- Healthcare IT

- Surface Disinfectant Market

Surface Disinfectant Market Size, Share, and Growth Forecast, 2026 - 2033

Surface Disinfectant Market by Composition (Chemical, Bio-based), Form (Liquid, Wipes, Sprays), End-user (Hospitals, Laboratories, Households, Hotels/Restaurants/Cafes, Educational Institutions), and Regional Analysis for 2026 - 2033

Surface Disinfectant Market Size and Trends Analysis

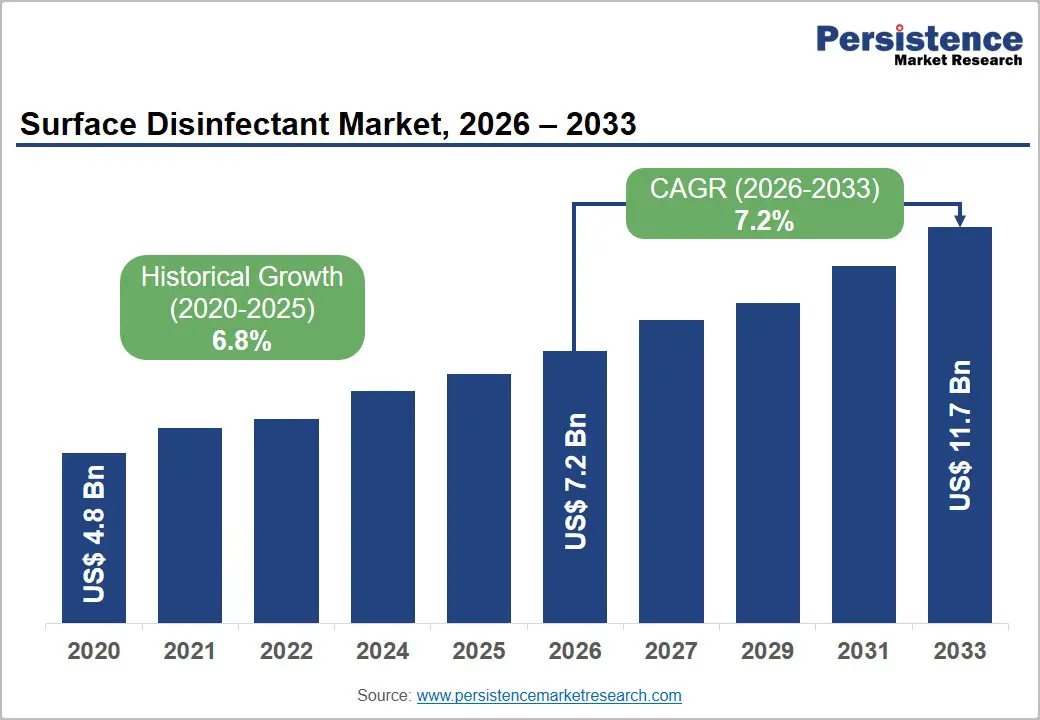

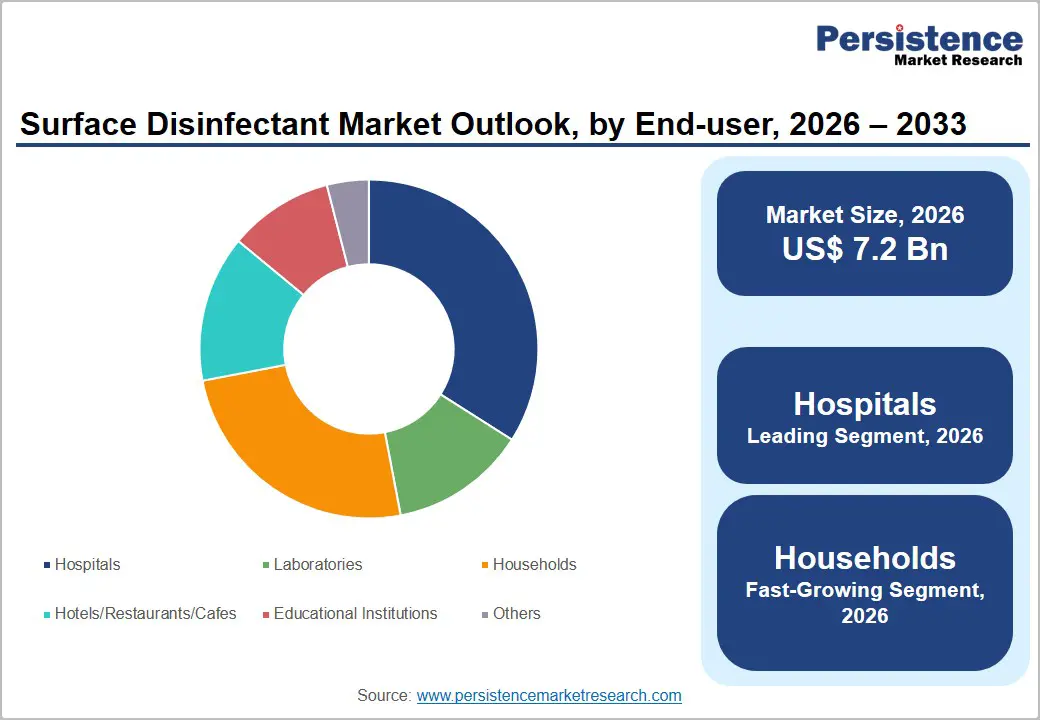

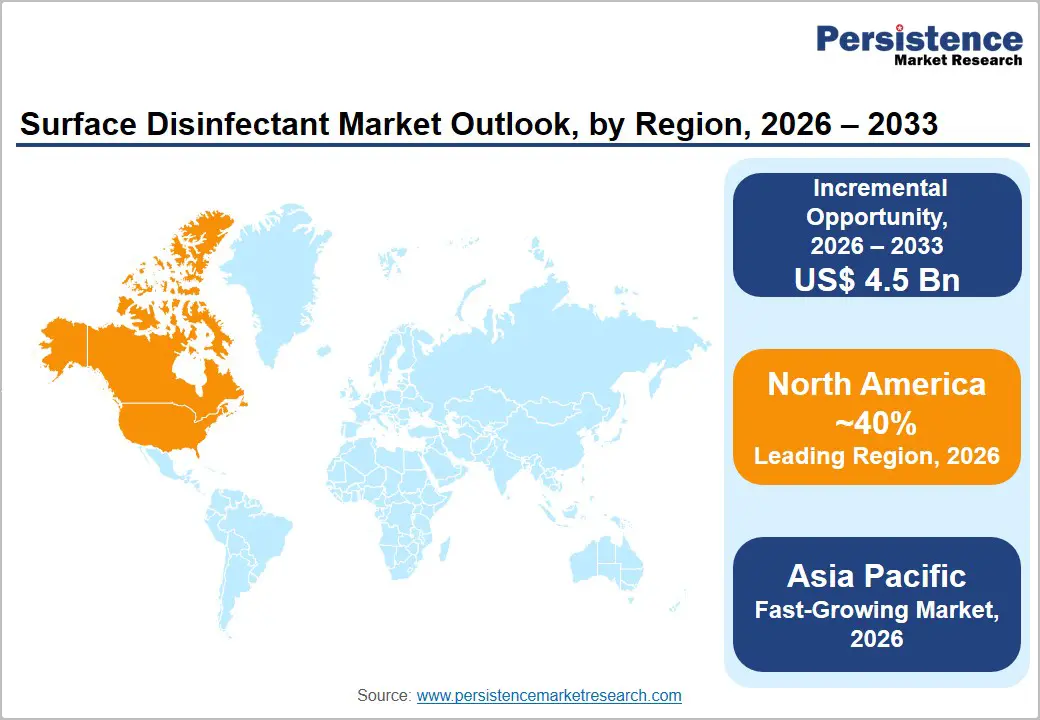

The global surface disinfectant market size is likely to be valued at US$7.2 billion in 2026 and is expected to reach US$11.7 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by increasing emphasis on infection prevention and environmental hygiene across healthcare and commercial sectors.

According to the World Health Organization (WHO, 2024) infection prevention and control (IPC) guidelines, effective surface disinfection is a critical measure to reduce healthcare-associated infections in clinical environments. The U.S. Centers for Disease Control and Prevention (CDC, 2025) continues to recommend routine environmental cleaning and disinfection of high-touch surfaces in healthcare and public facilities to limit pathogen transmission. Regulatory frameworks such as the U.S. Environmental Protection Agency (EPA, List N updates 2024) support approved disinfectant efficacy against emerging pathogens.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong healthcare infrastructure, stringent EPA and CDC regulations, and high adoption of advanced infection prevention solutions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid healthcare infrastructure expansion, urbanization, and rising hygiene awareness.

- Leading Composition: The chemical segment is anticipated to dominate the market in 2026, accounting for 70% of revenue share, driven by its broad-spectrum effectiveness, well-established formulations, and extensive adoption across institutional settings.

- Leading Form: The liquid segment is anticipated to be the leading form, accounting for over 50% of the revenue share in 2026, supported by cost-effective large-scale usage in healthcare and commercial facilities, along with versatility and operational efficiency.

- Key Opportunity: The key market opportunity in the surface disinfectant market is the rising shift toward sustainable, bio-based formulations and advanced ready-to-use disinfection technologies driven by stricter hygiene regulations and expanding healthcare infrastructure.

DRO Analysis

Driver - Rising Prevalence of Hospital-Acquired Infections (HAIs)

The rising prevalence of hospital-acquired infections is a major driver of the surface disinfectant market, as healthcare facilities prioritize infection prevention and environmental hygiene. According to the World Health Organization (WHO, 2024), HAIs remain a significant global patient safety challenge, increasing morbidity, mortality, and healthcare costs. This has led to stricter cleaning protocols and mandatory disinfection practices in hospitals and clinics.

Surface disinfectants are widely used to reduce microbial contamination on high-touch areas such as beds, medical equipment, and surgical rooms, thereby minimizing infection transmission risks in healthcare environments across both developed and emerging healthcare systems. The increasing burden of antimicrobial-resistant pathogens has intensified reliance on effective surface disinfection solutions in healthcare settings.

Regulatory bodies such as the U.S. Centers for Disease Control and Prevention (CDC, 2025) emphasize routine cleaning and disinfection of environmental surfaces to break infection transmission chains. Hospitals are increasingly adopting advanced disinfectant formulations with broad-spectrum efficacy, including alcohol-based and hydrogen peroxide-based products.

Restraint - Structural Challenges from Alternative Disinfection Methods

One key restraint in the surface disinfectant market is the growing adoption of alternative disinfection technologies such as ultraviolet (UV-C) disinfection systems, steam sterilization, and electrostatic spraying technologies. These methods are increasingly being deployed in hospitals and commercial facilities due to their ability to reduce chemical usage and provide automated or contactless disinfection. According to CDC infection control guidance (2025), UV-C systems are being evaluated as supplemental disinfection tools that can reduce dependency on traditional chemical disinfectants in certain high-risk environments.

Concerns regarding chemical exposure, toxicity, and environmental impact are pushing end-users toward non-chemical or low-residue alternatives. Healthcare institutions are increasingly exploring sustainable cleaning systems to comply with environmental safety standards and occupational health guidelines. While chemical disinfectants remain essential for broad-spectrum efficacy, competition from advanced physical disinfection methods and integrated cleaning systems is creating structural limitations in market expansion.

Opportunity - Technological Convergence and Sustainable Formulations

A major opportunity in the surface disinfectant market lies in technological convergence and the development of sustainable, bio-based formulations. Increasing environmental regulations and sustainability commitments by healthcare and commercial institutions are driving demand for eco-friendly disinfectants. According to the U.S. Environmental Protection Agency (EPA, 2024), there is growing emphasis on safer chemical ingredients and reduced environmental toxicity in disinfectant products.

This has encouraged manufacturers to innovate plant-based actives, biodegradable surfactants, and low-residue formulations that maintain high antimicrobial efficacy while reducing ecological impact. Technological integration is also creating new growth opportunities through smart disinfection systems and hybrid cleaning solutions.

Companies are combining chemical disinfectants with automated dispensing systems, IoT-enabled monitoring, and precision application technologies to enhance efficiency and reduce waste. This convergence supports optimized hygiene management in hospitals, laboratories, and commercial spaces.

Category-wise Analysis

Composition Insights

The chemical segment is expected to lead, accounting for 70% of revenue share in 2026, due to its proven broad-spectrum antimicrobial efficacy and rapid action against bacteria, viruses, and fungi. Chemical disinfectants such as alcohols, quaternary ammonium compounds, chlorine-based agents, and hydrogen peroxide formulations are widely used across hospitals and industrial cleaning applications. For example, products from Ecolab are extensively used in hospital sanitation programs to ensure compliance with strict hygiene standards and reduce healthcare-associated infection risks across critical care environments.

The bio-based segment is likely to represent the fastest-growing segment, supported by increasing environmental regulations and rising demand for sustainable and non-toxic cleaning solutions. These products are derived from plant-based extracts, enzymes, and biodegradable surfactants, offering safer alternatives for human health and the environment. For instance, GOJO Industries has introduced greener hygiene solutions under its sustainability initiatives targeting reduced chemical impact while maintaining antimicrobial effectiveness.

Form Insights

The liquid segment is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by its versatility, cost-effectiveness, and suitability for large-scale applications. Liquid disinfectants provide superior surface coverage and are widely used in dilution-based cleaning systems across hospitals, laboratories, and commercial facilities. A notable example includes Diversey liquid disinfectant solutions, which are widely deployed in healthcare environments for terminal cleaning.

Wipes are likely to be the fastest-growing form segment due to convenience, portability, and reduced risk of cross-contamination. They are increasingly used in fast-paced environments such as clinics, laboratories, food service areas, and households where quick disinfection is required. For example, Clorox disinfecting wipes are widely used in residential and commercial settings for rapid surface cleaning.

End-user Insights

Hospitals are expected to account for 50% of the revenue share in 2026, due to strict infection prevention protocols and high-risk patient environments. Continuous exposure to pathogens, surgical procedures, and intensive care requirements drives consistent demand for high-performance disinfectants. For instance, 3M disinfectant solutions are widely used in hospital sanitation programs to maintain sterile environments.

The household segment is likely to represent the fastest-growing segment, supported by rising hygiene awareness, lifestyle changes, and increased focus on sanitation in public-facing environments. Post-pandemic behavioral shifts have significantly increased the use of disinfectants in homes for daily cleaning of kitchens, bathrooms, and frequently touched surfaces. A notable example includes Procter & Gamble’s hygiene products, which are widely used in households and commercial kitchens for routine disinfection.

Regional Insights

North America Surface Disinfectant Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, supported by strong healthcare infrastructure, strict regulatory frameworks, and high awareness of infection prevention. Increasing focus on hospital-acquired infection reduction and adoption of advanced, fast-acting formulations continue to strengthen market growth. For example, Ecolab plays a major role in providing hospital-grade disinfection solutions widely used across healthcare and food service industries.

U.S. Surface Disinfectant Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 85% of the market share in 2026, driven by advanced hospital systems, high healthcare spending, and strict CDC infection prevention protocols. Hospitals and healthcare facilities extensively use EPA-approved disinfectants for surface cleaning in ICUs, operating rooms, and emergency units. Growing concerns over antimicrobial resistance and hospital-acquired infections are encouraging adoption of high-efficiency disinfectants.

Canada Surface Disinfectant Market Trends

Canada is likely to be a significant market for surface disinfectants, holding approximately 15% of the market share in 2026, supported by strong provincial infection control policies. Hospitals are increasingly focusing on eco-friendly and hydrogen peroxide-based disinfectants to meet sustainability goals and safety standards. Rising investments in healthcare infrastructure modernization and infection prevention programs are increasing product adoption. Public health agencies emphasize routine surface disinfection in hospitals, clinics, and long-term care facilities.

Europe Surface Disinfectant Market Trends

Europe is likely to be a significant market for surface disinfectants, due to strict regulatory frameworks, strong sustainability focus, and high adoption in healthcare and commercial sectors. The EU Biocidal Products Regulation (BPR) ensures strict compliance with safety and efficacy, encouraging innovation in eco-friendly formulations. For instance, BODE Chemie GmbH offers widely used hospital disinfectant solutions across Europe, supporting infection control protocols in clinical and surgical environments.

U.K. Surface Disinfectant Market Trends

The U.K. is likely to be a significant market for surface disinfectants, accounting for approximately 15% of the European market share in 2026, supported by NHS infection prevention and control programs aimed at reducing healthcare-associated infections. Hospitals and clinics are increasingly using ready-to-use disinfectant wipes and sprays for rapid and effective surface cleaning. Post-pandemic hygiene awareness has also increased adoption in public and residential settings. Government initiatives focusing on healthcare safety and hospital modernization are increasing disinfectant usage.

Germany Surface Disinfectant Market Trends

Germany is anticipated to dominate the regional market, accounting for around 37% of the Europe market share in 2026, due to a highly developed healthcare system and strong infection prevention standards in hospitals and laboratories. German healthcare facilities widely use alcohol-based and hydrogen peroxide disinfectants for surgical and ICU sanitation. Strong regulatory oversight ensures high product quality and compliance with hygiene standards. Increasing focus on sustainability is driving adoption of environmentally friendly disinfectant solutions.

Asia Pacific Surface Disinfectant Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rapid urbanization, expanding healthcare infrastructure, and rising awareness of hygiene practices. Increasing investments in hospitals, laboratories, and public health systems are driving strong demand for disinfectant products. A notable example includes GOJO Industries, which has expanded its hygiene solutions across Asia Pacific, providing alcohol-based disinfectants widely used in hospitals and public healthcare environments.

China Surface Disinfectant Market Trends

China is projected to dominate the regional market, holding around 35% of the regional market share in 2026, due to large-scale healthcare infrastructure development, government health reforms, and strict infection control standards. Hospitals are increasingly adopting advanced disinfectant systems, including automated and high-efficiency chemical formulations, to improve hygiene outcomes. Strong domestic manufacturing capabilities ensure affordable product availability and wide distribution.

India Surface Disinfectant Market Trends

India is expected to emerge as a significant market for surface disinfectants, accounting for approximately 17% share in 2026, due to expanding healthcare infrastructure, rising awareness of hygiene, and growth in the hospitality and residential sectors. Government initiatives such as the Swachh Bharat Mission and healthcare modernization programs are improving sanitation practices across urban and rural areas. Hospitals, diagnostic laboratories, and clinics are increasingly adopting chemical disinfectants for infection control.

Competitive Landscape

The global surface disinfectant market exhibits a moderately fragmented structure, driven by increasing demand for infection prevention, stringent hygiene regulations, and rising adoption across healthcare, commercial, and residential sectors. The market is characterized by the presence of both multinational corporations and regional manufacturers offering a wide range of chemical and bio-based disinfectant solutions.

With key leaders, including Ecolab, Procter & Gamble, 3M, GOJO Industries, and Diversey, competition is highly intense across product innovation, pricing strategies, and distribution networks. These companies focus on expanding their portfolios with fast-acting, broad-spectrum, and environmentally friendly formulations to meet evolving regulatory and consumer expectations.

Key Industry Developments:

- In April 2026, Roam Technologies launched a Defra-approved disinfectant (Virox) designed to strengthen biosecurity in livestock farming and enhance protection against major animal diseases, including avian influenza and foot-and-mouth disease.

- In October 2025, Metrex announced the launch of CaviCide™ HP, a ready-to-use hydrogen peroxide-based surface disinfectant designed for healthcare environments to improve infection prevention efficiency and safety.

Companies Covered in Surface Disinfectant Market

- PDI, Inc.

- GOJO Industries, Inc.

- W.M. Barr

- Spartan Chemical Company, Inc.

- W.W. Grainger, Inc.

- Kimberley-Clark Corporation (KCWW)

- BODE Chemie GmbH

- Evonik Industries AG

- BASF SE

- Ecolab

- Procter & Gamble

Frequently Asked Questions

The surface disinfectant market is projected to reach US$7.2 billion in 2026.

The surface disinfectant market is driven by rising healthcare-associated infections, strict hygiene regulations, and increasing demand for infection prevention across healthcare, commercial, and residential sectors.

The surface disinfectant market is expected to grow at a CAGR of 7.2% from 2026 to 2033.

Key opportunities include growth in bio-based eco-friendly disinfectants, expansion in emerging markets, and adoption of advanced ready-to-use and sustainable disinfection technologies.

PDI, Inc., GOJO Industries, Inc., W.M. Barr, Spartan Chemical Company, and Evonik Industries AG are the leading players.