- Hardware & Software IT Services

- AI-Powered Storage Market

AI-Powered Storage Market Size, Share, and Growth Forecast, 2025 - 2032

AI-Powered Storage Market by System Type (Direct-attached Storage (DAS), Others), End-user (Enterprises, Government Bodies, Others), Storage Medium (Hard Disk Drive (HDD), Solid State Drive (SSD)), Storage Architecture (File-based Storage, Others), and Regional Analysis for 2025 - 2032

AI-Powered Storage Market Share and Trends Analysis

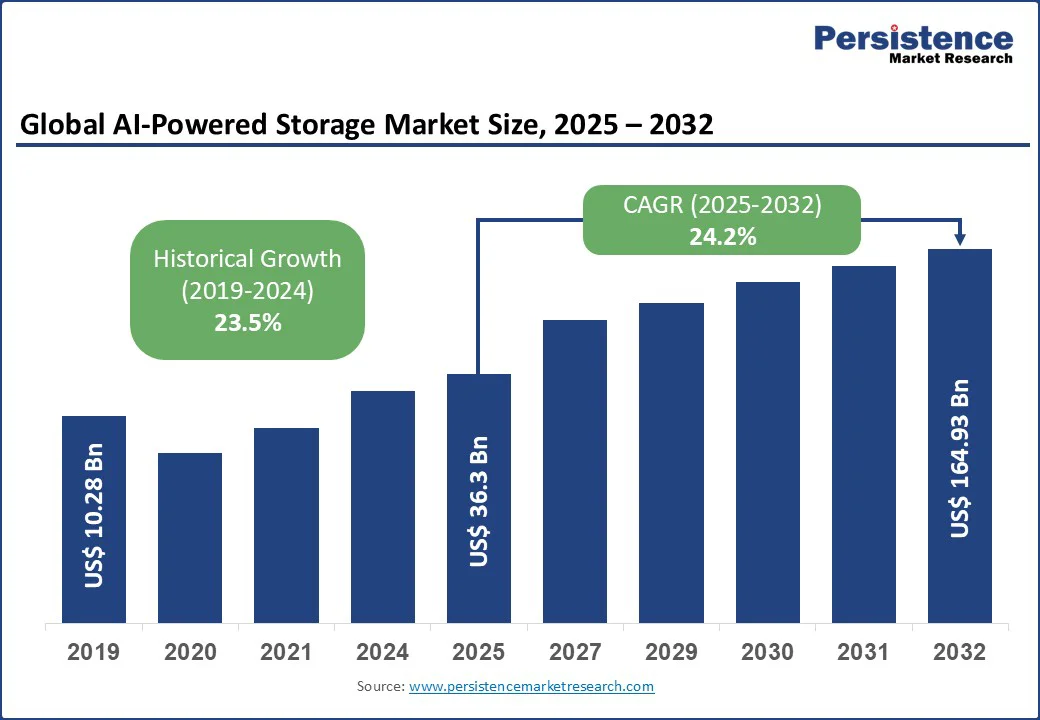

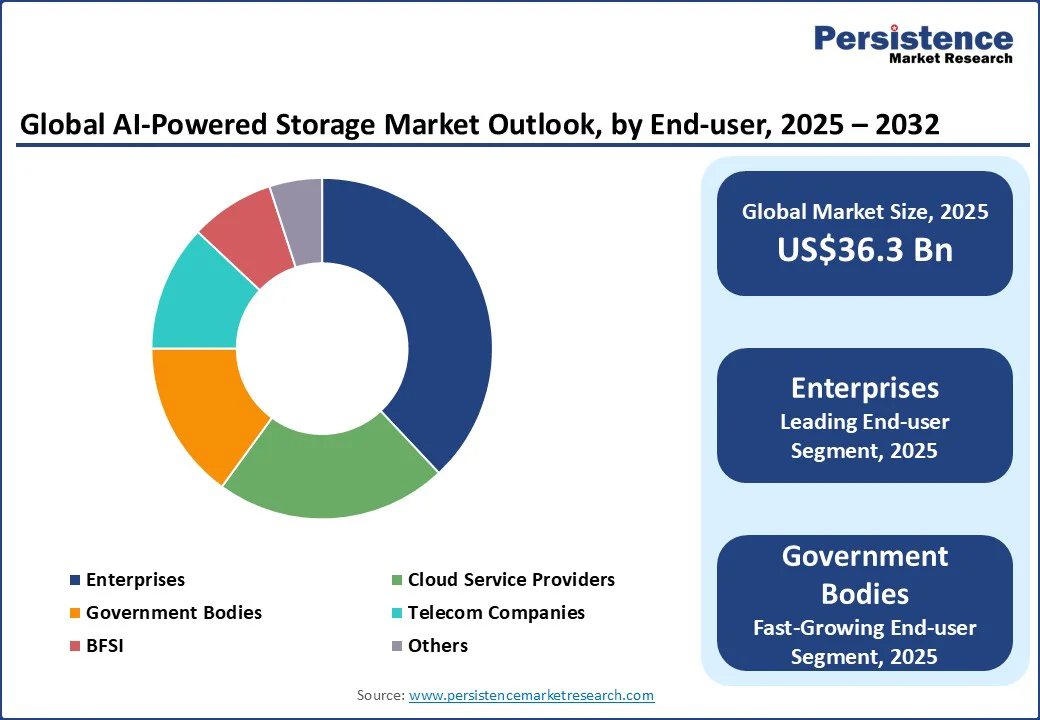

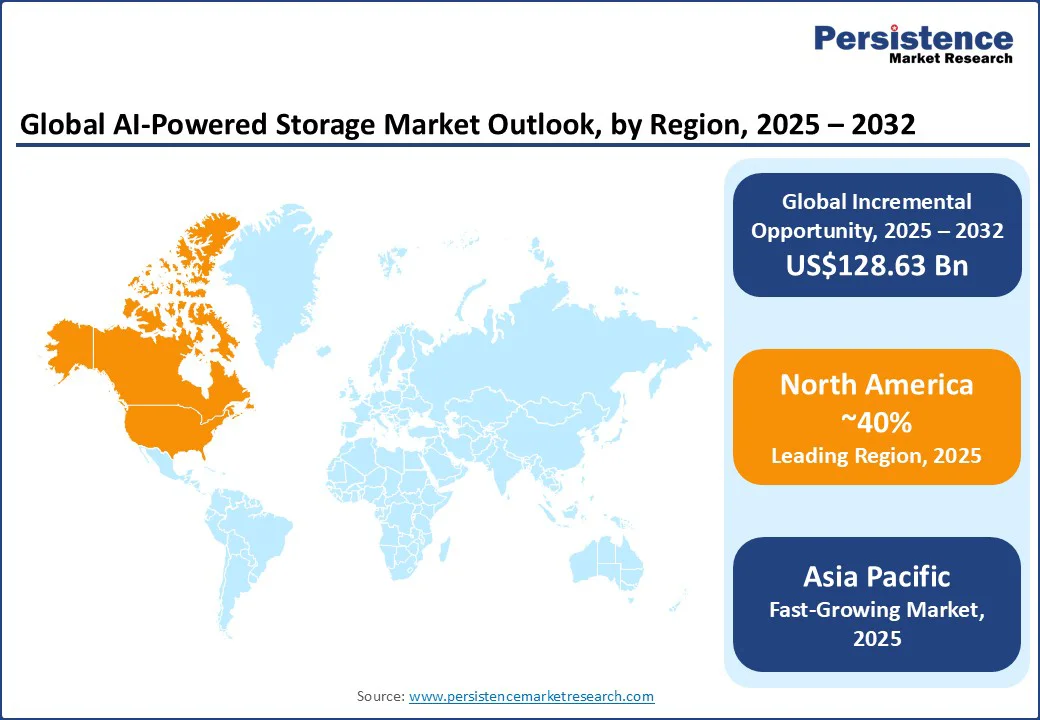

The global AI-powered storage market size is likely to be valued at US$36.3 Bn in 2025, and is estimated to reach US$164.93 Bn by 2032, growing at a CAGR of 24.2% during the forecast period 2025 - 2032.

Key Industry Highlights:

- Dominant End-user Segment: At around 38.0%, the enterprise segment is set to dominate the AI-powered storage market revenue share in 2025, due to widespread digital transformation and hybrid cloud storage adoption by organizations across industries.

- Fastest-growing End-user Segment: Government bodies are expected to experience the fastest growth with a CAGR of approximately 25.6%, on account of the increasing urgency among governments to manage vast, mission-critical datasets supporting national security, public safety, and citizen services.

- Leading Region: North America's leading share of nearly 40.0% in 2025 is backed by the strong presence of tech innovation giants such as Google and IBM, edge computing proliferation, and investments in energy-efficient AI storage technologies by enterprises in the region.

- Fastest-growing Regional Market: Asia Pacific, which is likely to hold around 32.0% market share in 2025, is poised to be the fastest-growing regional market through 2032, fueled by rapid industrialization, digital transformation of enterprise operations, and government-backed AI initiatives.

- Notable Development: In March 2025, IBM partnered with NVIDIA to integrate the NVIDIA AI Data Platform into its hybrid cloud infrastructure, launching content-aware storage within IBM Fusion to help enterprises build, scale, and manage generative and agentic AI workloads more effectively.

- Driver: The exponential growth in unstructured data from AI and IoT workloads, propelling demand for scalable, low-latency, and secure intelligent storage solutions.

- Emerging trends such as the convergence of storage with edge computing, hybrid and multi-cloud adoption, and AI-enabled automation and predictive analytics are creating vast opportunities for innovation and market expansion.

| Global Market Attribute | Key Insights |

|---|---|

| AI-Powered Storage Market Size (2025E) | US$36.3 Bn |

| Market Value Forecast (2032F) | US$164.93 Bn |

| Projected Growth (CAGR 2025 to 2032) | 24.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 23.5% |

The shift toward hybrid and multi-cloud environments, and the integration of artificial intelligence (AI) with energy-efficient storage technologies, are opening unprecedented opportunities for innovation and market penetration. AI-powered storage is revolutionizing how organizations manage surging data volumes by integrating AI into storage architectures.

Growth, Barriers, & Opportunity Analysis

Exponential Growth in Data Volume to Accelerate the AI Storage Market

The primary driver propelling the growth of the AI-powered storage market is the exponential surge in unstructured data generation, driven by the proliferation of digital technologies and devices powered by AI applications, IoT ecosystems, and cloud computing.

A recent study projects that the global datasphere will reach an astonishing 175 zettabytes by 2025, creating an unforeseen requirement for intelligent storage systems. This swelling data volume necessitates storage solutions with unmatched capacity, ultra-low latency, and real-time processing capabilities, prompting tech giants to innovate AI-optimized hardware and software.

In April 2025, Lenovo unveiled its largest-ever storage portfolio refresh, featuring 21 new AI-optimized ThinkSystem and ThinkAgile models, including AI Starter Kits, the industry’s first liquid-cooled HCI appliance, and hybrid cloud/virtualization solutions.

These solutions are designed to deliver up to 3 times the performance, achieve massive energy savings, and enable faster AI inferencing. Several such innovations are being regularly introduced in the market to support complex AI workloads, hybrid cloud models, and edge computing scenarios, forging new frontiers in the storage market ecosystem.

Hidden Expenses and High Operational Costs of AI Integration

The formidable burden of high initial capital expenditure, combined with hidden costs, operational expenses, and intricate integration challenges, which disproportionately impact small & medium enterprises (SMEs) and cost-sensitive industries, is turning out to be a critical growth-limiting factor for the AI-powered storage market.

Deploying AI-driven infrastructures necessitates expansive investments in cutting-edge hardware, AI-optimized software, and specialized talent, a trifecta that often culminates in a steep financial threshold, dissuading organizations from adoption despite long-term efficiency gains.

The initial budget for installing an AI storage system can easily run into six figures for enterprise-grade solutions, with hidden infrastructure costs potentially inflating the outlay by 30% to 50%. Moreover, integration complexities further exacerbate this barrier, as legacy storage systems lack standardized APIs, resulting in protracted migration timelines exceeding 12 months and requiring costly data preprocessing and reconciliation.

Compounding these issues are the stringent data privacy regulations, such as the GDPR of the European Union (EU), which amplify compliance costs and deployment delays, especially in multi-jurisdictional cloud and hybrid storage architectures.

Fusion of Edge Computing Technologies with AI to Bolster Strong Market Prospects

The seamless convergence of AI storage technologies with edge computing infrastructures is offering an efficient and cutting-edge solution to meet the escalating demand for real-time processing and ultra-low latency data management. As enterprises increasingly deploy AI workloads across distributed environments, this shift necessitates intelligent storage architectures capable of autonomously managing vast heterogeneous datasets near the source.

In March 2025, Aetina introduced a range of AI-powered edge computing innovations at Embedded World 2025, including its DeviceEdge systems built on NVIDIA Jetson Orin modules for intelligent decision-making, as well as the Qualcomm-backed MegaEdge AIP-FR68 workstation for high-performance on-premises generative AI and computer vision workloads.

This fusion not only accelerates enterprise digital transformation but positions AI-powered edge storage as a critical enabler for IoT expansion, autonomous systems, and immersive technologies such as augmented reality (AR) and virtual reality (VR).

The rising emphasis on data sovereignty and privacy compliance incentivizes localized AI storage solutions, creating a strong demand in regulated sectors such as healthcare, finance, and government. This intersection of AI, edge computing, and smart storage architectures represents a watershed point for players aiming to capture new revenue streams in the evolving data-centric economy.

Category-wise Analysis

End-user Insights

Enterprises, expected to hold a 38.0% revenue share in 2025, are driving demand for AI-powered storage due to the rapid growth of unstructured and structured data from digitizing operations in industries such as retail, healthcare, and manufacturing. The shift toward Industry 4.0 and AI-enabled automation requires intelligent storage systems capable of real-time data processing, automated storage stratification, and predictive maintenance.

In August 2025, Dell launched major upgrades to its AI Data Platform, partnering with Elastic and NVIDIA to boost data ingestion, retrieval, and GPU-accelerated performance for enterprise AI workloads. Enterprises are also investing heavily in hybrid cloud and edge computing architectures to support low-latency AI workloads, fueling the adoption of AI-powered storage systems that seamlessly integrate with complex multi-cloud environments.

Government bodies are set to witness the fastest growth in AI-powered storage adoption on account of an urgent need by governments worldwide to manage vast, mission-critical datasets supporting national security, public safety, and citizen services. Digitization efforts across government sectors are aimed toward scalability, unification of AI workloads across hybrid cloud platforms, and advanced analytics capabilities.

In August 2025, DeepSeek's new V3.1 AI model adopted a UE8M0 FP8 data format that cuts memory, computing power, and bandwidth demands significantly, enabling it to run on emerging Chinese-made chips and bolster China’s push for AI self-sufficiency. The growing focus on compliance with regulations such as GDPR and data sovereignty concerns will propel investment in secure and AI-enhanced storage infrastructure in the coming years.

Storage Architecture Insights

File-based storage is anticipated to retain its dominant position with a market revenue share of around 40.0% in 2025, owing to its ability to provide familiar and intuitive hierarchical data organization ideal for enterprise applications and legacy systems. Its proven efficiency in managing structured data such as documents, spreadsheets, and archived files infuses confidence in enterprises seeking reliability alongside AI-driven integration such as predictive analytics and ransomware protection.

An excellent example of this is the April 2025 announcement by Panzura of the integration of its Symphony platform with IBM Storage Deep Archive on the Diamondback tape library, automating metadata extraction and making archived “cold” data easily accessible for AI training and business discovery across distributed systems. Despite emerging alternatives, the compatibility of file storage systems with existing enterprise workflows and hybrid cloud environments is the primary factor ensuring the sustained market leadership of this segment.

Object storage, projected to register the highest CAGR through 2032, is experiencing rapid adoption owing to its scalability, metadata tagging, and inherent durability that perfectly suit the enormous, diverse datasets powering AI and machine learning models. The growth of unstructured data from images, videos, IoT sensor outputs, and autonomous system logs makes object storage indispensable for storing and retrieving data in distributed AI ecosystems.

Cloud-native architectures that optimize object storage and facilitate multi-cloud and hybrid deployments are crucial for digital transformation initiatives. Enterprises operating in niches such as fintech and autonomous vehicles are increasingly leveraging object storage for AI training datasets and real-time analytics, capitalizing on its flexibility and cost-effectiveness.

Regional Insights

North America AI-Powered Storage Market Trends

North America is predicted to secure approximately 40.0% of the AI-powered storage market share in 2025. Its dominance is principally rooted in the early adoption of AI technologies by enterprises in the region to manage exponentially rising data volumes across sectors and industries.

The U.S. spearheads the regional market, being home to some of the largest and futuristic innovation hubs and major cloud companies in the world that have been investing heavily in AI-enhanced storage infrastructures.

Regional projects exemplifying industrial-scale innovation include the signing of a non-binding MOU between SES AI and AISPEX in January 2025. This project aims to deliver up to 100 MWh of AI-managed battery energy storage systems at a Texas crypto-mining site, enhancing battery health and safety via its “AI for Safety” platform.

Asia Pacific AI-Powered Storage Market Trends

Asia Pacific is slated to be the fastest-growing regional market with a projected CAGR exceeding 27.0% during 2025 - 2032. Rapid modernization of legacy storage and retrieval systems across industries, unprecedented digitization drives by SMEs as well as large enterprises, and government-led AI initiatives such as South Korea’s smart infrastructure project are key growth determinants.

The burgeoning middle-class internet users and rising AI workload volumes in core sectors such as finance and manufacturing are likely to generate a massive demand for scalable, cost-efficient AI storage solutions in the region. The expansion of 5G networks will further support edge AI storage deployments, making Asia Pacific a hotbed for the innovation and adoption of cutting-edge storage technologies.

Europe AI-Powered Storage Market Trends

In Europe, market growth is contingent on enterprises of all sizes aligning with Industry 4.0 frameworks, fostering automated, AI-enabled manufacturing and logistics requiring intelligent, secure storage architectures. Strict data sovereignty laws such as GDPR have created an enormous demand for localized AI-powered storage solutions compliant with regional regulations, stimulating innovation in hybrid cloud and edge storage models tailored for privacy-centric enterprises.

European companies are also required to prioritize sustainability considerations when building or modifying their technological infrastructure, boosting the adoption of energy-efficient AI-driven storage systems.

Competitive Landscape

The global AI-powered storage market landscape is dynamic, shaped by the interplay of technological innovation, strategic partnerships, and aggressive portfolio expansion by leading players aiming to meet the soaring demand for intelligent data management.

The market is characterized by a moderately concentrated structure where a handful of technology giants and innovative startups occupy commanding positions, continuously investing in advancements such as AI-driven automation, machine learning-enabled predictive analytics, and non-volatile memory technologies such as NVMe and 3D XPoint.

Key companies such as Dell Technologies, IBM, and Pure Storage are rapidly refreshing their storage portfolios to incorporate liquid-cooled hyperconverged infrastructure and AI-powered ransomware protection. Furthermore, the advent of cloud and edge computing, coupled with data security and compliance imperatives, has sped up the inclusion of hybrid cloud offerings and encrypted storage solutions, intensifying competition.

Key Industry Developments

- In August 2025, IFS, an industrial AI software provider, acquired 7bridges, an AI-driven supply chain logistics specialist, boosting its logistics optimization capabilities. Alongside acquiring TheLoops and launching the Nexus Black AI accelerator, IFS is set to deliver advanced AI-enabled supply chain solutions for manufacturing, aerospace, and defense.

- In August 2025, MinIO launched MinIO Academy, a centralized platform offering role-specific training and hands-on labs for IT professionals to master AIStor, its high-performance object storage solution for Generative AI and analytics. Programs range from a free 60-day trial Quick Start to paid enterprise and partner tracks, addressing the growing skill gap in AI infrastructure.

- In June 2025, Pure Storage expanded its next-gen portfolio with FlashArray//XL R5, FlashArray//ST, and FlashBlade//S R2. It also introduced extended object support in FlashArray, enabling unified block, file, and object storage for seamless Enterprise Data Cloud deployment across on-premises, hybrid, and multicloud environments.

Companies Covered in AI-Powered Storage Market

- Dell Technologies Inc.

- Hewlett-Packard Enterprise Company

- NetApp, Inc.

- Pure Storage, Inc.

- International Business Machines Corporation (IBM)

- Seagate Technology LLC

- Western Digital Corporation

- NVIDIA Corporation

- Micron Technology, Inc.

- Wiwynn Corporation

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Amazon Web Services, Inc. (AWS)

- Cisco Systems, Inc.

- Synopsys, Inc.

- Advanced Micro Devices, Inc. (AMD)

- Arm Holdings plc

- Hitachi, Ltd.

- Toshiba Corporation

- Sensetime Group Inc.

Frequently Asked Questions

The AI-powered storage market is projected to reach US$36.3 Bn in 2025.

The exponential surge in unstructured data generation due to the proliferation of digital technologies and devices powered by AI applications, IoT ecosystems, and cloud computing is driving the market.

The market is poised to witness a CAGR of 24.2% from 2025 to 2032.

The convergence of AI storage technologies with edge computing infrastructures to meet the escalating demand for real-time processing and ultra-low latency data management, and the increasing deployment of AI workloads across distributed environments by enterprises are key market opportunities.

Dell Technologies Inc., Hewlett-Packard Enterprise Company, and NetApp, Inc. are some of the leading players in the market.