- Renewable Energy

- Rooftop Solar PV Market

Rooftop Solar PV Market Size, Share, and Growth Forecast for 2025 - 2032

Rooftop Solar PV Market By Technology (Crystalline Silicon, Thin Films, Others), Connectivity (On-Grid, Off-Grid), Capacity (Below 10 kW, 10 kW to 100 kW, 100 kW to 1 MW, Above 1 MW), Application (Residential, Commercial, Industrial), and Regional Analysis for 2025 - 2032

Rooftop Solar PV Market Size and Trends Analysis

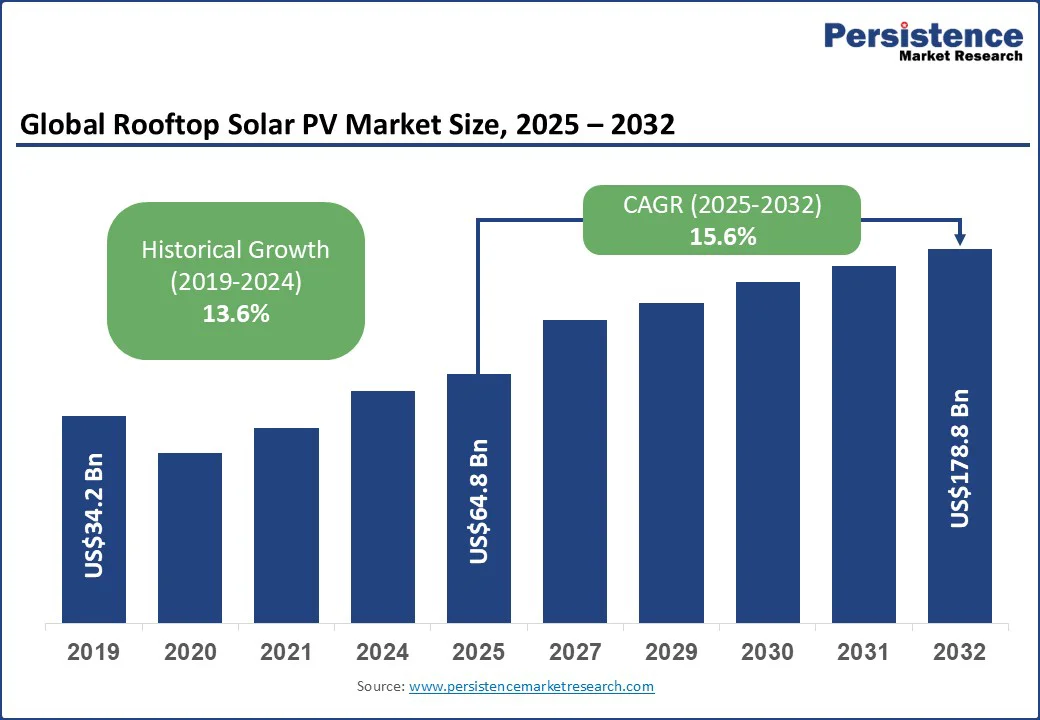

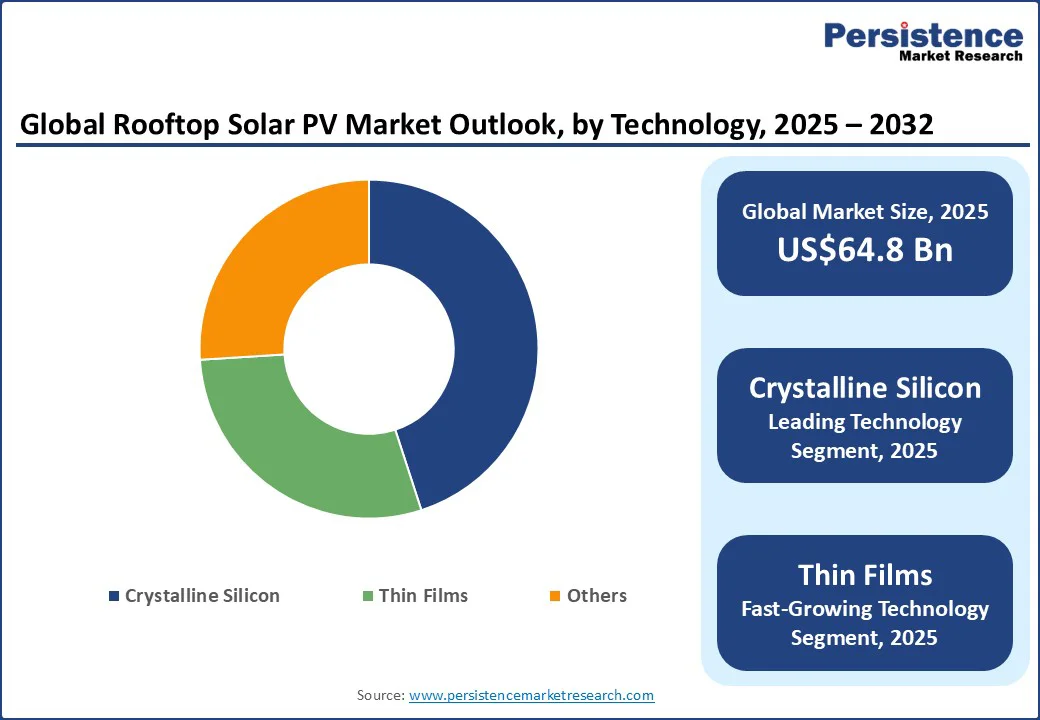

The global rooftop solar PV market size is likely to be valued at US$64.8 Bn in 2025 and is expected to reach US$178.7 Bn by 2032, growing at a CAGR of 15.6% during the forecast period from 2025 to 2032.

This rapid growth highlights the sector’s pivotal role in the global energy transition, driven by government incentives, cost-effective technological advancements, and rising demand for energy independence. Increasing investments in renewable infrastructure continue to strengthen rooftop solar’s role as a vital driver of sustainable urban development.

Key Industry Highlights

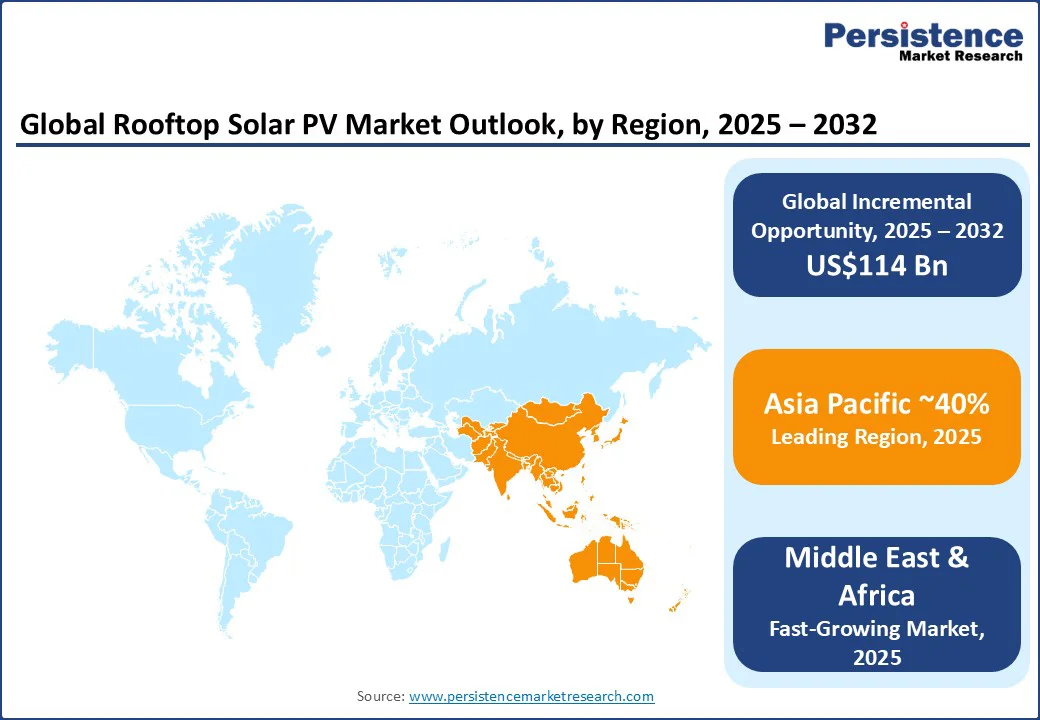

- Leading Region: Asia Pacific is anticipated to lead globally with approximately 40% market share, buoyed by strong government incentives, urbanization, and industrial energy demand across China, India, and Japan.

- Fastest-growing Region: The Middle East & Africa is anticipated to emerge as the fastest-growing region in the global rooftop solar PV market in 2025, expanding at a robust 17.1% CAGR, driven by abundant sunlight, strong government support, declining technology costs, and rising energy demand.

- Dominant Application Type: Residential application remains dominant by ~60% share, driven by urban rooftop expansion and favorable net-metering policies encouraging homeowners to invest in self-generation.

- Fastest-growing Application Type: The commercial segment is anticipated to be the fastest-growing, propelled by corporate sustainability goals and large-scale rooftop installations aimed at reducing operating costs and environmental footprint.

- Leading Technology Type: Crystalline silicon is projected to hold approximately 45% share of the market in 2025, driven by its high efficiency, proven reliability, and steady cost reductions, making it the preferred choice for residential and commercial users seeking faster payback periods.

- Fastest-growing Technology Type: Thin-film modules are likely to emerge as the fastest-growing technology, despite crystalline silicon holding a significant share of around ~45%; thin-film adoption is rising due to lower costs and installation versatility.

|

Global Market Attribute |

Key Insights |

|

Rooftop Solar PV Market Size (2025E) |

US$64.8 Bn |

|

Market Value Forecast (2032F) |

US$178.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

15.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

13.6% |

Market Dynamics

Driver - Policy-Led Economics Powering the Global Rooftop Solar Revolution

The foremost global driver for rooftop solar adoption is regulatory support that enables prosumers to thrive at scale. Net-metering and self-consumption frameworks, fiscal incentives, and solar-ready building standards enhance rooftop project economics by providing advantages over retail tariffs. As a result, adoption is accelerating across residential, commercial, and industrial segments. Rapidly declining equipment costs further compress payback periods, making investment decisions faster and more attractive.

The EU’s Solar Rooftops Initiative embeds solar-ready requirements and phased obligations in the revised Energy Performance of Buildings Directive, driving distributed PV from 2027 to 2030. India’s PM Surya Ghar scheme targets 10 million rooftop homes with clear subsidy pathways, while MNRE reports 19.88 GW of grid-connected rooftop installed as of July 2025. The IEA highlights solar PV as the largest contributor to renewable additions in 2024, with distributed growth set to accelerate, while DOE/NREL confirms continuing cost declines.

Restraint - Grid Bottlenecks and Supply Chain Gaps Restrain Rooftop Solar Scalability

The rapid growth potential of rooftop solar is increasingly tempered by challenges in connecting systems to the grid. Lengthy permitting processes, restrictive utility interconnection rules, and limited grid flexibility often delay installations, leaving both households and businesses frustrated despite favorable economics. These hurdles not only extend project timelines but also erode investor confidence in certain markets.

Beyond regulatory delays, supply chain vulnerabilities add another layer of complexity. Advanced components such as smart inverters, storage-ready modules, and other balance-of-system parts remain concentrated in a few manufacturing hubs, leaving the market exposed to shortages and price volatility. Fluctuating raw material costs and fragmented sourcing structures have resulted in installation backlogs and unpredictable project economics, ultimately constraining the pace at which rooftop solar can scale globally.

Opportunity - Digitalization and Smart Integration Elevate Rooftop Solar to the Next Growth Phase

Rooftop solar is rapidly evolving from simple power generation to an intelligent energy ecosystem. The rise of smart inverters, AI-driven energy management, and storage-linked systems is transforming rooftops into dynamic grid assets that support demand response and enhance energy resilience. This shift enhances efficiency while aligning with global sustainability goals, positioning rooftop PV as a vital pillar in achieving decentralized, net-zero energy networks.

Momentum for this transformation is already visible across policy and industry landscapes. The European Commission’s Digitalisation of Energy Action Plan highlights the role of rooftop PV in smarter grids, while India’s Green Energy Corridor is upgrading infrastructure for distributed generation.

On the corporate side, innovators such as Tesla and Sungrow are embedding digital monitoring, storage, and EV charging into rooftop solutions, shaping a consumer-centric and intelligent solar ecosystem that defines the market’s next phase of growth.

Category-wise Analysis

Technology Insights

Crystalline silicon is expected to hold a significant position in the global rooftop solar PV market with an estimated share of ~45% in 2024. Its leadership is supported by high efficiency, proven reliability, and steady cost reductions, making it the preferred choice for residential and commercial users seeking faster payback periods. Governments also favor this technology in subsidy programs due to its scalability and long-standing performance, ensuring continued growth alongside advancements in storage and grid integration.

Thin-film technologies, though smaller in share, represent the fastest-growing segment. Their lightweight structure and ability to operate efficiently under low light and high temperatures make them ideal for industrial and unconventional rooftops. Supportive initiatives, especially in Europe and Japan, for building-integrated photovoltaics are still in the early stages but are gaining momentum through R&D and pilot projects, positioning them as future disruptors in the rooftop solar landscape.

Propulsion Type Insights

On-grid rooftop solar PV systems are projected to lead with approximately 70% in 2024. Their dominance is driven by supportive frameworks such as net-metering, feed-in tariffs, and renewable portfolio standards that ensure financial returns and grid integration benefits.

Residential, commercial, and industrial users across Europe, the U.S., and China increasingly favor on-grid installations to hedge against rising electricity prices and secure long-term savings, making them the central pillar of global rooftop solar deployment.

Off-grid systems, though smaller in share, represent one of the fastest-growing opportunities. Their relevance is pronounced in Asia, Africa, and Latin America, where limited grid infrastructure and the need for energy self-sufficiency fuel adoption. Programs such as India’s solar village schemes and Africa’s donor-backed mini-grid initiatives are expanding access to clean power for rural communities and remote industries.

Regional Insights

Asia Pacific Rooftop Solar PV Market Trends - Emerges as the Global Pacesetter Through Policy Support and Consumer Adoption

Asia Pacific is expected to lead the global market with approximately 40% share, supported by robust government incentives, rapid urbanization, and growing industrial energy demand in China, India, and Japan. China anchors Asia Pacific’s rooftop PV landscape, driven by large-scale county-wide distributed programs and strong manufacturing capacity.

According to the International Energy Agency (IEA), China added a record 36 GW of rooftop solar capacity in Q1 2025, underscoring its position as the global leader in distributed solar adoption. Momentum is also strong in India, where the Ministry of New and Renewable Energy (MNRE) has rolled out the PM Surya Ghar program, targeting 30 GW of residential rooftop installations by FY 2026-27, backed by subsidies and domestic manufacturing mandates.

Australia’s Clean Energy Regulator reported over 300,000 new rooftop installations in 2024, reflecting steady household adoption supported by incentive schemes and rising battery attachments. Japan complements the region’s strength with its Feed-in Premium framework, encouraging self-consumption and ensuring sustained growth in residential adoption. Collectively, robust policies, regulatory backing, and consumer-driven energy independence are positioning Asia Pacific as the global pacesetter for rooftop PV scale and innovation.

North America Rooftop Solar PV Market Trends - Incentives and Residential Growth

The U.S. leads North America’s rooftop solar PV market, supported by favorable policy incentives and rapidly expanding residential adoption. The U.S. Department of Energy (DOE) reports that rooftop PV contributed significantly to distributed generation growth in 2024, with adoption accelerated by the Inflation Reduction Act’s tax credits and state-level net metering frameworks.

Canada is also seeing rising momentum, with programs under Natural Resources Canada (NRCan) promoting rooftop solar through the Canada Greener Homes Initiative, which provides grants and loans for residential solar adoption. Together, these developments highlight how strong regulatory backing, cross-border investments, and consumer demand for energy independence are reinforcing North America’s position as a critical growth region for rooftop PV.

Europe Rooftop Solar PV Market Trends - Policy Harmonization and Market Incentives

Germany stands at the forefront of Europe’s rooftop solar PV market, underpinned by strong regulatory frameworks and household adoption. The European Commission has advanced the Solar Rooftops Initiative within its Energy Performance of Buildings Directive, mandating solar-ready and phased rooftop installations across residential and commercial structures from 2027 onward, solidifying Germany’s leadership.

France and Italy are also showing robust momentum, supported by national feed-in premium schemes and tax credits, while the International Energy Agency (IEA) highlights both nations among Europe’s fastest-growing solar adopters in 2024.

The United Kingdom is witnessing a surge in small-scale rooftop installations driven by falling costs and rising consumer demand for energy independence, while Spain has capitalized on the removal of the “sun tax” and new self-consumption policies to accelerate rooftop adoption. Collectively, policy harmonization under the EU Green Deal, reinforced by national subsidy frameworks, positions Europe as a pivotal region in advancing distributed rooftop solar deployment.

Competitive Landscape

The global rooftop solar market is highly competitive with PV players driving growth through capacity expansion, technology upgrades, and strategic partnerships, creating a competitive yet collaborative environment. By aligning with policy incentives and digital energy trends, they are accelerating adoption while keeping solutions affordable and innovative. This healthy competition is steering the industry toward sustainable long-term growth.

Supply chains are equally evolving, with localized production, smarter distribution networks, and digital sales platforms enhancing efficiency. Stronger manufacturer-distributor coordination ensures resilience, better service, and reliable market scaling, making competition a catalyst for broader rooftop PV adoption.

Key Industry Developments

- In March 2025, LONGi unveiled record-breaking 33% efficiency in crystalline silicon-perovskite tandem solar cells, setting a new global benchmark at SNEC 2025. This strengthened LONGi’s leadership in solar innovation, positioning tandem technology as a future enabler for higher rooftop system yields and lower levelized cost of electricity (LCOE).

- In May 2025, LONGi launched its EcoLife Series of back-contact (HBC) residential solar modules, offering 25% efficiency with 510 W output and 30-year durability. The product line specifically targeted rooftop applications, enhancing aesthetics and longevity while meeting growing consumer demand for reliable home energy solutions.

- In April 2025, Complete Solaria rebranded as SunPower, following its acquisition of SunPower’s assets, marking the legacy brand’s comeback with renewed market presence. This strategic move revived one of the most recognized names in solar, aiming to expand its rooftop portfolio and regain trust among residential and commercial customers.

Companies Covered in Rooftop Solar PV Market

- LONGi Group

- SunPower Corporation

- First Solar, Inc.

- Canadian Solar Inc.

- Trina Solar Co. Ltd.

- E-Ton Solar Tech Co., Ltd.

- Jinko Solar Holding Co. Ltd.

- Indosolar Ltd

- Yingli Energy Development Company Limited

- Hanwha Qcells Co., Ltd.

- Silfab Solar Inc.

- JA Solar Technology Co., Ltd

Frequently Asked Questions

The rooftop solar PV market is set to reach US$64.8 Bn in 2025.

Favorable policies and economic incentives are fueling the rooftop solar boom, reshaping how energy is generated and consumed at the community level.

The industry is estimated to rise at a CAGR of 15.6% from 2025 to 2032.

Smart digital solutions and advanced integration are opening new avenues for rooftop solar, driving efficiency and scalability.

The major players include LONGi Group, SunPower Corporation, First Solar, Inc., Canadian Solar Inc., and Trina Solar Co. Ltd.