- Semiconductor Materials & Components

- Surface Acoustic Wave Filters Market

Surface Acoustic Wave Filters Market Size, Share, and Growth Forecast 2026 - 2033

Surface Acoustic Wave Filters Market by Filter Type (Low-Pass SAW Filters, Band-Pass SAW Filters, High-Pass SAW Filters, Band-Stop SAW Filters), by Frequency Range (Sub-1 GHz, 1–2.5 GHz, 2.5–5 GHz, Above 5 GHz), by Application (Mobile Devices, Telecommunications Infrastructure, Wireless Communication Systems, IoT Devices & Wearables, Signal Processing Equipment), by End-User, by Regional Analysis, 2026–2033

Surface Acoustic Wave Filters Market Size and Trend Analysis

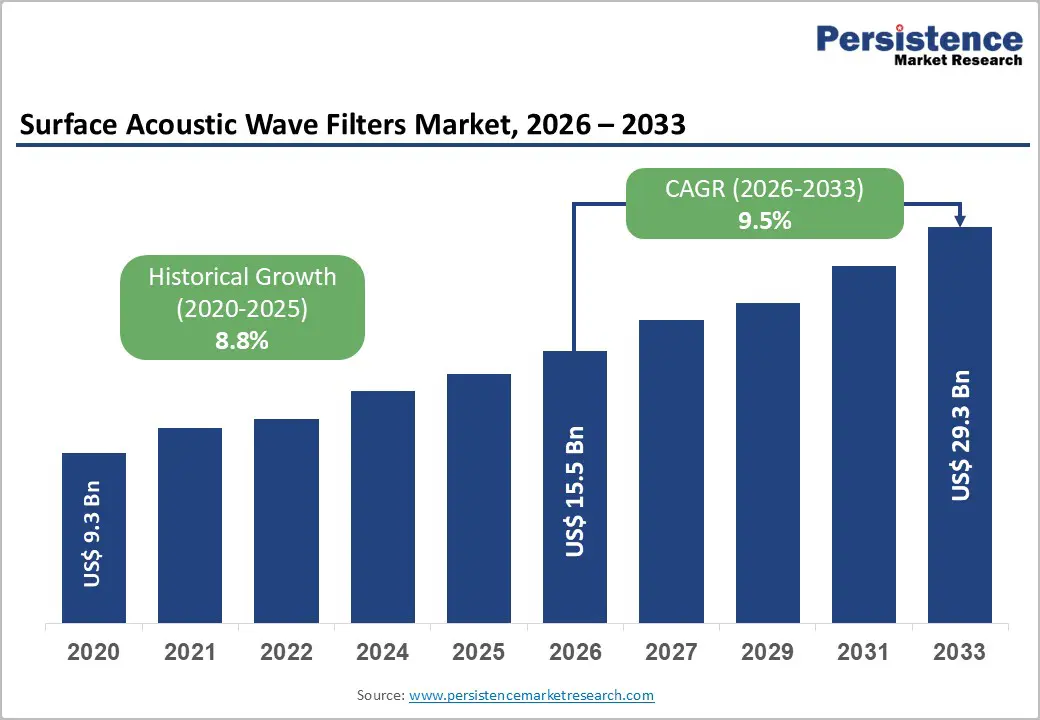

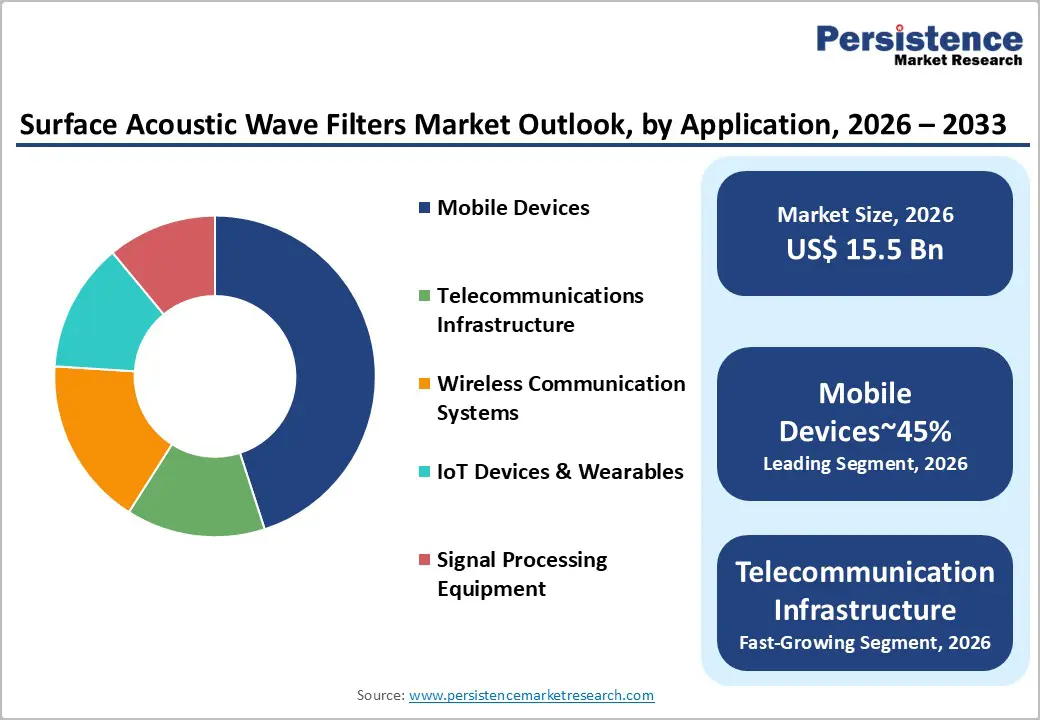

The global Surface Acoustic Wave (SAW) Filters Market size is likely to be valued at US$ 15.5 Billion in 2026 and is expected to reach US$ 29.3 Billion by 2033, growing at a CAGR of 9.5% during the forecast period from 2026 to 2033. Strong demand for compact, low-cost RF filtering solutions in 4G/5G mobile devices, dense telecommunications infrastructure, and rapidly expanding IoT ecosystems is accelerating the adoption of SAW filters.

Key Market Highlights

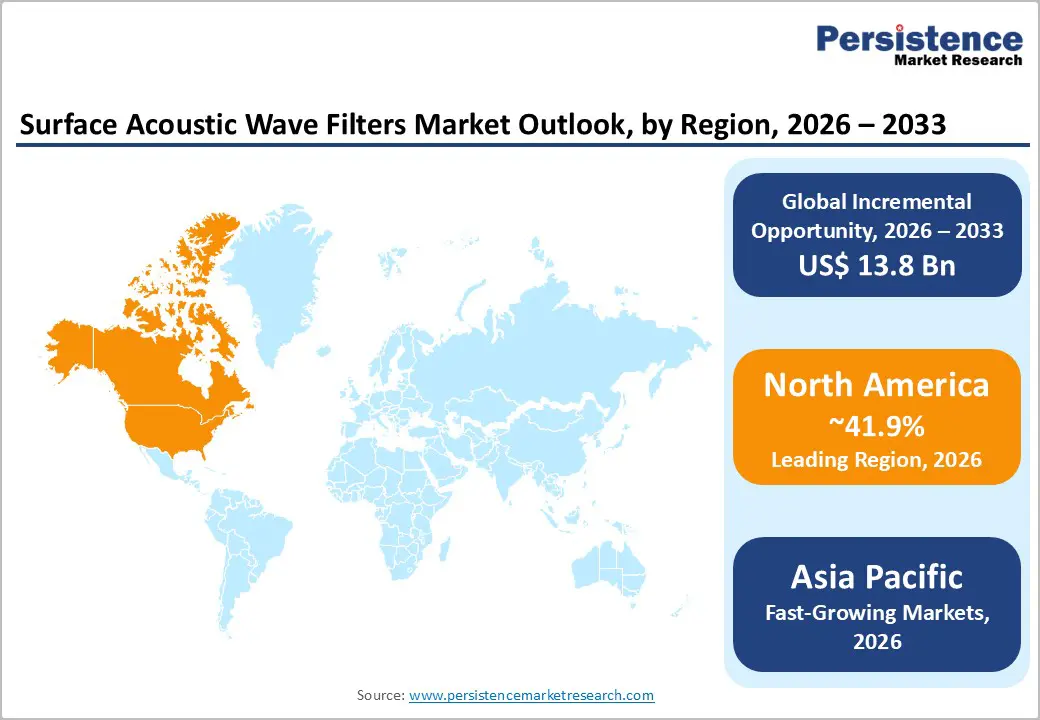

- Leading region: North America remains a leading market for Surface Acoustic Wave Filters, with a 41.9% share, driven by advanced 5G deployment, a strong RF front-end design ecosystem, and early adoption in premium smartphones, networking equipment, and critical infrastructure applications.

- Fastest-growing region: Asia Pacific is the fastest-growing regional market with a rising CAGR of 10.7%, benefiting from large-scale smartphone production, rapid 4G/5G subscriber growth in China and India, and expanding IoT manufacturing, which together amplify SAW filter volumes across applications.

- Dominant segment: By application, Mobile Devices form the dominant segment holding approx 45%, as modern smartphones and tablets integrate dozens of SAW filters for LTE/5G, Wi-Fi, Bluetooth, and GNSS, making handsets the largest consumer of SAW components globally.

- Fastest growing segment: Among end-user industries, Automotive and Industrial connectivity is emerging as a fastest growing cluster, driven by adoption of V2X, telematics, industrial IoT, and smart factory solutions that require reliable low-to-mid band RF filtering.

- Key market opportunity: Major opportunities lie in thin-film SAW, TC-SAW, and hybrid SAW/BAW modules that extend SAW performance into higher bands and harsh environments, enabling suppliers to capture value in 5G, Wi-Fi 6E/7, automotive, and industrial applications.

| Key Insights | Details |

|---|---|

|

Surface Acoustic Wave Filters Market Size (2026E) |

US$ 15.5 Billion |

|

Market Value Forecast (2033F) |

US$ 29.3 Billion |

|

Projected Growth CAGR (2026–2033) |

9.5% |

|

Historical Market Growth (2020–2025) |

8.8% |

Market Dynamics

Market Growth Drivers

Proliferation of 4G/5G Networks and High-Density RF Front Ends

The foremost growth driver for the surface acoustic wave filters market is the rapid expansion of 4G LTE and 5G cellular networks, which significantly increases RF complexity per device. Modern 5G smartphones can integrate 60–100+ RF filters across multiple low, mid, and supplemental bands, compared with a fraction of that in earlier generations.

The annual shipments of acoustic RF filters are projected to roughly double between 2020 and 2025 as 5G and Wi-Fi 6E/7 are rolled out globally, reflecting the multiplication of bands, carrier aggregation, and MIMO configurations. SAW filters are preferred for low- and many mid-band allocations because of their favorable cost structure and mature, high-yield manufacturing. As operators densify networks with macro and small cells, and device OEMs integrate more bands into thin form factors, SAW filters gain additional design-in opportunities across both user equipment and infrastructure RF chains.

Explosive Growth in IoT Devices, Wearables, and Connected Consumer Electronics

A second major driver is the exponential rise of IoT endpoints and connected consumer devices, from smartwatches and wearables to smart home and industrial sensors. Global IoT connections are forecast in multiple industry and governmental assessments to reach tens of billions of devices by the late 2020s, each requiring robust RF filtering for standards such as NB-IoT, LTE-M, Wi-Fi, Bluetooth Low Energy, and Sub-GHz proprietary links.

SAW filters, including TC-SAW and multi-layer SAW variants, offer low insertion loss, compact footprint, and attractive cost for battery-powered devices, making them ideal for wearables and sensor nodes that demand miniaturization and energy efficiency. In addition, many consumer electronics and industrial IoT gateways integrate several radios simultaneously, increasing co-existence challenges and driving demand for high-selectivity SAW filters that can manage interference and maintain signal integrity in congested spectrum environments.

Market Restraints

Growing Competitive Pressure from Bulk Acoustic Wave (BAW) and Advanced Acoustic Technologies

One of the key restraints is intensifying competition from BAW filters and newer acoustic technologies in higher-frequency and ultra-wideband applications. BAW architectures such as FBAR and SMR typically outperform traditional SAW at frequencies above about 2.5–3 GHz, offering better Q factors, power handling, and selectivity required for demanding 5G mid-band and high-band channels as well as Wi-Fi 6E/7.

Major RF players are investing heavily in BAW and derivatives like XBAR®-based resonators to cover upper 5G and WiFi bands, which can displace SAW content in these ranges and cap SAW share growth. As device architectures consolidate more functions into integrated RF modules, design decisions at the module level can privilege BAW in critical paths, limiting the upside for SAW in some premium, performance-centric applications.

Thermal Stability and Performance Limitations at Higher Frequencies

Another restraint stems from SAW’s intrinsic sensitivity to temperature variation and material constraints that can lead to performance degradation at higher frequencies or in harsh environments. For automotive, aerospace, and certain infrastructure applications, stringent requirements on frequency stability, linearity, and power handling challenge conventional SAW designs.

While TC-SAW technologies significantly improve stability, they can still lag advanced BAW in extreme conditions, pushing OEMs toward alternative filters in critical sub-6 GHz and emerging bands. This performance gap can limit SAW penetration in some automotive V2X, radar, and defense systems, where reliability and temperature robustness are paramount, slowing adoption across the highest-margin industrial and mission-critical use cases.

Market Opportunities

Emergence of Thin-Film SAW, TC-SAW, and Hybrid Filter Architectures

Significant opportunity lies in the continued evolution of thin-film SAW, TC-SAW, and hybrid filter modules that blend SAW and BAW within integrated RF front ends. Advanced SAW technologies enable operation further into mid- and even selected higher bands while enhancing temperature stability and linearity. Industry analyses of RF filters in the 2025 timeframe show that improved materials (e.g., LiTaO, engineered substrates) and multi-layer structures allow SAW solutions to handle more mid-band 5G and Wi-Fi 6E/7 channels at competitive die cost.

By co-packaging SAW with BAW and switches, OEMs can optimize performance and cost across the full band portfolio. For SAW filter suppliers, this opens opportunities to remain indispensable in 5G smartphones, IoT gateways, and CPEs as RF modules become more complex. Collaborations with leading RF front-end providers and chipset vendors to co-design such modules represent a compelling path to capture incremental value and defend share.

Expansion into Automotive, Industrial, and High-Reliability Wireless Applications

The rising integration of wireless connectivity in automotive, industrial, healthcare, and smart manufacturing environments creates attractive opportunities for SAW filters beyond traditional handsets. Advanced driver-assistance systems, V2X communication, remote diagnostics, industrial robotics, and medical telemetry increasingly rely on robust sub-6 GHz links with high selectivity and low latency.

Reports on RF filter demand indicate strong adoption of acoustic filters across Automotive & Mobility and Industrial sectors as wireless penetration deepens in safety and control systems. SAW filters, with their proven reliability and cost-efficiency in low-to-mid bands, are well-positioned for applications like keyless entry, tire pressure monitoring, industrial sensor networks, and home healthcare devices. As these sectors digitize and adopt private 4G/5G and dedicated IoT networks, SAW suppliers that qualify their products to automotive and industrial standards and offer extended-temperature and long-lifecycle support can unlock high-value, less-commoditized demand pools.

Category-wise Insights

By Filter Type Analysis

Within filter type, Band-Pass SAW Filters account for an estimated leading share of around 60% of the Surface Acoustic Wave Filters Market, reflecting their central role in channel selection for modern RF systems. Band-pass filters are indispensable in mobile devices, telecommunications infrastructure, and wireless communication systems, where they isolate specific uplink and downlink bands and support carrier aggregation across multiple spectrum blocks.

Industry analyses of RF front ends show that the majority of acoustic filters in smartphones and IoT modules are band-pass devices tuned to narrow frequency allocations across low and mid bands. Their dominance is underpinned by the need to balance selectivity, insertion loss, and compact form factor in densely packed RF modules. As spectrum usage intensifies and coexistence challenges grow, high-performance band-pass SAW filters remain critical for suppressing adjacent-channel interference, thereby sustaining their outsized share compared to low-pass, high-pass, and band-stop SAW implementations.

By Frequency Range Analysis

By frequency range, the 1–2.5 GHz segment is the leading band for SAW filters, with an approximate share of 40% in SAW deployments across key applications. This range maps to many mainstream LTE, legacy 3G/4G, GPS, and sub-2.4 GHz Wi-Fi/Bluetooth bands where SAW technology provides an optimal trade-off between performance and cost. Industry reports on RF filters indicate that SAW remains the workhorse technology in low and mid bands, with BAW gaining prominence only beyond roughly 2.5 GHz and into higher 5G and Wi-Fi 6E channels.

The heavy concentration of global mobile traffic in these mid-bands and the sheer installed base of compatible devices reinforce the leadership of the 1–2.5 GHz segment. As operators continue to refarm spectrum and deploy 5G in lower bands for coverage, SAW filters tuned to this range will remain heavily designed into both devices and infrastructure, sustaining robust unit demand.

By Application Analysis

Across applications, Mobile Devices represent the leading segment, accounting for an estimated 45% of SAW filter consumption, given the enormous global installed base of smartphones and tablets. Modern handsets incorporate dozens of SAW filters for LTE/5G, Wi-Fi, Bluetooth, and GNSS, and global smartphone shipments remain in the hundreds of millions of units per year, with many devices featuring multiple SIMs and expanded band support.

Analyses of RF front-end architectures for mobile phones highlight SAW as the dominant filter type for low and mid-band operations due to its compactness and cost-effectiveness. As OEMs introduce new generations of 5G and advanced Wi-Fi-enabled devices, the content-per-device in filters continues to rise, even where BAW handles some higher bands. Coupled with growth in IoT Devices & Wearables, mobile-centric applications create a strong baseline for SAW demand and anchor long-term volume visibility for leading suppliers.

By End-User Analysis

By end-user, Consumer Electronics leads the Surface Acoustic Wave Filters Market, capturing an estimated share of close to 50%. This segment includes smartphones, tablets, wearables, gaming consoles, set-top boxes, and smart home devices that integrate multi-standard wireless connectivity. RF filter market studies consistently highlight consumer mobile and connectivity devices as the largest sink for SAW filters, driven by volume scale and rapid product refresh cycles.

In 2024, SAW filters accounted for the majority of RF filters used in low- to mid-frequency applications, such as mobile handsets and GPS systems, underscoring their deep penetration in consumer electronics. The proliferation of smart TVs, Wi-Fi mesh routers, and streaming devices further adds to this demand. While telecommunications, automotive, aerospace & defense, healthcare, and industrial are expanding application areas, consumer electronics remains the primary volume engine, shaping cost curves and technology roadmaps for SAW manufacturing.

Regional Insights

North America Surface Acoustic Wave Filters Market Trends

North America is a leading region in the Surface Acoustic Wave Filters Market, underpinned by early adoption of 4G/5G networks, strong RF front-end design capabilities, and a large premium smartphone and networking equipment base. Analyses of RF filters and acoustic technologies indicate that North America accounts for a significant share of global acoustic filter demand, with the U.S. market driving much of this through advanced telecom infrastructure, data center connectivity, and high-end consumer devices. The region is home to major RF front-end and filter players, including Qorvo, Skyworks Solutions, Inc., and Qualcomm Technologies, Inc., which integrate SAW and BAW solutions into modules for leading handset OEMs and network equipment suppliers.

Moreover, North America’s strong innovation ecosystem accelerates the development of advanced SAW derivatives and hybrid solutions. Are companies investing in thin-film SAW, TC-SAW, and new resonator designs to address evolving 5G and Wi-Fi 6E/7 requirements, as illustrated by ongoing R&D and product announcements in RF filter portfolios. Regulatory clarity from U.S. spectrum authorities and continued investment in 5G rollouts, private networks, and automotive connectivity provide a supportive backdrop for SAW demand. As critical infrastructure, defense, and industrial players add more wireless links, North America is expected to remain a technology and design hub for next-generation acoustic filter solutions leveraging both SAW and complementary technologies.

Europe Surface Acoustic Wave Filters Market Trends

Europe represents a robust and technologically sophisticated market for SAW filters, driven by advanced telecom networks, strong automotive and industrial bases, and coordinated regulatory frameworks across the EU. Key countries such as Germany, the U.K., France, and Spain are actively deploying 5G infrastructure, modernizing broadband networks, and promoting digitalization initiatives, thereby increasing demand for RF filtering in base stations, small cells, and consumer devices. European RF and semiconductor suppliers participate in the broader RF filters ecosystem, and collaboration with global leaders enables European OEMs to integrate cutting-edge SAW solutions into communication, automotive, and industrial platforms.

Regulatory harmonization within the European Union—including spectrum allocation policies, device conformity standards, and automotive safety regulations—supports scalable deployment of wireless technologies using SAW-based RF front ends. Germany’s leadership in automotive engineering and industrial automation, combined with the U.K. and France’s strengths in telecom and defense, creates diversified demand for SAW filters in V2X, industrial IoT, and satellite-communication-related applications. As Europe advances Industry 4.0 initiatives and accelerates the adoption of electric and connected vehicles, SAW filters are expected to see increased use in embedded connectivity modules, telematics, and sensor networks, despite some high-frequency applications leaning toward BAW solutions.

Asia Pacific Surface Acoustic Wave Filters Market Trends

Asia Pacific is the fastest-growing region in the Surface Acoustic Wave Filters Market, supported by high-volume electronics manufacturing, aggressive 5G rollouts, and the presence of many leading SAW suppliers. Countries such as China, Japan, South Korea, and emerging ASEAN economies host large-scale production of smartphones, consumer electronics, and networking equipment, all of which heavily utilize SAW filters in low and mid bands. Analyses of regional markets show that China and India are experiencing rapid growth in SAW filter demand, driven by expanding 4G/5G subscriber bases, government-backed digitalization programs, and strengthening domestic electronics manufacturing ecosystems.

Japan and other East Asian countries are also key players, with companies like Murata Manufacturing Co., Ltd., Taiyo Yuden Co., Ltd., and Kyocera Corporation shaping global supply and technology trajectories. Asia Pacific’s cost-competitive manufacturing capabilities and investments in advanced packaging, thin-film processing, and substrate technologies enable high-volume, cost-effective SAW production. As IoT, smart factories, and smart city initiatives scale across China, India, and ASEAN, SAW filters will continue to see robust uptake in both consumer and industrial connectivity applications. The region’s dual role as a demand center and production hub ensures its centrality in the future growth of the global SAW filter landscape.

Competitive Landscape

The Surface Acoustic Wave Filters Market exhibits a moderately concentrated structure, with a group of global leaders alongside specialized regional players. Key companies such as Murata Manufacturing Co., Ltd., Skyworks Solutions, Inc., Qorvo, Inc., Qualcomm Technologies, Inc., Taiyo Yuden Co., Ltd., and Kyocera Corporation leverage strong IP portfolios, advanced manufacturing, and deep integration with handset and infrastructure OEMs to capture significant market share in high-volume segments. These leaders differentiate through R&D in TC-SAW and thin-film SAW, co-integration of SAW and BAW within RF modules, and close co-design partnerships with chipset vendors. Emerging trends include vertical integration from materials to modules, expansion into automotive and industrial connectivity, and business models centered on platform-based RF solutions rather than discrete components. Smaller firms and niche providers compete through custom designs, specialty frequency bands, and application-specific performance optimizations.

Key Market Developments

- January 2026: Skyworks Solutions, Inc. highlighted next-generation acoustic filter and RF front-end solutions for 5G and Wi-Fi applications at CES 2026, emphasizing integrated SAW/BAW platforms for intelligent connectivity.

- November, 2025: Skyworks Solutions, Inc. presented at a leading global technology and AI conference, outlining the role of advanced SAW and BAW filters in enabling dense 5G deployments and high-performance wireless systems.

- 2025: Leading SAW suppliers, including Murata Manufacturing Co., Ltd., Qorvo, Inc., and others, introduced new thin-film SAW and TC-SAW products targeting mid-band 5G and Wi-Fi 6E/7 channels, enhancing frequency coverage and temperature stability of SAW solutions.

Companies Covered in Surface Acoustic Wave Filters Market

- Murata Manufacturing Co., Ltd.

- Microchip Technology Inc.

- Skyworks Solutions, Inc.

- Qualcomm Technologies, Inc.

- Qorvo, Inc.

- AVX Corporation

- Tai-Saw Technology Co., Ltd.

- API Technologies Corp

- Kyocera Corporation

- Abracon

- Taiyo Yuden Co., Ltd.

- TAIYO YUDEN Group

- TDK Corporation

- Broadcom Inc.

- Akoustis Technologies, Inc.

- Resonant

Frequently Asked Questions

The global Surface Acoustic Wave Filters Market is expected to reach around US$ 29.3 Billion by 2033, up from about US$ 15.5 Billion in 2026, reflecting a robust forecast CAGR of 9.5% between 2026 and 2033.

Key demand drivers include the proliferation of 4G/5G mobile networks, increasing RF complexity in smartphones, expansion of IoT devices and wearables, and growing connectivity needs in consumer electronics, telecommunications infrastructure, and industrial environments requiring compact, cost-effective RF filtering.

By application, Mobile Devices constitute the leading segment, as smartphones and tablets integrate a high number of SAW filters for LTE/5G, Wi‑Fi, Bluetooth, and GNSS, making handheld devices the largest consumer of SAW components globally.

North America holds a leading position, supported by advanced 5G deployments, a strong RF design ecosystem, early adoption in premium mobile devices, and significant demand from telecom infrastructure, defense, and critical connectivity applications.

A key opportunity lies in thin‑film SAW, TC‑SAW, and hybrid SAW/BAW RF modules, which extend SAW applicability into higher frequencies and challenging environments, enabling suppliers to tap growth in 5G, Wi‑Fi 6E/7, automotive connectivity, and industrial IoT.

Major players include Murata Manufacturing Co., Ltd., Microchip Technology Inc., Skyworks Solutions, Inc., Qualcomm Technologies, Inc., Qorvo, Inc., AVX Corporation, Tai-Saw Technology Co., Ltd., API Technologies Corp, Kyocera Corporation, Abracon, Taiyo Yuden Co., Ltd., along with additional participants such as TDK Corporation, Broadcom Inc., and Akoustis Technologies, Inc.