- Renewable Energy

- Solar Charge Controller Market

Solar Charge Controller Market Size, Share, and Growth Forecast 2026 - 2033

Solar Charge Controller Market by Product Type (PWM - Pulse Width Modulation, MPPT - Maximum Power Point Tracking), Current Capacity (Less than 20A, 20A to 50A, More than 50A), Application (Industrial, Commercial, Residential, Others), and Regional Analysis, 2026 - 2033

Solar Charge Controller Market Size and Trend Analysis

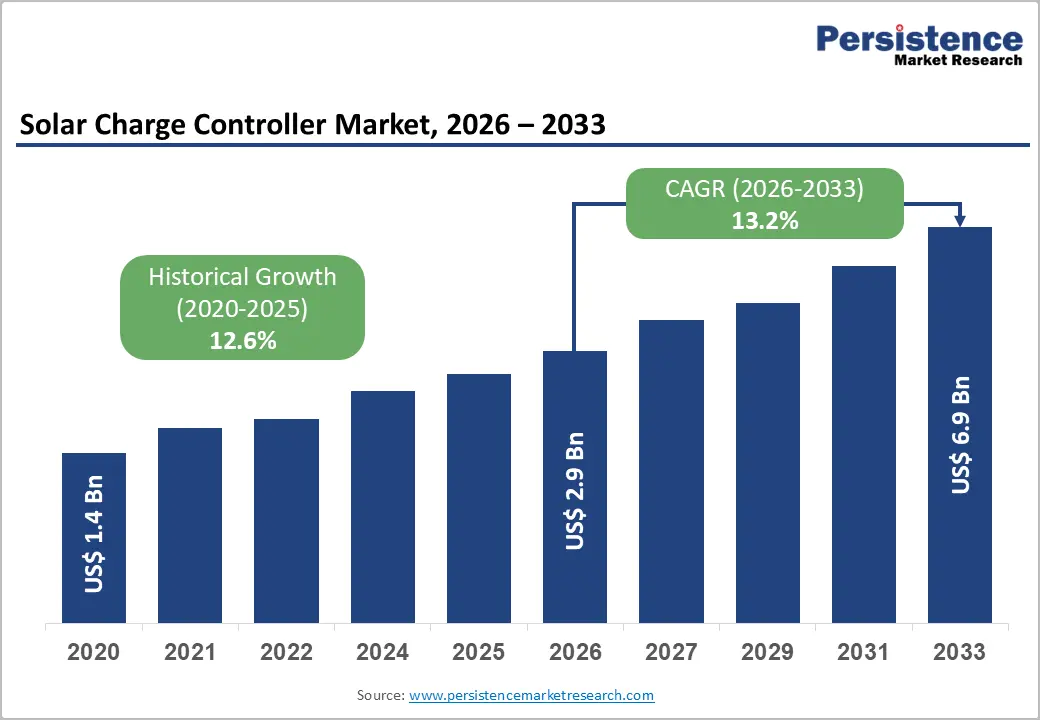

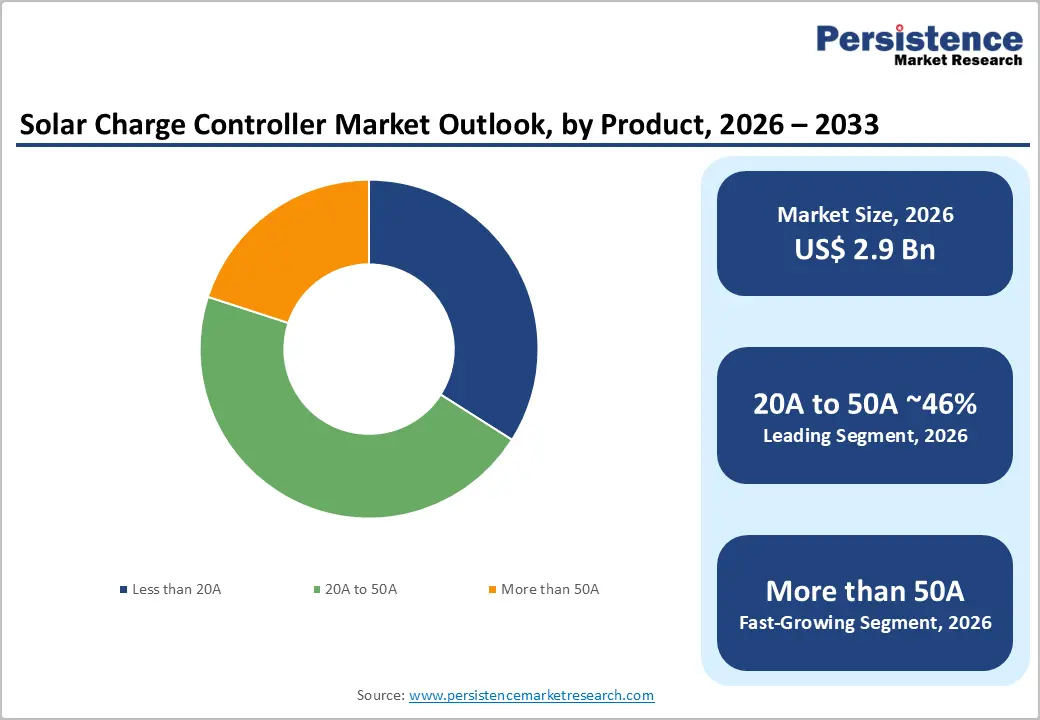

The global solar charge controller market size is expected to be valued at US$ 2.9 billion in 2026 and projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 13.2% between 2026 and 2033. This exceptional growth trajectory is driven by the exponential global expansion of solar photovoltaic (PV) installations, accelerating off-grid electrification programs in developing economies, and strong adoption of MPPT technology in both residential and commercial energy storage systems.

The market expanded from US$ 1.4 billion in 2020 to a historical CAGR of 12.6%, reflecting surging demand from Asia Pacific's solar-powered rural electrification initiatives and the rapid proliferation of rooftop solar-plus-storage systems across North America and Europe.

Key Industry Highlights:

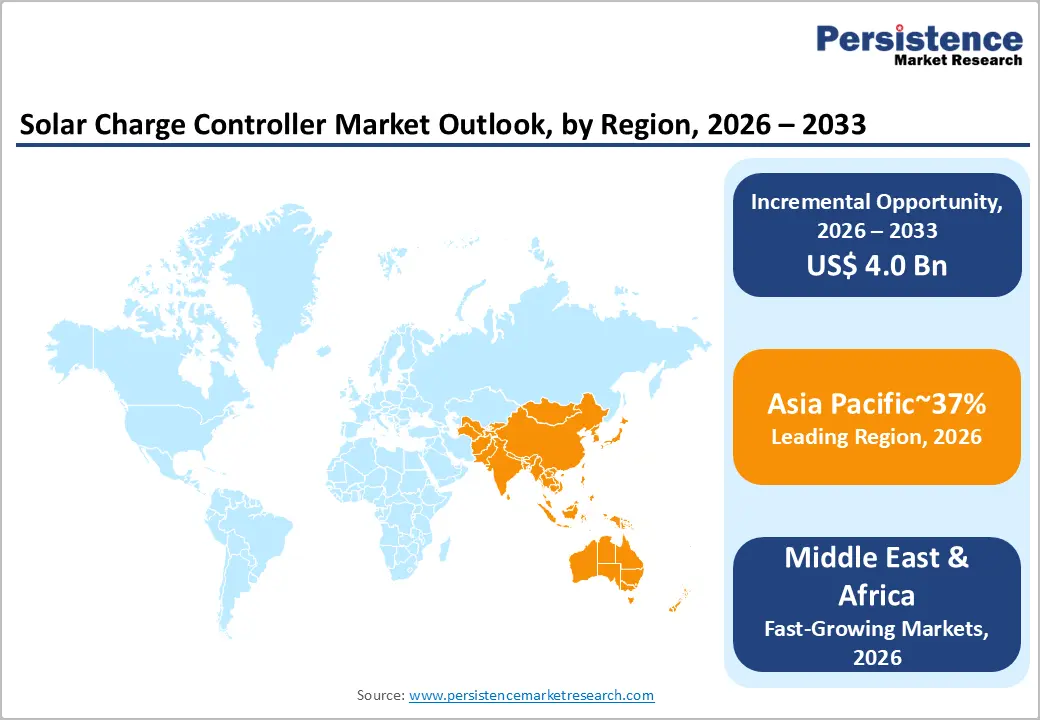

- Leading Region: Asia Pacific leads the global solar charge controller market with 37% market share in 2026, driven by China's massive solar manufacturing ecosystem, India's government-backed rooftop solar programs targeting 10 million installations, and large-scale off-grid electrification across Southeast Asia.

- Fastest Growing Region: MEA is the fastest growing solar charge controller region, with over 600 million people lacking electricity access per AfDB data and programs like Africa's Desert to Power Initiative targeting 10,000 MW of solar capacity driving unprecedented off-grid deployment demand.

- Dominant Product Segment: MPPT solar charge controllers hold 56% market share in 2026, commanding dominance due to their 10-30% energy yield advantage over PWM, compatibility with lithium batteries, and mandatory use in high-voltage solar panel string configurations.

- Fastest Growing Product Segment: PWM controllers are the fastest growing product type at 14% CAGR (2026 - 2033), driven by massive off-grid solar home system deployments in MEA and South Asia where cost-effective, entry-level solar electrification solutions are prioritized for rural energy access.

- Key Opportunity: Integration of IoT monitoring, mobile app connectivity, and LiFePO4/NMC battery algorithms in MPPT controllers creates a high-value upgrade supercycle, as the global transition toward lithium storage, projected by IEA to dominate by 2030, requires advanced charge management systems.

DRO Analysis

Drivers - Explosive Global Expansion of Solar PV Installations and Off-Grid Electrification

The unprecedented scale of solar photovoltaic deployment worldwide is the primary structural driver of solar charge controller demand. The International Energy Agency (IEA) reported that global solar PV capacity additions reached a record 295 GW in 2022, with the agency's Net Zero Emissions by 2050 Scenario targeting cumulative solar PV capacity exceeding 14,000 GW by 2050. Every off-grid, hybrid, and battery-backed solar installation requires a charge controller to regulate charging and prevent battery damage.

The United Nations' Sustainable Development Goal 7 (SDG 7), targeting universal access to affordable and clean energy, has mobilized hundreds of billions in funding for off-grid solar electrification across Sub-Saharan Africa, South Asia, and Southeast Asia, directly expanding the addressable market for solar charge controllers in remote and semi-remote installations globally.

Rising Adoption of Residential and Commercial Solar Energy Storage Systems

The rapid proliferation of residential solar-plus-storage systems, combining rooftop PV panels with lithium-ion or lead-acid battery banks, is creating a large and growing demand base for advanced solar charge controllers, particularly MPPT variants. According to the Solar Energy Industries Association (SEIA), cumulative residential solar installations in the U.S. surpassed 4 million homes by 2023, with storage attachment rates growing rapidly.

Government incentives including the U.S. Inflation Reduction Act's 30% Investment Tax Credit (ITC) for solar-plus-storage systems and the EU's Solar Energy Strategy targeting 320 GW of solar capacity by 2025 are accelerating residential and commercial installations globally. Each new installation incorporating battery storage requires a charge controller, directly translating policy-driven solar growth into sustained unit demand.

Restraints - Price Erosion and Commoditization of Low-End PWM Controllers

Intense competition among low-cost manufacturers, particularly from China, has driven significant price erosion in the PWM solar charge controller segment, compressing margins for all market participants. Average selling prices for entry-level PWM units have declined by an estimated 30-40% over the past five years, according to industry trade publications.

While this benefits end users, it creates sustained revenue pressure for manufacturers without differentiated product lines or strong brand equity. The commoditization of the lower-end segment makes it increasingly difficult for smaller manufacturers to achieve profitability, consolidating market share toward larger players with broader product portfolios.

Technical Complexity and Consumer Awareness Gaps in Emerging Markets

Despite growing solar adoption in emerging markets, limited technical awareness among end users regarding controller specifications, particularly the distinction between PWM and MPPT technology and their respective application suitability, leads to suboptimal purchasing decisions. Incorrect sizing or mismatched controller selection can reduce system efficiency by 10-30%, as noted in technical guidelines published by the International Renewable Energy Agency (IRENA). This knowledge gap suppresses upgrade cycles from PWM to higher-value MPPT controllers, slowing revenue growth per installation in cost-sensitive markets where consumer education and distributor technical training remain limited.

Opportunities - Surging Demand from the Middle East & Africa Solar Electrification Programs

The Middle East & Africa region represents the fastest growing market for solar charge controllers globally, underpinned by ambitious off-grid electrification programs, declining solar panel costs, and governments' urgent need to extend energy access without costly grid infrastructure expansion. The African Development Bank (AfDB) estimates that over 600 million people in Sub-Saharan Africa lack access to electricity, with off-grid solar being identified as the most cost-effective solution for the majority.

Programs such as Africa's Desert to Power Initiative, aiming to generate 10,000 MW of solar power for 250 million people, and Saudi Arabia's Vision 2030 Renewable Energy Program targeting 50% renewable energy by 2030 are channeling massive investment into solar systems requiring charge controllers, making MEA the highest-growth opportunity region for manufacturers through the forecast period.

Integration of IoT, Smart Monitoring, and Lithium Battery Compatibility in MPPT Controllers

The convergence of IoT connectivity, cloud-based energy management, and lithium battery technology is creating a premium product opportunity that commands significantly higher average selling prices. Next-generation MPPT controllers with integrated Wi-Fi/Bluetooth monitoring, mobile app compatibility, and multi-chemistry battery support (LiFePO4, NMC, lead-acid) are experiencing strong adoption in the residential and commercial segments. Victron Energy, Renogy, and Schneider Electric SE have introduced smart MPPT controllers with remote firmware updates and real-time performance analytics.

The global transition toward lithium-ion battery storage, projected by the IEA to dominate new installations by 2030, requires charge controllers with advanced battery management algorithms, creating an upgrade supercycle for MPPT smart controllers among existing solar system owners globally.

Category-wise Analysis

Product Type Insights

MPPT (Maximum Power Point Tracking) solar charge controllers hold the dominant position in the product type segment with 56% market share in 2026. MPPT technology's superiority lies in its ability to continuously optimize the electrical operating point of solar panels, extracting 10-30% more energy compared to PWM controllers under real-world conditions involving partial shading, temperature variation, and panel soiling, as documented in technical evaluations by IRENA and multiple solar research institutions.

MPPT controllers are also required for high-voltage panel strings and lithium battery systems, making them the default choice for commercial, industrial, and premium residential installations. Leading manufacturers including Morningstar Corporation OutBack Power Technologies, and Sungrow Power Supply Co., Ltd maintain extensive MPPT product portfolios, reinforcing the segment's technological and commercial dominance.

Current Capacity Insights

The 20A to 50A current capacity segment leads the market, accounting for approximately 46% market share in 2026. This mid-range capacity tier is the most widely deployed across residential rooftop solar systems, small commercial installations, and off-grid rural electrification projects, the three largest application categories globally. A 20-50A MPPT controller can effectively manage solar arrays ranging from approximately 400W to 3,000W at 12-48V battery systems, covering most typical residential and small commercial system sizes.

This capacity range balances cost-effectiveness with functional versatility, enabling use across a broad spectrum of applications without over-engineering. The Less than 20A segment serves entry-level off-grid applications, while More than 50A controllers address large commercial and industrial solar installations.

Application Insights

The residential application segment holds the leading position, representing approximately 42% of market share in 2026. The global surge in rooftop solar adoption, accelerated by falling panel costs, government incentive programs, and rising electricity tariffs, has made residential installations the single largest demand category for solar charge controllers.

According to IRENA, global residential solar capacity has been growing at double-digit rates annually, with tens of millions of new residential installations requiring charge controllers each year. The U.S. Inflation Reduction Act, India's PM Surya Ghar Muft Bijli Yojana targeting 10 million rooftop solar installations, and Germany's Solar Strategy for residential adoption collectively drive the residential segment's commanding market position through the forecast period.

Regional Insights

Asia Pacific leads the global solar charge controller market with 37% market share in 2026, while Middle East & Africa (MEA) is the fastest growing region, projected to record the highest CAGR through 2026 - 2033, driven by off-grid electrification urgency and ambitious solar energy transition programs across the region.

North America Solar Charge Controller Market Trends and Insights

North America is a technologically advanced solar charge controller market, characterized by strong adoption of high-capacity MPPT controllers in residential and commercial solar-plus-storage systems. The U.S. Inflation Reduction Act's 30% ITC is accelerating rooftop solar and energy storage deployments. Smart, IoT-enabled controllers with mobile app integration are the fastest growing product tier, supported by the region's high consumer digital adoption rates and premium brand preferences.

U.S. Solar Charge Controller Market Size

The United States accounts for approximately 80% of North American solar charge controller market revenue in 2026. With cumulative residential solar surpassing 4 million homes per SEIA data and storage attachment rates rising, the U.S. market is driven by premium MPPT adoption. The ITC extension under the Inflation Reduction Act through 2032 ensures sustained installation momentum and charge controller demand.

Europe Solar Charge Controller Market Trends and Insights

Europe represents a mature yet fast-evolving solar charge controller market, driven by the EU Solar Energy Strategy targeting 320 GW of capacity by 2025 and 600 GW by 2030. Residential energy independence motivations, amplified by energy price volatility post-2021, have dramatically accelerated rooftop solar-plus-storage adoption. Smart MPPT controllers with grid-connection monitoring and multi-battery-chemistry support are the dominant product tier across Germany, Italy, and the Netherlands.

Germany Solar Charge Controller Market Size

Germany contributes approximately 23% of European solar charge controller market revenue in 2026. Germany added a record 7.5 GW of solar capacity in 2022, per Bundesnetzagentur data, with rooftop installations driving charge controller demand. The country's feed-in tariff reforms and battery storage incentives under the Renewable Energy Sources Act (EEG) are sustaining strong residential solar-plus-storage deployment, requiring advanced MPPT charge controllers.

U.K. Solar Charge Controller Market Size

The United Kingdom represents approximately 11% of European solar charge controller market revenue in 2026. The UK Smart Export Guarantee (SEG) and falling battery storage costs are incentivizing residential solar-plus storage installations. The British Solar Renewables (BSR) association reports growing rooftop deployment rates, supporting steady MPPT controller demand, particularly in the residential and small commercial segments benefiting from government energy affordability programs.

France Solar Charge Controller Market Size

France accounts for approximately 9% of European solar charge controller market revenue in 2026. France's Programmation Pluriannuelle de l'Énergie (PPE) targets significant solar capacity expansion, supporting new installations. The French Environment and Energy Management Agency (ADEME) have promoted off-grid and hybrid solar systems in rural and island territories, generating demand for charge controllers beyond traditional grid-tied markets.

Asia Pacific Solar Charge Controller Market Trends and Insights

Asia Pacific leads global solar charge controller consumption, anchored by China's massive solar manufacturing and deployment ecosystem and India's rapidly expanding rooftop and off-grid solar programs. China alone accounts for approximately 40% of regional demand, with domestic manufacturers BEIJING EPSOLAR TECHNOLOGY CO. LTD and SRNE Solar Co., Ltd supplying both domestic and export markets. Southeast Asian off-grid electrification and Japan's post-Fukushima distributed energy push further diversify regional demand drivers.

India Solar Charge Controller Market Size

India represents approximately 20% of Asia Pacific solar charge controller market revenue in 2026. The PM Surya Ghar Muft Bijli Yojana targeting 10 million rooftop installations and the PM-KUSUM scheme for agricultural solar pumps, which individually require charge controllers, are key government-led drivers. India's Ministry of New and Renewable Energy (MNRE) targets 500 GW of renewable capacity by 2030, underpinning sustained demand growth.

Japan Solar Charge Controller Market Size

Japan contributes approximately 11% of Asia Pacific solar charge controller market revenue in 2026. Japan's distributed energy policy and residential solar adoption, supported by the Feed-in Tariff (FIT) and subsequent Feed-in Premium (FIP) systems, drive demand for advanced MPPT controllers. Japan's focus on energy resilience following natural disasters has accelerated solar-plus-storage adoption in residential and commercial segments, requiring sophisticated charge management solutions.

Southeast Asia Solar Charge Controller Market Size

Southeast Asia accounts for approximately 15% of Asia Pacific market revenue in 2026. The region's large rural off-grid populations, particularly in Indonesia, the Philippines, and Vietnam, represent a significant demand pool for PWM and entry-level MPPT controllers in off-grid solar home systems. The ASEAN Plan of Action for Energy Cooperation (APAEC) targets 23% renewable energy share by 2025, supporting national electrification programs that deploy solar charge controllers at scale.

Competitive Landscape

The global solar charge controller market is moderately fragmented, with a mix of established multinational players and a large base of Asian manufacturers competing across price and technology tiers. Schneider Electric SE, Victron Energy, and Morningstar Corporation lead on technology differentiation, particularly smart MPPT functionality and multi-battery-chemistry compatibility, while BEIJING EPSOLAR, SRNE Solar, and Renogy compete aggressively on price and volume.

Key differentiators include IoT/app integration, lithium battery algorithm support, and regulatory certification breadth. Emerging business model trends include direct-to-consumer e-commerce channels and solar kit bundling, pairing panels, batteries, and controllers as turnkey systems, which is reshaping distribution dynamics across residential and off-grid segments.

Key Developments

- In March 2025 , Victron Energy launched its next-generation SmartSolar MPPT series with integrated VE.Smart Networking, enabling seamless synchronization between multiple charge controllers and battery monitors in larger solar installations via Bluetooth mesh technology.

- In October 2024, Renogy introduced its Wanderer Li PWM and advanced MPPT controller series with dedicated LiFePO4 charging algorithms and integrated Bluetooth monitoring, targeting the rapidly growing residential and mobile solar (RV/marine) market segments.

- In June 2023, Schneider Electric SE announced expanded compatibility of its MPPT Solar Charge Controller range with lithium iron phosphate (LiFePO4) battery systems, addressing the accelerating shift away from lead-acid storage across commercial and industrial solar applications.

Solar Charge Controller Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.4 Billion |

| Current Market Value (2026) | US$ 2.9 Billion |

| Projected Market Value (2033) | US$ 6.9 Billion |

| CAGR (2026 - 2033) | 13.2% |

| Leading Region | Asia Pacific, 37% market share (2025) |

| Dominant Category - Product Type | MPPT Controllers, 56% market share (2025) |

| Top-Ranking Category - Current Capacity | 20A to 50A, 46% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 4.0 Billion |

Companies Covered in Solar Charge Controller Market

- Schneider Electric SE

- Morningstar Corporation

- Phocos

- BEIJING EPSOLAR TECHNOLOGY CO. LTD

- SRNE SOLAR CO., LTD

- Victron Energy

- Kontron Solar GmbH

- Luminous India

- Wenzhou Xihe Electric Co., Ltd

- Renogy

- OutBack Power Technologies

- Sungrow Power Supply Co., Ltd

- KATEK Memmingen GmbH

- AIRKOM

- Sunforge LLC

Frequently Asked Questions

The global solar charge controller market is projected to be valued at US$ 2.9 billion in 2026, up from US$ 1.4 billion in 2020. The market is forecast to reach US$ 6.9 billion by 2033, growing at a CAGR of 13.2%.

Primary demand drivers include record global solar PV capacity additions, reaching 295 GW in 2022 per IEA data, and the U.S. Inflation Reduction Act's 30% Investment Tax Credit accelerating residential solar-plus-storage deployments.

Asia Pacific leads with approximately 37% market share in 2026, anchored by China's dominant solar manufacturing and deployment capacity, India's government-backed rooftop and agricultural solar programs, and large-scale rural electrification across Southeast Asia.

The foremost opportunity lies in smart MPPT controllers with IoT connectivity and lithium battery compatibility, targeting the global transition to LiFePO4 and NMC storage systems, projected by the IEA to dominate new solar installations by 2030.

Leading companies in the global solar charge controller market include Schneider Electric SE, Victron Energy, Morningstar Corporation, OutBack Power Technologies, BEIJING EPSOLAR TECHNOLOGY CO. LTD, SRNE Solar Co., Ltd, Renogy, Sungrow Power Supply Co., Ltd, Luminous India, and Phocos.