- Renewable Energy

- Non-Concentrating Solar Collectors Market

Non-Concentrating Solar Collectors Market Size, Share, and Growth Forecast, 2026 – 2033

Non-Concentrating Solar Collectors Market by Technology Type (Flat Plate Collector, Evacuated Tube Collector, Unglazed Collector), Material Type (Metal, Plastic, Glass, Others), Application (Residential Heating, Commercial Heating, Industrial Heating, Agricultural Heating), and Regional Analysis for 2026-2033

Non-Concentrating Solar Collectors Market Share and Trends Analysis

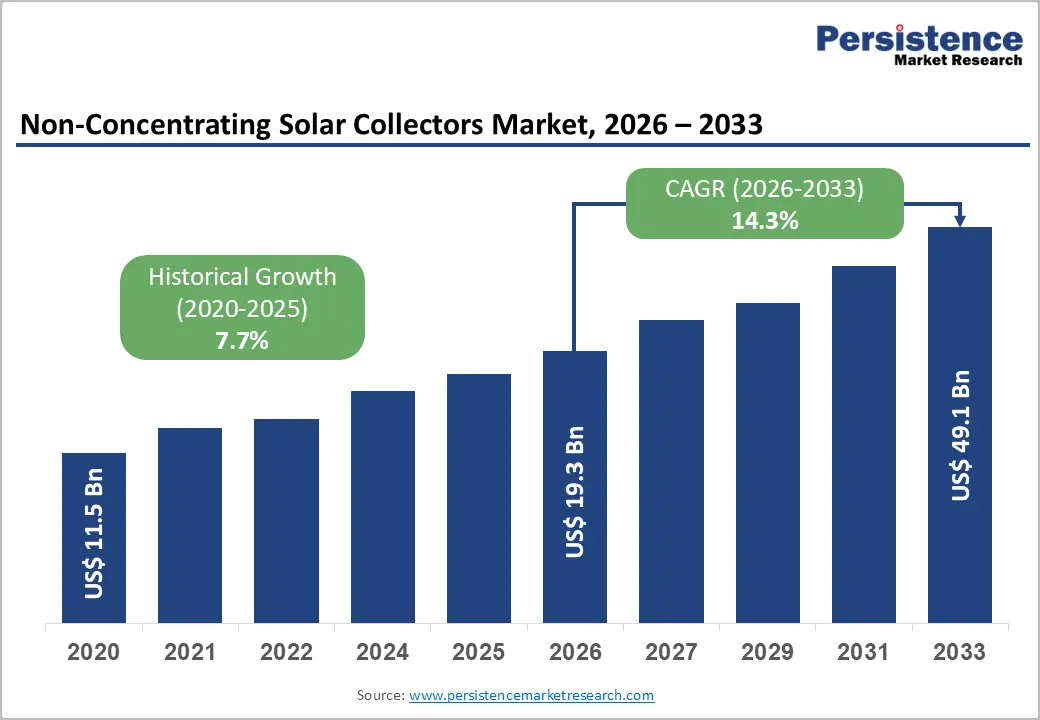

The global non-concentrating solar collectors market size is likely to be valued at US$ 19.3 billion in 2026, and is projected to reach US$ 49.1 billion by 2033, growing at a CAGR of 14.3% during the forecast period 2026−2033.

Market expansion is driven by rising demand for decentralized renewable energy systems and adoption of sustainable heating solutions. Increasing urbanization, population growth, and government-led renewable energy mandates encourage deployment in residential and commercial sectors. Technological innovation in collector efficiency and durability enhances adoption across diverse climatic conditions. Integration with smart monitoring platforms enables real-time performance tracking, improving operational efficiency and consumer confidence. Rising awareness of environmental impact and energy cost reduction motivates commercial and industrial entities to integrate solar thermal solutions. Strengthening infrastructure in developing regions facilitates wider accessibility, enabling market penetration in previously underdeveloped areas.

Key Industry Highlights

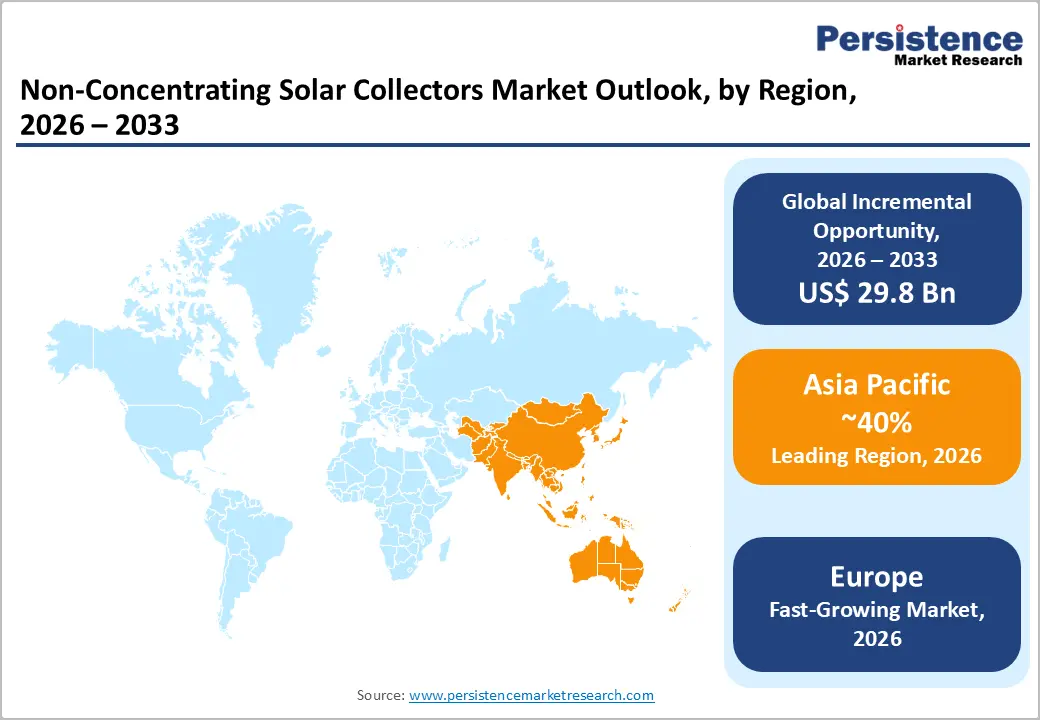

- Dominant Region: Asia Pacific is slated to lead the market in 2026 with an estimated 40% share, driven by strong manufacturing and supportive policies.

- Fastest-growing Regional Market: Europe is expected to be the fastest-growing market from 2026 to 2033, supported by policies and regulatory incentives.

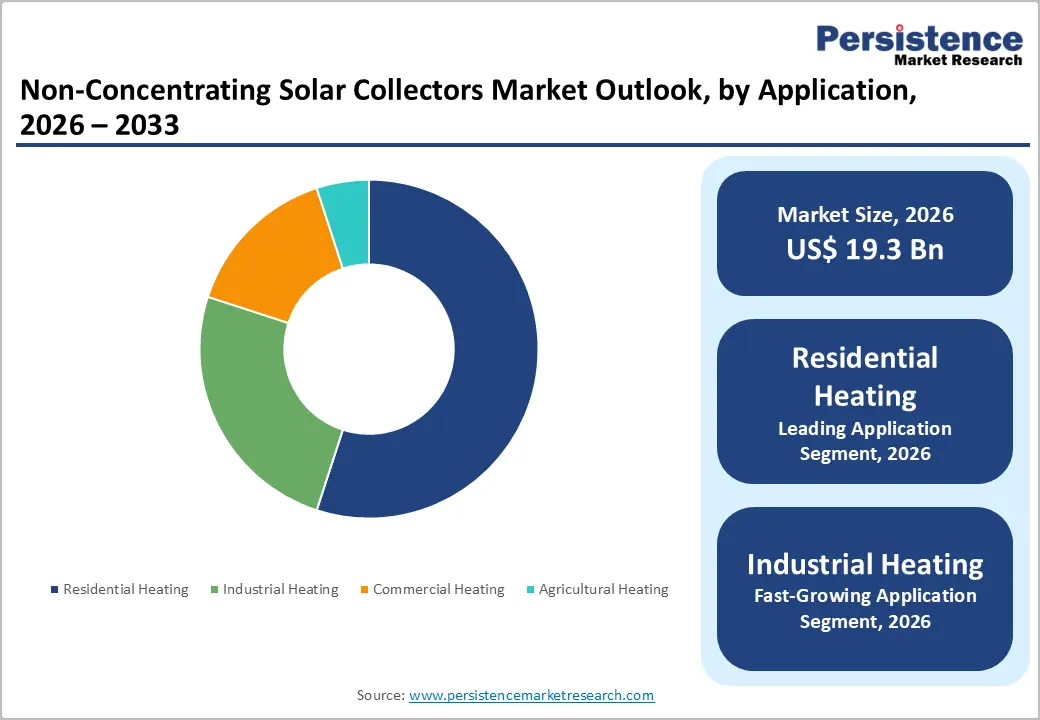

- Leading Application: Residential heating is likely to hold nearly 55% of the market share in 2026, boosted by ease of installation, efficiency, and cost savings.

- Fastest-growing Application: Industrial heating is set to be the fastest-growing application from 2026 to 2033, propelled by high thermal demand and cost-saving opportunities.

| Key Insights | Details |

|---|---|

|

Non-Concentrating Solar Collectors Market Size (2026E) |

US$ 19.3 Bn |

|

Market Value Forecast (2033F) |

US$ 49.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Government Incentives and Regulatory Support

Government incentives create a predictable cost reduction pathway for investors and end users, directly improving project economics and lowering barriers to adoption. For example, the U.S. Internal Revenue Service (IRS) offers a 30% Residential Clean Energy Tax Credit on eligible solar and related clean energy property costs for systems installed through December 31, 2025, enabling homeowners to recoup a substantial portion of upfront expenditure through their federal tax liability. By shifting a significant portion of capital outlay into tax savings, this incentive reshapes investment calculations for residential and commercial buyers, shortening payback periods and improving return on investment metrics for renewable heating and hot water solutions.

Regulatory support from government agencies establishes clear rules of engagement and a stable policy environment that encourages long term planning and capital commitments by developers and financiers. Clear eligibility criteria for tax credits, standards for equipment certification, and defined sunset dates on incentives reduce investor uncertainty and allow supply chain actors to align product development and deployment schedules with policy timelines. This framework attracts capital by reducing perceived risk, fostering economies of scale in manufacturing and installation, and enabling new financing mechanisms such as third party ownership and green bonds.

Growth in Residential and Commercial Heating Demand

The rise in demand for heating services in homes and businesses reflects a fundamental shift in energy consumption patterns that directly influences thermal system deployment. Water heating alone represents about 18% of a typical U.S. home’s energy use, making it one of the largest controllable loads for consumers seeking to manage utility expenses and energy security. Solar derived heat delivers a reliable source of thermal energy that offsets conventional fuel use, leading to significant reductions in operating costs compared with grid dependent systems. On a government platform, the U.S. Department of Energy (DOE) notes that solar water heating systems can reduce water heating bills by 50%–80%, meaning stakeholders in both residential and commercial segments can achieve tangible savings while curbing exposure to volatile fuel markets.

Business demand patterns also show increasing prioritization of energy performance and sustainability metrics in building operations. Commercial facilities such as hotels, hospitals and educational campuses allocate substantial budget to meet consistent hot water and space heating loads, where high thermal demand correlates with operating costs and carbon intensity. In this context, solar based thermal solutions provide organizations with a method to mitigate expense escalation tied to fossil fuel price fluctuations and regulatory emissions targets, enhancing financial predictability.

Heavy Dependence on Solar Availability

Solar radiation levels vary significantly over time and geography, which impacts the thermal output of systems that directly rely on sunlight to generate usable heat. In locations with frequent cloud cover, seasonal monsoons, or extended periods of low solar irradiance, actual energy capture can fall well below design expectations, affecting performance predictability and financial returns. Government sourced solar resource assessment data highlight the ongoing need for accurate, high resolution irradiation profiles to inform system planning and mitigate risks associated with resource uncertainty. Variability in solar intensity throughout the day and across seasons influences operational yield and exposes projects to revenue volatility when sunlight availability dips, with increased reliance on supplemental heating or storage systems where sunlight is insufficient.

Energy planners and stakeholders recognize that operational efficiency and system utilization are constrained by the inherent intermittency of solar irradiance. Solar forecasting and resource assessment programs at national laboratories are funded to refine models that quantify short term and long term resource patterns, providing essential data for design optimization and risk reduction. When solar radiation fluctuates unexpectedly due to weather patterns or geographic differences, thermal delivery rates decline and performance projections become less reliable, leading to higher integration costs and underutilized capacity during low-irradiance periods.

Competition from Other Renewables

Non-concentrating solar collectors face strong market pressure due to the rapid expansion of alternative renewable energy technologies. Photovoltaic (PV) systems and heat pumps attract investment from residential, commercial, and industrial sectors seeking versatile and high-efficiency energy solutions. PV systems generate electricity directly from sunlight, providing greater energy flexibility for on-site consumption or grid export. Heat pumps offer efficient space and water heating with minimal reliance on solar irradiance, enabling year-round performance. Market stakeholders often prioritize these solutions over thermal collectors, viewing them as integrated options for reducing operational costs and enhancing energy management.

Emerging hybrid solutions combining PV, battery storage, and electric heat pumps further intensify market challenges. Investors and end-users compare lifecycle costs, maintenance requirements, and return on investment, frequently selecting technologies delivering multiple energy services. Non-concentrating solar collectors focus primarily on thermal energy generation, which restricts flexibility for applications requiring electricity or hybrid energy systems. Financial incentives and incentives frameworks increasingly favor technologies with higher energy output per unit area and multi-purpose functionality, resulting in slower adoption of standalone thermal collectors.

Opportunity Analysis- Expansion into Industrial and Commercial Applications

Industrial and commercial users demand consistent, high temperature heat for operations such as food processing, chemical production, textile manufacturing, and mineral treatment, driving the attractiveness of thermal solutions that integrate with existing heat systems. Government and industry data show significant momentum in deploying solar-derived process heat, with 106 new solar heat for industrial process (SHIP) plants beginning operation across 20 countries in 2024. Government records indicate this uptake reflects increasing interest in reducing fossil fuel consumption and stabilizing energy costs in heat-intensive sectors.

Industrial and commercial applications offer scale and predictable thermal loads that align well with solar heat usage, enabling heat generation at temperatures required for cleaning, sterilization, drying, and chemical reactions without the volatility of fossil fuel prices. Broader adoption in these segments supports corporate environmental commitments and regulatory compliance with emissions standards, particularly where policy frameworks encourage renewable heat deployment.

Technological Innovation and Integration

Government research funding and integration programs drive innovation by accelerating the development, validation, and commercialization of advanced solar technologies and systems. U.S. Department of Energy initiatives, for instance, promote collaboration between national laboratories, industry, and academia to improve reliability, efficiency, and cost-effectiveness of next-generation solar solutions. Structured programs targeting systems integration, manufacturing competitiveness, and deployment strategies encourage adoption of advanced materials, coatings, and monitoring systems.

Industry participants gain access to technical platforms, standardized evaluation methods, and knowledge networks that support improved design and system performance. Integration initiatives ensure that solar technologies interface effectively with energy storage and grid infrastructure, increasing deployment flexibility and operational stability. Public-sector programs reduce technical risk and enable demonstration projects, which attract private capital and stimulate faster adoption of innovative solutions.

Category-wise Analysis

Technology Type Insights

Flat plate collector is anticipated to secure around 52% of the non-concentrating solar collectors market revenue share in 2026, reflecting widespread use in residential and commercial applications. Reliability, proven efficiency under moderate climate conditions, and ease of installation contribute to market dominance. Compatibility with existing water heating and heating, ventilation, and air conditioning (HVAC) systems facilitates integration and adoption across diverse user segments. Operational stability and durability enhance provider preference, encouraging large-scale procurement. Regulatory frameworks supporting energy efficiency improvements in buildings further reinforce flat plate adoption.

Evacuated tube collector is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by high thermal efficiency and superior performance in low-temperature and low-insolation conditions. Innovation in tube materials, selective coatings, and vacuum sealing techniques enhances energy capture and reduces heat loss. Increased adoption in industrial and agricultural heating applications drives volume growth. Technological advancements supporting hybrid system integration with smart monitoring platforms encourage early adoption.

Application Insights

Residential heating is likely to be the leading segment with a projected 55% of the non-concentrating solar collectors market share in 2026 due to widespread adoption in urban and suburban households. Ease of installation, operational efficiency, and cost reduction benefits support high uptake. Systems are compatible with existing hot water and space heating infrastructure, reducing retrofitting complexity and shortening installation timelines. Consumers benefit from predictable energy savings and lower utility bills, making adoption economically appealing. Provider recommendations are reinforced by system reliability, minimal maintenance requirements, and long service life.

Industrial heating is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by integration in process heating, boiler pre-heating, and chemical manufacturing applications. High thermal demand and long operational hours make solar thermal solutions attractive for cost reduction and environmental compliance. Providers recognize potential for measurable energy savings and return on investment, motivating adoption. Integration with automated and digital energy management systems enables predictive monitoring, performance optimization, and data-driven operational decisions.

Regional Insights

North America Non-Concentrating Solar Collectors Market Trends

North America exhibits strong market potential for non-concentrating solar collectors due to widespread adoption in commercial, institutional, and residential heating applications. Government programs and regulatory incentives prioritize renewable heat technologies as part of broader energy efficiency and decarbonization strategies. Building codes mandate performance standards for new construction, prompting developers to incorporate thermal solutions into water heating and space conditioning systems.

Industrial sectors, including food processing, chemical manufacturing, and institutional facilities, demonstrate growing demand for low-temperature process heat, where non-concentrating collectors provide predictable output and operational reliability.

Market growth is reinforced by increasing interest in hybrid energy solutions that combine solar thermal collectors with heat pumps, thermal storage, and building automation systems. Strategic partnerships between technology providers, utilities, and end users support pilot installations and demonstration projects, generating operational data and validating performance claims. Workforce training and certification programs improve installer competency, reducing performance variability and ensuring system reliability. Digital performance analytics enable predictive maintenance and energy cost tracking, facilitating decision-making for large-scale installations.

Europe Non-Concentrating Solar Collectors Market Trends

Europe is forecasted to be the fastest-growing market for non-concentrating solar collectors between 2026 and 2033, stimulated by policy frameworks that link renewable heat adoption to enforceable decarburization targets and building energy performance standards. Regulatory mechanisms, including energy performance certificates for commercial and residential structures, create measurable incentives for developers and owners to reduce heat demand intensity, prioritizing low-temperature thermal solutions with predictable output under varying climate conditions. National climate commitments drive reductions in fossil fuel use for space and water heating, encouraging procurement teams to integrate solar thermal solutions in long-term energy planning.

Growth trajectory benefits from an integrated ecosystem connecting technology developers, capital providers, and end users through performance-based incentives and risk mitigation strategies. Performance guarantees verified by third parties reduce uncertainty for institutional buyers managing distributed energy systems. Research programs fund pilot deployments that integrate collectors with heat pumps, stratified thermal storage, and predictive control, generating data that strengthens underwriting standards and operational benchmarks.

Standardized components and interoperability protocols streamline supply chains, allowing rapid scaling without compromising quality. Workforce development initiatives enhance installer competency in hydraulic balancing and sensor calibration, ensuring field performance aligns with modeled outcomes.

Asia Pacific Non-Concentrating Solar Collectors Market Trends

Asia Pacific is expected to lead with an estimated 40% of the non-concentrating solar collectors market value in 2026, supported by deep industrial capacity, targeted renewable heat strategies, and integrated supply chains that lower unit costs. Robust manufacturing ecosystems in the region enable production of key components at scale, reducing lead times and enabling competitive pricing relative to alternative solutions. China recorded sustained expansion of thermal collector deployment through utility and commercial programs that emphasize energy intensity reduction.

India implemented national renewable heating targets that align public and private investment toward distributed heat systems, accelerating adoption in large urban centers. Japanese markets benefit from structured collaboration between industrial heat users and technology providers, driving tailored solutions for commercial applications.

Market dominance in the region is underpinned by a convergence of demand drivers that extend beyond macroeconomic growth. Large-scale infrastructure investments and diversified energy portfolios create pull from utility and district heating projects that favor non-concentrating solutions for low-temperature applications. Cost structures in several markets reflect integrated logistics and local content requirements that strengthen competitive positioning relative to imports.

Private capital flows into deployment partnerships with technology providers, enabling risk sharing on performance guarantees and financing arrangements that improve project economics. Education and certification programs for installers enhance quality assurance and reduce performance variability in field operations, which boosts confidence among corporate and institutional buyers.

Competitive Landscape

The global non-concentrating solar collectors market exhibits a moderately fragmented structure, with leading players accounting for 40–50% of total revenue. Key companies such as Viessmann, Solahart, Bosch Thermotechnik, Prosunpro, and Vaillant Group shape competitive dynamics through diversified product portfolios and strong distribution networks. Market influence derives from a combination of technological expertise, operational reliability, and established brand recognition. Advanced absorber designs, selective coatings, and durable construction allow companies to deliver consistent thermal performance across residential, commercial, and industrial applications.

Competitive positioning emphasizes differentiation through technological innovation, system integration, and service capabilities. Viessmann leverages advanced control systems and digital monitoring to optimize energy output, while Solahart focuses on modular designs and turnkey solutions tailored for residential and small commercial installations. Bosch Thermotechnik deploys scalable manufacturing and component standardization to ensure cost-effective reliability. Prosunpro integrates intelligent monitoring systems with predictive maintenance features, enhancing operational transparency for large-scale users.

Key Industry Developments

- In February 2026, Naked Energy launched VirtuMAX, a ground-mounted evacuated-tube solar thermal system designed to deliver high-performance renewable heat for industrial sites and district heating networks. Its tubular design uses up to 85% of ground area for energy generation, improves structural durability and accessibility, and supports decarbonization of industrial heat.

- In December 2025, China introduced a policy roadmap to accelerate solar thermal power deployment, targeting 15 GW of installed capacity by 2030. The plan aims to build a globally competitive industry with domestically developed technologies, while declining costs are expected to bring solar thermal generation closer to parity with coal power.

Companies Covered in Non-Concentrating Solar Collectors Market

- Viessmann

- Solahart

- Bosch Thermotechnik

- Prosunpro

- Vaillant Group

- Dimas SA

- XNE Group

- Greenonetec

Frequently Asked Questions

The global non-concentrating solar collectors market is projected to reach US$ 19.3 billion in 2026.

Rising demand for renewable heating, government incentives, and increasing adoption in residential and commercial buildings are driving the market.

The market is poised to witness a CAGR of 14.3% from 2026 to 2033.

Expansion in emerging economies, integration with smart building systems, and demand for sustainable district heating present key market opportunities.

Some of the key market players include Viessmann, Solahart, Bosch Thermotechnik, Prosunpro, Vaillant Group, and Dimas SA.