- Food Ingredients & Additives

- Rice Protein Market

Rice Protein Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Rice Protein Market by Source (Brown Rice, White Rice), by Form (Isolates, Concentrates, Hydrolysates), by Nature (Organic, Conventional), by End Use (Functional Foods, Snacks & Cereals, Dairy Alternatives, Bakery & Confectionery, Animal Feed, Sports Nutrition, Others), by Regional Analysis, 2026 - 2033

Rice Protein Market Share and Trends Analysis

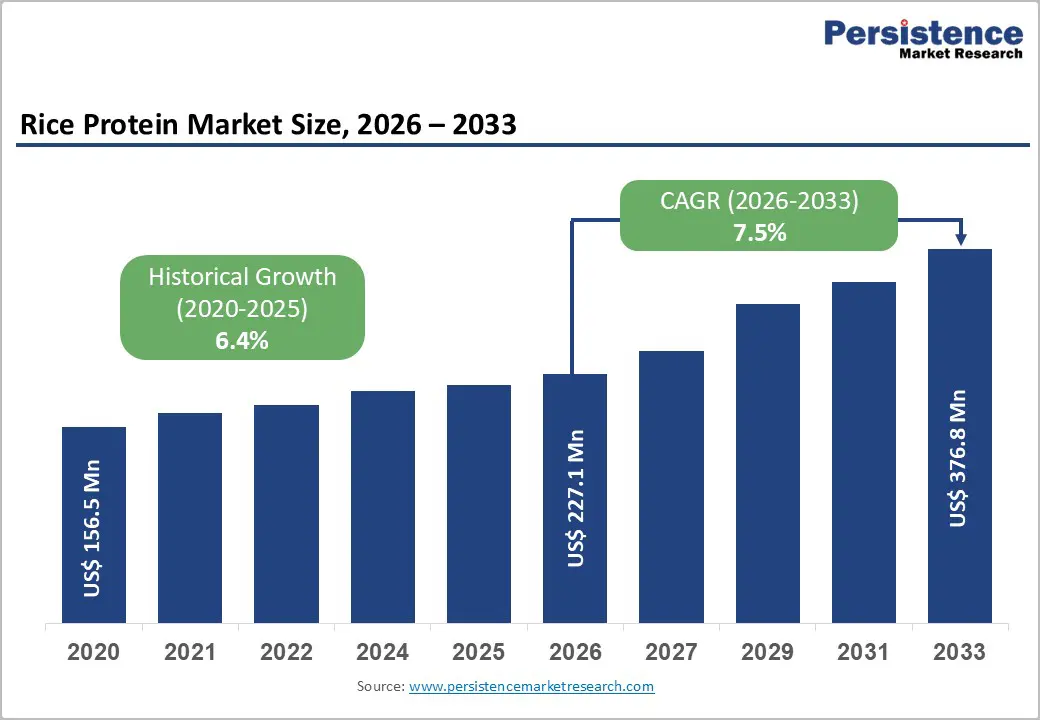

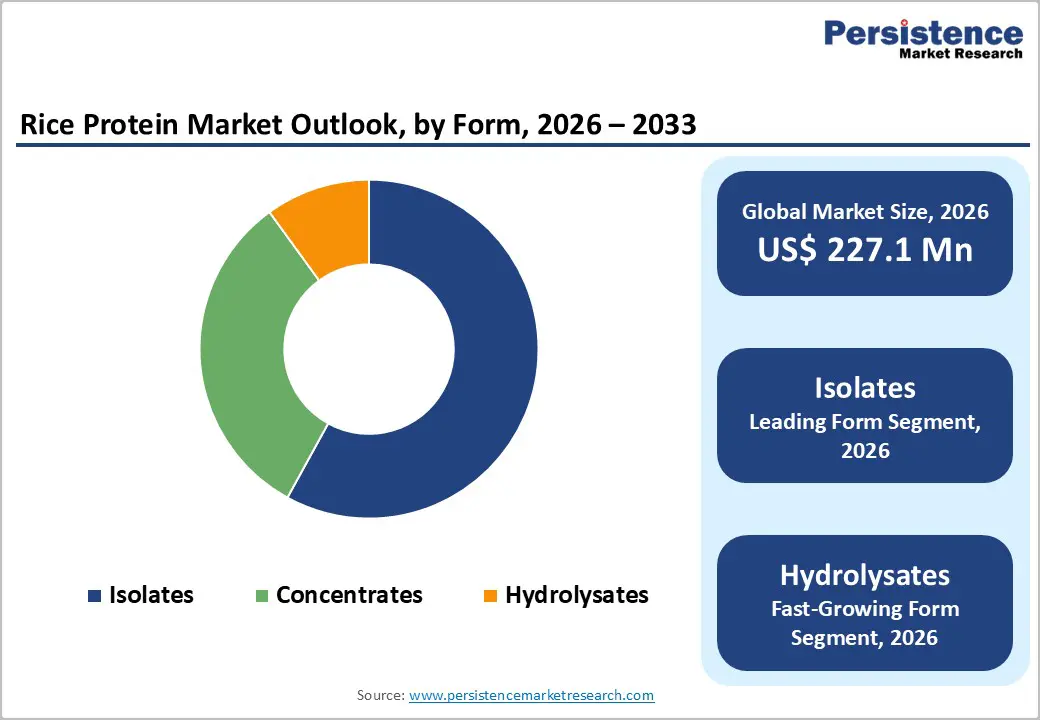

The global rice protein market size is expected to be valued at US$ 227.1 million in 2026 and projected to reach US$ 376.8 million by 2033, growing at a CAGR of 7.5% between 2026 and 2033.

Rice protein is rapidly reshaping the global plant-based nutrition landscape, appealing to health-conscious, eco-aware, and flexitarian consumers. Its versatility across beverages, bars, and fortified foods positions it as a strategic ingredient for innovation-driven food and beverage companies.

Key Industry Highlights:

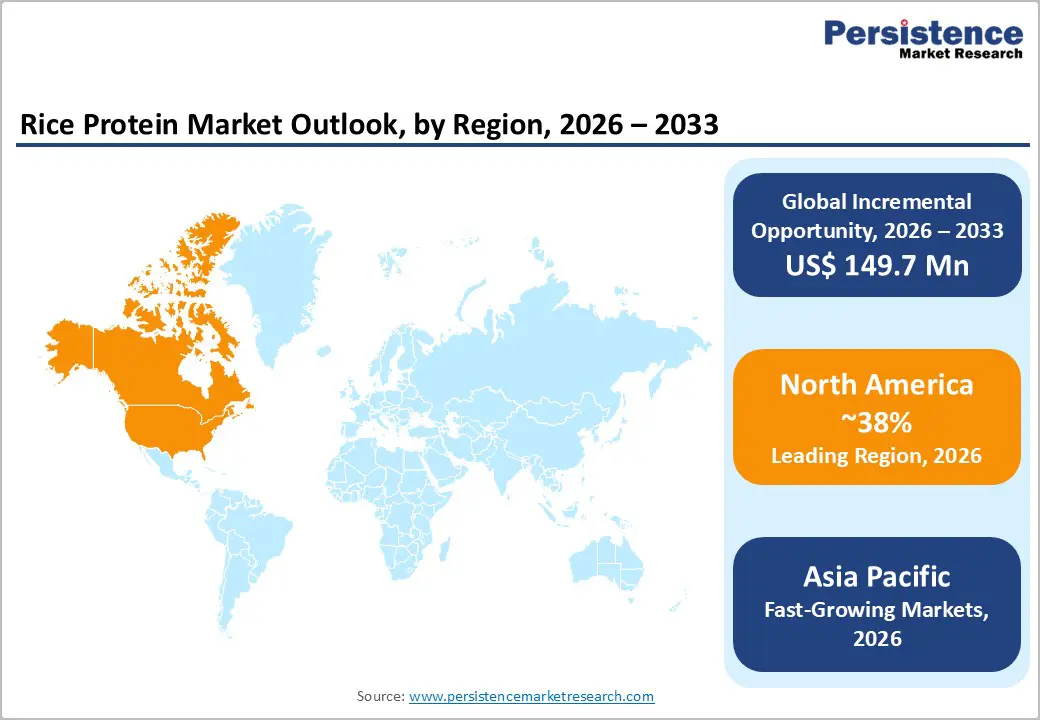

- Leading Region: North America, holding 38% market share, driven by strong adoption of plant-based, hypoallergenic, and fortified protein products, along with clean-label and sustainability-focused consumer demand.

- Fastest-Growing Region: Asia Pacific, fueled by urbanization, rising health awareness, and growing incorporation of rice protein in functional beverages, nutrition bars, and convenient meal solutions across India, China, Japan, and South Korea.

- Fastest-Growing Form Segment: Isolates, driven by high protein concentration, neutral flavor, solubility, and functional versatility in beverages, bars, and nutritional supplements.

- Market Drivers: Rising vegan and flexitarian lifestyles, growing demand for digestive wellness, clean-label ingredients, and sustainable protein sources across retail, foodservice, and health-focused channels.

- Opportunities: Innovation in neutral-flavored rice protein isolates and organic variants enables premium positioning, product differentiation, and entry into beverages, bars, and ready-to-drink formats for startups and established players.

- Key Developments: In July 2025, BENEO partnered with Rikolto and CarbonFarm to support sustainable rice production in Vietnam. In January 2025, Axiom Foods launched Oryzatein® 2.0, a grit-free rice protein for clean-label formulations. In May 2024, Müller renewed its partnership with footballer Declan Rice for the ‘Rice, Rice Baby’ campaign to expand category growth.

| Key Insights | Details |

|---|---|

| Global Rice Protein Market Size (2026E) | US$ 227.1 Mn |

| Market Value Forecast (2033F) | US$ 376.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Driver - Growth of vegan and flexitarian lifestyles driving adoption across diverse food and beverage categories

A surge in vegan and flexitarian lifestyles is transforming consumer choices, redefining protein sourcing across the global food and beverage spectrum. With more individuals reducing animal-based products, rice protein emerges as a versatile alternative that meets dietary preferences while delivering essential amino acids. Its neutral flavor and clean-label appeal enable seamless incorporation into beverages, bars, and bakery products, catering to evolving taste expectations.

Food manufacturers are responding by launching protein-enriched snacks, dairy alternatives, and fortified meal replacements tailored for plant-focused diets. Functional beverages, smoothies, and nutrition bars are increasingly fortified with rice protein to satisfy convenience and health-oriented demands. As awareness of sustainable and ethical protein grows, rice protein adoption expands across retail, foodservice, and health-conscious channels. This shift positions rice protein as a strategic ingredient bridging consumer demand for plant-based nutrition with manufacturers’ innovation goals.

Restraints - Perceived taste and texture challenges compared with whey or soy proteins

Rice protein often faces scrutiny due to its subtle flavor profile and slightly grainy texture compared with whey or soy proteins, influencing formulation decisions. Consumers accustomed to smooth, creamy, or highly soluble protein sources may perceive rice protein as less palatable in certain beverages or food applications. This sensory gap can limit adoption in competitive segments like protein shakes or meal replacements.

Formulators must navigate challenges in masking earthy notes, improving mouthfeel, and ensuring consistent solubility, particularly in cold or ready-to-drink formats. Without effective sensory optimization, rice protein products risk lower acceptance among mainstream consumers. This restraint necessitates targeted ingredient development, blending strategies, and flavor innovation to overcome inherent taste and texture limitations. Persistent attention to product experience is crucial to elevate rice protein’s market positioning and broaden its functional application.

Opportunity - Innovation in neutral-flavored rice protein isolates for easier integration into beverages, bars, and ready-to-drink formats

The taste and texture limitations of rice protein present unique opportunities for innovation-driven companies. By developing enhanced solubility, smoother mouthfeel, and neutralized flavor profiles, manufacturers can differentiate products in competitive protein markets. Functional blends, encapsulation technologies, and texturization strategies enable rice protein to mimic the sensory qualities of whey or soy, broadening consumer appeal.

Startups and established players can exploit this gap by creating specialized formulations for beverages, ready-to-eat meals, and plant-based dairy alternatives. Enhanced organoleptic properties unlock premium positioning and allow rice protein to enter segments previously dominated by traditional proteins. Marketing strategies emphasizing clean-label, hypoallergenic, and sustainable benefits combined with sensory improvement can accelerate adoption. Addressing these sensory challenges transforms a perceived limitation into a strategic advantage, fostering product innovation, expanding target markets, and strengthening brand credibility in the growing plant-based protein sector.

Category-wise Analysis

By Form Insights

Isolates hold approx. 68% market share as of 2025, driven by superior protein concentration and functional versatility. Rice protein isolates deliver high purity, neutral taste, and consistent solubility, making them ideal for beverages, bars, and nutritional supplements. Their ability to blend seamlessly into diverse formulations enhances product stability and consumer acceptance across plant-based and wellness-focused categories.

Food manufacturers prefer isolates due to their predictable performance under varied processing conditions, enabling precise dosing and targeted nutrition profiles. Isolates support high-protein claims, texture consistency, and clean-label positioning without compromising flavor or mouthfeel. This performance advantage reinforces their dominance over concentrates and flour forms. As demand for protein-enriched products rises globally, isolates remain the preferred choice, bridging sensory quality, functional performance, and formulation flexibility, solidifying their leadership in the global rice protein market.

By Nature Insights

Organic Rice Protein are projected to reach a CAGR of 10.4% during the forecast period, fueled by rising consumer preference for natural, minimally processed ingredients. The organic segment appeals to health-conscious buyers seeking sustainable, clean-label nutrition in beverages, snacks, and plant-based meal solutions. Certifications for organic sourcing strengthen consumer trust and provide differentiation in crowded protein markets.

Food and beverage companies increasingly incorporate organic rice protein into fortified bars, dairy alternatives, and functional beverages to meet evolving lifestyle demands. Its hypoallergenic nature and environmental benefits amplify appeal across wellness-focused and eco-conscious segments. Expansion of certified organic rice cultivation and processing infrastructure supports supply stability and product scalability. Together, these factors position organic rice protein as a premium, fast-growing segment aligned with both consumer trends and strategic growth initiatives for key players and emerging startups.

Regional Insights

North America Rice Protein Market Trends

North America holds approximately 38% market share in the global rice protein market, driven by strong consumer interest in plant-based nutrition and functional wellness products. In the U.S., demand centers on clean-label, hypoallergenic, and fortified protein solutions, spurring innovation in beverages, bars, and meal replacements. Functional applications emphasize digestive health, energy support, and sustainable sourcing, appealing to both vegan and flexitarian populations.

Canada reflects a rising preference for organic, non-GMO, and environmentally responsible proteins, supported by transparent labeling and retailer initiatives. Companies are expanding product portfolios through fortified snacks, dairy alternatives, and ready-to-drink beverages, emphasizing protein quality and taste optimization. Strong collaboration between ingredient suppliers and food manufacturers accelerates new launches. These trends highlight North America as a mature, innovation-driven market where consumer expectations, sustainability focus, and regulatory clarity intersect, sustaining rice protein demand and shaping product development strategies.

Asia Pacific Rice Protein Market Trends

Asia Pacific rice protein market is expected to grow at a CAGR of 9.6%, driven by increasing health awareness and urbanized lifestyles. In India, rising consumption of protein-enriched beverages, nutrition bars, and fortified staples stimulates demand for rice protein. China sees growth in functional beverages and convenient meal solutions incorporating plant-based proteins, reflecting evolving dietary preferences.

Japan emphasizes quality, digestive benefits, and precise formulation standards, favoring rice protein in wellness-focused foods and supplements. South Korea’s young, health-conscious consumers drive adoption in functional snacks, dairy alternatives, and ready-to-drink protein drinks. Expansion of modern retail channels and e-commerce enhances accessibility of rice protein products across the region. Combined, these trends indicate strong regional potential, with rice protein positioned as a clean-label, hypoallergenic, and sustainable protein solution meeting diverse dietary needs in the Asia Pacific’s rapidly evolving food and beverage landscape.

Competitive Landscape

The global Rice Protein Market is moderately fragmented, featuring multinational ingredient suppliers alongside regional processors. Leading companies focus on strategic partnerships with food manufacturers, ensuring consistent quality, supply reliability, and tailored product solutions for the growing plant-based sector. Production expansion emphasizes functional performance, taste optimization, and clean-label compliance.

Product innovation targets solubility, amino acid profile enhancement, and sensory improvement. Sustainability initiatives optimize rice utilization, reduce waste, and promote responsible sourcing. Certifications for organic, non-GMO, and hypoallergenic standards enhance credibility across health-conscious and regulatory-conscious markets. B2B collaborations drive co-development of fortified beverages, snacks, and supplements. Compliance with regional food safety regulations shapes formulation and labeling strategies. Competitive advantage increasingly hinges on innovation, technical expertise, and long-term partnerships, allowing both established players and emerging startups to capture growth in the expanding global rice protein industry.

Key Developments:

- In July 2025, BENEO teamed up with Rikolto and CarbonFarm to launch a three-year project supporting sustainable rice production in Vietnam. The initiative is funded by the Government of Flanders to drive climate-friendly agricultural practices.

- In January 2025, Axiom Foods launched Oryzatein® 2.0, a white, grit-free rice protein with extra low heavy metal content. The upgrade targets clean-label and allergen-friendly protein formulations for food and beverage manufacturers.

- In May 2024, Müller renewed its partnership with footballer Declan Rice, rolling out the next phase of its ‘Rice, Rice Baby’ campaign. The initiative aims to boost Müller Rice Protein sales and expand category growth.

Companies Covered in Rice Protein Market

- Cargill,Incorporated

- IFF

- Glanbia plc

- Ingredion

- Kerry Group Plc

- Tate & Lyle

- Axiom Foods, Inc.

- Roquette Frères

- BENEO

- Louis Dreyfus Company

- Others

Frequently Asked Questions

The global rice protein market is projected to be valued at US$ 227.1 Mn in 2026.

Growth of vegan and flexitarian lifestyles driving adoption across diverse food and beverage categories driving growth in the global Rice Protein market.

The global rice protein market is poised to witness a CAGR of 7.5% between 2026 and 2033.

Innovation in neutral-flavored rice protein isolates for easier integration into beverages, bars, and ready-to-drink formats presenting significant growth opportunities for companies in the Rice Protein market.

Major players in the global Rice Protein market include Cargill,Incorporated, IFF, Glanbia plc, Ingredion, Kerry Group Plc, Tate & Lyle, Axiom Foods, Inc., and others