- Semiconductor Materials & Components

- Storage Adapter Market

Storage Adapter Market Size, Share, and Growth Forecast 2026 - 2033

Storage Adapter Market by Product Type (iSCSI, RAID, Fibre Channel (FC), Fibre Channel over Ethernet (FCoE), SAS/SATA, Others), Application (Servers, Storage Area Networks (SAN), Network Attached Storage (NAS), Workstations, Portable Storage, Industrial Equipment, Data Center Infrastructure, Others), Data Transfer Speed (Up to 6 Gbps, 6–12 Gbps, 12–32 Gbps, 32–100+ Gbps), End-user (Individual, Commercial, Industrial, Government), by Regional Analysis, 2026 - 2033

Storage Adapter Market Size and Trend Analysis

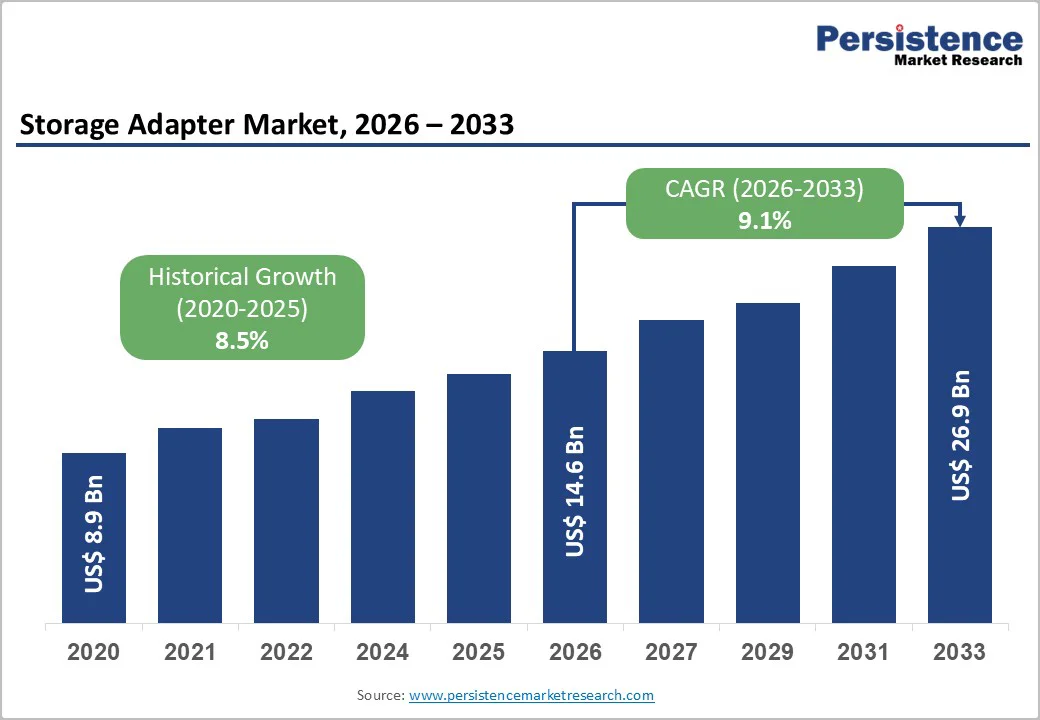

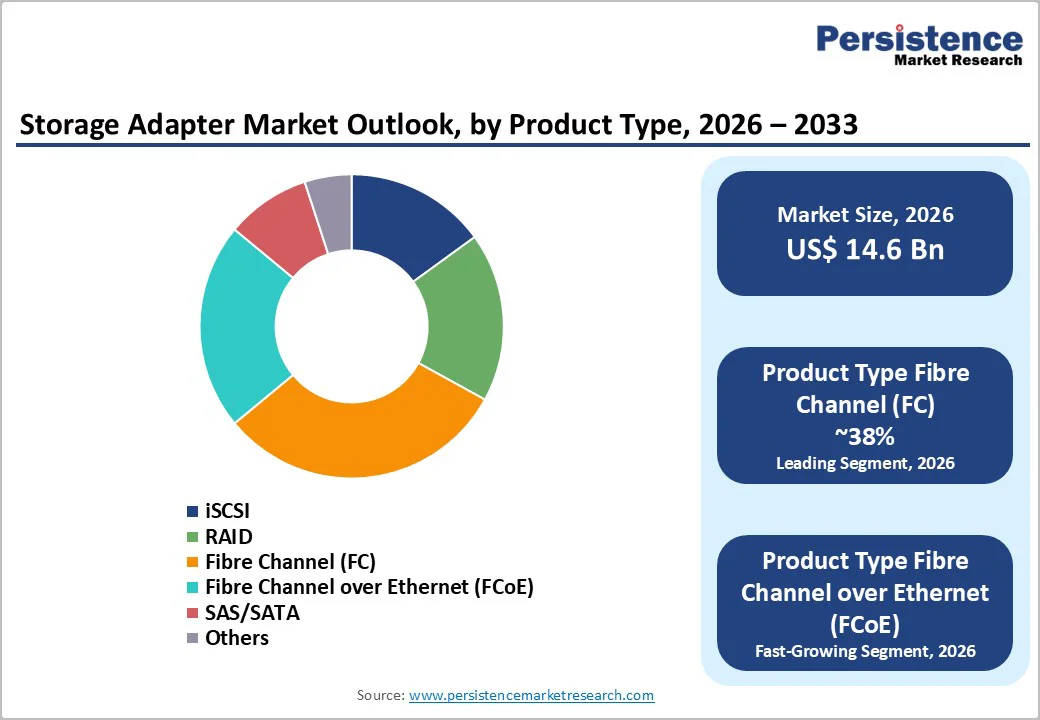

The global storage adapter market size is projected to reach US$ 14.6 billion in 2026 and rise to US$ 26.9 billion by 2033, reflecting a steady CAGR of 9.1% between 2026 and 2033.

The market growth is primarily fueled by the explosive rise in data generation across enterprise, cloud, and hyperscale environments. As organizations accelerate their shift toward cloud-native infrastructure, AI-driven workloads, and high-performance computing, the need for high-bandwidth, low-latency connectivity between servers and storage systems has intensified. The rapid adoption of NVMe and flash-based storage further amplifies demand for advanced HBAs and RAID controllers. Widespread upgrades to support 5G networks and edge computing continue to reinforce the strong outlook for storage interconnect solutions.

Key Market highlights

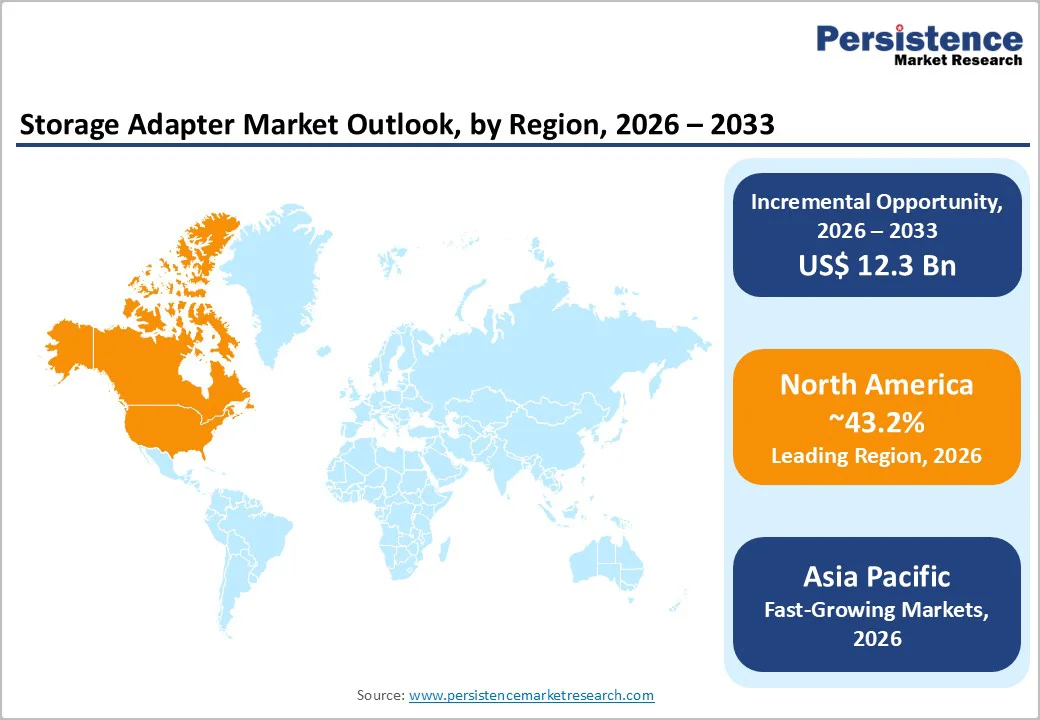

- Leading Region: North America leads the storage adapter market with a 43.2% share, driven by hyperscale cloud providers, legacy data center modernization, and early adoption of advanced storage protocols.

- Fastest-Growing Region: Asia Pacific is expanding rapidly, accounting for 39.2% of the market, fueled by 5G rollout, digital transformation in China and India, and significant investments in edge and cloud data centers.

- Dominant Segment: Fibre Channel (FC) remains the leading product type, holding approximately 38% market share, favored for its reliability and deterministic performance in mission-critical enterprise SAN environments.

- Fastest-Growing Segment: Adapters supporting 32–100+ Gbps speeds are experiencing the highest growth, as modern data centers upgrade to handle AI workloads, NVMe flash storage, and high-bandwidth applications.

- Key Market Opportunity: Edge computing infrastructure presents a substantial growth avenue, requiring ruggedized, compact, and energy-efficient adapters for remote deployments in industrial, telecom, and IoT environments.

| Key Insights | Details |

|---|---|

|

Storage Adapter Market Size (2026E) |

US$ 14.6 Billion |

|

Market Value Forecast (2033F) |

US$ 26.9 Billion |

|

Projected Growth CAGR (2026-2033) |

9.1% |

|

Historical Market Growth (2020-2025) |

8.5% |

Market Dynamics

Drivers - Exponential Expansion of Hyperscale Data Centers and Cloud Infrastructure Deployment

The accelerating global buildout of hyperscale data centers is a key catalyst for the storage adapter market. Cloud leaders such as AWS, Microsoft Azure, and Google Cloud continue scaling their server and storage capacities to support unprecedented data volumes in the Zettabyte era. These environments depend on high-performance storage adapters to ensure ultra-low-latency, high-reliability connections across SAN, NAS, and distributed storage systems. As data-intensive applications expand, the need for resilient, high-bandwidth physical interconnects becomes increasingly essential.

Furthermore, the shift toward software-defined data center storage (SDS) and hyperconverged infrastructure (HCI) magnifies this demand. These modern architectures decouple storage from traditional hardware, instead relying heavily on SAS, NVMe-oF, and Fibre Channel adapters to sustain seamless throughput and scalability. Supporting this trend, IDC highlights that global spending on cloud-centric compute and storage infrastructure continues to outpace traditional on-premise investments, directly elevating the adoption of advanced storage adapter technologies.

Rapid Adoption of NVMe, Flash Storage, and High-Performance Data Architectures

The ongoing transition from hard disk drives to solid-state and NVMe-based storage is significantly propelling market growth. Flash-driven ecosystems require data paths capable of sustaining extremely high I/O operations, making traditional interfaces obsolete and pushing enterprises to upgrade to next-generation storage adapters. These advanced adapters, tailored for speeds beyond 32 Gbps and 64 Gbps, are significant for real-time analytics, AI training, high-frequency trading, and other latency-sensitive workloads.

Emerging technologies such as PCIe Gen 5.0 and Gen 6.0 are being integrated into new HBA and RAID adapter designs, aligning storage performance with cutting-edge CPUs and accelerators. This industry-wide technology refresh is accelerating replacement cycles across commercial and industrial sectors. As more organizations migrate to high-performance flash architectures, demand continues to intensify for robust, scalable storage adapters that optimize throughput and minimize latency.

Restraints - Rising Cybersecurity Risks in High-Speed Storage Connectivity Environments

The rapid adoption of high-bandwidth storage adapters such as NVMe-over-Fabrics (NVMe-oF), FCoE, and advanced iSCSI ecosystems introduces elevated cybersecurity risks. As data traffic scales across hybrid and multi-cloud infrastructures, adapters become key points of vulnerability. Attackers can exploit weak authentication, unsecured ports, or misconfigured zoning to intercept or corrupt data. Enterprises handling sensitive workloads, such as financial services, healthcare, and government, face increased compliance and data protection challenges, which raises the cost and complexity of implementing secure storage networking.

Encryption, traffic monitoring, and zero-trust frameworks significantly increase hardware overhead and operational load. Smaller enterprises often delay upgrades because integrating robust security stacks into high-speed adapters requires additional appliances, licenses, and trained personnel. The fear of potential data breaches or lateral network attacks slows down modernization and contributes to hesitancy in adopting next-generation storage connectivity solutions.

Skills Gap and Operational Complexity Limiting Deployment Efficiency

Modern storage adapters demand deep expertise in protocol tuning, fabric management, virtualization integration, and performance optimization. However, the global IT workforce faces a notable skills shortage in high-performance storage networking, especially across Fibre Channel, RDMA-based protocols, and next-generation Ethernet technologies. Organizations lacking specialized talent struggle to configure multi-protocol environments, perform firmware updates, or ensure interoperability among adapters, switches, and hyperconverged systems, resulting in increased downtime and operational inefficiencies.

This skills gap forces enterprises to rely heavily on OEM-managed services or third-party integrators, driving up deployment and maintenance costs. SMEs and industrial end-users, in particular, often postpone upgrades due to the technical complexity and the fear of misconfiguring critical infrastructure. This operational burden slows adoption and is a substantial restraint on broader market expansion.

Opportunities - Growing Edge Infrastructure and IoT Deployment Creating New Connectivity Demand

The rapid expansion of edge computing ecosystems is opening a major growth avenue for storage adapter vendors. With IoT devices, autonomous systems, remote industrial equipment, and smart infrastructure generating massive real-time data, edge nodes require compact, rugged, and power-efficient storage interfaces. Unlike traditional data centers, these environments operate under constrained thermal and power budgets, creating strong demand for adapters that deliver high throughput in small form factors. Manufacturers that design purpose-built adapters for edge servers, micro data centers, and industrial gateways stand to benefit significantly.

The ongoing global rollout of 5G enhances data traffic at the edge, driving the need for reliable SAS/SATA, NVMe, and Ethernet-based connectivity for immediate data ingestion and local processing. This shift enables adapter vendors to diversify into telecom, industrial automation, and mission-critical IoT infrastructure segments, creating long-term adoption momentum beyond core enterprise deployments.

Acceleration of AI, ML, and Generative AI Workloads Driving High-Performance Adapter Innovation

The enterprise transition toward large-scale AI, ML, and generative AI workloads is creating strong demand for next-generation storage adapters capable of sustaining extremely high throughput and low latency. These workloads rely heavily on rapid data movement between GPUs, storage arrays, and compute clusters. This creates opportunities for “intelligent” adapters featuring onboard offload engines for compression, encryption, erasure coding, and data-path acceleration, reducing CPU burden and improving overall system performance. Developers who integrate smart firmware and computational storage capabilities will capture a meaningful competitive advantage.

AI-driven data centers increasingly deploy high-speed interconnects such as InfiniBand, RDMA-over-Ethernet, and GPU-direct storage solutions. Vendors specializing in ultra-high-bandwidth adapters for parallel file systems and AI training pipelines can tap into premium, fast-growing segments as hyperscalers and enterprises build out next-generation AI infrastructure.

Category-wise Analysis

Product Type Insights

The Fibre Channel (FC) segment leads the product type category with around 38% market share, upheld by its mission-critical role in enterprise SAN environments. Industries such as banking, financial services, healthcare, and government continue to rely on FC for deterministic, lossless, and ultra-reliable data transport. Continuous upgrades to 32G and 64G FC technologies and the enormous installed base requiring ongoing refresh cycles further cement its dominance. Its strong heritage and proven interoperability across global data centers keep Fibre Channel firmly positioned as the preferred backbone for all-flash storage arrays and high-availability architectures.

The fastest-growing product type is FCoE (Fibre Channel over Ethernet), which combines Fibre Channel reliability with Ethernet flexibility. FCoE adoption is accelerating in modern data centers and virtualized environments, enabling enterprises to consolidate storage and network infrastructure, reduce cabling, and lower operational costs while supporting high-speed Ethernet connectivity.

Application Insights

The data center infrastructure segment leads the application category with an estimated 42% market share, propelled by hyperscale expansion, colocation facility growth, and increasing workload consolidation. Storage I/O efficiency is central to these environments, creating consistent demand for high-density HBAs, RAID cards, and advanced connectivity solutions. With most data center traffic now internal (storage–server), robust adapter infrastructure remains foundational for ensuring predictable performance, high availability, and support for large-scale virtualized environments.

On the growth front, cloud and virtualized workloads are the fastest-growing application segment. The rise of disaggregated and software-defined storage, alongside rapid adoption of SaaS, PaaS, and AI cloud services, is accelerating the procurement of high-bandwidth adapters. These environments increasingly rely on NVMe-oF, RDMA, and 100GbE/200GbE connectivity, driving higher-than-average growth rates within cloud-optimized storage networking solutions.

Data Transfer Speed Insights

The 32–100+ Gbps speed segment leads the market with roughly 35% share, fueled by the need to support bandwidth-intensive workloads such as high-resolution video processing, genomic sequencing, real-time analytics, and large-scale virtualization. As 12 Gbps and 16 Gbps standards increasingly act as bottlenecks for modern NVMe SSD arrays, enterprises are rapidly transitioning to faster interfaces. Investments in 100GbE/200GbE NICs and 64G FC HBAs also reinforce this segment’s leadership as data centers prioritize higher throughput and reduced latency.

The fastest-growing speed segment is the ultra-high-performance tier powered by PCIe Gen 5 and Gen 6 technologies, which enable unprecedented data transfer capabilities for next-generation applications. This segment is expanding rapidly due to AI training clusters, GPU-accelerated computing, and emerging HPC workloads, all of which demand parallel data movement at extreme speeds, driving adoption of cutting-edge adapters.

End-user Insights

The commercial segment dominates the end-user landscape with about 60% market share, anchored by enterprises, IT & telecom providers, and global cloud operators. Digital transformation initiatives, large-scale data center expansions, and rising adoption of virtualization and high-performance storage architectures sustain strong demand. Commercial users rely heavily on discrete adapters for redundancy, hardware RAID, and high-availability storage configurations, making them the primary consumers of premium SAN/NAS connectivity hardware.

The fastest-growing segment is cloud-native enterprises and digital service providers, driven by escalating deployment of AI-driven platforms, multi-cloud architectures, and edge-integrated cloud infrastructure. These organizations require high-speed NVMe-oF, RDMA, and Ethernet-based adapters to support distributed workloads, containerized environments, and emerging data-intensive applications, resulting in rapid year-over-year growth within this end-user category.

Regional Insights

North America Storage Adapter Market Trends

North America leads the global storage adapter market with a 43.2% share, primarily driven by substantial investments from hyperscale cloud providers and enterprise IT modernization initiatives. The U.S. hosts a mature digital ecosystem with early adoption of advanced storage protocols like NVMe-oF and 400GbE. Key growth factors include legacy data center upgrades to support AI, analytics, and high-performance computing workloads, as well as stringent data retention requirements in healthcare, banking, and finance. The presence of major technology players such as Intel, Broadcom, and NVIDIA (Mellanox) accelerates innovation and reduces time-to-market for next-generation storage adapters.

The region continues to benefit from strong capital expenditure on information processing equipment, reinforcing demand for enterprise-grade storage connectivity. Increasing adoption of high-bandwidth adapters for SAN, NAS, and cloud deployments ensures North America retains its market dominance, with sustained procurement for AI-driven workloads, edge computing, and hybrid cloud infrastructure fueling long-term growth.

Europe Storage Adapter Market Trends

Europe is witnessing steady growth with a CAGR of 9.9%, shaped by regulatory compliance (GDPR), data sovereignty mandates, and a strong emphasis on energy-efficient green data centers. Germany and the U.K. serve as industrial and manufacturing hubs, where ruggedized storage adapters are integrated into automation systems. Regional initiatives like “Digital Europe” and sovereign cloud projects, including GAIA-X, are stimulating the construction of local data centers, driving demand for reliable and high-performance storage connectivity solutions.

High-performance computing (HPC) collaborations, led by organizations such as CERN, further drive Europe’s need for low-latency, high-bandwidth interconnects. The growing adoption of NVMe-oF and energy-efficient adapters in hyperscale and enterprise data centers reflects Europe’s balanced focus on performance, compliance, and sustainability, supporting a consistent growth trajectory for the storage adapter market.

Asia Pacific Storage Adapter Market Trends

Asia Pacific is the fastest-growing market, accounting for 39.2% share, fueled by rapid digitalization across China, India, and Southeast Asia. Massive investments in 5G networks are driving edge data center deployments, creating demand for high-density storage connectivity solutions. Initiatives like China’s “Eastern Data, Western Computing” program are accelerating the adoption of both domestic and international storage technologies. Manufacturing hubs in Taiwan and South Korea support a resilient supply chain for adapter components, while the expansion of e-commerce, gaming, and cloud services is generating unprecedented data volumes that require high-performance HBAs and RAID controllers.

SMEs in the ASEAN region are increasingly adopting cost-efficient SAS and SATA adapters, while large cloud providers continuously upgrade storage fabrics for enhanced throughput and low-latency operations. This combination of government initiatives, private investments, and booming digital services is propelling Asia Pacific’s storage adapter market at a rapid pace.

Competitive Landscape

The storage adapter market is highly consolidated, with a few key players dominating high-performance segments such as Fibre Channel and enterprise RAID. High entry barriers exist due to the complex engineering required for high-speed signal integrity, rigorous driver certification across major operating systems, and the need to meet enterprise-grade reliability and security standards. Market leaders focus on vertical integration, often producing their own controller silicon to optimize cost, performance, and product quality.

Differentiation in this market is achieved through advanced firmware capabilities, including enhanced error recovery, diagnostics, and encryption. Strategic collaborations with server OEMs enable pre-validated, plug-and-play adapters, ensuring seamless deployment for enterprise customers and strengthening competitive positioning.

Key Market Developments

- In October 2024, Broadcom announced the general availability of its Gen 7 Fibre Channel HBAs, specifically designed to support autonomous SAN operations and maximize the performance of all-flash data centers.

- In August 2024, Hewlett Packard Enterprise (HPE) expanded its collaboration with Intel to integrate the latest silicon photonics-based storage adapters into their ProLiant server line, aiming to reduce latency in AI model training clusters.

- In March 2023, Microchip Technology released its new series of 24G SAS/PCIe Gen 4 Tri-Mode storage controllers, enabling data centers to mix and match NVMe, SAS, and SATA drives within the same server infrastructure for maximum flexibility.

Companies Covered in Storage Adapter Market

- Broadcom (LSI)

- Intel

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- Microchip (Adaptec)

- Fujitsu

- Lenovo

- ATTO Technology

- Supermicro

- IBM

- Huawei

- Marvell

- Toshiba

- Hitachi Vantara

- Advantech

- Promise Technology

- Areca Technology

Frequently Asked Questions

The global storage adapter market is forecast to reach a valuation of US$ 26.9 Billion by 2033, expanding from US$ 14.6 Billion in 2026.

Key drivers include the rapid expansion of hyperscale data centers, the rising adoption of NVMe and flash storage arrays, and increasing infrastructure requirements for AI workloads, 5G networks, and edge computing deployments.

The Fibre Channel (FC) segment holds the largest share at approximately 38%, maintaining dominance due to its reliability in mission-critical enterprise SAN networks.

Asia Pacific, accounting for 39.2% of the market, is anticipated to be the fastest-growing region, driven by digitalization, 5G expansion, and large-scale data center investments in China, India, and Southeast Asia.

The growth of Edge Computing infrastructure offers significant opportunities, requiring specialized, ruggedized, and energy-efficient storage adapters for decentralized and remote processing environments.

Major players include Broadcom, Intel, Dell Technologies, HPE, Cisco Systems, Microchip, Marvell, and IBM.