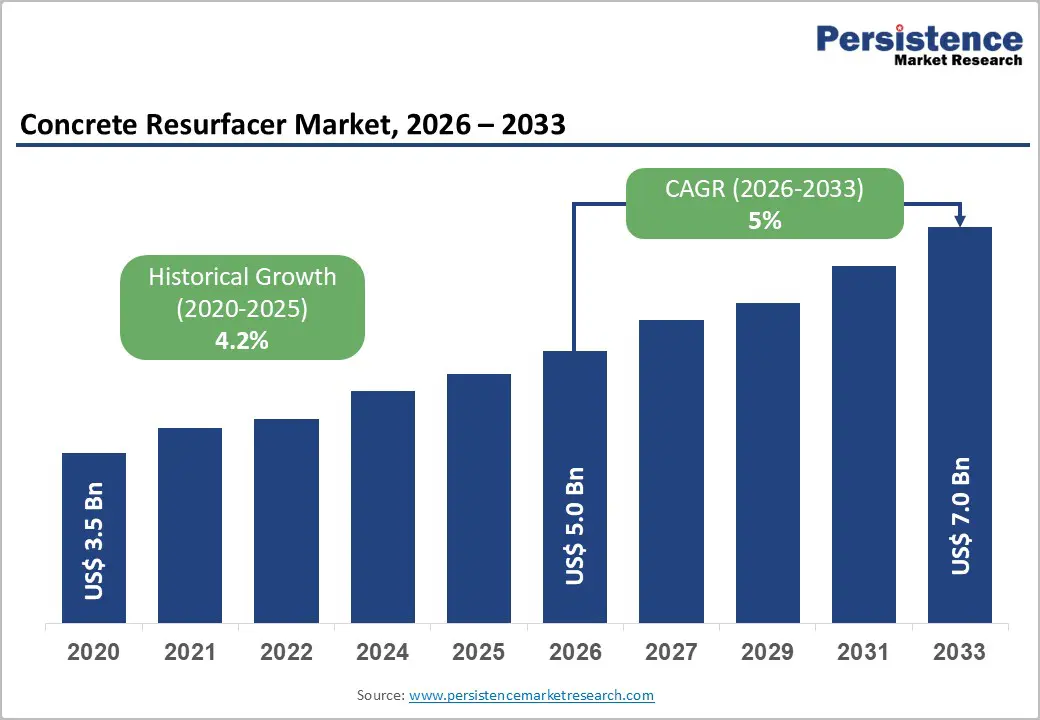

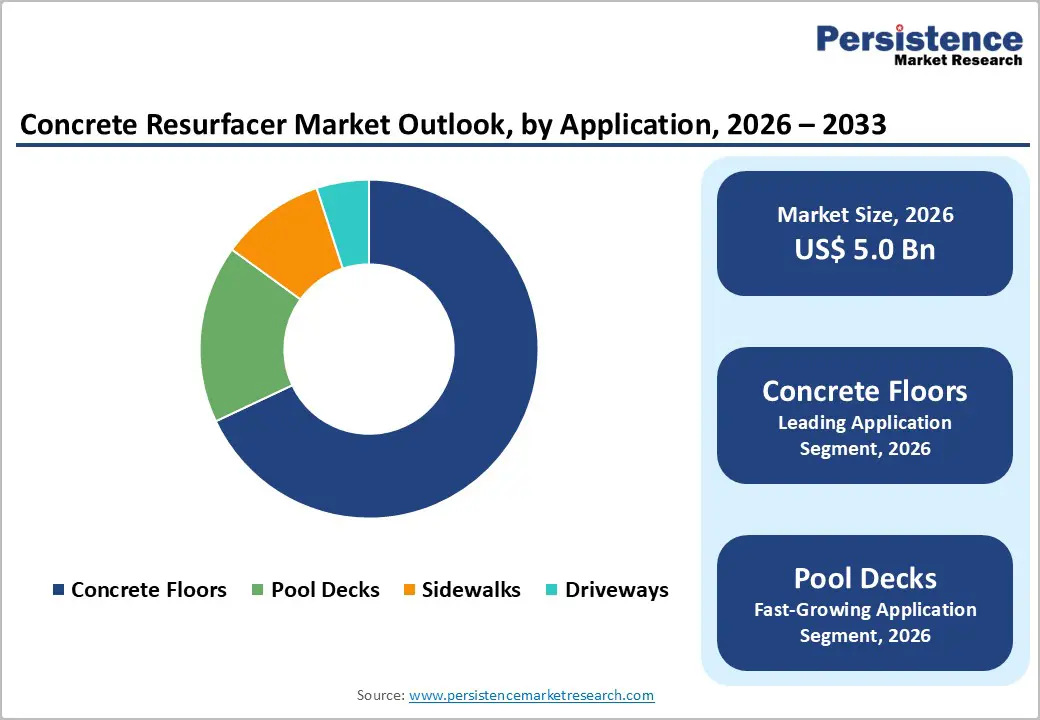

The global concrete resurfacer market size is likely to be valued at US$ 5.0 billion in 2026, and is projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 5.0% during the forecast period 2026 - 2033.

This market expansion is driven by accelerating infrastructure rehabilitation requirements, rising urbanization in emerging economies, and increasing adoption of cost-effective maintenance solutions. The market benefits from technological advancements in polymer-modified formulations that deliver superior adhesion and durability. Growing emphasis on sustainable construction practices and the expansion of decorative concrete applications in residential and commercial sectors further propel market growth, positioning concrete resurfacers as essential solutions for extending the lifespan of aging concrete infrastructure.

Key Industry Highlights

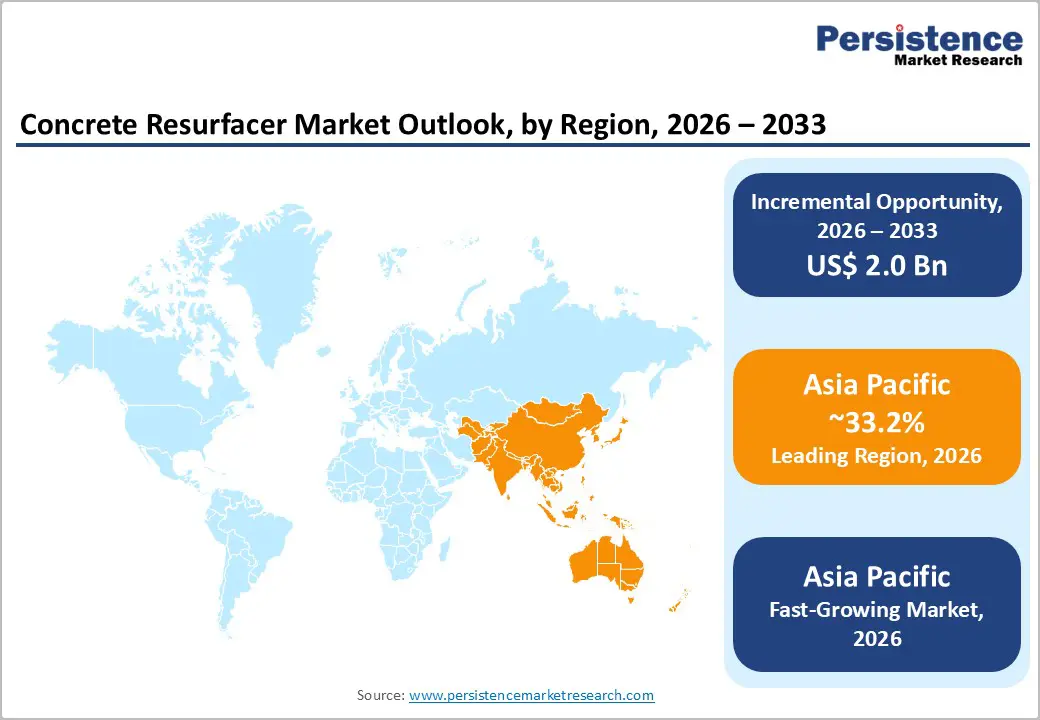

- Regional Leadership: Asia Pacific is expected to be the leading and fastest-growing market with around 33% market share in 2026, supported by rapid urbanization and expansive infrastructure projects.

- Leading & Fastest-growing Product Formulation: Fiber-reinforced is set to dominate with approximately 48.5% revenue share in 2026, with organic modification exhibiting the strongest growth through 2033.

- Major Driver: Aging infrastructure has become a key growth catalyst for the concrete resurfacer market as public assets approach the end of their intended service lives.

- Prominent Opportunity: The accelerating global shift toward sustainable construction practices is creating substantial growth opportunities for eco-friendly concrete resurfacing solutions.

- April 2025: The A64 highway resurfacing project in the U.K. established a benchmark for near-net-zero concrete restoration, demonstrating how advanced low-carbon asphalt formulations and precision milling processes minimize emissions while maximizing pavement longevity.

| Key Insights | Details |

|---|---|

| Concrete Resurfacer Market Size (2026E) | US$ 5.0 Bn |

| Market Value Forecast (2033F) | US$ 7.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Infrastructure Rehabilitation and Aging Concrete Assets

Aging infrastructure has become a key growth catalyst for the concrete resurfacer market as public assets approach the end of their intended service lives. The American Society of Civil Engineers (ASCE) reports that more than 45,000 bridges in the United States are in poor condition and require immediate repair or rehabilitation. This trend extends beyond North America, with bridges, highways, and municipal structures across Europe and Japan showing significant wear due to years of deferred maintenance and environmental exposure. As load-bearing capacity and surface integrity continue to decline, both government agencies and private asset owners are increasingly seeking efficient, cost-effective restoration solutions to preserve structural performance and safety.

Concrete resurfacing has become an essential method for extending the lifespan of existing infrastructure while minimizing capital expenditure and environmental impact. Compared with full demolition and reconstruction, resurfacing generally reduces project costs by 40-60% and minimizes downtime as well as traffic disruption. These advantages align with public infrastructure programs that emphasize efficient spending and sustainability. Governments in North America and Europe are allocating billions of dollars annually to rehabilitation projects through programs such as the Infrastructure Investment and Jobs Act (IIJA) in the United States and the European Investment Plan (EIP). Such initiatives continue to drive strong demand for concrete resurfacer products across highways, bridges, public facilities, and parking structures. As policy emphasis shifts toward preventive maintenance and lifecycle asset management, resurfacing technologies are playing an increasingly pivotal role in optimizing budgets and strengthening infrastructure resilience.

Regulatory and Environmental Compliance Challenges

Evolving environmental regulations are reshaping production and application practices across the concrete resurfacer industry. Agencies such as the United States Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have established stringent limits on volatile organic compound (VOC) emissions and hazardous chemical handling, driving manufacturers toward safer, water-based formulations. While this transition supports long-term sustainability and worker safety, it also introduces technical and financial hurdles. Reformulating solvent-based systems without compromising adhesion strength, curing performance, or weather resistance requires specialized research and capital-intensive process adjustments. Many companies, particularly small and mid-sized firms, face operational strain as legacy solvent-based products undergo phase-out processes or requalification cycles to comply with emerging global standards.

Regional discrepancies in environmental policies further complicate compliance strategies. Standards differ widely across North America, Europe, and Asia, creating inconsistencies in VOC limits, labeling requirements, and permitted additive content. These gaps hinder global product standardization and require manufacturers to maintain region-specific formulations, increasing production and regulatory costs. In addition, phase-outs of hazardous additives disrupt existing supply chains and slow regulatory approval for new materials. Companies that invest in adaptive research and development (R&D) programs, digital regulatory tracking, and early collaboration with governing bodies can mitigate these risks and maintain competitiveness. As environmental policies tighten worldwide, proactive compliance and sustainability-led innovation will become essential for securing market access and maintaining brand credibility in the concrete resurfacer segment.

Sustainable Construction and Green Building Initiatives

The accelerating global shift toward sustainable construction practices is creating substantial growth opportunities for eco-friendly concrete resurfacing solutions. Certifications such as Leadership in Energy and Environmental Design (LEED) and the Building Research Establishment Environmental Assessment Method (BREEAM) increasingly shape material selection criteria in both public and private project. By lowering material consumption and transport requirements, resurfacing contributes to measurable reductions in embodied carbon a key performance indicator under most green building assessment systems. Public agencies and real estate developers now view resurfacing not only as a maintenance strategy but also as a core component of sustainable asset management.

Government policies and carbon reduction commitments continue to accelerate adoption of sustainable materials across the construction sector. In Europe circular economy directives and green procurement guidelines strongly encourage the use of recycled and bio-based components in infrastructure projects. For example, in October 2025, Holcim UK partnered with National Highways to complete a demonstration project on the M5 motorway, incorporating graphene into a section of E21 Stone Mastic Asphalt (SMA) specification to enhance mechanical strength, fatigue resistance, and surface durability while extending pavement life and supporting lower-carbon construction practices. Similar regulatory momentum is emerging in North America and parts of Asia Pacific, where urban development programs integrate carbon footprint reduction and life-cycle performance metrics into project planning. Manufacturers investing in low-carbon, recycled-content, and bio-based resurfacer formulations are well positioned to capture premium pricing from environmentally conscious buyers and institutional investors prioritizing sustainability credentials.

Category-wise Analysis

Product Formulation Insights

Fiber-reinforced is poised to the leading segment in 2026, capturing approximately 48.5% of the concrete resurfacer market revenue share. This dominance is driven by their superior mechanical and structural performance, which combines enhanced tensile strength, excellent crack resistance, and extended durability under continuous load and high-traffic conditions. These formulations use steel, glass, or synthetic fibers to significantly improve the bonding and flexibility of concrete, enabling consistent performance across industrial floors, parking structures, and large commercial spaces. Contractors and facility managers are increasingly recognizing that fiber-reinforced resurfacing systems lower long-term maintenance costs and extend service life, delivering measurable value. As a result, this segment will continue to strengthen its position as fiber-reinforced concrete resufacers remain the preferred choice for both structural restoration and performance-driven resurfacing applications.

Organic modification is likely to be the fastest-growing segment during the 2026-2033 forecast period. This accelerated growth derives from breakthrough polymer-based technologies delivering improved adhesion, flexibility, and aesthetic capabilities. These advanced formulations address evolving market demands for low-VOC emissions, rapid curing times, and enhanced weather resistance across diverse climate conditions. Increasing adoption in residential and light commercial applications, where ease of application and visual appeal are prioritized, drives segment expansion.

Application Insights

Concrete floors are slated to command a projected 35% market revenue share in 2026. This leadership reflects broad usage across residential, commercial, and industrial environments where resurfacing offers a cost-efficient way to restore worn interior and exterior surfaces. In residential properties, homeowners increasingly adopt resurfacing to renew garage floors, basements, and patios without the expense or disruption of full replacement. Commercial spaces such as retail outlets, warehouses, and office complexes rely on high-performance resurfacing systems that provide durability, low maintenance, and aesthetic versatility. Industrial facilities also demand specialized formulations capable of resisting chemical spills, mechanical abrasion, and frequent cleaning cycles.

Pool decks are expected to be the fastest-growing segment during the 2026-2033 forecast period. This exceptional growth trajectory reflects rising consumer emphasis on outdoor living spaces, safety considerations, and aesthetic customization. Modern pool deck resurfacing products incorporate non-slip additives addressing liability concerns while offering extensive design flexibility through colored finishes, textured surfaces, and decorative patterns. The hospitality sector's expansion, particularly resort and recreational facility development in emerging tourism markets, substantially contributes to segment momentum. Aging residential pool infrastructure in developed markets has created a widespread replacement demand, while new construction increasingly specifies decorative concrete finishes that require specialized resurfacer products for long-term maintenance and aesthetic refresh cycles.

End-User Insights

Expected to holding nearly 41% of the revenue share, the commercial segment is well-positioned to lead in 2026, driven by extensive concretization requirements across retail centers, office buildings, warehouses, and hospitality facilities. Commercial property managers prioritize concrete resurfacing for parking structures, loading docks, pedestrian areas, and interior floors to maintain property values, ensure safety compliance, and minimize operational disruptions. The segment benefits from professional procurement processes that recognize lifecycle cost advantages and specify quality materials, supporting premium product adoption. Scheduled maintenance programs at institutional and corporate facilities generate recurring demand, providing market stability and predictable revenue streams for manufacturers serving commercial channels.

The residential segment is anticipated to be the fastest-growing between 2026 and 2033, fueled by a marked increase in home improvement activity and growing consumer awareness of resurfacing solutions. Rising property values incentivize homeowners to invest in curb appeal enhancement and functional upgrades that deliver attractive return-on-investment ratios. The segment accelerated by online tutorials and readily available consumer-grade products at retail channels, expands market accessibility beyond professional contractors. The movement toward decorative concrete is likely to transform concrete surfaces from purely functional elements into design features, driving premium product adoption in residential applications and supporting segment growth outpacing overall market expansion.

Regional Insights

Asia Pacific Concrete Resurfacer Market Trends

Asia Pacific is expected to dominate with a projected 33.2% of the concrete resurfacer market share in 2026, supported by rapid urbanization, expansive infrastructure projects, and a growing middle class that demands better-quality living environments. Countries such as China and India are driving this momentum through large-scale development programs and long-term urban planning initiatives focused on modernizing transport, housing, and public facilities. China’s Belt and Road Initiative (BRI) continue to generate demand for construction materials across multiple partner nations, while India’s Smart Cities Mission has accelerated urban infrastructure upgrades and maintenance cycles. Even in mature economies such as Japan, strict seismic safety standards and an aging infrastructure base sustain consistent demand for repair and strengthening applications. Across the ASEAN, economic expansion and rising infrastructure spending are broadening market opportunities as cities modernize and population densities climb.

Structural advantages further reinforce Asia Pacific market competitiveness in the global concrete resurfacer industry. The region benefits from abundant raw material availability, cost-efficient labor, and a well-established cement manufacturing base, all of which enhance production capacity and supply chain resilience. These factors enable local and international manufacturers to scale operations quickly and offer competitively priced solutions that meet the diverse needs of residential, commercial, and infrastructure projects. However, regulatory standards vary widely across countries, ranging from Japan’s sophisticated quality and safety frameworks to developing compliance systems in emerging Southeast Asian markets. This variation creates both challenges and entry opportunities for producers willing to invest in market-specific certification, training, and technical support.

Europe Concrete Resurfacer Market Trends

The European concrete resurfacer market landscape is governed by a mature and highly regulated environment shaped by advanced construction standards, strong environmental governance, and a long-standing commitment to sustainability. The performance of the regional market is underpinned by extensive infrastructure networks, aging transportation systems, and dense urban environments that require continuous maintenance and rehabilitation. Germany remains the core market, supported by its industrial base and emphasis on preserving road and manufacturing infrastructure. The United Kingdom and France follow closely, with steady demand linked to urban renewal programs, modernization of heritage structures, and sustained commercial development activity. On the other hand, Spain is witnessing renewed momentum as investments in tourism facilities and residential construction strengthen after an extended period of economic stabilization.

The European regulatory framework plays a decisive role in shaping competitive strategy and product innovation. Harmonized product standards and environmental directives established by the European Union (EU), including the Construction Products Regulation (CPR) and European Green Deal, set clear expectations on durability, safety, and carbon performance. These initiatives encourage the adoption of resurfacing solutions that reduce waste generation and extend infrastructure service life, directly supporting circular economy objectives. Compliance, however, comes with stringent testing protocols and certification requirements that demand significant investment in research, development, and technical validation. European manufacturers have responded by focusing on ultra-low-carbon formulations, bio-based materials, and digital application tools that improve accuracy and resource efficiency on job sites.

North America Concrete Resurfacer Market Trends

North America remains one of the most developed and strategically important regional markets globally for concrete resurfacer solutions, owing to mature construction practices, strong regulatory oversight, and consistent infrastructure investment. The United States leads regional growth, driven by the ongoing need to repair and modernize aging bridges, highways, and public facilities. This structural need is reinforced by well-established safety and construction standards that require periodic inspections and rehabilitation to preserve system integrity. The combination of rigorous engineering codes, advanced material technology adoption, and an extensive distribution network ensures product accessibility across diverse geographic conditions, from dense metropolitan areas to remote industrial zones.

The regulatory framework continues to shape industry evolution and competitive positioning. Guidelines from the U.S. EPA on VOC emissions are encouraging the transition toward low-emission and water-based resurfacing formulations. Furthermore, large-scale public infrastructure initiatives have strengthened demand predictability and created long-term purchasing continuity for both public and private stakeholders. North America’s innovation ecosystem, supported by major construction chemical manufacturers, remains a driving force behind global product advancement. Competitive dynamics within the region are characterized by continuous product differentiation, responsive customer service, and strategic partnerships that integrate research, training, and customized on-site technical support establishing North America as both a model of best practices and a key innovation hub for the global resurfacing industry.

Competitive Landscape

The global concrete resurfacer market features a moderately concentrated structure, led by major organizations such as Sika AG, BASF SE, Mapei Corporation, Pidilite Industries Limited, and Ardex Group. These entities have been commanding 55-60% of total market share in 2026 through established brand equity and extensive distribution networks. Market dynamics have been varying significantly across product tiers, with lower-cost categories maintaining accessible entry points that allow regional suppliers to gain traction via competitive pricing and proximity-based logistics. Producers who excel in these segments will have captured volume-driven opportunities by aligning offerings with budget-conscious infrastructure projects in developing regions.

Premium and specialty categories have been safeguarding established players through elevated technical demands and rigorous regulatory standards that deter casual entrants. Manufacturers from emerging economies have been thriving in targeted niches by leveraging customer closeness, flexible supply chains, and customization to regional building norms. This dual-market configuration has been rewarding organizations that balance scale advantages with localized execution. Stakeholders prioritizing innovation in high-barrier segments alongside agile niche strategies will have fortified their positions as construction demands evolve toward durability and sustainability.

Key Industry Developments

- In October 2025, Hoffman Concrete Contractors expanded its service lineup to include concrete resurfacing, allowing customers to restore worn driveways, patios, and walkways without full replacement. The company positions the new service as a cost-effective way to improve durability and curb appeal, complementing its existing residential and commercial concrete offerings

- In September 2025, the New Delhi Municipal Council (NDMC) announced plans to resurface 79 strategically important roads connecting landmarks such as Parliament House and Rashtrapati Bhavan using advanced technologies including hot mix, cold milling, bituminous concrete, and micro-surfacing. The project, developed with CSIR-Central Road Research Institute (CRRI), aims to enhance road durability, safety through thermoplastic markings, and urban mobility while reducing long-term maintenance expenses.

- In February 2025, Like-Nu Concrete launched a spray-on Concrete Restoration Kit for nationwide retail availability, enabling contractors and homeowners to restore distressed surfaces such as driveways, patios, walkways, and pool decks using a proprietary professional-grade formula. The DIY solution offers easy application completing in one to two hours with 30-minute drying time, permeating existing concrete to allow breathability and prevent blistering.

Companies Covered in Concrete Resurfacer Market

- Sika AG

- BASF SE

- Mapei Corporation

- The Quikrete Companies

- H.B. Fuller Company

- CTS Cement Manufacturing Corporation

- LATICRETE International Inc.

- Ardex Group

- The Euclid Chemical Company

- Westcoat Specialty Coating Systems

- Pidilite Industries Ltd.

- Sakrete Inc.

- TCC Materials

- Fosroc International Ltd.

- W.R. Meadows Inc.

Frequently Asked Questions

The global concrete resurfacer market is projected to reach US$ 5.0 billion in 2026.

Aging infrastructure, sustainability regulations, and a strengthening demand for cost-effective restoration solutions across construction sectors are driving the market.

The market is poised to witness a CAGR of 5% from 2026 to 2033.

Major opportunities lie in eco-friendly product innovation, infrastructure modernization programs, and adoption of smart, low-carbon resurfacing technologies.

Sika AG, BASF SE, Mapei Corporation, Pidilite Industries Ltd., and Ardex Group are some of the key players in this market.