- Plastics, Polymers & Resins

- Europe Styrene Butadiene Rubber Market

Europe Styrene Butadiene Rubber Market Size, Share, and Growth Forecast 2026 - 2033

Europe Styrene Butadiene Rubber Market by Product Type (Emulsion SBR, Non-oil Extended, Oil Extended, Solution SBR, Butyl Lithium, Phenyl Lithium, Others), Application (Tires, Footwear, Adhesives, Construction, Others), and Country Analysis for 2026 - 2033

Europe Styrene Butadiene Rubber Market Size and Trend Analysis

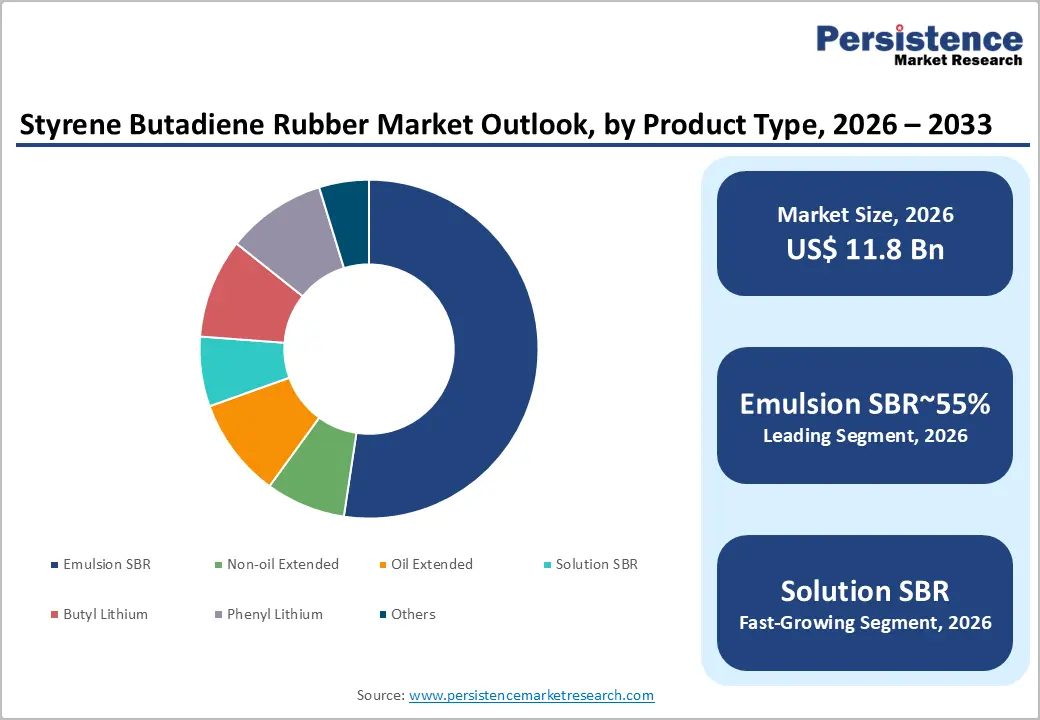

Europe Styrene Butadiene Rubber market size is supposed to be valued at US$ 11.8 Billion in 2026 and is projected to reach US$ 18.5 Billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The market's sustained and accelerating growth is driven by the structural dominance of tire manufacturing as the primary SBR consumption sector, accounting for the majority of global SBR demand, combined with rising automotive production volumes globally, the accelerating transition to fuel-efficient low-rolling-resistance tires mandated by tightening EU tire labeling regulations, and expanding SBR consumption in construction, adhesives, and footwear applications across emerging economies.

Key Industry Highlights:

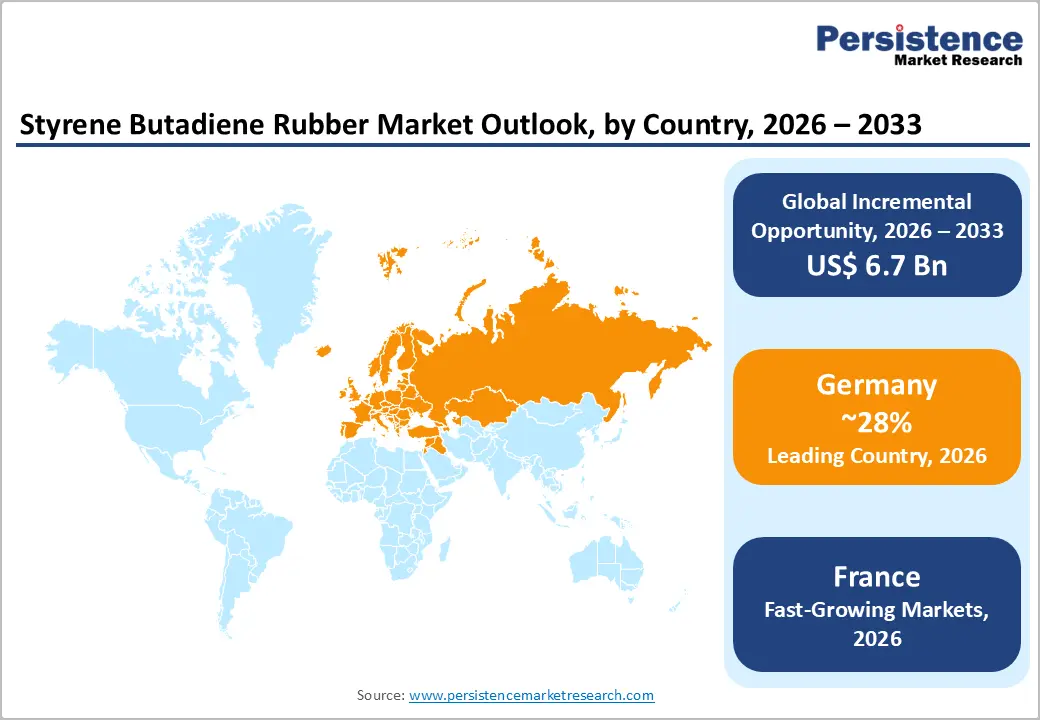

- Leading Country: Germany leads the European Styrene Butadiene Rubber market, anchored by ARLANXEO's world-class SBR facilities in Dormagen and Leverkusen, Continental AG's BEV tire compound R&D centers in Hannover, VCI's €12 billion German chemical sector R&D investment in 2023, and the EU tire labeling regulation mandating premium S-SBR adoption across European passenger car OEM tire supply programs.

- Dominant Product Type: Emulsion SBR dominates the Product Type segment with approximately 55% revenue share, anchored by the IISRP's documented dominance of E-SBR as the global highest-volume synthetic rubber grade by production tonnage, its cost-competitiveness versus S-SBR in standard tire and footwear applications, and its established multi-decade manufacturing infrastructure position across all major SBR-producing geographies globally.

- Fastest Growing Product Type: Solution SBR is the fastest-growing Product Type segment, driven by EU Regulation (EU) 2020/740 tire labeling mandates, ACEA's documented 1.5 million+ EU BEV registrations in 2023 generating demand for EV-specific premium compound tires, and ARLANXEO's Buna® VSL and Synthos S.A.'s S-SBR grade portfolio expansions targeting European tire OEM BEV program requirements.

- Key Market Opportunity: Bio-based SBR development and EU NGEU construction investment represent the dual key market opportunities, with ETRMA's Circular Rubber Roadmap targeting 100% circular rubber by 2050, Synthos S.A.'s bio-butadiene research partnership, and the EU's €648 billion NGEU program stimulating SBR latex construction chemical demand across 35 million building renovations targeted under the Renovation Wave Strategy.

| Key Insights | Details |

|---|---|

|

Styrene Butadiene Rubber Market Size (2026E) |

US$ 11.8 Billion |

|

Market Value Forecast (2033F) |

US$ 18.5 Billion |

|

Projected Growth CAGR (2026–2033) |

6.6% |

|

Historical Market Growth (2020–2025) |

6.1% |

Market Dynamics

Drivers - EU Tire Labeling Regulation and Fuel Efficiency Mandates Accelerating Premium Solution SBR Adoption Across European Tire OEMs

The European Union's tire labeling framework, governed by EU Regulation (EU) 2020/740 (which updated and replaced the original Regulation (EC) No 1222/2009 from May 2021), mandates that all tires sold in EU member states carry standardized performance labels rating wet grip, rolling resistance, and external rolling sound across an A–E grading scale, compelling tire manufacturers to adopt higher-performance synthetic rubber compounds in order to achieve commercially competitive label ratings that influence consumer purchasing decisions. Solution SBR (S-SBR), with its superior wet grip performance, lower hysteresis enabling reduced rolling resistance fuel savings, and enhanced abrasion resistance compared to conventional Emulsion SBR, is the technically preferred synthetic rubber grade for manufacturing EU label A and B wet grip category tires and A rolling resistance category tires.

The European Automobile Manufacturers' Association (ACEA) documents that European OEM vehicle fuel economy requirements, reinforced by the EU CO2 emission performance standards for passenger cars requiring fleet-average CO2 of 95 g/km, create indirect OEM procurement pressure on tire suppliers to provide fuel-efficient tire compound solutions that favor S-SBR over E-SBR in premium tire segments. ARLANXEO's Buna® VSL S-SBR grades and LANXESS's Krynol® performance SBR portfolio are among Europe's technically most referenced high-performance S-SBR product families for premium tire compound applications, with both companies investing in capacity and grade portfolio expansion to serve structurally growing European tire OEM demand.

Automotive Production Recovery and EV Tire Demand Creating Incremental SBR Procurement Growth Across European Supply Chain

The European automotive industry's production recovery and the accelerating transition to battery electric vehicles (BEVs), documented by ACEA as growing to over 1.5 million BEV registrations in the EU in 2023, are generating new and distinct SBR demand dynamics, as BEV tires require specialized high-performance rubber compounds with enhanced load-bearing capacity, reduced rolling resistance for range optimization, and elevated noise reduction characteristics that are best achieved through premium Solution SBR and functionalized S-SBR formulations. BEV vehicles, which are typically 20–30% heavier than equivalent internal combustion engine (ICE) vehicles due to battery pack mass, exert higher tire wear forces and require tires with enhanced durability compound formulations that consume more high-performance S-SBR per tire compared to standard passenger car tire grades.

Continental AG (headquartered in Hannover, Germany) and Michelin (headquartered in Clermont-Ferrand, France) have both publicly announced dedicated BEV-specific tire product lines, including Continental's EcoContact™ 7 and Michelin's Pilot Sport EV, each requiring specially engineered S-SBR compounds that generate above-average S-SBR content per tire compared to standard passenger car compound formulations. ARLANXEO (a Saudi Aramco subsidiary) serves as the primary S-SBR supplier to these European BEV tire OEM programs from its European production facilities in Dormagen and Leverkusen, Germany.

Restraints - Butadiene Feedstock Price Volatility and Supply Chain Disruption Creating SBR Production Cost Instability

Styrene Butadiene Rubber production is fundamentally dependent on butadiene, a co-product of naphtha steam cracking extracted from the C4 hydrocarbon stream of ethylene cracker units, whose supply is structurally constrained by ethylene production volume fluctuations and the long-term trend toward lighter ethane cracker feedstocks in the United States that produce significantly lower C4 butadiene co-product yields.

The International Institute of Synthetic Rubber Producers (IISRP) has documented significant butadiene price volatility cycles, with spot butadiene prices ranging from under €500/tons to over €2,000/tons within single-year periods during supply disruption events, generating severe SBR production cost instability that compresses manufacturer margins and creates customer supply agreement pricing tensions that are difficult to manage within long-term contract frameworks typical of the tire industry.

Competitive Pressure from Bio-Based and Natural Rubber Alternatives Constraining SBR Market Share in Sustainable Product Segments

Growing sustainability mandates across European automotive and consumer goods supply chains, driven by the EU's Corporate Sustainability Reporting Directive (CSRD) and the EU Taxonomy Regulation framework for sustainable economic activities, are creating competitive pressure from bio-based synthetic rubber alternatives and high-quality natural rubber (NR) for SBR in tire compound formulations where sustainability credentials are becoming commercially relevant procurement criteria.

The Global Platform for Sustainable Natural Rubber (GPSNR), a multi-stakeholder initiative established in 2018 including major tire manufacturers Michelin, Bridgestone, and Continental AG, is actively promoting certified sustainably sourced natural rubber that competes with synthetic SBR in tire compound formulations where natural rubber's renewable and biodegradable origin provides a sustainability differentiation advantage over petroleum-derived SBR at equivalent performance levels.

Opportunities - Bio-Based SBR Development and Green Chemistry Innovation Creating Premium Sustainable Rubber Market Opportunities

The European chemical industry's strategic pivot toward bio-based feedstocks and circular chemistry, driven by the European Green Deal, the EU Chemical Strategy for Sustainability, and major European tire OEM sustainability commitments published under Science Based Targets initiative (SBTi) frameworks, is creating a compelling commercial opportunity for SBR producers able to develop and commercialize bio-based Styrene Butadiene Rubber grades derived from renewable feedstock butadiene and bio-styrene that maintain full performance equivalence with petroleum-derived S-SBR while delivering verifiably lower life cycle carbon footprints. ARLANXEO and LANXESS have both initiated research programs into bio-based butadiene feedstock pathways, including fermentation-derived butadiene from renewable sugars, as part of their long-term sustainable rubber development strategies aligned with European chemical industry carbon neutrality commitments.

The European Tyre and Rubber Manufacturers' Association (ETRMA) published its Circular Rubber Roadmap in 2023, outlining the European tire and rubber industry's pathway to 100% circular rubber by 2050, which explicitly identifies bio-based synthetic rubber development as a critical technology pathway requiring collaborative industry investment. Synthos S.A., the largest synthetic rubber producer in Central and Eastern Europe and a significant S-SBR producer, has announced research collaborations targeting bio-based butadiene integration into its S-SBR production process at its Owicim, Poland facility, positioning the company for early-mover advantage in the premium bio-based SBR market segment.

Construction Sector SBR Demand Expansion Driven by EU Infrastructure Investment and Sustainable Waterproofing Applications

The European construction sector's accelerating adoption of SBR-modified polymer cement mortars, waterproofing membranes, adhesives, and bitumen modification applications, stimulated by the European Union's €648 billion NextGenerationEU (NGEU) recovery investment program and the Renovation Wave Strategy targeting the energy-efficient renovation of 35 million buildings across EU member states by 2030, is creating a structurally growing non-tire SBR demand category that provides meaningful revenue diversification beyond the tire industry's cyclical demand dynamics. SBR latex is widely used as a polymer modifier in cementitious waterproofing systems, tile adhesive formulations, and exterior insulation finishing systems (ETICS), all of which are high-growth construction chemical categories driven by the EU's Energy Performance of Buildings Directive (EPBD) requirements for improved building thermal performance.

The European Construction Industry Federation (FIEC) documented that European construction output reached approximately €1.8 trillion in 2023, with renovation and energy-efficiency retrofit construction representing the fastest-growing sub-segment directly aligned with SBR latex construction chemical application growth. Dow Chemical and BASF SE are among the leading SBR latex suppliers to the European construction chemicals market, producing specialized SBR emulsion grades for adhesive, sealant, and waterproofing compound formulation that are procured by construction chemical companies including Sika AG and MAPEI.

Category-wise Analysis

By Product Type Insights

Emulsion SBR (E-SBR) leads the Europe Styrene Butadiene Rubber market by product type, accounting for approximately 55% of total product type segment revenue in 2026, a dominant position reflecting E-SBR's established commercial maturity, lower production cost versus Solution SBR, and continued large-volume consumption in standard passenger car tire compounds, truck and bus tire treads, footwear soling compounds, and industrial rubber product manufacturing that collectively constitute the largest aggregate SBR volume consumption sectors globally. E-SBR, produced through aqueous emulsion polymerization of styrene and butadiene monomers at temperatures of either 5°C (Cold SBR) or 50°C (Hot SBR), benefits from decades of established manufacturing infrastructure across European, North American, and Asian production facilities, with well-characterized physical property databases extensively referenced in tire compound design manuals.

The International Institute of Synthetic Rubber Producers (IISRP) documents E-SBR as the largest-volume synthetic rubber grade globally by production tonnage. Solution SBR (S-SBR) holds approximately 30% of product type revenue, and is the fastest-growing sub-segment, driven by EU tire labeling mandates and BEV tire compound requirements compelling accelerated S-SBR adoption across premium tire segments.

By Application Insights

Tires dominate the Europe Styrene Butadiene Rubber market by application, commanding approximately 65% of total application segment revenue in 2026, a commanding market position reflecting SBR's foundational role as the synthetic rubber of choice for tire tread compound formulations across passenger car, light truck, and commercial vehicle tire categories globally, where its superior abrasion resistance, wet traction performance, and processing characteristics make it technically the most commercially established synthetic rubber for tire manufacturing. The European Tyre and Rubber Manufacturers' Association (ETRMA) reports that Europe's tire industry consumed approximately 1.3 million tonss of synthetic rubber annually in recent years, with SBR representing the largest single synthetic rubber grade by consumption volume in tire compound manufacturing across all major European OEM tire producers.

Continental AG, Michelin, Pirelli, and Bridgestone Europe are the four largest European tire manufacturers collectively consuming the dominant share of European SBR procurement from producers including ARLANXEO, LANXESS, and Synthos S.A. The Construction application segment holds the second position at approximately 12% of revenue, and represents the fastest-growing non-tire SBR application category driven by EU NGEU infrastructure investment and EPBD building renovation mandates.

Regional Insights

Germany Styrene Butadiene Rubber Market Trends

Germany is the leading European market for Styrene Butadiene Rubber, anchored by its concentration of world-class automotive and tire manufacturing OEMs, globally influential SBR chemical producers, and a regulatory environment that simultaneously mandates higher-performance rubber compounds through EU tire labeling and vehicle emissions standards. ARLANXEO, the world's leading dedicated synthetic rubber company, operating under full ownership of Saudi Aramco, maintains its primary SBR production facilities in Dormagen and Leverkusen, Germany, making Germany the most production-significant SBR geography in Europe. LANXESS AG (headquartered in Cologne, Germany), which retains SBR-related activities through its specialty chemicals portfolio, and Evonik Industries AG (headquartered in Essen, Germany) contribute rubber process chemicals and specialty compound additives that make Germany the most complete SBR value chain geography in Europe.

Continental AG's tire compound research centers in Hannover and Frankfurt are at the forefront of Solution SBR compound development for BEV-specific tire applications, collaborating directly with ARLANXEO and Evonik on next-generation functionalized S-SBR formulations targeting the growing European premium electric vehicle tire market. The German Chemical Industry Association (VCI) has documented that the German chemical sector, of which synthetic rubber is a core segment, invested over €12 billion in R&D in 2023, confirming the structural depth of Germany's innovation investment in advanced synthetic rubber materials science that sustains its leadership position in the European and global SBR technology landscape.

Italy Styrene Butadiene Rubber Trends

Italy is a commercially significant European SBR market, anchored by its world-renowned tire manufacturing industry anchored by Pirelli (headquartered in Milan), one of Europe's largest premium tire manufacturers with P Zero™ and Cinturato™ product lines requiring high-performance Solution SBR compound formulations, and its substantial automotive and footwear manufacturing industries that collectively sustain diversified SBR demand across tire, footwear, adhesive, and construction chemical application categories.

Pirelli's strategic focus on the ultra-high-performance (UHP) and premium tire segment, which Pirelli's Annual Report 2023 documents as accounting for over 76% of group revenues, generates disproportionate demand for premium S-SBR grades with superior wet grip and low rolling resistance performance characteristics, positioning Italy as a above-average-growth premium SBR demand geography within the European market.

Italy's footwear manufacturing industry, with Confindustria Moda documenting Italy as Europe's largest footwear manufacturing economy with over 7,000 footwear companies primarily concentrated in the Veneto, Tuscany, and Marche regions, is a significant consumer of Emulsion SBR in shoe soling compound formulations, sustaining a large non-tire domestic SBR consumption base. The EU's REACH Regulation compliance framework, enforced by Italy's national chemicals authority ISPRA, shapes the SBR compound formulations permissible in Italian consumer footwear and construction adhesive applications, creating regulatory alignment incentives for Italian SBR consumers to source from REACH-certified European SBR producers including ARLANXEO and Synthos S.A.

France Styrene Butadiene Rubber Trends

France is a strategically important European SBR market, anchored by Michelin's dominant global tire manufacturing presence headquartered in Clermont-Ferrand, and sustained by France's significant automotive supply chain including Stellantis (headquartered in Amsterdam with major French manufacturing operations) and Renault Group (headquartered in Boulogne-Billancourt), whose passenger car production programs generate substantial domestic SBR compound procurement. Michelin's commitment to 100% sustainable materials in its tires by 2050, published in the company's 2023 Annual and Sustainable Development Report, directly shapes French SBR procurement strategy, with Michelin actively collaborating with SBR producers on bio-based butadiene sourcing pathways and devulcanization-based recycled SBR integration into tire compound formulations.

France's construction sector, with Fédération Française du Bâtiment (FFB) documenting sustained construction activity supported by France Relance investment programs, generates significant domestic demand for SBR latex in polymer-modified mortar, waterproofing membrane, and construction adhesive formulations. The French Environment and Energy Management Agency (ADEME) is actively funding bio-based rubber research programs under its France 2030 industrial innovation investment plan, supporting academic and industrial research collaborations targeting bio-based SBR and thermoplastic elastomers that align with France's chemical industry decarbonization objectives under the Stratégie Nationale Bas-Carbone (SNBC). INEOS and LyondellBasell serve the French SBR and related polymer market through their European petrochemical distribution networks connecting Belgian and Dutch production hubs to French industrial customers.

Competitive Landscape

The Europe Styrene Butadiene Rubber market is moderately consolidated, with ARLANXEO, LANXESS, Synthos S.A., and SABIC commanding leading European positions through large-scale dedicated SBR production assets, proprietary S-SBR grade portfolios, and long-term supply agreements with major European tire OEMs. Key competitive differentiators include functionalized S-SBR technology patents, ISO 9001 and IATF 16949 automotive quality certifications, application engineering technical service capabilities, and proximity to European tire manufacturing clusters.

Dow and BASF SE compete in SBR latex segments for construction and adhesive applications. Emerging trends include bio-based SBR R&D partnerships with renewable feedstock companies, circular rubber programs aligned with ETRMA's 2050 circular rubber roadmap, and carbon footprint-labeled S-SBR product grades serving sustainability-conscious European tire OEM procurement criteria under SBTi compliance commitments.

Key Developments:

- In March 2025, ARLANXEO announced an expansion of its high-performance Solution SBR (S-SBR) production capacity at its Dormagen, Germany facility, targeting the growing demand from European BEV tire manufacturers for premium functionalized S-SBR compounds with enhanced wet grip and low rolling resistance performance in electric vehicle tire compound applications.

- In November 2024, Synthos S.A. unveiled a strategic research partnership with a leading European renewable chemistry institute to develop bio-based butadiene production pathways for integration into its S-SBR fermentation production program at Owicim, Poland, targeting early-mover position in the emerging bio-based synthetic rubber market aligned with European tire OEM sustainability commitments.

- In June 2024, LANXESS AG completed a strategic portfolio restructuring, separating its synthetic rubber activities under the ARLANXEO platform while redirecting LANXESS core focus toward specialty chemicals, reinforcing ARLANXEO's position as Europe's dedicated synthetic rubber technology leader with full strategic independence to pursue SBR capacity expansion and bio-based rubber innovation investments aligned with European market demand growth.

Companies Covered in Europe Styrene Butadiene Rubber Market

- ARLANXEO

- Synthos S.A.

- LANXESS AG

- AkzoNobel

- BASF SE

- INEOS

- LyondellBasell

- Evonik Industries AG

- SABIC

- Dow

Frequently Asked Questions

Europe Styrene Butadiene Rubber market is estimated to be valued at US$ 11.8 Billion in 2026 and is projected to reach US$ 18.5 Billion by 2033, registering a forecast CAGR of 6.6% from 2026 to 2033. The market recorded a historical CAGR of 6.1% between 2020 and 2025, driven by EU tire labeling mandates, BEV tire compound demand, construction sector SBR latex adoption, and ongoing Solution SBR capacity investment by ARLANXEO and Synthos S.A.

The primary drivers are EU Regulation (EU) 2020/740 tire labeling mandates compelling adoption of premium Solution SBR compounds for A-rated wet grip and rolling resistance tires, and ACEA's documented 1.5 million+ EU BEV registrations in 2023 driving demand for BEV-specific high-performance tire compounds requiring advanced functionalized S-SBR grades from ARLANXEO's Buna® VSL and Synthos S.A.'s dedicated S-SBR product families serving Continental AG, Michelin, and Pirelli compound manufacturing programs.

Emulsion SBR (E-SBR) leads the Product Type segment with approximately 55% revenue share in 2026, confirmed by IISRP documentation of E-SBR as the world's highest-volume synthetic rubber grade, its cost-competitive manufacturing economics versus S-SBR, and its continued large-scale consumption in standard passenger car tire treads, commercial vehicle tire compounds, footwear soling, and industrial rubber product manufacturing across all major global SBR production and consumption geographies.

Germany leads the European Styrene Butadiene Rubber market, anchored by ARLANXEO's world-class production facilities in Dormagen and Leverkusen, Continental AG's BEV tire R&D programs in Hannover, LANXESS AG's Cologne specialty chemical operations supporting rubber compound manufacturing, and the VCI's documented €12 billion German chemical sector R&D investment sustaining Germany's technical leadership in advanced S-SBR grade development and premium automotive tire compound innovation.

The most significant opportunities are bio-based SBR development aligned with ETRMA's Circular Rubber Roadmap targeting 100% circular rubber by 2050, with Synthos S.A.'s bio-butadiene research and ARLANXEO's renewable feedstock programs positioned to capture premium sustainable SBR demand, and EU NGEU's €648 billion construction investment driving SBR latex demand across 35 million building renovations targeted under the EU Renovation Wave Strategy through the 2026–2033 forecast period.