- Hardware & Software IT Services

- Tape Storage Market

Tape Storage Market Size, Share, and Growth Forecast, 2026 - 2033

Tape Storage Market by Technology (LTO-1 to LTO-5, LTO-6, LTO-7, LTO-8, DDS-1, DDS-2, DDS-3, DDS-4, DLT IV and SDLT), by Storage Capacity (Up to 1TB, 1TB to 5TB, 5TB to 10TB,10TB to 50TB and Above 50TB), Application (IT and Telecommunication, Banking, Financial Services and Insurance, Media and Entertainment, Research and Academia, Healthcare, Oil and Gas, Government and Defense and Others), End-user (Cloud Providers, Data Centers, Enterprises and Others) and Regional Analysis for 2026 - 2033

Tape Storage Market Size and Trends Analysis

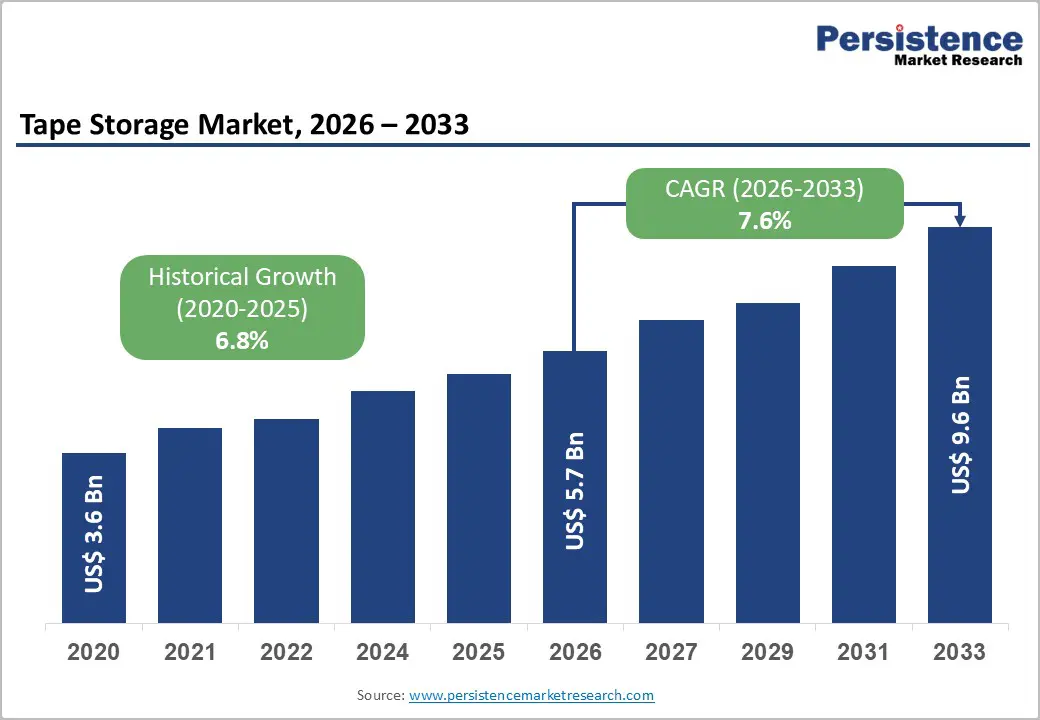

The global tape storage market size is likely to be valued at US$ 5.7 billion in 2026 and is projected to reach US$ 9.6 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. The market is driven by exponential global data generation exceeding 100+ zettabytes annually, stringent cybersecurity requirements establishing air-gapped offline backup needs, and superior total-cost-of-ownership advantages compared to alternative storage technologies.

Key Industry Highlights:

- Leading Technology: LTO-8 dominates with 18.5% market share through established infrastructure compatibility and mature production, while DDS-4 represents the fastest-growing segment at 9% CAGR, capturing cost-sensitive mid-market and emerging market segments through affordability positioning.

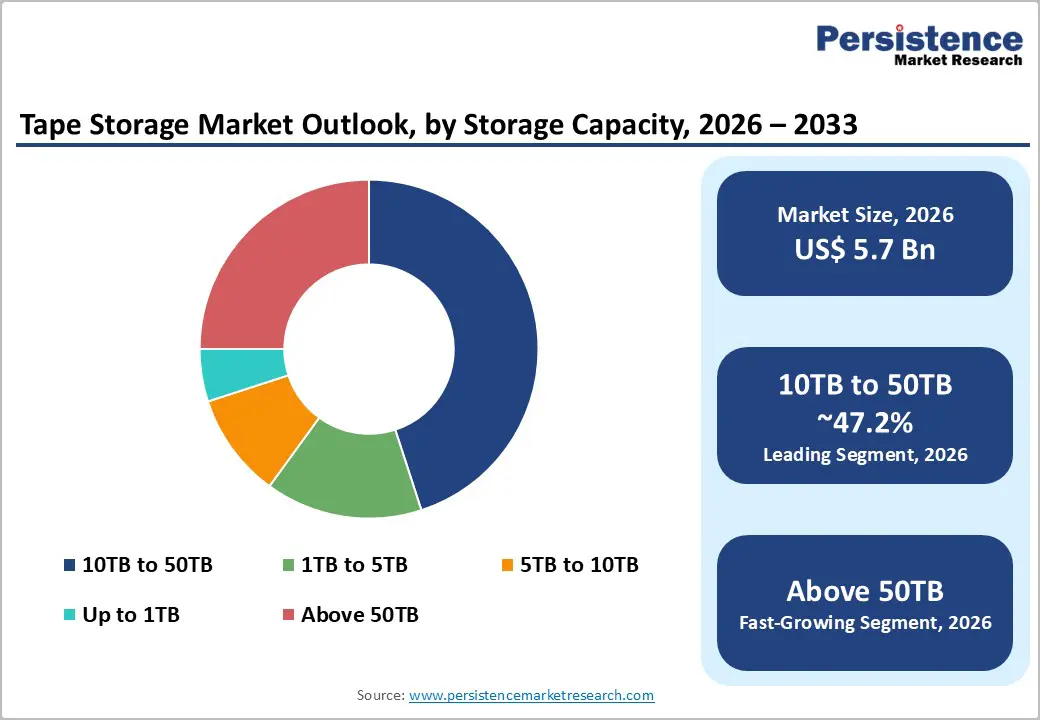

- Dominant Capacity Range: 10TB to 50TB capacity cartridges command 47.2% market share, reflecting LTO-8/LTO-9 technology alignment, while the above-50 TB segment represents the fastest-growing at 16% CAGR, driven by IBM TS1170 50TB cartridges and hyperscaler petabyte-scale archival requirements.

- Primary Application Sector: Data centers establish 36.5% market share as hyperscaler infrastructure mainstays; Enterprises represent the fastest-growing segment at 11% CAGR, driven by ransomware resilience and compliance-driven offline backup adoption accelerating.

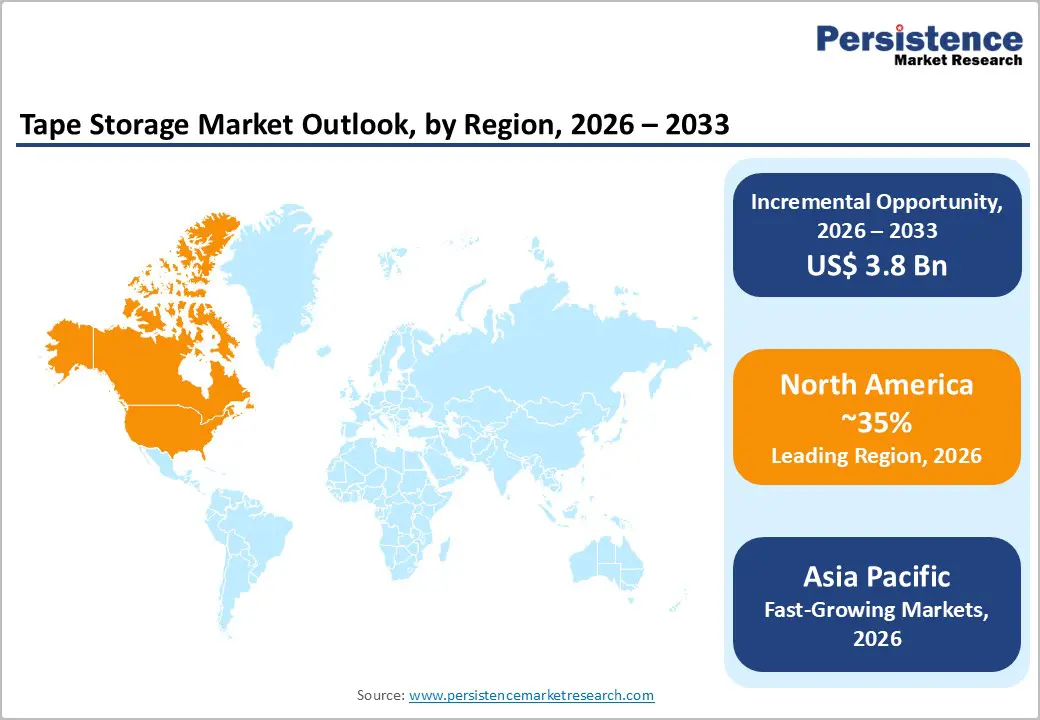

- Regional Market Leadership: North America maintains 35% global market share driven by financial services and regulatory compliance emphasis; Europe commands 26% share with GDPR stringency, Asia Pacific demonstrates fastest regional growth at 13% CAGR, expanding from 22% current share to 28% by 2033.

- Ransomware Resilience Driver: Air-gapped tape backup adoption accelerating 30% annually as enterprises implement 3-2-1 backup strategies; cyber insurance providers offering 15% premium reductions for verified tape-based offline backup systems.

- Market Consolidation: Top 5 suppliers control 70% global market share, with IBM, Quantum (post-Spectra acquisition), HPE, Fujifilm, and Sony maintaining technology and relationship dominance; LTO ecosystem strengthening through LTO-10 standardization and open-platform emphasis versus proprietary IBM format.

| Key Insights | Details |

|---|---|

|

Tape Storage Market Size (2026E) |

US$ 5.7 Bn |

|

Market Value Forecast (2033F) |

US$ 9.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.6% |

|

Historical Market Growth (CAGR 2020 to 2024) |

6.8% |

Market Dynamics

Drivers - Ransomware Proliferation and Air-Gapped Offline Backup Adoption

Ransomware attack frequency has escalated exponentially, with reported incidents increasing 48% year-over-year, resulting in estimated US$ 34+ billion cumulative organizational damages through 2025. Tape storage, offering inherent air-gapped capabilities preventing network-based malware propagation and ransomware encryption, establishes critical cybersecurity infrastructure component. Traditional disk-based and cloud storage systems remain vulnerable to lateral network movement, enabling rapid encryption across multiple storage platforms, whereas tape systems, physically isolated from networks, provide bulletproof ransomware immunity.

Enterprise IT leadership, increasingly mandating 3-2-1 backup strategies (3 copies, 2 different media, 1 offsite location), systematically incorporates tape storage as an essential compliance element. Cyber insurance providers offer 10% premium reductions for organizations implementing verified air-gapped tape backup systems, establishing direct financial incentives to adopt. Managed service providers and business continuity specialists report 30% year-over-year increases in customer requests for tape-based disaster recovery implementations.

Superior Total-Cost-of-Ownership and Energy Efficiency Advantages

Tape storage delivers significantly lower cost-per-terabyte compared to alternative technologies, with per-unit costs ranging from US$ 8-15/TB compared to disk systems at US$ 25-40/TB and cloud storage at US$ 50-100+/TB. Energy consumption advantages are substantial, with tape systems requiring minimal operational power during storage phases versus continuously powered disk arrays, reducing electricity costs by 85% for cold data tiers. Enterprise operating expense reduction, with tape-based archiving, reducing infrastructure power consumption by 40-60% compared to traditional SAN-based systems, directly improves profitability metrics and sustainability initiatives.

Hyperscaler data centers, managing exabyte-scale datasets, report 30% reduction in total data storage costs when implementing tiered storage architectures incorporating tape as ultimate cold-tier storage. Environmental sustainability alignment, with tape technology consuming a fraction of the power requirements of disk-based alternatives, supports organizational carbon neutrality commitments.

Restraints - Cloud Storage Competition and Perception of Technology Obsolescence

Cloud storage adoption, with market expansion exceeding 30% annually, positions cloud providers as primary competitors to tape storage infrastructure. Consumer and mid-market perception of tape as legacy technology, despite technological advancement, creates adoption barriers, particularly among smaller organizations and emerging technology sectors. Cloud storage marketing emphasizing convenience, scalability, and reduced capital expenditure appeals to CFO-driven purchasing decisions emphasizing operational expense reduction. Technology transition delays, with organizations migrating from tape to cloud-based solutions, creating multi-year technology refresh cycles, constrain market replacement demand.

Competitive pricing pressure from cloud providers, including AWS Glacier ($4/TB annually), creates economic headwinds against traditional tape pricing models. Integration complexity with modern cloud-native architectures, requiring specialized software bridges and API implementations, establishes adoption barriers for organizations standardized on cloud infrastructure.

High Equipment Acquisition Costs and Supply Chain Dependencies

Tape storage library systems, including drives and cartridges, require substantial capital investment ranging from US$ 100,000-2,000,000+ per installation, depending on capacity and automation levels. Equipment obsolescence risk, with technology generations transitioning every 3-5 years, creates capital depreciation pressures and forced upgrade cycles requiring sustained investment commitments. Supply chain concentration, with IBM dominating LTO drive manufacturing (80%+ market share) and Sony/Fujifilm controlling cartridge production, establishes vendor lock-in risks.

Specialized skills requirements for tape storage management, including tape librarians and storage administrators, create workforce scarcity and training burden. Backward compatibility limitations between tape generations, with LTO-8 drives unable to read LTO-6 cartridges, establish technology debt preventing indefinite hardware amortization. Lead time constraints for tape library procurement, extending 12-18 months for complex installations, prevent rapid capacity scaling and create procurement rigidity.

Opportunity - Tape-Cloud Hybrid Architectures and Data Lifecycle Management Optimization

Hybrid storage architectures combining tape with cloud services for tiered data management represents distinct market opportunity addressing both cost-efficiency and operational flexibility requirements. Data lifecycle management platforms, automating data movement across hot (cloud), warm (disk), and cold (tape) storage tiers based on access patterns, are emerging market segment valued at US$ 2-3 billion with 15-% CAGR. Backup-as-a-service (BaaS) providers increasingly incorporate tape as backend storage infrastructure supporting cost-effective long-term retention, creating an incremental market opportunity.

Market projections indicate tape-cloud hybrid deployments will represent 35% of total enterprise backup installations by 2033, translating to US$ 1.5-2.5 billion incremental market opportunity. Managed service providers offering tape-integrated disaster recovery and business continuity services represent an emerging business model enabling market expansion beyond traditional equipment vendors.

High-Capacity Cartridge Technology Advancement and Above-50TB Segment Growth

Next-generation LTO-9 and LTO-10 technologies, delivering 18TB and 36TB native capacities respectively, establish expanded storage density enabling data center consolidation and cost reduction. Above-50TB segment, currently representing 8-% of market but expanding 25-30% annually, reflects an emerging opportunity in hyperscaler deployments requiring petabyte-scale archival capabilities. IBM's proprietary JF format tapes delivering 50TB native capacity represent technology leadership, establishing premium positioning and margin expansion opportunities.

Market projections indicate above-50TB cartridge segment will reach US$ 1.2-1.8 billion valuation by 2033, representing 22-25% CAGR, substantially exceeding overall market growth. Fujifilm laboratory demonstrations of 580TB raw capacity tapes establish a long-term technology runway supporting sustained market growth and competitiveness versus alternative storage technologies.

Category-wise analysis

Technology Type Insights

LTO-8 holds 18.5% market share due to its balanced combination of higher capacity and mature adoption. Offering 12TB native and 30TB compressed storage, it delivers double the capacity of LTO-7 while remaining backward compatible with existing systems. Strong OEM support from IBM, Quantum, and HPE, and annual production exceeding 50 million cartridges ensure supply stability and competitive pricing. Proven reliability and standardized manufacturing sustain its relevance as transitions to LTO-9 progress gradually over the next 5–7 years.

DDS-4 is the fastest-growing segment, expanding at 9% CAGR through 2033. Its lower-cost architecture appeals to mid-sized enterprises and emerging markets. Specialized uses such as seismic archiving and legacy systems, combined with cartridge costs 30% below LTO, support continued adoption, particularly in cost-sensitive Asia Pacific regions.

Storage Capacity Analysis

Cartridges with 10TB to 50TB capacity account for 47.2% market share, driven by alignment with widely deployed LTO-8 and LTO-9 technologies offering an optimal balance between storage density and operational efficiency. This range supports cost-per-terabyte optimization while maintaining ease of handling and compatibility with existing automated tape libraries. Standardization across enterprise data centers and tiered storage architectures reinforces dominance, as procurement practices favor proven infrastructure with minimal integration complexity.

Above-50TB cartridges represent the fastest-growing segment, expanding at 15% CAGR through 2033. Demand is fueled by hyperscale data centers with massive archival needs and technology leadership such as IBM TS1170 50TB cartridges. Upcoming LTO-10 commercialization (36TB native/90TB compressed) will further accelerate adoption, positioning ultra-high-capacity cartridges as the next growth engine in tape storage.

End-use Insights

Data center facilities account for 36.5% market share due to their essential role in supporting the global digital economy. Hyperscale operators such as Amazon, Google, Microsoft, and Alibaba integrate tape storage into multi-tier archival architectures to optimize cost per terabyte for cold data. Standardized procurement practices, disaster recovery requirements, and geographically distributed backup strategies sustain steady demand. Tape-based infrastructure also underpins cloud archival services including AWS Glacier, Google Coldline, and Azure Archive.

Enterprise deployments represent the fastest-growing end-use segment, expanding at 11% CAGR through 2033. Rising ransomware threats and adoption of 3-2-1 backup strategies with offline storage drive procurement. Increasing regulatory retention mandates and heightened business continuity planning further accelerate adoption. Cost-effective tape solutions are also enabling broader uptake among mid-sized enterprises, expanding the overall addressable market.

Regional market insights

North America Tape Storage Market Analysis

North America commands approximately 35% of global tape storage market share, valued at approximately US$ 2.2 billion in 2026 with projections approaching US$ 3.3 billion by 2033. The United States represents the dominant regional market contributor, accounting for 80% of North American market value, driven by hyperscaler data center concentration, financial services sector dominance, and regulatory compliance intensity.

Financial services sector adoption, with banking, insurance, and investment firms managing massive transaction and customer data archives, represents the primary market driver establishing sustained high-volume tape procurement. Government agencies and defense contractors, maintaining classified document archives and operational records, allocate substantial tape storage budgets. Third, cybersecurity incident response emphasis, with enterprise organizations increasingly implementing tape-based offline backup as a ransomware remediation strategy, drives procurement acceleration.

Europe Tape Storage Market Analysis

Europe represents approximately 25% of the global tape storage market share, valued at approximately US$ 1.5 billion in 2026. Germany, the United Kingdom, France, and Spain collectively represent 78% of the European market value, reflecting data privacy legislation stringency and regulatory compliance emphasis.

European market includes established suppliers maintaining regional headquarters and support operations, including IBM and Quantum, complemented by regional specialists and system integrators. GDPR Article 17 (Right to Be Forgotten) requirements, combined with data residency regulations, establish strict data management protocols influencing tape archival strategies.

Asia Pacific Tape Storage Market Trends

Asia Pacific region demonstrates robust growth dynamics, commanding approximately 22% market share with projections increasing to 28% by 2033. The region valued at approximately US$ 1.1-1.4 billion in 2026 is anticipated to reach US$ 2.7-3.4 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 13%. Data center expansion, driven by cloud services adoption and video streaming infrastructure buildout, represents the primary regional differentiator, establishing rapid tape storage demand growth.

IT and telecommunications sector modernization, particularly in India, China, and Southeast Asia, drives enterprise tape storage procurement acceleration. Third, government digital initiatives, including surveillance systems deployment and administrative data digitization, create proportionate tape storage requirements.

Competitive Landscape

The global tape storage market demonstrates moderate consolidation with specialized storage equipment manufacturers maintaining dominant market positioning through integrated product portfolios and established customer relationships. The top 5 suppliers, including IBM, Quantum (post-Spectra Logic acquisition), HPE, Fujifilm, and Sony, collectively control approximately 70% of global market share, reflecting incumbent advantages and supply chain integration. Market structure reflects bifurcation between integrated drive/cartridge manufacturers (IBM, proprietary formats) and standardized platform participants (Quantum, HPE supporting LTO).

Key Industry Developments:

- In August 2025, IBM announced a strategic partnership with a leading cloud service provider to enhance its tape storage solutions, integrating advanced AI capabilities. This move is significant as it not only strengthens IBM's position in the cloud storage market but also aligns with the growing trend of AI integration in data management, potentially offering customers more efficient and intelligent storage solutions.

- In September 2025, Hewlett Packard Enterprise launched a new line of tape storage products designed for high-density data centers. This initiative reflects the company's commitment to innovation and addresses the increasing need for scalable storage solutions.

Companies Covered in Tape Storage Market

- Dell Inc.

- Fujifilm Holdings Corporation

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Lenovo

- Oracle

- Overland Storage

- Qualstar Corporation

- Quantum Corporation

- Seagate Technology PLC

- Sony Corporation

- Others Key Players

Frequently Asked Questions

The Tape Storage market is estimated to be valued at US$ 5.7 Bn in 2026.

The primary demand driver for the tape storage market is the rapid growth of data generation combined with the need for cost-effective, long-term, and secure data archiving.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Tape Storage market.

Among the End- use, Data Centers holds the highest preference, capturing beyond 36.5% of the market revenue share in 2026, surpassing other End- use type.

The key players in Tape Storage are Dell Inc., Fujifilm Holdings Corporation, IBM Corporation, Lenovo and Oracle.