- Specialty & Fine Chemicals

- Conductive Silicone Rubber Market

Conductive Silicone Rubber Market Size, Share, and Growth Forecast 2026 - 2033

Conductive Silicone Rubber Market by Product Type (Thermally Conductive, Electrically Conductive, and Others), Application (Automotive & Transportation, Electrical & Electronics, Industrial Machines, and Others), and Regional Analysis for 2026 - 2033

Conductive Silicone Rubber Market Size and Share Analysis

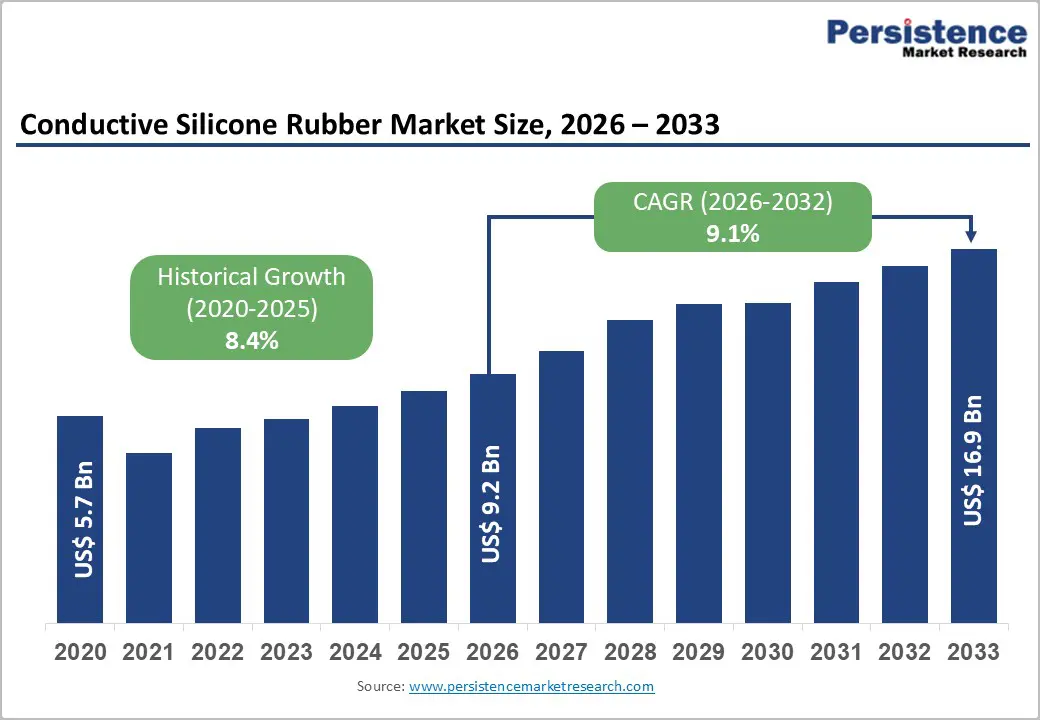

The global conductive silicone rubber market size is likely to be valued at US$ 9.2 billion in 2026 and is projected to reach US$ 16.9 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033.

The market expansion is driven by exponential growth in electric vehicle adoption with global EV sales surpassing 17 million units in 2024 representing 25% year-over-year expansion, creating unprecedented demand for advanced thermal management materials ensuring optimal battery performance and safety within temperature ranges of 10°C to 50°C, and accelerating 5G infrastructure deployment and consumer electronics miniaturization requiring sophisticated thermal interface materials and electromagnetic interference shielding.

Key Industry Highlights:

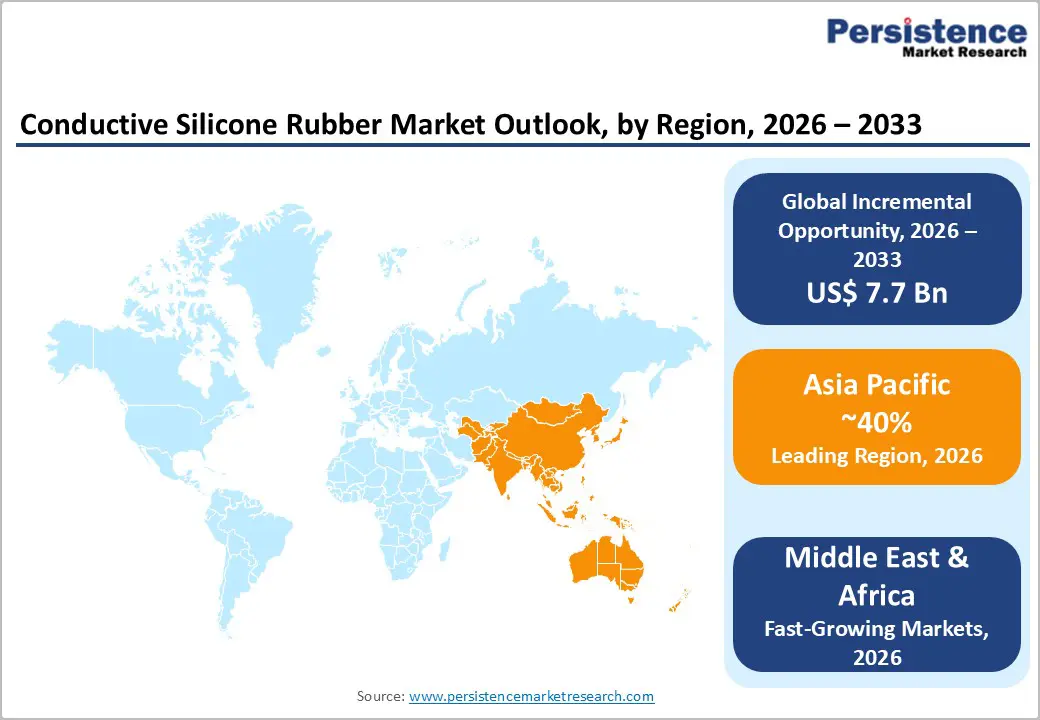

- Leading Region: Asia Pacific dominates the global conductive silicone rubber market with a commanding 40.50% market share, anchored by China accounting for 70% of global EV production in 2024, Japan's advanced semiconductor sectors, and South Korea's electronics manufacturing, establishing sustained regional leadership.

- Fastest Growing Region: North America experiences robust growth driven by U.S. automotive electrification programs, 5G infrastructure deployment, aerospace defense applications, and an established innovation ecosystem supporting accelerated regional market expansion through the forecast period.

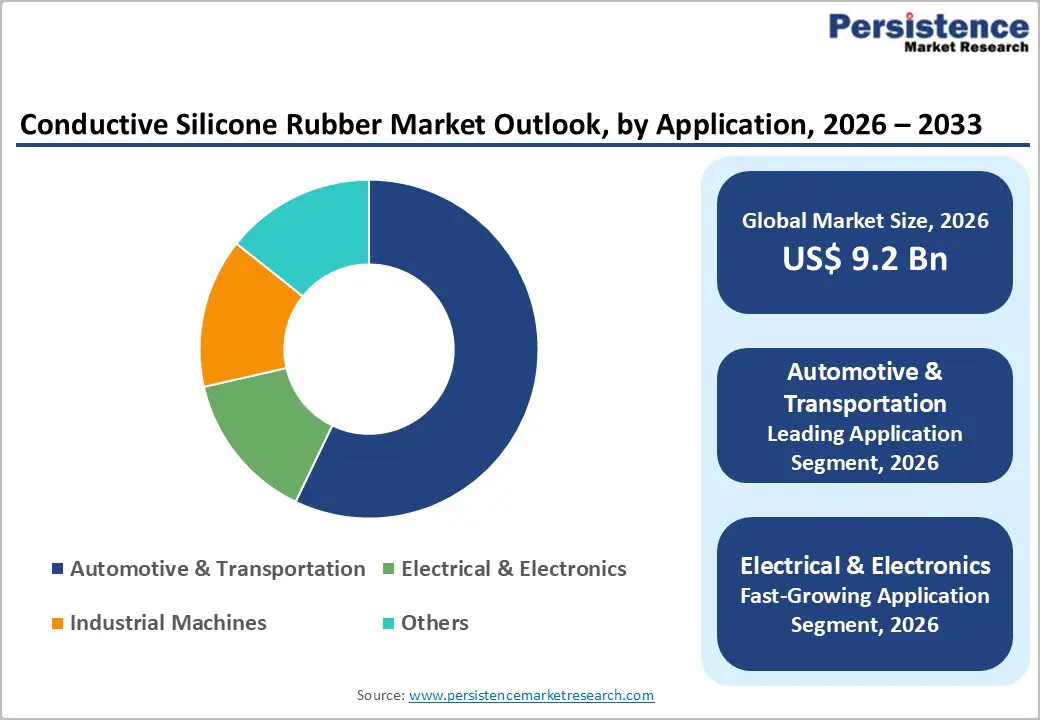

- Dominant Application: Automotive and transportation application maintains market dominance with 36.4% market share in 2024, driven by electric vehicle adoption, battery thermal management requirements, wiring harness integration, and ADAS sensor applications supporting sustained segment leadership.

- Growing Application: Electrical and electronics applications experience fastest growth through the forecast period, propelled by 5G infrastructure expansion, LED lighting adoption, medical device integration, consumer electronics miniaturization, establishing exceptional growth momentum.

- Key Opportunity: Bio-based silicone formulation development and aerospace-defense application expansion represent exceptional opportunities, driven by sustainability initiatives, renewable resource policies, advanced thermal management requirements, and specialized high-performance applications supporting premium market positioning.

| Key Insights | Details |

|---|---|

|

Global Conductive Silicone Rubber Market Size (2026E) |

US$ 9.2 Bn |

|

Market Value Forecast (2033F) |

US$ 16.9 Bn |

|

Projected Growth CAGR(2026-2033) |

9.1% |

|

Historical Market Growth (2020-2025) |

8.4% |

Market Dynamics

Drivers - Accelerated Electric Vehicle Adoption and Need for Thermal Management

The global electric vehicle market has experienced transformational growth with sales surpassing 17 million units in 2024, representing 25% year-over-year expansion and establishing unprecedented demand for specialized thermal management materials. China maintained dominant market position, accounting for 70% of global EV production in 2024, driving regional demand for advanced silicone-based thermal interface materials. EV battery pack thermal management requires precise temperature maintenance between 10°C and 50°C with temperatures below 10°C reducing energy storage performance and temperatures exceeding 50°C accelerating aging and increasing thermal runaway risk.

Tesla's 4680 battery cell technology utilizes silicone adhesives with 3 W/m·K thermal conductivity distributing heat evenly across cell surfaces, establishing performance benchmarks. Thermally conductive silicone gap fillers serving as interface materials between cooling plates and battery cells have become essential infrastructure providing thermal conductivity significantly exceeding air (0.024 W/m·K) supporting efficient heat dissipation. Growing electrification of commercial vehicles, buses, and logistics fleets is expanding end-market demand beyond passenger vehicles establishing sustained growth drivers through forecast period.

5G Infrastructure Expansion and Advanced Electronics Miniaturization

5G network rollout and telecommunications infrastructure development are creating substantial incremental demand for electrically conductive silicone rubber providing electromagnetic interference (EMI) shielding and electrostatic dissipation (ESD) protection essential for high-frequency signal transmission equipment. Advanced semiconductor miniaturization in consumer electronics, computing devices, and telecommunications equipment requires thermally conductive interface materials managing heat dissipation from increasingly power-dense components.

Graphene nanotube technology advancement enables achievement of electrical conductivity at ultralow dopant concentrations of 0.5 wt% compared to traditional carbon black requiring 5-25 wt% loadings, preserving mechanical flexibility and enabling color customization while reducing surface marking and electrical hot spots. LED lighting technology adoption for illumination and agricultural applications requires thermally conductive compounds ensuring reliable long-term performance and extended service life of 10-12 years. Wearable device proliferation incorporating biosensors, health monitoring systems, and personal electronic devices establishes growing demand for flexible, thermally conductive silicone compounds supporting advanced consumer electronics market expansion.

Restraint - Alternative Material Competition and Technical Standardization Challenges

Advanced thermal interface materials including phase change materials (PCM), graphene-based compounds, and ceramic thermal pads are emerging as competitive alternatives potentially achieving comparable or superior performance at evolving pricing structures. Regulatory compliance requirements including UL fire protection ratings, FDA approvals for medical applications, and ECHA chemical regulations extend commercialization timelines and certification costs limiting innovation velocity. Technical standardization challenges across diverse applications and operating environments require extensive testing and customer collaboration increasing development complexity.

High Raw Material Costs and Specialized Manufacturing Requirements

Conductive silicone rubber formulation requires specialized filler materials including aluminum oxide, boron nitride, graphene nanotubes, and metal-based nanoparticles exhibiting high thermal and electrical conductivity, creating elevated raw material costs compared to standard elastomer compounds. Manufacturing processes require precision equipment, technical expertise, and rigorous quality control increasing production complexity and capital investment requirements limiting supplier base expansion. Price volatility affecting petroleum-derived feedstocks and specialty chemical inputs creates cost uncertainty affecting manufacturer profitability and pricing stability.

Opportunities - Bio-Based Silicone Formulation Development and Sustainability-Driven Market Expansion

Sustainable and environmentally friendly conductive silicone formulations represent exceptional growth opportunities driven by corporate environmental commitments, government clean energy policies, and consumer preference for sustainable materials. Wacker Chemie AG's May 2024 launch of ELASTOSIL eco LR 5040, a bio-methanol-based silicone rubber featuring high durability and tear resistance for medical, baby care, and food product applications, demonstrates commercial viability of sustainable formulations.

Bio-based alternatives utilizing renewable feedstocks enable circular economy alignment and carbon footprint reduction supporting premium market positioning. Government sustainability incentives and corporate carbon neutrality targets establish favorable market conditions for renewable material adoption. Cosmetics and personal care industries leading adoption of natural compounds create demonstration applications supporting market expansion into adjacent segments. Research advancement in renewable resource utilization and processing optimization is enabling cost-competitive sustainable alternatives challenging traditional petroleum-derived markets.

Advanced Thermal Interface Solutions and Aerospace/Defense Application Expansion

Advanced thermal interface material development addressing high-performance computing, aerospace systems, and defense applications represents significant growth opportunity driven by technical performance requirements exceeding commercial electronics standards. Aerospace thermal management systems, lightning strike protection equipment, and electromagnetic shielding applications require specialized conductive silicone formulations operating across extreme temperature ranges (-40°C to +200°C) with precision performance tolerances.

Shin-Etsu Chemical's September 2024 launch of ST-OR Type heat-shrinkable silicone tubing for EV and hybrid vehicle busbar covering featuring 1.0 W/m·K thermal conductivity demonstrates continuous innovation addressing evolving market requirements. Busbar protection applications in high-voltage power distribution systems require conductive silicone coatings preventing arcing, providing electrical insulation, and maintaining thermal barriers under extreme conditions. Defense sector electromagnetic hardening requirements and military vehicle electrification programs establish specialized end-market demand supporting premium pricing and sustained growth through forecast period.

Category-wise Analysis

Product Type Insights

Thermally conductive silicone rubber formulations command market dominance, accounting for approximately 47% of total market share in 2026, driven by exceptional performance in thermal management applications across electric vehicles, telecommunications equipment, LED lighting, and high-performance computing systems. Thermal conductivity ranging from 1-8 W/m·K represents dramatic improvement over conventional silicone rubber's insulative properties while maintaining mechanical flexibility and processing compatibility essential for industrial applications.

Filler technology including aluminum oxide and boron nitride enables precise thermal property tuning addressing application-specific requirements across diverse industries. EV battery module integration represents the primary demand driver, with thermally conductive gap fillers and adhesives serving as essential components in cooling systems ensuring uniform temperature distribution and preventing thermal runaway events. Semiconductor and microelectronics cooling requirements are expanding market opportunities as miniaturization trends create higher power density necessitating advanced thermal solutions. Continuous product innovation by major manufacturers including Shin-Etsu and Momentive targeting mobility and electronics markets supports continued segment dominance through forecast period.

Application Insights

The automotive and transportation segment represents the dominant conductive silicone rubber application, commanding 36% market share in 2026, driven by comprehensive integration across engine systems, electrical wiring harnesses, battery seals, sensors, ignition systems, and thermal management components. Electric vehicle electrification necessitates specialized silicone compounds providing thermal insulation and conductivity, electrical safety, and environmental protection across high-voltage battery systems and power distribution networks. ADAS (Advanced Driver Assistance Systems) sensors and connected vehicle electronics require EMI shielding and thermal stability establishing expanding application scope beyond traditional engine compartment components. Spark plug boots, fuel injector seals, and connector applications leverage exceptional weather resistance, heat durability, and chemical resistance of conductive silicone formulations. Automotive cooling plate interfaces utilizing metal substrates with silicone adhesive bonding enable efficient heat transfer from battery cells to cooling systems maintaining thermal stability essential for battery longevity. Commercial vehicle electrification including buses, trucks, and logistics vehicles is expanding market opportunities beyond passenger vehicle segments supporting sustained application growth.

The electrical and electronics segment represents the fastest-growing application category over 2026-2033 forecast period, driven by increasing integration of conductive silicone rubber across connectors, gaskets, housings, keypad assemblies, and electromagnetic shielding applications. 5G infrastructure expansion necessitates electromagnetic interference (EMI) shielding materials protecting sensitive telecommunications equipment from external electromagnetic interference and internal signal crosstalk. Wires and cables require conductive rubber coatings and insulation layers providing electrical conductivity control and environmental protection.

LED lighting systems benefit from thermally conductive silicone compounds enabling efficient heat dissipation from high-brightness light-emitting diodes maintaining color accuracy and extended operational lifespan. Mobile and remote keypad manufacturing utilizes conductive silicone elastomers enabling electrical contact reliability and mechanical durability across millions of actuation cycles. Medical device applications including ECG electrodes, EEG electrodes, and defibrillator pads require biocompatible conductive compounds combining electrical conductivity, skin compatibility, and sterilization resistance. The growth in the electronic industry is driven by consumer device proliferation and industrial automation expansion, and is establishing sustained demand drivers supporting segment growth throughout the forecast period.

Regional Insights

North America Conductive Silicone Rubber Market Trends

North America represents a significant conductive silicone rubber market anchored by the United States maintaining market leadership through advanced automotive manufacturing, electronics innovation, and aerospace defense applications. U.S. regulatory framework including Underwriters Laboratory (UL) standards and FDA compliance requirements establish rigorous quality specifications driving adoption of high-performance materials. Automotive electrification programs by major OEMs and specialized EV manufacturers create substantial demand for thermal interface materials and electrical shielding components. 5G infrastructure deployment across North American telecommunications networks is generating incremental demand for EMI shielding and electrical conductivity solutions.

Canada participates in North American automotive supply chains with an established manufacturing presence supporting regional material demand. Mexico's automotive sector expansion through USMCA trade agreements and nearshoring manufacturing trends establishes growing market opportunities for conductive silicone suppliers supporting regional assembly operations.

Europe Conductive Silicone Rubber Market Trends

Europe represents a significant global market with Germany maintaining technology leadership through advanced material formulation expertise and an established manufacturer base. Wacker Chemie AG's headquarters in Munich, Germany and production facilities across Europe establish manufacturing and innovation presence supporting regional market dominance. European Union automotive electrification mandates and emissions reduction requirements drive EV adoption, creating sustained conductive silicone demand.

European Chemicals Agency (ECHA) compliance requirements establish stringent environmental standards, driving sustainable formulation development, including bio-based alternatives. Sustainability initiatives and circular economy policies across EU member states support premium market positioning for environmentally friendly conductive silicone products.

Asia Pacific Conductive Silicone Rubber Trends

Asia Pacific is likely to command the global conductive silicone rubber market with 40.5% share in 2026, anchored by China's exceptional dominance, representing more than 60% of regional demand. China's EV market leadership, with 70% of global EV production in 2024, establishes unprecedented demand for thermal management materials across battery systems, charging infrastructure, and vehicle electronics. Government policies prioritizing manufacturing competitiveness and green energy vehicle adoption create sustained procurement requirements supporting regional market expansion.

Japan maintains strong market presence through Shin-Etsu Chemical's advanced thermal interface material development and automotive component integration by major OEMs, including Toyota and Honda. South Korea's electronics manufacturing dominance and KCC Corporation's full acquisition of Momentive Performance Materials in 2024 establish regional innovation capability supporting competitive positioning in advanced conductive silicone markets.

Competitive Landscape

The conductive silicone rubber market exhibits a moderately consolidated competitive structure dominated by global specialty chemical manufacturers with integrated capabilities spanning raw material sourcing, formulation development, manufacturing, and technical customer support. Tier -1 companies, including Dow, Wacker Chemie AG, Shin-Etsu Chemical, and Saint-Gobain, collectively command approximately 50%+ global market share through comprehensive product portfolios, manufacturing scale, and technical excellence. Dow maintains market leadership through diverse product offerings addressing automotive, electronics, aerospace, and telecommunications applications. Wacker Chemie AG's emphasis on bio-based formulations and capacity expansion demonstrates sustainability-focused competitive differentiation.

Tier 2 manufacturers including Momentive (now fully controlled by KCC Corporation), Western Rubbers, and Specialty Silicone Products manage approximately 25-30% market share, differentiating through specialized formulations and regional expertise. Competitive strategies emphasize R&D investments in advanced filler technologies, sustainable alternatives, and customized application development supporting market differentiation.

Key Market Developments

- In September 2025, WACKER is setting new benchmarks in the field of flexible printed electronics at K 2025. The company has begun serial production of its innovative sensor laminates under the brand name NEXIPAL Sense. Produced using a fully automated roll-to-roll process developed in-house, NEXIPAL Sense laminates consist of highly stretchable insulating and conductive silicone rubber films.

- In March 2024, KCC Corporation finalized acquisition of remaining minority shares of Momentive Performance Materials, establishing full ownership and integrating silicone manufacturing capabilities with KCC's broader chemical portfolio to develop high-grade silicones across diverse end-use industries globally.

- In May 2024, Wacker Chemie AG introduced ELASTOSIL eco LR 5040, a bio-methanol-based silicone rubber featuring high durability and tear resistance for medical, baby care, and food product applications, demonstrating market commitment to sustainable, environmentally friendly formulations.

- In September 2024, Shin-Etsu Chemical introduced ST-OR Type heat-shrinkable silicone tubing for electric and hybrid vehicle busbar covering offering 1.0 W/m·K thermal conductivity and -40°C to +200°C operating range, addressing emerging EV thermal management requirements.

Companies Covered in Conductive Silicone Rubber Market

- Dow

- Saint-Gobain

- Wacker Chemie AG

- Western Rubbers

- Western Polyrub India Pvt. Ltd.

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- KCC CORPORATION

- China Bluestar International Chemical Co., Ltd.

- REISS MANUFACTURING, INC.

- MESGO SpA

- Jan Huei K.H. Industry Co., Ltd.

- Soliani EMC

- Simolex Rubber

Frequently Asked Questions

The global Conductive Silicone Rubber Market is projected to reach US$ 16.9 billion by 2033, expanding from US$ 9.2 billion in 2026 at a CAGR of 9.1%, driven by electric vehicle thermal management demand, 5G infrastructure expansion, electronics miniaturization, and aerospace defense applications supporting sustained market growth.

Market demand growth is driven by multiple converging factors including electric vehicle adoption surpassing 17 million units in 2024 with 25% year-over-year expansion; 5G telecommunications infrastructure deployment requiring electromagnetic interference shielding; advanced electronics miniaturization.

Automotive and transportation applications represent the dominant segment commanding 36.4% market share in 2026, driven by electric vehicle electrification, battery thermal management requirements, wiring harness integration, ADAS sensor applications, and comprehensive vehicle electronics component utilization supporting sustained segment dominance.

Asia Pacific commands market leadership with 40% global conductive silicone rubber market share, anchored by China accounting for 70% of global EV production in 2024, Japan's advanced semiconductor manufacturing, South Korea's electronics expertise, and government-backed electrification initiatives supporting sustained regional market dominance.

Major market opportunities include bio-based silicone formulation development supporting sustainability objectives; aerospace and defense thermal management applications requiring extreme temperature performance; graphene nanotube technology advancement enabling ultralow dopant concentrations; 5G and telecommunications infrastructure expansion driving EMI shielding demand.