- Automotive Components & Materials

- Automotive Interior Surface Lighting Market

Automotive Interior Surface Lighting Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Interior Surface Lighting Market by Product Type (Strip, Panel), Vehicle Type (Passenger Cars (Compact, Mid-size, Luxury, SUVs), LCVs, HCVs (Buses), Trucks, Others), Application (Dashboard, Roof Ceiling, Doors, Floor, Center Console, Others), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Automotive Interior Surface Lighting Market Size and Trend Analysis

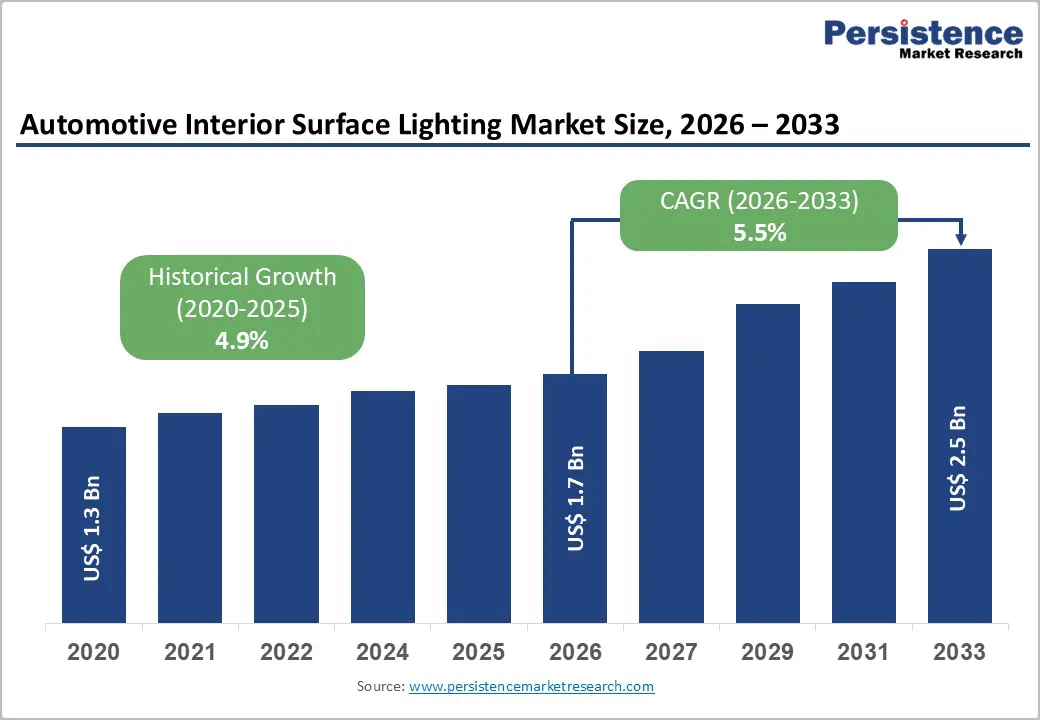

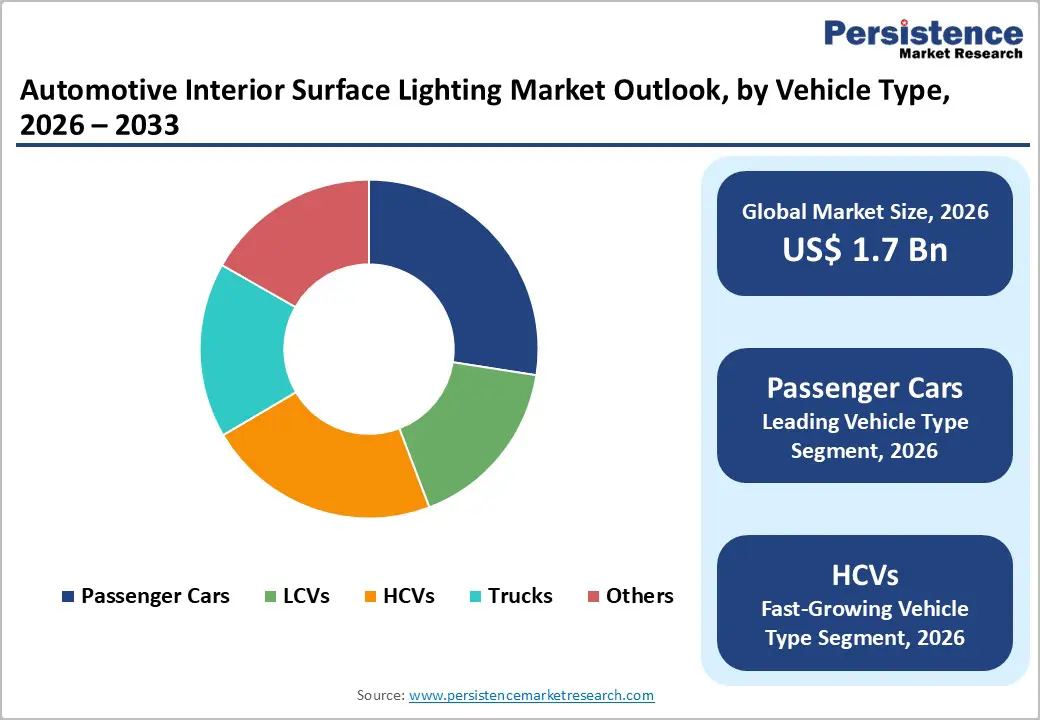

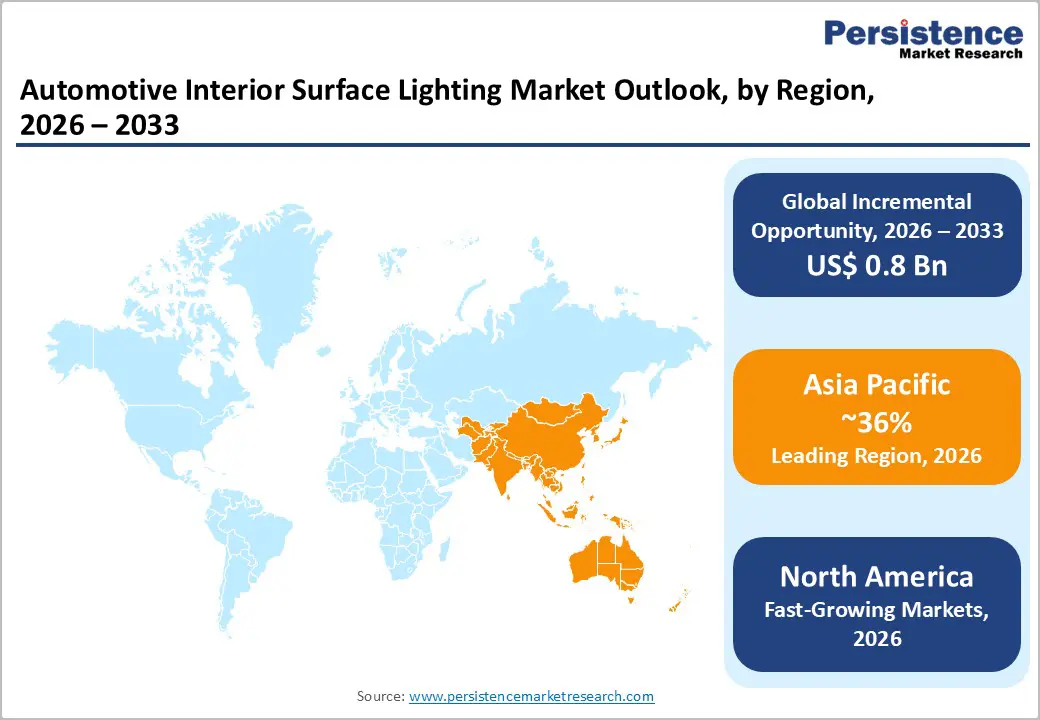

The global automotive interior surface lighting market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Rising demand for premium in-cabin experiences is accelerating adoption, as consumers increasingly value enhanced aesthetics, comfort, and personalization. The rapid growth of luxury vehicles and electric mobility is further driving the integration of advanced LED-based surface lighting for both ambient and functional applications. Moreover, regulatory emphasis on safety, visibility, and energy efficiency, along with continuous innovations in lighting technologies, is strengthening market expansion across vehicle categories worldwide.

Key Industry Highlights:

- Leading Region: Asia Pacific commands 36% share of the global market, driven by China’s vehicle production dominance and NEV adoption.

- Fastest-Growing Region: North America shows the fastest growth through connected car trends and smart cabin innovations.

- Leading Vehicle Category: Passenger cars dominate with 47.9% share, fueled by mass production and strong demand for aesthetic and ambient interior lighting, particularly in compact, mid-size, luxury, and SUV segments.

- Fastest-Growing Product Type: LED strips lead with 65% share and remain the fastest-growing product due to their flexibility, slim design, and energy efficiency in dashboards, doors, and other interior surfaces.

- Key Opportunity Segment: Electric and luxury vehicle interiors present prime growth opportunities, supported by policy incentives and rising adoption of premium, customizable cabin lighting solutions.

| Key Insights | Details |

|---|---|

| Automotive Interior Surface Lighting Size (2026E) | US$ 1.7 billion |

| Market Value Forecast (2033F) | US$ 2.5 billion |

| Projected Growth CAGR (2026-2033) | 5.5% |

| Historical Market Growth (2020-2025) | 4.9% |

Market Dynamics

Drivers - Growing Consumer Demand for Ambient, Personalized, and Premium Vehicle Interiors

Rising consumer preference for luxurious and visually appealing cabin environments is significantly boosting demand for automotive interior surface lighting solutions, including flexible LED strips and illuminated panels. With global passenger car production exceeding 80 million units annually (OICA), automakers increasingly adopt customizable lighting to enhance interior differentiation. Interior ambiance has become a key value driver, particularly in luxury segments where comfort and aesthetics influence purchase behavior.

Surface lighting also supports personalization trends, allowing drivers to select colors and themes. Energy-efficient LEDs reduce power consumption by up to 80% compared to halogen lighting, making them especially attractive for electric vehicles where battery efficiency is critical. This strengthens OEM adoption across mid- and high-end models.

Rapid Advancements in LED Innovation and Smart Interior Lighting Integration

Continuous improvements in LED technology and smart lighting controls are accelerating market growth by enabling dynamic, connected, and adaptive illumination systems. Innovations in RGB LEDs, programmable lighting modules, and app-synchronized controls enhance user experience through mood-based and responsive cabin lighting. Industry standards from SAE International, such as J1757, support reliable metrology for ambient lighting performance, ensuring quality integration.

Additionally, smart networking solutions like LIN-bus integrated LEDs reduce wiring complexity by nearly 50%, improving installation efficiency and lowering system costs. Such advancements make surface lighting easier to integrate into modern vehicle architectures. As premium models increasingly feature intelligent ambient lighting, adoption continues to expand rapidly across new vehicle platforms.

Restraints - High Upfront Investment Requirements and Complex Integration Challenges for OEMs

High initial costs associated with advanced automotive interior surface lighting systems remain a key restraint, especially in price-sensitive vehicle segments. Compared to conventional interior lighting, LED strips, flexible panels, and emerging OLED solutions require specialized materials and manufacturing processes, increasing component costs by nearly 20–30% according to supplier estimates. In addition, integrating these systems with vehicle electronics and infotainment platforms demands extensive validation and durability testing.

Such complexity raises R&D expenditures and extends development timelines, delaying product rollouts. These cost and engineering challenges limit adoption in mass-market vehicles, particularly in emerging economies where affordability and feature prioritization strongly influence purchasing decisions and OEM design strategies.

Strict and Regionally Diverse Regulatory Standards Limiting Market Scalability

Regulatory compliance requirements across different regions create significant barriers for manufacturers, complicating global standardization of interior surface lighting systems. For example, European regulations such as ECE R48 specify approved lighting intensities and color limitations, while U.S. NHTSA guidelines emphasize visibility and glare prevention. The lack of uniform global standards forces companies to redesign and customize lighting solutions for each market.

This regional variation increases development and certification costs by an estimated 15–25%, while lengthy approval cycles can delay commercialization of innovative technologies such as OLED-based panels. As a result, regulatory complexity continues to restrain rapid expansion and scalability.

Opportunity - Strong Growth Potential from Electric Vehicle Expansion and Premium Luxury Adoption

The rapid rise of electric vehicles and luxury mobility is creating major opportunities for automotive interior surface lighting suppliers. With global EV sales reaching nearly 14 million units in 2025 (IEA), automakers are increasingly focusing on premium cabin experiences through dynamic surface lighting panels and ambient illumination features. EV manufacturers emphasize comfort, personalization, and futuristic interiors to enhance brand appeal.

In parallel, sustainability policies such as the EU Green Deal encourage adoption of energy-efficient LED systems, supporting higher demand for advanced lighting solutions. Luxury brands like BMW and Mercedes are already integrating full-surface illumination concepts, opening strong growth pathways for suppliers targeting next-generation premium and new energy vehicle platforms.

Rising Aftermarket Customization Demand Supporting Wider Market Penetration

The growing popularity of vehicle personalization is expanding opportunities in the aftermarket for interior surface lighting retrofit solutions. With more than 250 million passenger cars over five years old across major markets, consumers increasingly seek plug-and-play lighting kits to modernize cabin aesthetics. Demand is particularly strong among younger buyers and automotive enthusiasts who value customizable RGB lighting synced with infotainment and mobile applications.

Advancements in modular, warranty-safe lighting systems are making aftermarket adoption easier and more reliable. This trend enables suppliers to reach beyond OEM channels and tap into a fast-growing customization ecosystem, supporting sustained market expansion through personalization-driven upgrades and lifestyle-oriented vehicle enhancements.

Category-wise Analysis

Product Type Insights

LED strips lead the automotive interior surface lighting market, capturing a 65% share in 2025 due to their flexibility in contouring dashboards, doors, and other interior surfaces. Their slim profile complements modern minimalist cabin designs, while energy efficiency and ease of installation make them a preferred choice. Industry data indicates 64.6% dominance in 2024, highlighting suitability for high-volume passenger car production globally. Strips provide uniform illumination without hotspots, enhancing both aesthetics and functionality.

Emerging segments like OLED panels and micro-LED modules are witnessing faster adoption, particularly in premium and electric vehicles. These solutions offer more design freedom and dynamic lighting effects, appealing to consumers seeking personalization and futuristic cabin experiences. Their integration into luxury models and smart interiors positions them as the fastest-growing category in innovation-driven markets.

Vehicle Type Insights

Passenger cars command the market with a 47.9% share in 2025, driven by large-scale production and strong consumer preference for visually appealing interiors. Segmentation into compact, mid-size, luxury, and SUVs shows that ambient lighting applications account for 78% of adoption. Studies by J.D. Power reveal that interior lighting improves satisfaction scores by 25% in passenger cars, while high annual production volumes exceeding 70 million units cement the category’s leadership.

Electric vehicles, luxury sedans, and SUVs are emerging as the fastest-growing segments. The emphasis on premium in-cabin experiences, interactive lighting, and personalized ambient themes drives adoption. Automakers increasingly integrate advanced lighting solutions to differentiate models, enhance comfort, and align with next-generation vehicle design trends, making these segments key growth areas.

Application Insights

Dashboard lighting holds a 35% share in 2025 as the leading application, combining functional visibility with aesthetic appeal. Integration with digital clusters enhances readability, while SAE metrology standards ensure uniform illumination. Premium models feature backlit surfaces, and compliance with NHTSA guidelines ensures glare-free operation. Functional adoption spans 80% of new vehicles, reflecting the critical role of dashboards in both style and safety.

Door trims, center consoles, and footwells are emerging as the fastest-growing applications. These areas allow ambient and decorative lighting to enhance passenger experience, support personalization, and complement digital interfaces. Increased adoption in luxury and electric vehicles highlights the trend toward full-cabin illumination, creating opportunities for advanced and flexible lighting solutions.

Sales Channel Insights

OEM channels dominate with an 89% share in 2025, as interior surface lighting is integrated during manufacturing for optimal design and durability. Rigorous validation ensures compliance with automaker specifications, and platform strategies support high-volume deployment, shipping 89.1% of units globally. OEM integration ensures seamless fit, quality consistency, and alignment with overall vehicle interior design aesthetics.

The aftermarket is the fastest-growing channel, driven by retrofit kits for personalization and aging vehicle fleets. Plug-and-play lighting strips and app-controlled modules allow consumers to upgrade interiors without OEM involvement. Enthusiast demand, modular designs, and compatibility with infotainment systems expand adoption, making the aftermarket an increasingly important avenue for suppliers to reach beyond factory-installed lighting.

Regional Insights

North America Automotive Interior Surface Lighting Market Trends

North America holds a significant share of the global automotive interior surface lighting market, with the U.S. leading due to a strong innovation ecosystem and high adoption of luxury and electric vehicles. Ambient LED strips are increasingly integrated into premium cabins, supported by NHTSA regulations ensuring safe, glare-free illumination. SAE standards further promote R&D and technology validation. In 2025, the region accounts for approximately 32% of the global market, reflecting its leadership in design-driven adoption.

The fastest growth within North America is driven by connected car trends and smart cabin innovations. Consumer demand for customizable, app-controlled lighting systems is rising across premium vehicles, while integration of dynamic, interactive lighting in EVs and high-end models accelerates adoption. Emerging smart lighting solutions for safety alerts and driver assistance features are also expanding the market footprint.

Europe Automotive Interior Surface Lighting Market Trends

Europe is experiencing steady growth in automotive interior surface lighting, driven by regulatory uniformity and strong luxury vehicle demand. Countries such as Germany and France benefit from harmonized ECE R48 standards, which mandate energy-efficient and safe lighting systems. Iconic models like the Mercedes E-Class feature integrated surface lighting panels, while UK and Spain follow with policies promoting electric vehicle adoption. The region is projected to grow at a CAGR of 5.9% between 2026 and 2033.

Premiumization and advanced cabin features are the fastest-growing trends across Europe. Automakers are increasingly integrating adaptive ambient lighting, OLED panels, and interactive LED systems to enhance passenger experience and differentiate models. Growth is particularly strong in luxury sedans and EV segments, where lighting contributes to brand value, personalization, and smart cabin development.

Asia Pacific Automotive Interior Surface Lighting Market Trends

Asia Pacific leads the global market with a 36% share in 2025, largely due to China’s dominance in vehicle production and NEV adoption. Chinese EVs feature full-cabin ambient and functional lighting systems, supporting both aesthetics and personalization. Japan leads in advanced lighting technology, while India’s automotive sector grows as affordability and mid-segment adoption increase. ASEAN countries leverage manufacturing advantages to accelerate production and integration of surface lighting across vehicle types.

The fastest-growing opportunities in Asia Pacific stem from electric and hybrid vehicle expansion, coupled with rising consumer interest in premium cabin features. Demand for customizable and interactive lighting is increasing in urban markets, and automakers are rapidly incorporating advanced LED and OLED panels in both domestic and export-oriented vehicles, driving widespread regional adoption.

Competitive Landscape

The automotive interior surface lighting market is moderately consolidated, with leading players leveraging strong OEM relationships to secure a position in new vehicle platforms. Key strategies focus on extensive R&D in smart LED technologies, energy-efficient solutions, and compatibility with electric and connected vehicles. Companies are expanding operations in high-growth regions to cater to rising demand for premium and personalized cabin lighting.

Market differentiation is achieved through customizable RGB lighting systems, dynamic ambient effects, and integration with digital interfaces. In parallel, aftermarket offerings are becoming increasingly fragmented, with retrofit kits and app-controlled modules creating new opportunities for smaller players and niche suppliers.

Key Developments:

- In April 2025, Valeo launched a smart interior lighting system equipped with integrated sensors for driver assistance and safety features. The system enables adaptive illumination based on driving conditions, enhancing both cabin aesthetics and functional visibility for premium and electric vehicles.

- In March 2023, Koito unveiled ultra-thin LED modules designed for automotive interiors, offering greater design flexibility and seamless integration into dashboards, doors, and trim panels. The modules provide uniform illumination with low power consumption, supporting both ambient and functional cabin lighting applications.

- In 2024, HELLA introduced adaptive mood lighting systems for vehicle interiors, allowing customizable RGB color schemes and dynamic lighting effects. The technology enhances passenger experience, integrates with infotainment and driving modes, and is targeted primarily at luxury and electric vehicle segments.

Companies Covered in Automotive Interior Surface Lighting Market

- Yanfeng Automotive Interiors

- Valeo SA

- HELLA KGaA Hueck & Co

- Everlight Electronics Co

- OSRAM Licht AG,

- LSI Industries Inc

- Efi lighting

- Toshiba Corporation

- Innotec Group

- DRÄXLMAIER Group

- Oshino Lamps Limited,

- Grupo Antolin

- ZKW Group GmbH

- DOMINANT Opto Technologies

- OptoElectronix, Inc.