- Renewable Energy

- Solar Backsheet Market

Solar Backsheet Market Size, Share, and Growth Forecast, 2025 - 2032

Solar Backsheet Market by Category (Fluoropolymer, Non-fluoropolymer), Mounting Type (Ground Mounted, Roof Mounted, Top-of-pole Mounted, Side-of-pole Mounted, Tracking System Mounted), Application (Residential, Commercial, Industrial, Others), and Regional Analysis for 2025 - 2032

Solar Backsheet Market Size and Trend Analysis

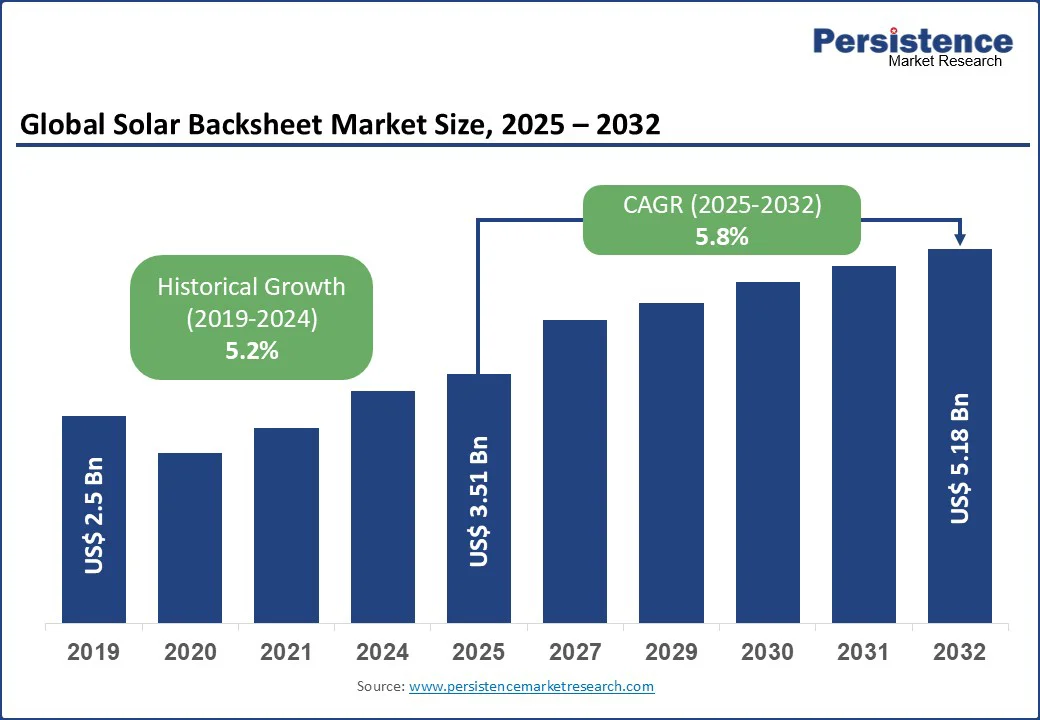

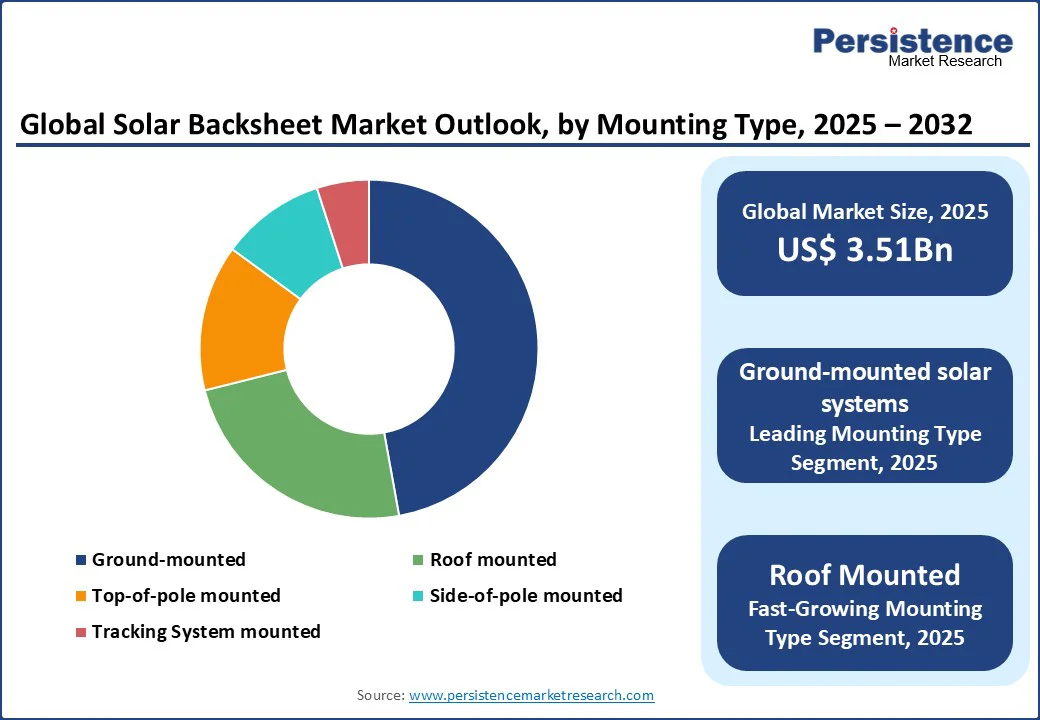

The global solar backsheet market size is likely to value at US$3.51 Bn in 2025 and reach US$5.18 Bn by 2032, growing at a CAGR of 5.8% during the forecast period from 2025 to 2032.

The solar backsheet market is experiencing robust growth, driven by the increasing adoption of solar energy, advancements in photovoltaic (PV) technology, and the rising demand for durable, high-performance materials in solar panel manufacturing. Solar backsheets, critical for protecting PV modules from environmental factors such as UV radiation, moisture, and temperature fluctuations, are essential for ensuring the longevity and efficiency of solar panels. The surge in renewable energy investments, supportive government policies, and the global push for sustainable energy solutions are key factors propelling market expansion.

Key Industry Highlights:

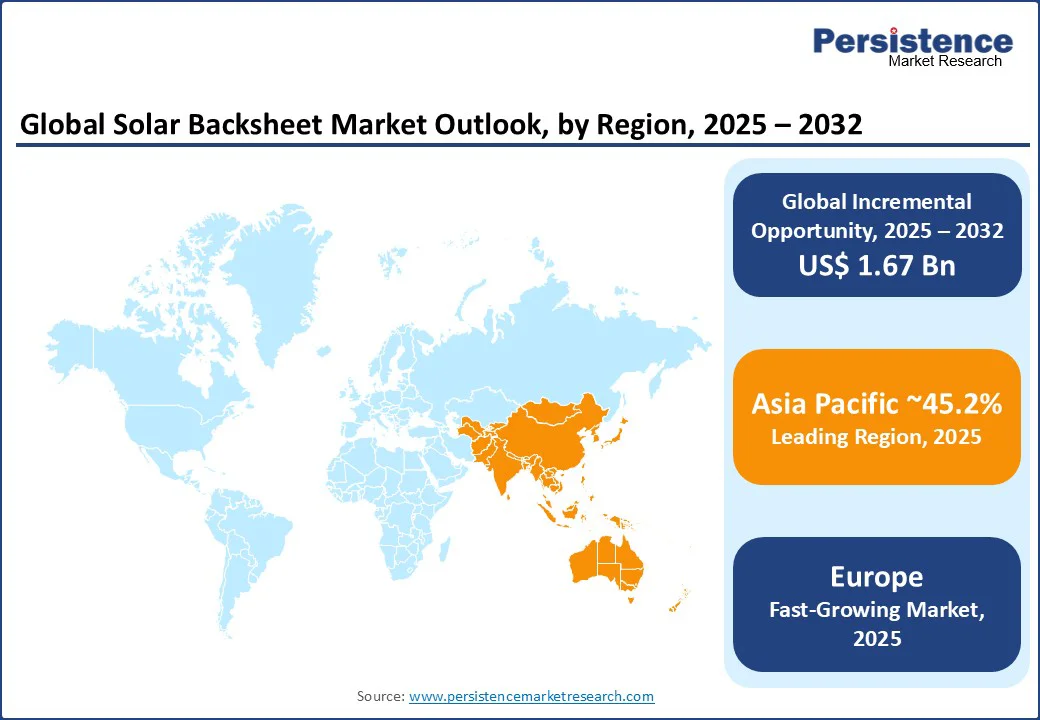

- Leading Region: Asia Pacific holds a 45.2% market share in 2025, driven by massive solar energy adoption, large-scale manufacturing, and supportive policies in countries such as China and India.

- Fastest-growing Region: Europe is the fastest-growing region, fueled by ambitious renewable energy targets, stringent environmental regulations, and increasing solar installations in Germany and Spain.

- Investment Plans: According to the International Energy Agency (IEA), State Grid Corporation of China plans to invest USD?350?billion between 2021 and 2025 to transform and upgrade the national power grid. The emphasis is on enhancing grid flexibility, enabling renewable integration, and modernizing infrastructure, boosting demand for high-quality solar backsheets in utility-scale projects.

- Dominant Category: Fluoropolymer backsheets account for 59.8% of the market share in 2025, owing to their superior durability, UV resistance, and suitability for harsh environments.

- Leading Application: Commercial applications contribute over 42.7% of market revenue, driven by the growing installation of solar panels in commercial buildings and solar farms.

|

Global Market Attribute |

Key Insights |

|

Solar Backsheet Market Size (2025E) |

US$ 3.51Bn |

|

Market Value Forecast (2032F) |

US$ 5.18Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics

Driver - Surging Demand for Solar Energy and Renewable Energy Investments

The global solar backsheet market is witnessing significant growth due to the rising demand for solar energy and substantial investments in renewable energy projects. Solar backsheets play a critical role in protecting PV modules, ensuring their efficiency and durability over 25–30 years. According to the International Renewable Energy Agency (IRENA), global solar photovoltaic capacity is expected to reach 2,840 GW by 2030, driven by supportive policies and declining solar panel costs.

In the Asia Pacific, China’s push for carbon neutrality by 2060 and India’s target of 500 GW renewable energy capacity by 2030 are driving large-scale solar installations, increasing demand for high-quality backsheets. In Europe, the EU’s REPowerEU plan aims to install 600 GW of solar capacity by 2030, further boosting demand. Companies such as DuPont and Coveme SpA are expanding production to meet the growing need for durable, weather-resistant backsheets, ensuring sustained market growth through 2032.

Restraint - High Production Costs and Competition from Alternative Materials

The solar backsheet market faces challenges due to high production costs and competition from alternative materials. Fluoropolymer-based backsheets, while durable, are expensive to manufacture due to the high cost of raw materials such as polyvinyl fluoride (PVF) and polyvinylidene fluoride (PVDF). In 2023, fluctuations in fluoropolymer prices increased production costs, impacting profitability for manufacturers, particularly smaller players.

Additionally, non-fluoropolymer backsheets, such as those made from polyethylene terephthalate (PET), are gaining traction due to their lower cost, posing a competitive threat. Limited standardization in backsheet quality across regions and concerns over long-term durability in extreme climates further hinder adoption in cost-sensitive markets. These factors create pricing pressures and restrain overall market growth, particularly in emerging economies.

Opportunity - Advancements in Backsheet Technology and Recycling Initiatives

The growing focus on sustainable solar technologies and recycling initiatives presents significant opportunities. Innovations in backsheet materials, such as enhanced fluoropolymer composites and eco-friendly non-fluoropolymer alternatives, are improving durability and reducing environmental impact. By 2050, the total value of materials recovered from end-of-life PV panels could exceed USD?15?billion, assuming a 30-year panel lifespan and proper recycling systems in place, encouraging manufacturers to develop recyclable backsheets.

Companies such as Arkema SA and Krempel GmbH are investing in R&D to create high-performance, recyclable backsheets for next-generation PV modules. Additionally, government incentives, such as the EU’s Circular Economy Action Plan, promote sustainable manufacturing practices, creating opportunities for manufacturers to align with green trends. The rising demand for lightweight, cost-effective backsheets in emerging markets such as India and Brazil further supports market expansion through 2032.

Category-wise Insights

By Category

- Fluoropolymer backsheets dominate the market, holding a 59.8% share in 2025, due to their exceptional durability, UV resistance, and moisture barrier properties. These backsheets, primarily made from PVF or PVDF, are widely used in utility-scale and commercial solar projects, where long-term reliability is critical. Companies such as DuPont (Tedlar PVF) and Coveme SpA lead with extensive portfolios, catering to demand in regions such as the Asia Pacific and Europe, where large-scale solar installations are prevalent.

- Non-fluoropolymer backsheets are the fastest-growing segment, driven by their cost-effectiveness and increasing adoption in residential and small-scale solar projects. Made from materials such as PET, these backsheets offer a balance of performance and affordability, appealing to cost-sensitive markets in South Asia and Latin America. Manufacturers such as Toyo Aluminium KK are innovating to enhance the weather resistance of non-fluoropolymer backsheets, supporting their rapid growth.

By Mounting Type

- Ground-mounted solar systems account for the largest market share, contributing over 47.3% of revenue in 2025, driven by their widespread use in utility-scale solar farms. These systems require robust backsheets to withstand prolonged environmental exposure. Companies such as Isovoltaic AG and 3M Co. supply high-performance backsheets for ground-mounted installations, particularly in China and the U.S., where large solar projects are expanding rapidly.

- Roof-mounted solar systems are the fastest-growing segment, fueled by increasing residential and commercial solar adoption. Roof-mounted installations benefit from lightweight, durable backsheets that ensure long-term performance in diverse climates. Manufacturers such as Madico Inc. and Taiflex Scientific Co., Ltd are focusing on flexible, high-efficiency backsheets to meet the growing demand in Europe and North America, where rooftop solar is gaining traction.

By Application

- The commercial sector dominates the solar backsheet market, contributing 42.7% of revenue in 2025, driven by the rapid installation of solar panels in commercial buildings, warehouses, and solar farms. High-performance backsheets are critical for ensuring the durability of PV modules in large-scale projects. Companies such as DuPont and Arkema SA cater to this segment with advanced fluoropolymer backsheets, particularly in the Asia Pacific and North America.

- The residential sector is the fastest-growing application, propelled by increasing homeowner adoption of solar energy and supportive government incentives. Residential solar installations require cost-effective, durable backsheets to ensure long-term performance. Manufacturers such as Targray Technology International Inc. and Krempel GmbH are developing affordable, high-quality backsheets to meet the rising demand in emerging markets such as India and Brazil.

Regional Insights

Asia Pacific Solar Backsheet Market Trends

The Asia Pacific dominates the solar backsheet market, holding a 45.2% share in 2025, driven by rapid solar energy adoption, large-scale manufacturing, and supportive government policies in China and India. China, the world’s largest solar market, according to IRENA, by the end of 2024, China accounted for over 50% of the world’s operational photovoltaic (PV) capacity, boosting demand for high-quality backsheets. The region’s robust supply chain and low-cost manufacturing, led by companies such as Toyo Aluminium KK and Taiflex Scientific Co. Ltd, ensure its market leadership. Rising investments in renewable energy and government-led initiatives further solidify Asia Pacific’s dominance through 2032.

Europe Solar Backsheet Market Trends

Europe is the fastest-growing region, driven by ambitious renewable energy targets, stringent environmental regulations, and increasing solar installations in Germany and Spain. The EU aims to bring online over 320?GW of solar PV capacity by 2025, and almost 600?GW by 2030, boosting demand for high-performance backsheets. According to the German Solar Association (BSW-Solar), the sector achieved a turnover of approximately €30 billion in 2024, driven by over 1 million new solar installations and around 575,000 battery storage systems. It relies on fluoropolymer backsheets for durability in utility-scale projects. Companies such as Isovoltaic AG and Coveme SpA dominate with innovative, eco-friendly backsheets, catering to the region’s focus on sustainability. Europe’s emphasis on green technologies and regulatory compliance drives rapid market growth.

North America Solar Backsheet Market Trends

North America is the second fastest-growing region, propelled by strong demand from the U.S. and Canada’s solar and renewable energy sectors. The U.S. solar market drives demand for durable backsheets in ground-mounted and commercial installations. Canada’s renewable energy policies support solar growth, particularly in rooftop applications. Major players such as DuPont and 3M Co. lead with extensive distribution networks, catering to large-scale projects. Consumer preference for high-quality, long-lasting backsheets and increasing investments in solar infrastructure strengthen North America’s market position through 2032.

Competitive Landscape

The global solar backsheet market is highly competitive, characterized by a mix of global giants and regional manufacturers. Leading players such as DuPont, Isovoltaic AG, and Coveme SpA dominate through innovative product portfolios and extensive global distribution networks.

The market is fragmented, with regional players such as Toyo Aluminium KK and Taiflex Scientific Co. Ltd focusing on localized offerings in the Asia Pacific. Companies are investing in advanced manufacturing technologies and sustainable materials to enhance market share, driven by demand for high-performance backsheets in commercial and utility-scale solar projects.

Key Industry Developments

- April 2025: DuPont showcased its Tedlar PVF film solutions at the International Signage Association (ISA) Expo 2025 in Las Vegas. Tedlar films offer extended lifespans ranging from 12 to over 20 years, depending on the specific demands of each application. DuPont featured a variety of protective overlaminate films designed to safeguard graphics against fading, graffiti, harsh cleaners, dirt and grime build-up, and mold and mildew growth.

- July 2024: Coveme SpA introduced dyMat ECO, a sustainable non-fluoropolymer backsheet with improved weather resistance, targeting residential and commercial rooftop installations in North America and Europe. dyMat ECO products are UL registered and certified by TUV Rheinland and TÜV SÜD, meeting international standards for safety and quality.

Companies Covered in Solar Backsheet Market

- DuPont de Nemours Inc.

- Isovoltaic AG

- Coveme SpA

- Arkema SA

- 3M Co.

- Toyo Aluminium KK

- Madico Inc.

- Taiflex Scientific Co. Ltd

- Krempel GmbH

- Targray Technology International Inc.

- Others

Frequently Asked Questions

The solar backsheet market is projected to reach US$3.51 Bn in 2025.

Growing demand for solar energy and renewable energy investments are the key market drivers.

The solar backsheet market is poised to witness a CAGR of 5.8% from 2025 to 2032.

Advancements in backsheet technology and recycling initiatives are the key market opportunities.

DuPont de Nemours Inc., Isovoltaic AG, Coveme SpA, and Arkema SA are key market players.