- Specialty & Fine Chemicals

- Rubber Anti-Tack Agents Market

Rubber Anti-Tack Agents Market Size, Share, and Growth Forecast, 2025 - 2032

Rubber Anti-Tack Agents Market By Product Type (Fatty Acid Esters, Fatty Acid Amides, Stearates, Soap, Silicone Polymers, Others), Applications (Rubber (Molded Products, Extruded Products, Others), Tire), Form (Powder, Liquid), Regional Analysis for 2025 - 2032

Rubber Anti-Tack Agents Market Size and Trend Analysis

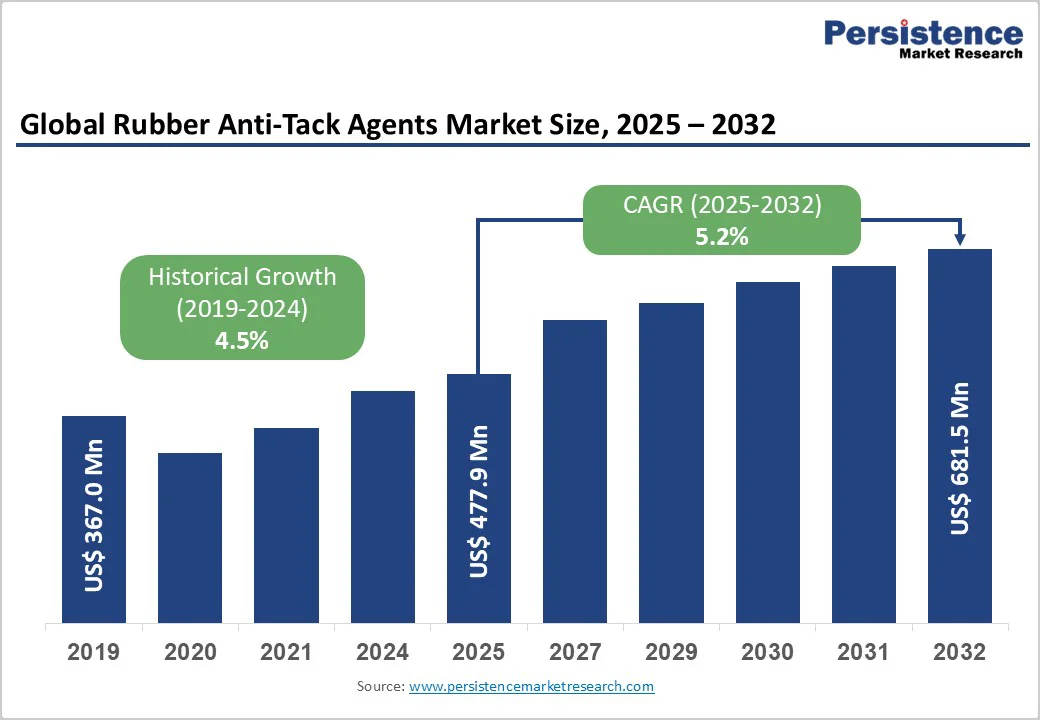

The global rubber anti-tack agents market size is likely to be valued at US$477.9 Million in 2025 and is expected to reach US$681.5 Million by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032, driven by accelerating tire manufacturing expansion and the rising adoption of electric vehicles (EVs) requiring specialized rubber compounds with enhanced processing efficiency.

The automotive industry produced 74.6 million vehicles in 2024, a 2.5% YoY increase, boosting demand for anti-tack agents used in tires and rubber components. Manufacturers are focusing on quality upgrades and eco-friendly formulations that deliver better lubrication and non-stick performance, ensuring consistent product quality and efficient production.

Key Industry Highlights

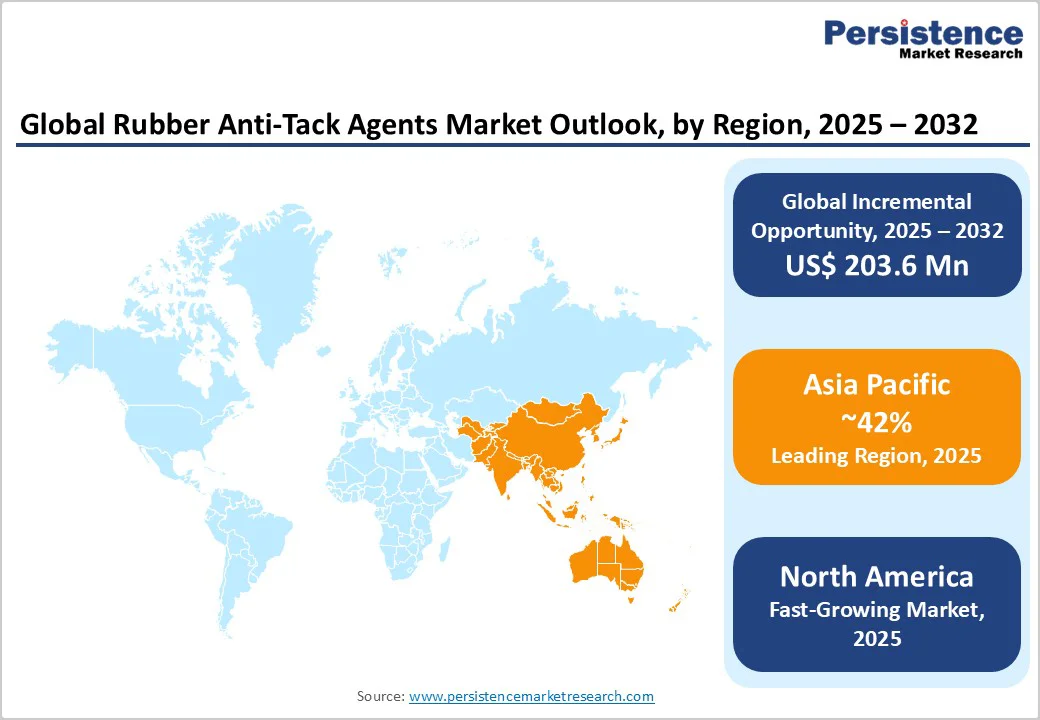

- Leading Region: Asia Pacific dominates the rubber anti-tack agents market with over 42% share in 2025, driven by massive tire and rubber manufacturing bases in China, India, and Southeast Asia.

- Fastest-Growing Region: North America holds a substantial market position with around 27% share in 2025, supported by advanced infrastructure, strict regulations, and established supply chains across tire and industrial rubber applications.

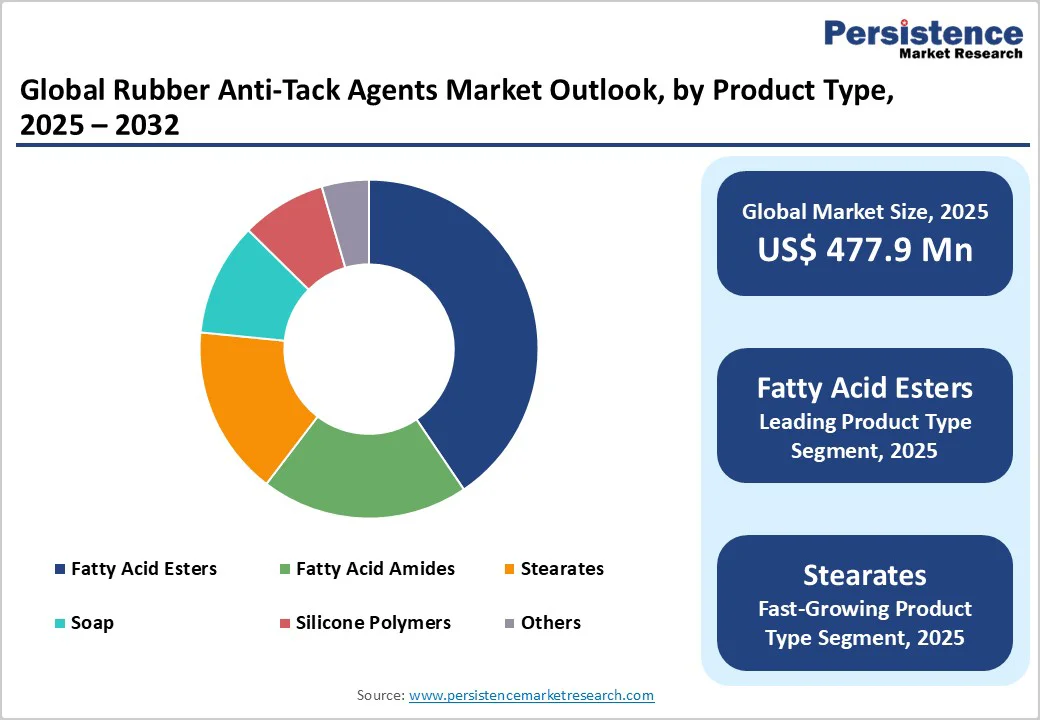

- Leading Category: Fatty acid esters lead the product category with approximately 28% market share, offering superior compatibility, sustainability, and processing efficiency across natural and synthetic rubber types.

- Fastest-Growing Category: Tire manufacturing remains the largest and fastest-growing application segment, propelled by rising global tire production, EV tire innovations, and advanced formulation requirements.

- Key Market Opportunity: Eco-friendly and bio-based formulations emerge as the key growth opportunity, with growing environmental regulations and sustainability goals driving the shift toward low-VOC, non-toxic, renewable anti-tack solutions.

| Key Insights | Details |

|---|---|

| Rubber Anti-Tack Agents Market Size (2025E) | US$477.9 Million |

| Market Value Forecast (2032F) | US$681.5 Million |

| Projected Growth CAGR (2025 - 2032) | 5.2% |

| Historical Market Growth (2019 - 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Tire Manufacturing Expansion and Rising Vehicle Production

Global tire output surpassed 2.4 billion units in 2024, fueled by surging vehicle production, especially in Asia Pacific, which accounts for over 60% of global tire manufacturing. China alone produced more than 940 million tires, while India’s production exceeded 180 million units, reflecting a strong downstream demand for anti-tack agents used in calendering and extrusion. These additives play a crucial role in ensuring uniform compound flow, reducing scrap generation, and maintaining operational efficiency.

The rapid penetration of EVs, expected to reach one in every five new vehicles by 2030, is reshaping tire design with higher torque, load-bearing, and temperature stability needs. Consequently, tire manufacturers are adopting specialized anti-tack solutions capable of withstanding advanced polymer blends and high thermal cycles during EV tire production.

Growing Adoption of Eco-Friendly and High-Performance Formulations

The transition toward sustainable and water-based anti-tack agents is accelerating, with over 70% of new product introductions in 2023 - 2024 emphasizing bio-based or non-toxic formulations. Regulatory bodies such as REACH (EU) and the U.S. EPA have tightened restrictions on solvent-based and zinc-stearate agents, compelling manufacturers to invest in greener alternatives. These eco-friendly agents reduce VOC emissions by up to 60%, improve workplace air quality, and align with corporate carbon-reduction goals.

Innovations in silicone-emulsion and fatty-acid derivative systems have enhanced rubber surface uniformity and reduced downtime caused by contamination or buildup. Leading producers are leveraging biodegradable emulsifiers and hybrid dispersions that improve mold release efficiency by 15-20%, demonstrating how sustainability and performance are converging to redefine the next generation of rubber anti-tack technologies.

Barrier Analysis - Volatile Raw Material Costs and Supply Chain Disruptions

Fluctuations in petroleum-based raw materials such as fatty acids, stearates, and silicone emulsions have created significant pricing instability for anti-tack agent producers. Prices of base feedstocks such as stearic acid and paraffin wax have witnessed volatility of 25-35% between 2021 and 2024, driven by crude oil price swings and logistic constraints. Such cost unpredictability directly affects production margins and end-user pricing, particularly for mid-tier and small manufacturers lacking long-term procurement contracts.

Global logistics disruptions triggered by events such as the Red Sea crisis and container shortages have strained the supply continuity of specialty chemicals across Asia and Europe. Import-dependent markets such as India and Southeast Asia face extended lead times of six to eight weeks, impacting production planning and formulation consistency. These constraints push producers toward diversifying sourcing channels and building localized inventories to stabilize operational flows.

Regulatory Compliance Complexity and Environmental Restrictions

Evolving environmental frameworks have introduced substantial compliance hurdles for anti-tack agent producers. The EU REACH and U.S. EPA regulations now require detailed chemical registration, toxicity testing, and emission monitoring, elevating R&D and certification costs by an estimated 15-20%. Restrictions on volatile organic compounds (VOCs) and hazardous residues have compelled reformulation of conventional solvent- or stearate-based agents into safer, water-based versions, often demanding new capital investments in processing equipment.

Regulatory fragmentation across regions, such as China’s MEE Chemical Safety standards and Japan’s CSCL compliance norms, forces multinational manufacturers to maintain separate product compositions for different markets. This complexity elongates time-to-market cycles and raises documentation and testing overheads. For small and medium enterprises (SMEs), these costs can erode competitiveness, deterring innovation and slowing global product expansion efforts.

Opportunity Analysis - Expansion into Medical Devices and High-Precision Rubber Applications

The medical and healthcare sector is emerging as a high-value growth avenue for rubber anti-tack agent producers. Global demand for medical-grade rubber products such as gloves, catheters, and tubing exceeded 400 billion units in 2024, driven by hygiene awareness and hospital expansion. Anti-tack agents are vital to maintaining surface sterility, preventing contamination, and meeting ISO 10993 and USP Class VI compliance.

Rising healthcare investment across Asia, particularly in India, Vietnam, and Indonesia is fueling local medical device production. This trend creates opportunities for suppliers of aqueous, residue-free, and non-toxic formulations tailored for medical rubber. Companies developing sterile, biocompatible anti-tack systems can establish strong OEM partnerships and long-term visibility in the precision medical materials space.

Development of Application-Specific Solutions for Electric Vehicle Components

The EV sector is reshaping global rubber chemistry needs, with EV production surpassing 14 million units in 2024. This transition demands anti-tack agents compatible with high-temperature elastomers used in EV tires, seals, and gaskets. These agents must ensure low residue, superior thermal stability, and process uniformity under elevated torque and temperature conditions.

Advanced anti-tack technologies are now being co-developed with OEMs to meet EV-specific requirements such as noise reduction, lightweighting, and chemical resistance. Components such as battery enclosures and insulation layers rely on precise molding, where tailored anti-tack systems improve yield and reduce scrap by up to 15%. Such innovation positions manufacturers as strategic partners in the growing e-mobility materials ecosystem.

Category-wise Analysis

Product Type Insights

Fatty acid esters dominate the rubber anti-tack agents market, holding about 28% share in 2025. Their strong lubricating and anti-stick properties ensure smooth rubber processing with minimal surface defects.

These bio-based esters are widely preferred in tire and industrial rubber manufacturing due to their high compatibility with natural and synthetic polymers. Their renewable origin and low environmental impact align with global sustainability mandates, further strengthening adoption.

The stearate-based anti-tack agents segment is emerging as the fastest-growing category, supported by their cost-effectiveness and versatility in diverse rubber compounding applications. Their excellent dispersion ability, good mold release characteristics, and proven performance in heat-intensive environments make them an ideal choice for automotive and industrial rubber processors seeking consistent and economical anti-tack performance.

Application Type Insights

Tires represent the leading application segment in the rubber anti-tack agents market, accounting for roughly 40% share in 2025. Anti-tack agents are crucial in preventing rubber sheet adhesion during calendering, extrusion, and curing.

Their uniform coating ensures dimensional accuracy and improved production efficiency. The rising global demand for passenger and commercial vehicle tires, coupled with high replacement rates, continues to sustain robust anti-tack consumption across tire plants in Asia-Pacific and Europe.

The industrial rubber products segment, covering hoses, belts, gaskets, and molded parts, is the fastest-growing application area. Rapid industrialization, infrastructure expansion, and increased adoption of high-performance elastomer components have spurred demand for customized anti-tack formulations engineered for precision molding and enhanced surface integrity.

Form Insights

Liquid formulations lead the rubber anti-tack agents market with an estimated over 60% share in 2025. These water-based systems offer excellent handling, minimal contamination, and compatibility with automated application methods such as spraying or dipping.

Their eco-friendly profile, free from volatile organic compounds (VOCs), aligns with tightening global emission norms. Improved coverage, stability, and ease of dilution make liquid formulations the preferred choice among large-scale tire and component manufacturers.

The powder form remains the fastest-growing subcategory in niche traditional manufacturing setups, particularly where manual processes persist. Powder-based agents are valued for their ease of storage and cost-effectiveness. However, innovation in fine-particle dispersion and hybrid coatings is helping extend their utility in selected low-moisture and high-friction rubber production lines.

Regional Insights

North America Rubber Anti-Tack Agents Trends

North America holds a substantial position in the rubber anti-tack agents market, accounting for approximately 27% share in 2025. The region benefits from advanced tire manufacturing capabilities, stringent occupational safety standards, and strong automotive OEM and replacement markets.

The U.S. leads regional demand, supported by well-established production hubs of premium tire manufacturers and consistent replacement cycles. Strict regulations by the U.S. Environmental Protection Agency (EPA) and OSHA have accelerated the transition toward low-VOC, water-based anti-tack formulations designed to meet environmental and workplace safety norms.

Innovation and sustainability remain the foundation of market growth in the region. Ongoing R&D investments by specialty chemical producers and adoption of automation technologies in rubber compounding have fostered the development of next-generation anti-tack agents compatible with modern, high-speed production systems. Expanding EV manufacturing and medical-grade rubber processing segments further strengthen North America’s role as a leader in product innovation and value-added applications.

Europe Rubber Anti-Tack Agents Trends

Europe’s rubber anti-tack agents market demonstrates steady growth, underpinned by strict environmental compliance and mature rubber manufacturing infrastructure. The EU’s REACH regulation continues to shape chemical formulation standards, driving the transition toward sustainable and biodegradable anti-tack agents. Germany leads regional demand due to its strong automotive and tire manufacturing sectors, while France, Spain, and the U.K. contribute significantly through industrial rubber component production.

European manufacturers are actively investing in R&D to create renewable, non-toxic anti-tack formulations that align with the region’s circular economy goals. The adoption of specialized solutions for high-performance, low-rolling-resistance tires, especially for EV and hybrid models, remains a key growth factor. The region’s strong regulatory harmonization and commitment to sustainability ensure consistent, though moderate, market expansion through the forecast period.

Asia Pacific Rubber Anti-Tack Agents Trends

Asia Pacific dominates the rubber anti-tack agents market, accounting for over 42% share in 2025. The region’s leadership stems from extensive tire and rubber manufacturing bases in China, India, and Southeast Asia, which collectively serve both domestic and export demand.

Massive investments in production infrastructure, expanding automotive output, and technological advancements in rubber compounding have positioned Asia-Pacific as the global hub for anti-tack consumption. China’s large-scale industrial base and India’s rapidly growing automotive manufacturing sector further reinforce the region’s strong market presence.

Rapid industrialization, cost competitiveness, and continuous capacity expansion across ASEAN economies such as Thailand, Indonesia, and Vietnam have attracted major specialty chemical producers. Government initiatives supporting sustainable manufacturing and eco-friendly formulations are accelerating the adoption of green anti-tack solutions. The region’s dominance is expected to continue as manufacturers prioritize renewable-based, waterborne formulations aligned with stricter environmental standards.

Competitive Landscape

The global rubber anti-tack agents market is moderately consolidated, featuring a mix of global specialty chemical producers and regional manufacturers competing through product innovation, technical expertise, and tailored customer solutions.

Competition centers on formulation performance, eco-friendly product development, and strong distribution networks that ensure reliable supply and application-specific compatibility across industries such as tire, automotive, and industrial rubber manufacturing.

Leading players focus on advancing sustainable, water-based, and low-emission formulations to comply with evolving environmental standards. Regional manufacturers, particularly in emerging markets, gain ground through localized production and cost-efficient solutions. Continuous R&D investments, technological upgrades, and strategic collaborations define the competitive direction of the market.

Key Industry Developments

- In November 2024, Polymer Solutions Group Expands Product Portfolio. Polymer Solutions Group strengthened its global market position through strategic product line expansion and technology integration across its SASCO Chemical and Alkon Solutions subsidiaries, enhancing competitive capabilities in specialized rubber additive formulations.

- In August 2024, LANXESS Advances Sustainability Initiatives LANXESS AG reported significant progress on environmental compliance and sustainable product development, with its Advanced Intermediates and Specialty Additives segments recording particularly strong growth, reflecting market demand for eco-friendly anti-tack solutions.

- In June 2024, Croda International launched sustainable Anti-Tack Formulations. Croda International introduced innovative bio-based anti-tack agent formulations derived from renewable sources, addressing market demand for sustainable rubber additives meeting stringent environmental standards and regulatory requirements.

Companies Covered in Rubber Anti-Tack Agents Market

- Polymer Solutions Group (SASCO)

- H. L. Blachford

- Lanxess

- Kettlitz-Chemie

- Barbe Group

- Lion Specialty Chemicals

- Struktol, King Industries

- Ocean Chemical

- PT Sejahtera Mitra Lestari

- Tianjin Xiongguan

- Fujian Anyuan

- Wisdom Chemical

- Croda International

- FACI SPA

- Baerlocher

- Evonik Industries

Frequently Asked Questions

The rubber anti-tack agents market is projected to reach US$681.5 Million by 2032, growing from US$477.9 Million in 2025 at a CAGR of 5.2%.

Key drivers include rising tire production, EV expansion, automotive growth, and the adoption of eco-friendly high-performance formulations.

Fatty acid esters lead the market with around 28% share in 2025, driven by superior lubricity and eco-friendly compatibility.

Asia Pacific dominates the market with over 42% share in 2025, led by massive tire and automotive manufacturing capacity.

Opportunities lie in EV tires, medical devices, eco-friendly formulations, and high-precision rubber applications.

Major players include Polymer Solutions Group, Lanxess, Croda, Evonik, Kettlitz-Chemie, Struktol, King Industries, Blachford, and Lion.