- Advanced Materials

- Synthetic Rubber Market

Synthetic Rubber Market Size, Share, and Growth Forecast, 2025 - 2032

Synthetic Rubber Market By Product Type (SBR, PBR, EPDM, Others), End-user (Automotive, Industrial Manufacturing, Construction, Others), and Regional Analysis for 2025 - 2032

Synthetic Rubber Market Size and Trends Analysis

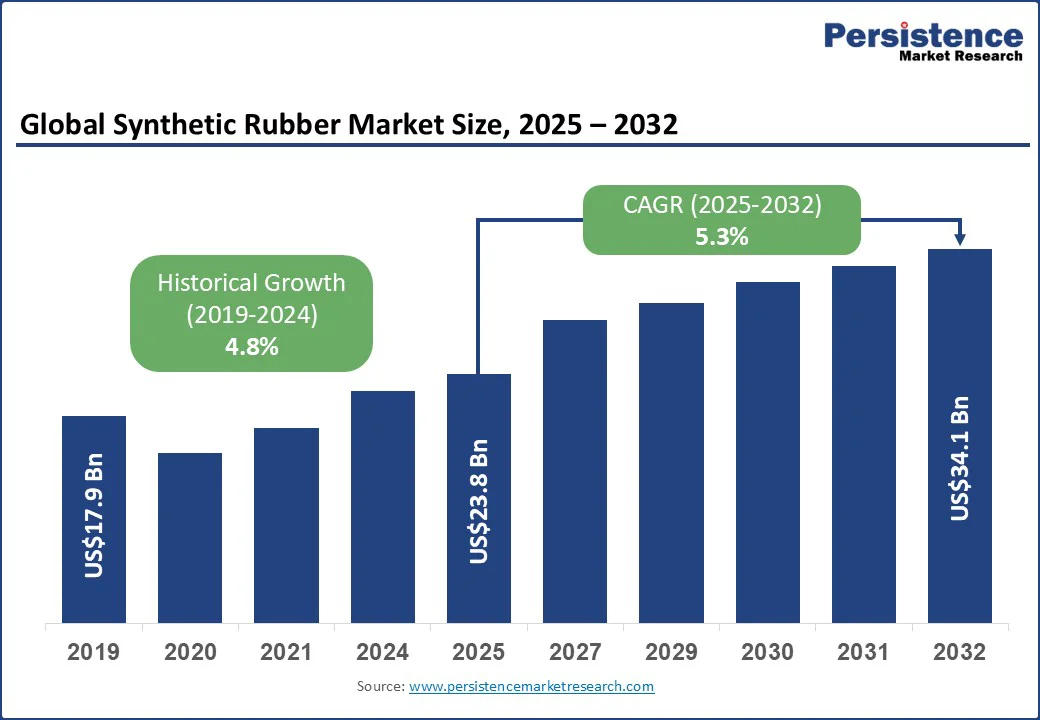

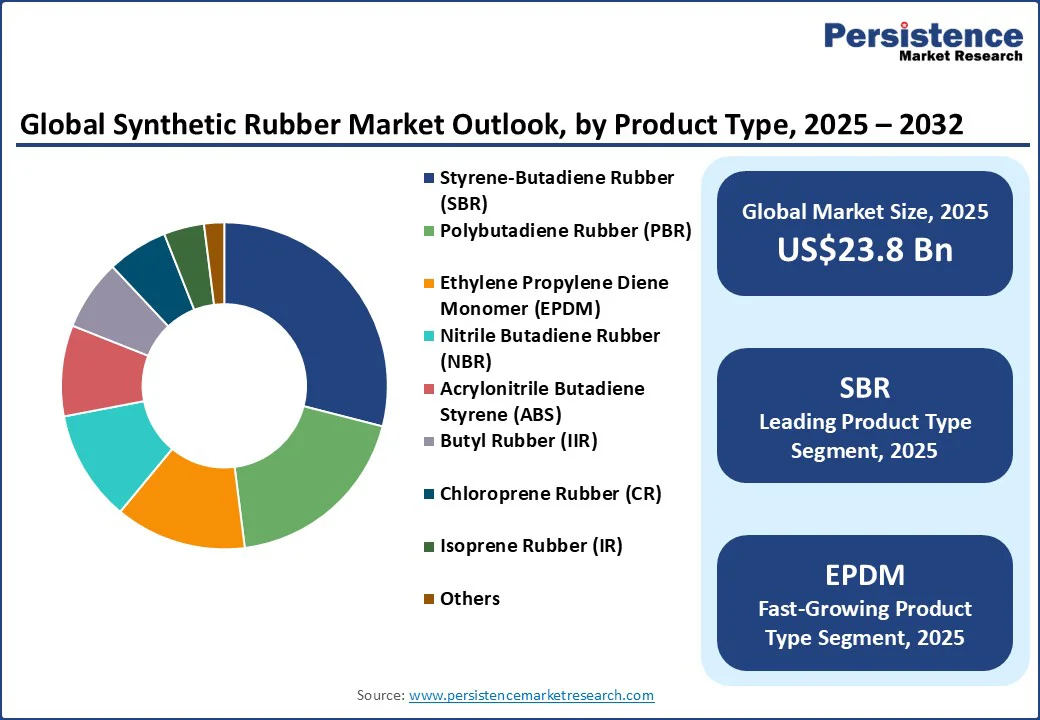

The global synthetic rubber market size is likely to be valued at US$23.8 Bn in 2025 and is expected to reach US$34.1 Bn by 2032, growing at a CAGR of 5.3% during the forecast period 2025 - 2032.

Key Industry Highlights:

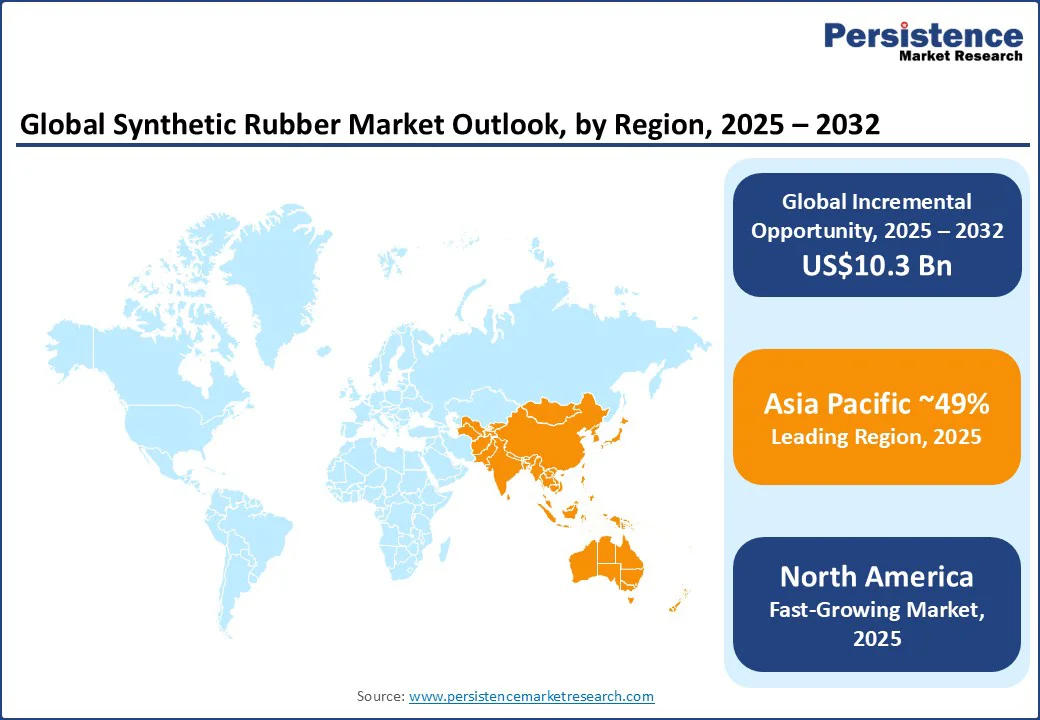

- Leading Region: Asia Pacific is expected to lead the market, accounting for approximately 49% of global revenue, driven by robust automotive production, rising EV adoption, and increasing industrial manufacturing, supported by government incentives and infrastructure investments in China, India, and Japan.

- Fastest-growing Region: North America, driven by a strong automotive sector and large-scale manufacturing; the U.S. leads with high demand for SBR and NBR in tires, seals, hoses, and gaskets, fueling its growth.

- Dominant Product Type: Styrene-Butadiene Rubber (SBR) is expected to lead the product segment with a 29% market share, driven by widespread use in tire manufacturing and automotive components, as well as advancements improving durability, performance, and environmental standards.

- Leading End-user: Automotive is projected to be the largest end-use segment, representing 36% of the market, supported by expanding passenger and commercial vehicle production, growing EV penetration, and stringent regulatory standards for fuel efficiency and safety.

| Global Market Attribute | Key Insights |

|---|---|

| Synthetic Rubber Market Size (2025E) | US$23.8 Bn |

| Market Value Forecast (2032F) | US$34.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market expansion is driven by increasing automotive production, rising demand for high-performance tires, and growth in industrial and construction applications. Regulatory mandates promoting eco-friendly and durable materials, coupled with continuous innovation in specialty rubbers and rising adoption in emerging economies, are further supporting market growth.

Automotive Demand and Material Innovation Fuel Global Synthetic Rubber Growth

The synthetic rubber market is experiencing significant growth due to the rapid expansion of the automotive sector, particularly in emerging economies. Increasing production of passenger vehicles and electric vehicles (EVs) has driven the demand for high-performance tires and durable rubber components such as seals, gaskets, and hoses.

Advances in synthetic rubber technology, including Styrene-Butadiene Rubber (SBR) and Ethylene Propylene Diene Monomer (EPDM), have enhanced wear resistance, thermal stability, and fuel efficiency, aligning with increasingly stringent safety and environmental regulations.

Rising vehicle production and government policies further reinforce this trend. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle output exceeded 92 million units in 2024, with over 50% originating from the Asia Pacific.

Initiatives such as China’s New Energy Vehicle mandate and India’s FAME program incentivize the use of advanced rubber materials in automotive applications. The European Tyre and Rubber Manufacturers’ Association (ETRMA) highlights ongoing R&D investments in sustainable synthetic rubbers, emphasizing technology-driven adoption across both mature and emerging markets.

Raw Material Volatility and Regulatory Pressures Challenge Synthetic Rubber Growth

Fluctuating crude oil prices and volatile raw material availability are significantly affecting the synthetic rubber market, as most synthetic rubbers are petroleum-based. Sudden price spikes increase production costs and create supply chain uncertainties, delaying manufacturing schedules and impacting the pricing of end products such as tires, industrial components, and medical elastomers.

Additionally, environmental regulations on chemical emissions and waste management in key regions, including Europe and North America, impose stricter compliance requirements on producers. These mandates often necessitate expensive process modifications, advanced emission control technologies, and rigorous quality testing, which can limit production flexibility and slow adoption of synthetic rubber solutions across automotive and industrial sectors.

Sustainability and Innovation Unlock Growth Opportunities in the Market

The growing focus on sustainable and eco-friendly synthetic rubbers presents a significant growth opportunity for the global market. Rising environmental awareness, combined with stricter emission regulations in developed regions, is pushing manufacturers to develop bio-based, recyclable, and low-VOC rubber products. Such innovations not only enhance environmental compliance but also improve the performance and durability of products across automotive, industrial, and healthcare sectors.

Leading manufacturers are investing heavily in green R&D, implementing digitalized production processes, and optimizing supply chains to reduce carbon footprints and energy consumption. In parallel, government initiatives, including the European Green Deal, China’s Circular Economy Promotion Law, and India’s sustainability incentives for industrial production, are creating a favorable policy environment that encourages the adoption of sustainable synthetic rubber solutions.

Collaboration between manufacturers and policymakers is further accelerating technological innovation and market penetration. This convergence of regulatory support, innovation, and growing consumer demand positions sustainable synthetic rubbers as a high-potential segment, offering long-term growth opportunities for manufacturers, suppliers, and end-users alike.

Category-wise Analysis

Technology Insights

Styrene-Butadiene Rubber (SBR), accounted for an estimated 29% revenue share, driven primarily by its extensive use in tire manufacturing and automotive components. The growing global vehicle production, coupled with rising adoption of electric vehicles, has further strengthened SBR demand, as manufacturers seek high-performance materials that enhance durability and fuel efficiency. Innovations in SBR formulations, aligned with regulatory standards for low emissions and eco-friendly materials, have reinforced its leading position across key regions.

Ethylene Propylene Diene Monomer (EPDM) is the fastest-growing product segment, with a CAGR of ~5.9%, propelled by increasing application in seals, gaskets, and roofing membranes within construction and industrial sectors. Nitrile Butadiene Rubber (NBR) and Polybutadiene Rubber (PBR) serve critical roles in oil-resistant components and high-strength industrial applications, supported by government initiatives promoting energy-efficient machinery and sustainable industrial operations.

Specialty rubbers such as Butyl Rubber (IIR), Chloroprene Rubber (CR), and Isoprene Rubber (IR) cater to niche applications in aerospace, healthcare, and chemical industries, where stringent safety and performance standards drive adoption.

Propulsion Type Insights

The automotive sector remains the largest end-user segment, capturing an estimated 36% of global revenue, driven by sustained growth in passenger and commercial vehicle production. Rising electric vehicle adoption and stringent fuel efficiency regulations have increased demand for high-performance tires, seals, and gaskets, making synthetic rubbers essential in modern automotive manufacturing. Technological advancements in materials and ongoing investments in R&D further reinforce the segment’s dominant position.

Industrial manufacturing and construction are key contributors to market expansion, collectively accounting for approximately 21% of revenue. Industrial demand is supported by synthetic rubbers’ application in hoses, belts, and machinery components, while construction relies on EPDM and other specialty rubbers for roofing, insulation, and sealing solutions.

Policy measures promoting energy-efficient manufacturing and sustainable building materials in regions such as Europe and the Asia Pacific have accelerated adoption. Niche sectors, including healthcare, aerospace, and oil & gas, though smaller in share, are witnessing steady growth due to the growing use of bio-compatible, chemical-resistant, and specialty elastomers.

Regional Insights

Asia Pacific Synthetic Rubber Market Trends - Global Pacesetter in Rooftop Solar Through Policy Support and Consumer Adoption

The Asia Pacific region is projected to dominate the market, contributing around 49% of global revenue, fueled by strong automotive production, growing EV adoption, and expanding industrial manufacturing, supported by government incentives and infrastructure development in China, India, and Japan.

China dominates, driven by its vast automotive industry and manufacturing base. In 2023, China produced over 2.5 million vehicles, boosting demand for SBR and Polybutadiene Rubber PBR used in tires. Government initiatives such as “Made in China 2025” aim to enhance domestic production and reduce import reliance, strengthening the synthetic rubber sector.

Japan’s market is growing steadily, driven by demand for high-performance rubbers and eco-friendly alternatives. Stringent environmental regulations and incentives for sustainable manufacturing promote the adoption of advanced synthetic rubbers and enhance global competitiveness.

Strong industrial demand, policy support, and technological innovation across these countries are expected to sustain the Asia Pacific’s market momentum, positioning the region as a leading contributor to the global synthetic rubber industry.

North America Synthetic Rubber Market Trends - Industrial Demand and Technological Advancement Drive the Market

The U.S. leads, driven by a strong automotive sector and high industrial demand for SBR and NBR in applications such as tires, seals, hoses, and gaskets. High demand for SBR and NBR in tires, seals, hoses, and gaskets has strengthened market growth. Recent developments include investments by major manufacturers in sustainable production and advanced rubber formulations to meet environmental standards and improve product performance.

Canada also shows steady growth, driven by industrial expansion and construction activities, with government initiatives promoting eco-friendly materials and energy-efficient manufacturing. Policies supporting innovation, safety compliance, and sustainable industrial practices further enhance the adoption of synthetic rubbers in both countries.

Technological advancements, regulatory compliance, and growing industrial and automotive demand are expected to sustain North America’s market momentum, reinforcing the region’s strategic significance within the global synthetic rubber industry.

Europe Synthetic Rubber Market Trends - Germany Leads Through Innovation and Regulatory Support

Germany leads the European synthetic rubber market, accounting for a significant revenue share due to its strong automotive and industrial manufacturing sectors. The country’s focus on advanced automotive technologies, including electric and hybrid vehicles, has fueled demand for high-performance rubbers such as SBR and NBR. In 2023, leading German manufacturers launched initiatives to enhance sustainable production, including investments in eco-friendly synthetic rubber formulations and digitalized manufacturing processes.

France, Italy, and the U.K. are key markets, supported by growing automotive production and construction activities. Policies promoting energy-efficient manufacturing, recycling, and sustainability are encouraging the adoption of eco-friendly synthetic rubbers.

Regulatory standards, such as the EU’s REACH regulations, further drive compliance and innovation in material formulations. Technological advancements, environmental regulations, and industrial demand are expected to continue shaping the European synthetic rubber market, reinforcing its strategic significance and long-term growth potential within the global industry.

Competitive Landscape

The global synthetic rubber market is highly competitive with manufacturers actively investing in innovation, sustainable production, and advanced formulations, driving healthy competition that accelerates the adoption of high-performance synthetic rubbers across automotive, industrial, and construction sectors. Strategic collaborations and capacity expansions enhance efficiency, differentiation, and alignment with evolving sustainability standards.

Suppliers and distributors optimize raw material procurement, inventory, and logistics to ensure timely delivery and cost-effective production. This streamlined supply chain, coupled with competitive innovation, strengthens market resilience, enabling players to capitalize on growth opportunities while maintaining a dynamic and forward-looking global market environment.

Key Industry Developments

- In April 2025, Sinopec partnered with Saudi Aramco’s Singapore unit to form Fujian Sinopec Aramco Refining and Petrochemical Co., a nearly US$4 Bn joint venture focused on port operations and petrochemical integration in Fujian province. This collaboration strengthened Sinopec’s feedstock security while expanding Aramco’s downstream footprint in one of China’s fastest-growing petrochemical hubs.

- In May 2025, The Goodyear Tire & Rubber Company signed a definitive agreement to sell its Goodyear Chemical synthetic rubber division to Gemspring Capital Management for approximately US$650 Mn, including key production and R&D sites in Texas and Ohio. The divestment allowed Goodyear to streamline its core tire business while giving Gemspring access to a specialized portfolio of performance polymers used in automotive, construction, and industrial sectors.

Companies Covered in Synthetic Rubber Market

- Trinseo

- The Goodyear Tire & Rubber Company

- China Petroleum & Chemical Corporation (Sinopec)

- LANXESS AG

- TSRC Corporation

- JSR Corporation

- Kumho Petrochemical Co., Ltd.

- Indian Synthetic Rubber Private Limited

- Apcotex Industries Limited

- Reliance Industries Limited

- Zeon Corporation

- Mitsui Chemicals, Inc.

- Saudi Basic Industries Corporation (SABIC)

- Denka Company Limited

Frequently Asked Questions

The market is set to reach US$23.8 Bn in 2025.

Expanding automotive production, rising demand from industrial and consumer goods sectors, along with continuous material innovation, are fueling strong growth in the synthetic rubber market.

The market is estimated to grow at a CAGR of 5.3% from 2025 to 2032.

Growing emphasis on sustainability and breakthrough innovations in eco-friendly production processes are unlocking new opportunities in the synthetic rubber market, driving long-term competitiveness and green advancements.

Key players include Trinseo, The Goodyear Tire & Rubber Company, China Petroleum & Chemical Corporation (Sinopec), LANXESS AG, TSRC Corporation, and JSR Corporation.