- Specialty & Fine Chemicals

- Nitrile Butadiene Rubber (NBR) Foam Products Market

Nitrile Butadiene Rubber (NBR) Foam Products Market Size, Share, and Growth Forecast, 2026-2033

Nitrile Butadiene Rubber (NBR) Foam Products Market by Product Type (Closed-Cell NBR Foam, Open-Cell NBR Foam, Composite Laminated Foams, Molded NBR Foam Components), Application (Thermal Insulation, Sealing, Acoustic Dampening, Mechanical Cushioning), End-Use (Automotive, Industrial, Construction, Others), and Regional Analysis for 2026-2033

Nitrile Butadiene Rubber (NBR) Foam Products Market Share and Trends Analysis

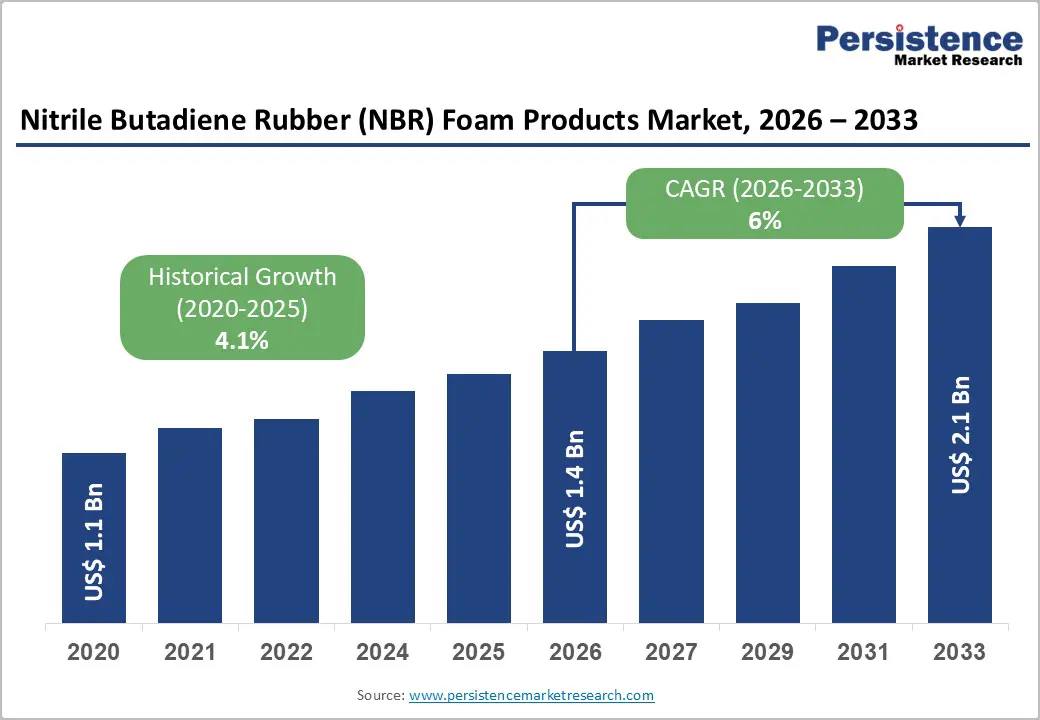

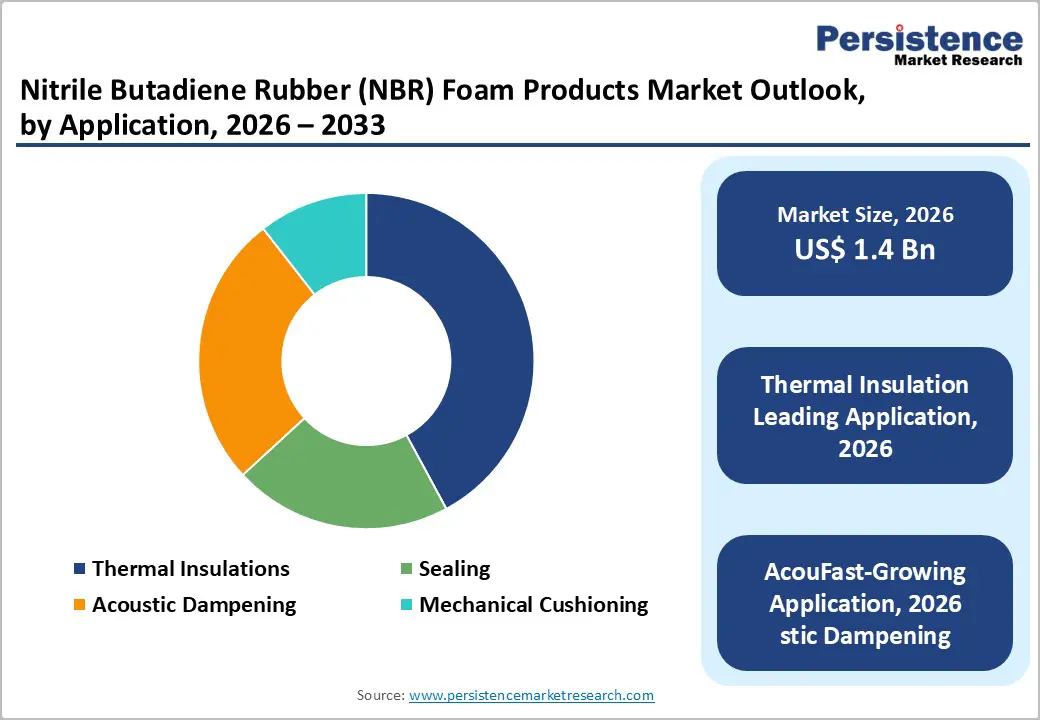

The global nitrile butadiene rubber (NBR) foam products market size is likely to be valued at US$ 1.4 billion in 2026, and is projected to reach US$2.1 billion by 2033, growing at a CAGR of 6% during the forecast period 2026 – 2033.

Market expansion is primarily driven by Asia-Pacific’s leadership in industrial and manufacturing activities, which supports strong demand for NBR and NBR foam products. The rapid growth of automotive and electric vehicle (EV) sectors is increasing the need for high-performance sealing, thermal insulation, and acoustic dampening solutions. The construction and heating, ventilation, & air-conditioning (HVAC) industries are adopting NBR foam for energy-efficient insulation and enhanced comfort. Industrial applications, including machinery and factory automation, are also contributing to rising consumption. Furthermore, technological advancements in composite laminated and molded foam components are enabling more versatile, customized solutions, while regulatory emphasis on energy efficiency and noise control strengthens long-term market adoption.

Key Industry Highlights

- Leading Applications: Thermal insulation is expected to lead with the largest share of about 40% in 2026, while acoustic dampening is projected as the fastest-growing 2026-2033 application at roughly 6.8% CAGR, owing to heightening demand for construction noise-control.

- Dominant Product Types: Closed-cell NBR foam is set to command around 50% revenue share in 2026, while composite laminated and molded foam components are likely to grow the fastest through 2033, driven by high-performance and customization requirements.

- Leading End-Uses: Automotive is slated to hold around 45% revenue share in 2026, while industrial is likely to grow the fastest from 2026 to 2033, fueled by machinery, factory automation, and infrastructure expansion.

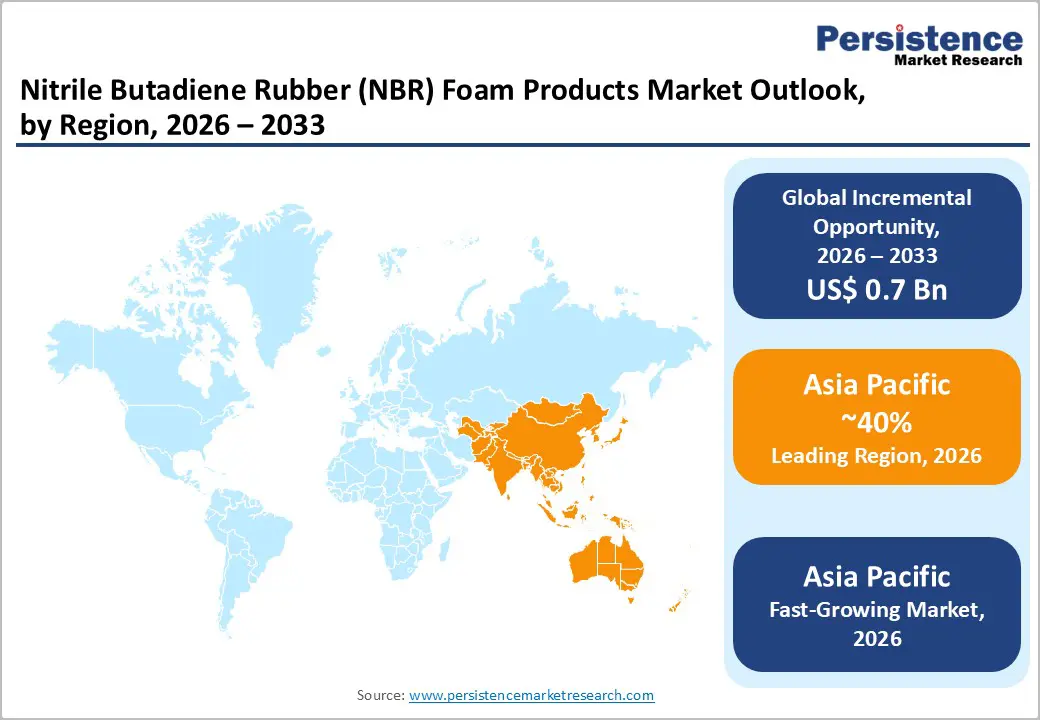

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 40% share in 2026, with North America representing a mature market with stable demand and the Europe market being driven by regulatory-compliant, high-performance adoption.

- Strategic Focus: Sustainability initiatives and EV-specific foam innovations are supporting premium adoption across automotive and industrial sectors, charting the growth trajectory of the market.

| Key Insights | Details |

|---|---|

| Nitrile Butadiene Rubber (NBR) Foam Products Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Automotive Production and Electrification Demand

Global automotive production continues to rise, with electric and hybrid vehicle adoption accelerating demand for advanced sealing, thermal insulation, and acoustic materials. In 2025, the International Energy Agency (IEA) reported that global electric car sales surpassed 17 million in 2024, aided by increased manufacturing capacity in key markets including China, the U.S., and Europe. Manufacturers are prioritizing materials that improve battery thermal management, noise reduction, and lightweight insulation, boosting demand for elastomeric foam products. Demand is not limited to EVs; conventional vehicle production remains robust, maintaining baseline demand for high-performance insulation and sealing materials.

Policy initiatives in multiple regions are amplifying this effect. The U.S. Environmental Protection Agency (EPA) has strengthened emission and fuel efficiency standards, encouraging adoption of innovative materials that support lighter, energy efficient vehicles. Meanwhile, Europe Union (EU)’s Green Deal transport strategies emphasize emissions reduction and sustainable supply chains, which create incentives for original equipment manufacturers (OEMs) to source advanced, compliant materials. As global vehicle production targets continue to rise, manufacturers increasingly integrate materials that offer improved performance without adding significant weight, positioning foam products as essential components of both conventional and next generation vehicles.

Regulatory Emphasis on Energy Efficiency and Comfort Requirements

Worldwide regulatory initiatives are tightening standards for energy efficiency in buildings and mechanical systems, directly influencing material demand. In the United States, the updated building energy codes effective January 2026 require higher thermal performance for insulation and HVAC systems in both new construction and retrofits, driving adoption of advanced insulating materials. Similarly, the EU’s Energy Performance of Buildings Directive (EPBD) reinforces improved building envelope standards and carbon reduction goals, increasing demand for materials that deliver effective thermal insulation and moisture resistance.

Concurrently, global noise regulations in automotive, aerospace, and industrial machinery are becoming more stringent, prompting manufacturers to adopt materials that enhance acoustic dampening without compromising other performance metrics. For example, updated noise control guidelines in several European markets require lower cabin and equipment sound levels, which elevates demand for effective acoustic insulation. Across commercial construction and transportation sectors, the intersection of energy efficiency mandates, indoor comfort standards, and performance expectations is creating sustained, measurable demand for products that provide combined thermal and acoustic benefits.

Regulatory Push for Energy Efficiency and High Performance Insulation

Global regulatory emphasis on energy performance in construction and infrastructure is creating significant opportunities for advanced foam materials with high thermal efficiency. For example, Japan’s Ministry of Land, Infrastructure, Transport and Tourism introduced stricter insulation requirements for new residential buildings beginning in 2026, supporting broader adoption of higher performance insulation materials that can meet tighter U value standards. In the United States, updated energy codes effective in 2026 require improved thermal performance for building envelopes and HVAC systems, aligning with sustainability goals and reducing energy consumption. These policies are lifting demand for materials that enhance heat retention and moisture resistance across commercial and residential sectors.

Such regulatory momentum also stimulates retrofitting markets, as existing building stock is upgraded to comply with newer codes. Incentive programs linked to energy savings and carbon reduction goals are making capital investments in high efficiency insulation more financially attractive. This trend spans developed and emerging markets where energy costs and sustainability targets are central to urban planning. Together, these regulatory movements broaden the addressable market for advanced foam products that combine thermal, acoustic, and moisture control capabilities, setting the stage for long term growth as codes evolve and enforcement intensifies.

Innovation in EV and Mobility Related Insulation Materials

Technological innovation in mobility materials is opening new opportunities for foam products that address thermal management and safety requirements in electric vehicles and energy storage systems. In July 2025, a major polymer manufacturer launched an advanced flame retardant encapsulation foam designed to limit thermal propagation in EV battery cells, directly addressing emerging safety standards in battery safety regulations.(turn0search0) These developments signal how materials innovation is increasingly critical to fulfilling regulatory and performance requirements in next generation vehicles. As OEMs pursue lighter, safer, and more efficient EV designs, demand grows for insulation materials that deliver multi functional performance.

The broader insulation market, including thermal and acoustic materials, is benefiting from trends in green building and industrial energy efficiency initiatives. Governments and industry stakeholders are promoting eco friendly and high performance materials in retrofits and new construction, supported by incentive programs and regulatory mandates that prioritize reduced energy consumption. These converging trends, mobility innovation, sustainability mandates, and heightened performance expectations, provide a fertile environment for foam manufacturers to expand into electric mobility, advanced infrastructure, and high efficiency insulation solutions, unlocking incremental market value downstream.

Category-wise Analysis

Product Type Insights

Closed cell NBR is set to command around 50% of the nitrile butadiene rubber foam products market revenue share in 2026 due to its strong moisture resistance, thermal insulation, and mechanical stability. These properties make it ideal for automotive sealing, HVAC insulation, and industrial vibration control where long term durability and energy performance are critical. Closed cell foams are increasingly specified in high temperature applications and harsh environments where material reliability is essential. This widespread adoption supports stable demand across transportation and construction sectors. Their non porous structure also provides superior moisture barriers, reducing degradation over time.

Composite laminated and molded NBR foam components are the fastest growing product type, projected at a 7.5% CAGR through 2033. Growth is propelled by the rise in multifunctional components tailored for electric vehicles, next generation industrial machinery, and premium HVAC systems. For example, automotive acoustic and thermal insulation solutions combining multiple foam layers are becoming part of EV interior modules, improving noise control and temperature management without adding weight, a trend highlighted by expanding global EV insulation supply initiatives in 2025 that focus on lightweight, high efficiency interior materials. Advances in molding and lamination technology further drive adoption by enabling custom shapes with integrated performance features.

Application Insights

Thermal insulation is expected to remain the leading application, expected to hold roughly 45% of the nitrile butadiene rubber foam products market share in 2026, supported by stringent energy efficiency requirements and performance demands in buildings, industrial systems, and vehicles alike. In automotive and EV segments, advanced thermal insulation materials are being developed to protect battery packs and power electronics, enhancing battery life and safety as detailed by global insulation market developments in 2025 that highlight expanded EV insulation offerings designed for high temperature stability. In construction and HVAC sectors, evolving energy codes and sustainability initiatives are bolstering the use of high performance insulation solutions that minimize heat transfer, reduce operating costs, and improve overall energy efficiency.

The acoustic dampening is projected to expand at a 6.8% CAGR through 2033, particularly in automotive and aerospace sectors where passenger comfort and regulatory noise limits drive demand for acoustic solutions. Recent industry trends show manufacturers integrating multi layer acoustic systems and advanced foam based materials to achieve superior sound absorption without compromising weight or performance — a trend that aligns with broader consumer and regulatory emphasis on quieter interior environments in vehicles and aircraft cabins. Additionally, structural and machinery applications are increasingly specifying acoustic insulation to meet stricter vibration and noise standards in industrial equipment.

Regional Insights

Asia Pacific Nitrile Butadiene Rubber (NBR) Foam Products Market Trends

Asia Pacific is expected to hold over 40% of NBR foam products market share in 2026, anchored by robust automotive production, infrastructure growth, and industrial expansion. Government policies in countries such as Japan are mandating stronger insulation performance standards starting in 2026, driving broader uptake of thermally efficient materials in buildings and industrial systems. Rapid urban development in India and Southeast Asia has also spiked the demand for construction and HVAC insulation products that balance energy efficiency with durability. Regional manufacturers are also investing in automation and precision fabrication to improve quality and reduce production costs.

Industry leaders in India’s polyurethane (PU) and foam sector called for updated government standards and policy support in late 2025, highlighting opportunities in sustainable materials and cold storage insulation solutions. This type of policy engagement strengthens the alignment between material innovation and infrastructure requirements, encouraging local companies to scale advanced foam solutions. These regulatory momentum and industry collaboration reinforce Asia Pacific’s strategic role in shaping global NBR foam use cases across automotive, construction, and industrial markets, sustaining demand well into the forecast period.

North America Nitrile Butadiene Rubber (NBR) Foam Products Market Trends

North America is anticipated to account for approximately 30% of the nitrile butadiene rubber foam products market value in 2026. Continued investment in energy efficient construction and industrial systems is driving advanced insulation adoption in commercial and residential sectors. In the U.S., new building efficiency standards taking effect in 2026 are expected to expand demand for higher performance thermal materials that improve HVAC system efficiency and reduce operating emissions. This regulatory push reinforces the use of advanced insulation solutions that meet both sustainability and building code requirements.

At the same time, accelerating commercial electric vehicle adoption is calling for enhanced insulation and thermal management materials, particularly in battery and cabin systems. For instance, the push for EV electrification in heavy duty vehicles, including new electric truck launches planned for 2026, underscores the importance of effective thermal and acoustic materials in next generation transportation. Such trends are expanding application diversity beyond traditional sectors, making North America a strategic hub for premium foam integration in both infrastructural and mobility solutions.

Europe Nitrile Butadiene Rubber (NBR) Foam Products Market Trends

Europe is a strategically significant regional market for NBR foam products, projected to contribute around 25% of global demand in 2026, propelled by strong regulatory frameworks for energy efficiency, emissions reduction, and material performance. Harmonized EU energy performance codes and fire safety mandates continue to elevate the adoption of high performance insulation materials in building retrofit and new construction projects. In France, Germany, and the U.K., such regulations are paired with incentives that support energy efficient upgrades, further embedding advanced thermal solutions into mainstream material choices.

European policy activity in late 2025 has also focused on vehicle lifecycle and circularity standards, including provisional agreements to boost recycling and reuse throughout vehicle manufacturing and end of life management. These initiatives raise the importance of materials capable of supporting circular economy objectives, where insulation, damping, and component recyclability become competitive differentiators. Despite shifts in EV policy debates, European suppliers continue emphasizing certified, high performance materials for both automotive and infrastructure sectors, reinforcing the region’s role as a key market for premium NBR foam product development.

Competitive Landscape

The global nitrile butadiene rubber foam products market structure is moderately consolidated, with BASF, Zotefoams, Sekisui Chemical, Recticel, and Armacell collectively accounting for over 50% of global revenue. These companies leverage strong OEM relationships, advanced manufacturing capabilities, and expertise in thermal, acoustic, and sealing solutions across automotive, construction, and industrial sectors. Heavy investment in R&D allows these leaders to maintain technological differentiation through innovations in composite laminated foams, molded components, and multi-layer noise, vibration, & harshness (NVH) solutions. Sustainability, energy efficiency, and EV-specific foam applications are also central to their product strategies.

Meanwhile, regional and niche competitors, including Kaneka Corporation, JSP Corporation, and Chongqing Yuli Chemical, focus on specialized applications and local market strengths. Barriers such as high raw material costs, compliance with global standards, such as ASTM International, and production complexity limit new entrants. However, digital manufacturing, automated fabrication, and customized solution capabilities are enabling smaller firms to capture niche opportunities. Market consolidation is expected to increase gradually, driven by mergers and acquisitions, strategic partnerships, and collaborations with tier 1 suppliers to expand both geographic reach and technological offerings.

Key Industry Developments

- In February 2026, Rogers Corporation reported strong full-year results, with improved margins and optimized operating structures. This performance enables continued investment in elastomeric and advanced foam solutions for automotive, industrial, and specialty applications, strengthening their market position.

- In November 2025, Zotefoams plc completed the acquisition of Spanish foam producer OKC for € 36 million, expanding its industrial and specialty foam capabilities. The deal provides earnings accretion through operational integration and broadens the company’s European market footprint.

- In March 2025, Armacell introduced ArmaFlex ECO550, a water-based, solvent-free adhesive range designed to improve efficiency, safety, and sustainability in insulation applications, requiring only one-third the quantity of conventional adhesives while delivering comparable bonding performance.

Companies Covered in Nitrile Butadiene Rubber (NBR) Foam Products Market

- Armacell

- Ridderflex

- W. Köpp

- RG Rom Gummi

- Fostek Corporation

- Kaimann GmbH

- L’isolante K-Flex

- Huamei Energy-Saving

- Aeroflex

- NMC

Frequently Asked Questions

The global NBR foam products market is projected to reach US$ 1.4 billion in 2026.

Rising automotive and EV production, growth in construction and HVAC, and expanding industrial applications are acting as key market drivers.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Opportunities exist in EV-specific foam solutions, advanced multi-layer composites, and high-performance thermal and acoustic insulation.

BASF, Zotefoams, Sekisui Chemical, Recticel, and Armacell are some of the leading market participants.