- Plastics, Polymers & Resins

- Plastic-Rubber Composite Market

Plastic-Rubber Composite Market Size, Share, and Growth Forecast 2026 - 2033

Plastic-Rubber Composite Market by Product Type (Thermoplastic Elastomers, Ethylene Propylene Diene Monomer, Rubber-Modified Plastics, Over-molded or Insert-molded Composites, Others), End-use Industry (Automotive, Consumer Goods, Construction, Electrical and Electronics, Healthcare, Industrial, Other), and Regional Analysis for 2026 - 2033

Plastic-Rubber Composite Market Size and Trend Analysis

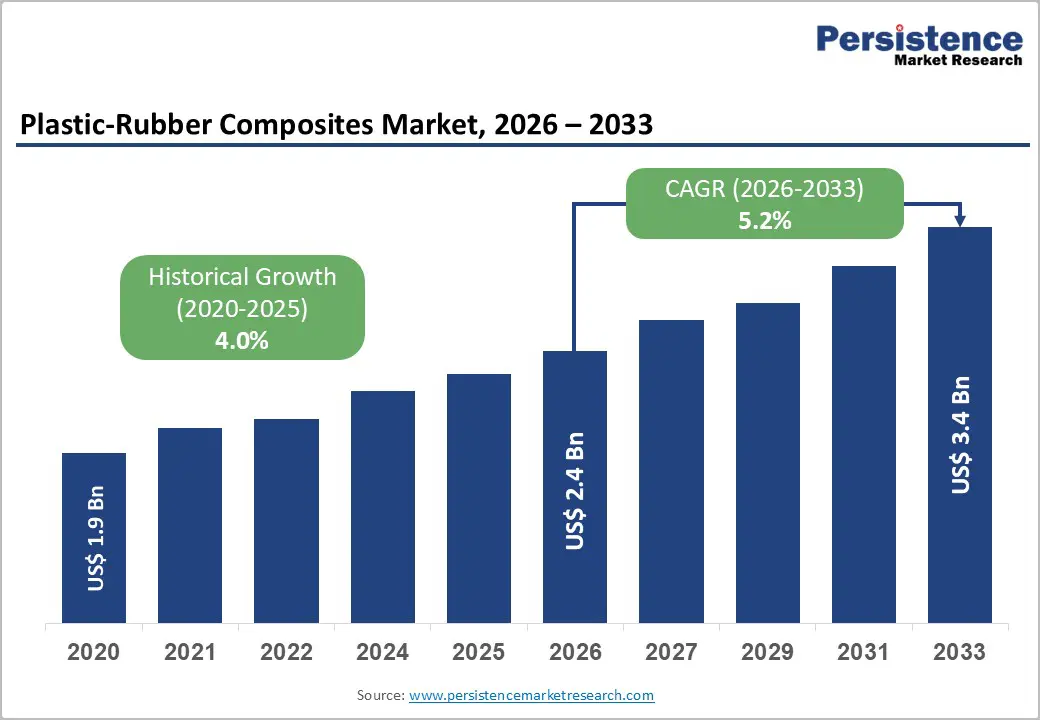

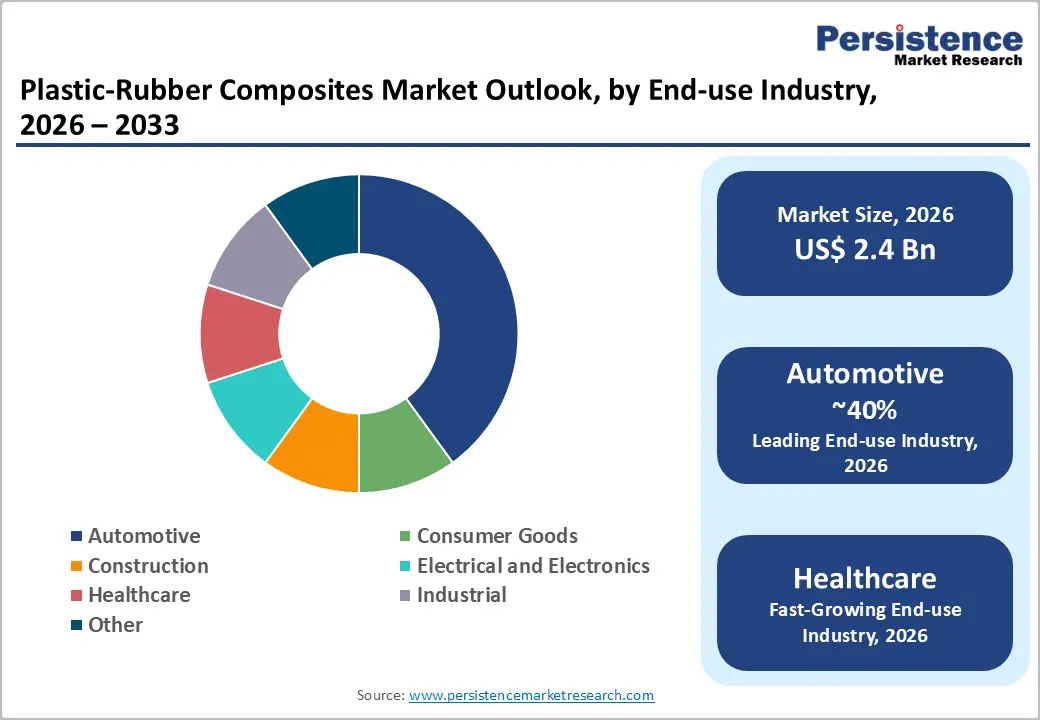

The global plastic-rubber composite market size is valued at US$ 2.4 billion in 2026 and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The market’s expansion is fundamentally driven by rising demand for lightweight, durable, and recyclable materials across automotive, construction, and healthcare sectors. Increasing global adoption of electric vehicles has further intensified the need for advanced polymer composites capable of delivering superior weight reduction, thermal stability, and mechanical performance. Concurrently, tightening regulatory standards, such as the EU End-of-Life Vehicle Regulation (ELVR) and U.S. Corporate Average Fuel Economy (CAFE) requirements, are compelling manufacturers to transition from conventional metals to high-performance plastic-rubber composites.

Key Industry Highlights:

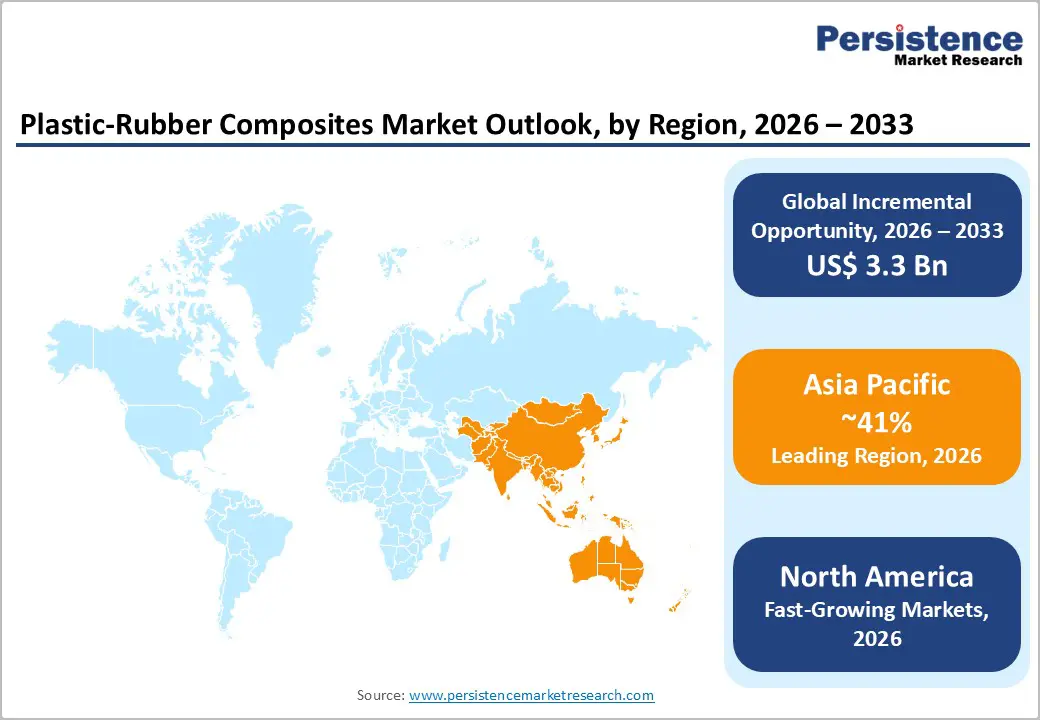

- Leading Region: Asia Pacific dominates the Plastic-Rubber Composite market, with 41% market share, driven by China's position as the world's largest EV market with 11 million EVs sold in 2024, alongside robust automotive and construction sectors across Japan, India, and ASEAN economies.

- Fastest Growing Region: North America is the fastest growing region in the market due to the region’s mature automotive industry, which is undergoing a rapid transition toward electric and autonomous vehicles, significantly increasing demand for high-performance polymer composites.

- Dominant Product Segment: Thermoplastic Elastomers (TPEs) lead the Plastic-Rubber Composite market with 38% revenue share, favored for their recyclability, design flexibility, and superior performance in automotive seals, medical devices, and consumer goods applications globally.

- Fastest Growing Product Segment: The Healthcare segment is among the fastest-growing end-use categories, driven by aging global demographics, rising medical device demand, and expanding approvals of biocompatible TPE and TPU grades for catheters, tubing, and implantable device applications.

- Key Opportunity: Bio-based and circular plastic-rubber composites represent the foremost strategic opportunity, fueled by the EU's ESPR regulation (effective July 2024), OEM mandates for recycled-content materials, and verified low-carbon product certifications such as ISCC PLUS.

| Key Insights | Details |

|---|---|

| Plastic-Rubber Composite Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.0% |

Market Dynamics

Drivers - Automotive Lightweighting and Electric Vehicle (EV) Surge

The automotive sector’s strategic transition toward electrification and enhanced fuel efficiency remains the principal catalyst for growth in the Plastic-Rubber Composite market. Global electric vehicle adoption has accelerated rapidly, with sales rising by 25% in 2024 to reach 17.6 million units and capturing a 20% share of new vehicle sales. As electric vehicles impose substantial battery-related weight burdens, automakers are increasingly replacing conventional metal components with advanced plastic-rubber composites to achieve meaningful weight reduction while maintaining structural performance.

Materials including Thermoplastic Elastomers (TPEs), Thermoplastic Vulcanizates (TPVs), and EPDM-based composites are now widely integrated into seals, gaskets, bumpers, cable sheathing, and under-hood systems. Furthermore, regulatory frameworks such as U.S. CAFE fuel-efficiency standards and the European Union’s CO- emission limits for passenger vehicles continue to reinforce the long-term imperative for lightweight composite adoption.

Expanding Applications in Construction and Infrastructure

Rapid urbanization across both emerging and advanced economies is substantially increasing demand for plastic-rubber composites within the construction and infrastructure sectors. These materials are prized for their long-term weatherability, UV resistance, chemical stability, and durability, attributes essential for modern sealing systems, roofing membranes, weatherstripping, and vibration-damping applications. According to projections by the United Nations Department of Economic and Social Affairs, approximately 68% of the global population will reside in urban areas by 2050, thereby intensifying worldwide construction activity.

EPDM-based composites are particularly prominent in building profiles and flat roofing systems due to their superior weather resistance and service lifespans exceeding 30 years. Additionally, initiatives promoting energy-efficient green buildings, such as the EU Green Deal and LEED certification programs, continue to accelerate the adoption of advanced composite sealing and insulation solutions.

Restraints - Volatility in Raw Material Prices

A major constraint on the Plastic-Rubber Composite market is the continued volatility of petrochemical-derived raw material prices, including propylene, ethylene, and specialty diene monomers. These fluctuations stem from crude oil price instability, geopolitical disruptions, and supply chain limitations, all of which directly affect polymer feedstock costs, as reported by the U.S. Energy Information Administration for the 2022-2024 period.

Resulting cost uncertainties reduce manufacturer margins and complicate long-term pricing agreements, particularly for small and mid-sized producers lacking hedging capabilities. This challenge is especially pronounced in highly price-competitive segments such as rubber-modified plastics for consumer goods.

Environmental and Regulatory Compliance Costs

Increasingly stringent chemical safety regulations, particularly the European Union’s REACH framework and associated Substances of Very High Concern (SVHC) restrictions, are imposing substantial compliance burdens on plastic-rubber composite manufacturers. These requirements necessitate continuous monitoring, detailed documentation, and material reformulation to ensure regulatory conformity.

The revised Classification, Labelling and Packaging (CLP) Regulation, implemented in 2024, has further increased procedural and formulation complexities. As a result, companies must allocate significant resources to R&D, toxicological assessment, and cross-border compliance management. These obligations are especially challenging for specialty composite producers operating in multiple jurisdictions, ultimately constraining overall market expansion.

Opportunities - Rise of Bio-Based and Sustainable Composite Solutions

The growing global emphasis on sustainability is generating significant opportunities for manufacturers developing bio-based plastic-rubber composites. Emerging regulatory frameworks, most notably the EU Ecodesign for Sustainable Products Regulation (ESPR), effective from July 2024, and forthcoming Digital Product Passport (DPP) requirements, are intensifying demand for materials with verifiable circular characteristics.

Dow Inc.’s introduction of NORDEL™ REN EPDM at the German Rubber Conference (DKT) 2024, a bio-based EPDM produced through an ISCC PLUS-certified mass-balance process that delivers a 39% reduction in carbon footprint compared with conventional EPDM. Consumer awareness of sustainable products has increased by 70% globally over the past five years, underscoring the market’s momentum. Manufacturers accelerating the commercialization of bio-attributed, chemically recycled, or mass-balance-certified composites are well-positioned to secure premium pricing, preferred OEM partnerships, and regulatory advantages in the forecast period.

Healthcare and Medical Device Applications

The healthcare sector represents a rapidly expanding, high-value growth avenue for plastic-rubber composites, driven by rising global medical device demand and aging population trends. According to the World Health Organization, the global population aged 60 years and above is expected to reach 2.1 billion by 2050, reinforcing sustained expansion in medical device manufacturing. Thermoplastic elastomers are increasingly utilized in catheters, syringe plungers, respiratory tubing, and implantable devices due to their biocompatibility, sterilization compatibility, and superior design flexibility over natural rubber.

Regulatory approvals under U.S. FDA 21 CFR 177.2600 and ISO 10993-1 biocompatibility standards are further supporting clinical adoption. Medical-grade TPU solutions from companies such as Covestro AG, including Desmopan® and Texin® portfolios, are increasingly specified for critical care applications.

Category-wise Analysis

Product Type Insights

Thermoplastic Elastomers (TPEs) hold a leading position in the Plastic-Rubber Composite market, accounting for an estimated 38% share of global revenue. Their dominance is attributed to the unique combination of rubber-like elasticity and thermoplastic processability, which supports efficient recycling, shorter production cycles, and seamless compatibility with standard injection-molding and extrusion systems. The automotive industry remains the principal end-use sector, utilizing TPEs in exterior filler panels, wipers, rocker panels, body seals, gaskets, door and window handles, and vibration-damping components.

Thermoplastic Vulcanizates (TPVs), primarily EPDM/polypropylene blends, represent the largest sub-segment due to their heat resistance, oil resistance, and ability to recycle production scrap. Growing sustainability imperatives are also increasing the adoption of bio-based TPE grades. Regulatory guidance from the U.S. EPA and the European Chemicals Agency is further accelerating the transition away from PVC-based materials, reinforcing TPEs’ market leadership through 2033.

Industry Insights

The automotive sector remains the leading end-use industry in the Plastic-Rubber Composite market, accounting for approximately 40% of total revenue. This dominance aligns with broader thermoplastic elastomer utilization trends, where automotive applications consistently generate the highest revenues. The industry’s reliance on lightweight materials continues to strengthen as OEMs adopt composite solutions to comply with U.S. CAFE fuel-efficiency regulations and the European Union’s CO- emission reduction standards.

Plastic-rubber composites are widely specified for seals, cable sheathing, under-hood systems, weather strips, and vibration-damping components. The accelerating global transition to electric vehicles, highlighted by 17.6 million EV sales in 2024, further amplifies demand, as EV platforms require higher composite content to offset battery-related mass. Continued growth in automotive manufacturing employment and capital investment reinforces production capacity, directly increasing TPE and EPDM composite integration across global vehicle programs.

Regional Insights

North America Plastic-Rubber Composite Market Trends

North America remains one of the most technologically advanced and regulation-driven markets for plastic-rubber composites, with the United States serving as its central hub. The region’s mature automotive industry is undergoing a rapid transition toward electric and autonomous vehicles, significantly increasing demand for high-performance polymer composites. According to the U.S. Energy Information Administration, electric car sales reached 1.6 million units in 2024, accounting for more than 10% of new vehicle sales and accelerating OEM adoption of lightweight composite components.

North America’s robust innovation landscape is supported by major companies such as BASF SE, Dow Inc., DuPont de Nemours, Inc., and Celanese Corporation, all investing in bio-based and recyclable composite technologies. Additionally, LANXESS AG’s 2025 expansion of rubber processing promoter production in South Carolina underscores the region’s strategic importance for capacity growth. Strong aftermarket demand for automotive interior plastics further amplifies regional momentum.

Europe Plastic-Rubber Composite Market Trends

Europe’s Plastic-Rubber Composite market is shaped by a stringent regulatory environment, strong sustainability ambitions, and long-established leadership in specialty polymers. Major demand originates from Germany, France, Italy, and the United Kingdom, supported by high-volume automotive manufacturing and advanced chemical industry clusters. Regulations such as the EU REACH framework and the Ecodesign for Sustainable Products Regulation (ESPR), effective July 2024, are driving manufacturers to adopt safer, more sustainable chemistries, thereby accelerating demand for bio-based and recyclable composite materials.

Eurostat reports that the EU achieved a €238-billion trade surplus in chemicals and related products in 2024, highlighting its competitiveness in specialty materials. BASF SE’s polyamide recycling technologies presented at K-2025 and Covestro AG’s investments in mechanically recycled polycarbonates further demonstrate Europe’s commitment to circular material innovation and regulatory alignment.

Asia Pacific Plastic-Rubber Composite Market Trends

Asia Pacific represents the largest regional market for plastic-rubber composites, with 41% market share, supported by a strong manufacturing base, rapidly expanding automotive production, and sustained urbanization across major economies. China remains the principal growth engine, recording 11-million electric vehicle sales in 2024 and accounting for 60% of the global EV market, a trend that is driving substantial demand for lightweight EPDM seals, TPE gaskets, and over-molded composite components.

India and ASEAN markets are emerging as high-growth hubs, strengthened by industrial policy incentives and increasing foreign direct investment in automotive and chemical sectors. Japan continues to exert considerable technological influence through leading companies such as Mitsui Chemicals, Toray Industries, and Teijin Limited. Covestro AG’s investment of over EUR-27-million in new recycled polycarbonate capacity further underscores the region’s rapid material innovation. Supported by accelerating construction activity, Asia Pacific is projected to achieve the highest CAGR through 2033.

Competitive Landscape

The global plastic-rubber composite market exhibits moderate consolidation, led by major chemical conglomerates such as BASF SE, Dow Inc., DuPont de Nemours, Inc., SABIC, and Covestro AG. These companies maintain substantial market influence through expansive product portfolios, proprietary composite technologies, and globally integrated manufacturing networks. Competitive differentiation is increasingly driven by investment in bio-based and circular composite materials, capacity expansion across high-growth regions, and strategic collaborations with automotive OEMs. Emerging business models emphasize mass-balance certification, chemical recycling integration, and material-as-a-service frameworks. Concurrently, R&D priorities are shifting toward SVHC-compliant formulations, sustainable feedstock utilization, and advanced TPE grades for medical and electric vehicle applications.

Key Developments:

- October 2025: BASF SE unveiled two pioneering polyamide (PA6) recycling technologies at K 2025 in Düsseldorf, enabling closed-cycle recovery of automotive plastic waste, including depolymerization and solvent-based recycling, in pilot projects with ZF Group and Pöppelmann for Mercedes-Benz components.

- September 2025: LANXESS AG announced the expansion of rubber processing promoter production at its Bushy Park, South Carolina, USA facility, marking the first time LANXESS will produce processing promoters in the United States, to meet rising demand and improve North American supply reliability.

- July 2024: Dow Inc. launched NORDEL™ REN EPDM at the German Rubber Conference (DKT) 2024, a bio-based EPDM produced via an ISCC PLUS-certified mass balance system, offering a 39% lower carbon footprint versus conventional EPDM grades for automotive and construction composite applications.

Top Companies in the Plastic-Rubber Composite Market

- BASF SE (Ludwigshafen, Germany) is the world's largest chemical company. Its Performance Materials division is a market leader in engineering plastics, TPEs, and rubber-plastic composite solutions across automotive, construction, and consumer goods applications. BASF's VALERAS® circular additives platform and pioneering automotive PA6 recycling technologies position it as a frontrunner in sustainable composite innovation.

- Dow Inc. (Midland, U.S.) is a leading materials science company with a comprehensive rubber and polymer composite portfolio, anchored by its NORDEL™ EPDM and SILASTIC™ Silicone product families. Committed to delivering 3 million metric tons per year of circular and renewable solutions by 2030, Dow's Advanced Molecular Catalyst technology delivers EPDM with 39% lower carbon footprint than conventional processes, making it a key innovation leader in the bio-based composite segment.

- Covestro AG (Leverkusen, Germany), a global polymer materials leader, specializes in high-performance polycarbonates and TPU composites under its Desmopan® and Texin® brands. With 46 production sites worldwide and a fully circular economy orientation, Covestro is aggressively expanding mechanically recycled polycarbonate capacity in the Asia Pacific, targeting over 60,000 tons annually by 2026, and aims for Scope 1 and 2 climate neutrality by 2035.

Companies Covered in Plastic-Rubber Composite Market

- BASF SE

- Dow Inc.

- DuPont de Nemours, Inc.

- Solvay S.A.

- Arkema S.A.

- Covestro AG

- Mitsui Chemicals, Inc.

- SABIC

- Sumitomo Chemical Co., Ltd.

- LANXESS AG

- Evonik Industries AG

- Celanese Corporation

- Toray Industries, Inc.

- Teijin Limited

- LyondellBasell Industries N.V.

Frequently Asked Questions

The global Plastic-Rubber Composite market is valued at US$ 2.4 Bn in 2026 and is projected to reach US$ 3.4 Bn by 2033, expanding at a CAGR of 5.2% over the 2026-2033 forecast period. The market was valued at US$ 1.92 Bn in 2020 and grew at a historical CAGR of 4.0% between 2020 and 2025, reflecting consistent demand across automotive, construction, and healthcare end-use sectors.

The primary growth drivers are the global automotive industry's transition to electric vehicles, with 17.6 million EVs sold in 2024 per IEA data, demanding lightweight composite solutions, and rapid urbanization spurring construction sector demand. Regulatory mandates, including U.S. CAFE standards and the EU Green Deal, are further compelling OEMs and building material manufacturers to adopt durable, recyclable plastic-rubber composites to meet fuel efficiency and sustainability targets.

Thermoplastic Elastomers (TPEs) are the leading product type segment, commanding approximately 38% revenue share. Their dominance is driven by superior recyclability, design flexibility, and compatibility with standard processing equipment, making them the material of choice for automotive seals, medical device components, and consumer goods

Asia Pacific is the leading region, driven by China's dominant EV manufacturing ecosystem (11 million EVs sold in 2024 per IEA), rapid urbanization driving construction composite demand, and a formidable specialty chemical manufacturing base spanning Japan, India, South Korea, and ASEAN. The region benefits from cost-competitive production, strong government industrial policy support, and expanding foreign investment in composite material capacity.

The most significant opportunity lies in bio-based and circular plastic-rubber composites. The EU Ecodesign for Sustainable Products Regulation (ESPR) (effective July 2024) and OEM mandates for recycled-content materials are driving demand for certified sustainable composites.

The leading companies in the global Plastic-Rubber Composite market include BASF SE, Dow Inc., DuPont de Nemours, Inc., Covestro AG, Arkema S.A., LANXESS AG, SABIC, Mitsui Chemicals, Inc., Sumitomo Chemical Co., Ltd., Evonik Industries AG, Celanese Corporation, LyondellBasell Industries N.V., Toray Industries, Inc., Teijin Limited, and Solvay S.A.