- Beauty & Personal Care

- Rice-based Skincare Products Market

Rice-based Skincare Products Market Size, Share, and Growth Forecast 2026 - 2033

Rice-based Skincare Products Market by Product Type (Cleansers & Toners, Moisturizers & Creams, Face Masks, Exfoliators & Scrubs, Sunscreens, Others), End-user (Women, Men, Kids), Distribution Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Rice-based Skincare Products Market Size and Trend Analysis

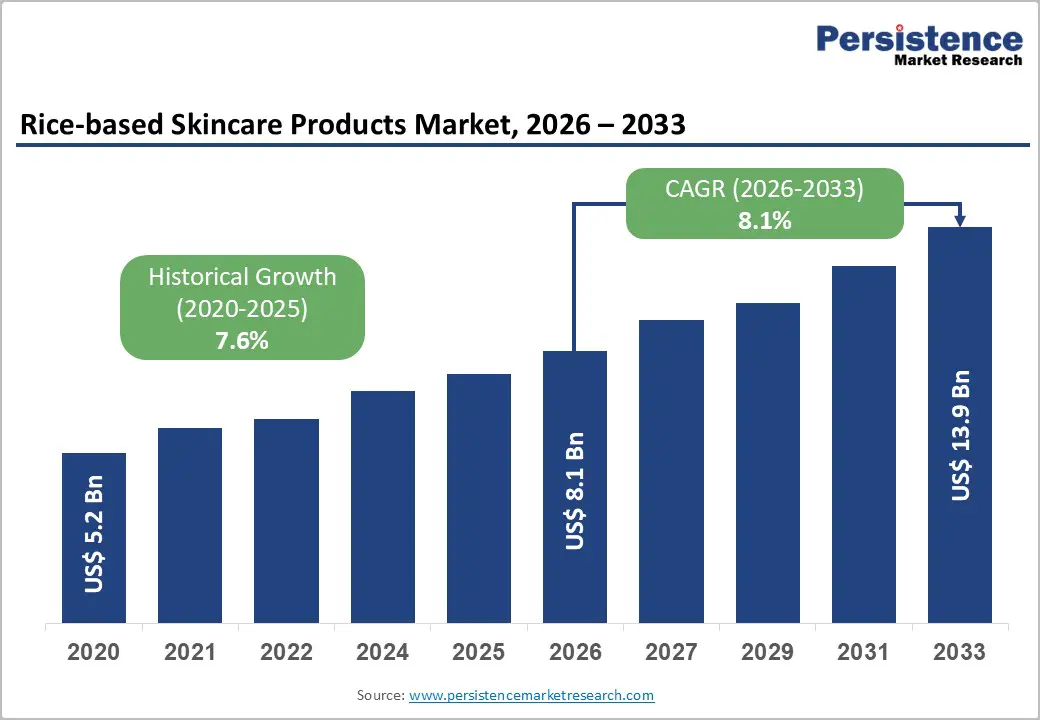

The global rice-based skincare products market size is supposed to be valued at US$ 8.1 billion in 2026 and is projected to reach US$ 13.9 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033.

This growth outlook builds on a strong base of consumers shifting toward clean, plant-based beauty and the global diffusion of K-beauty and J-beauty, where rice water, rice bran oil, and fermented rice actives are central to brightening, anti-aging, and barrier-repair routines. Clinical and dermatological evidence shows that rice-derived compounds such as phenolic acids, betaine, squalene, and tricin deliver antiaging, anti-inflammatory, whitening, photoprotective and moisturizing benefits while remaining non-irritating and hypoallergenic, reinforcing trust in rice-based ingredients.

Key Industry Highlights:

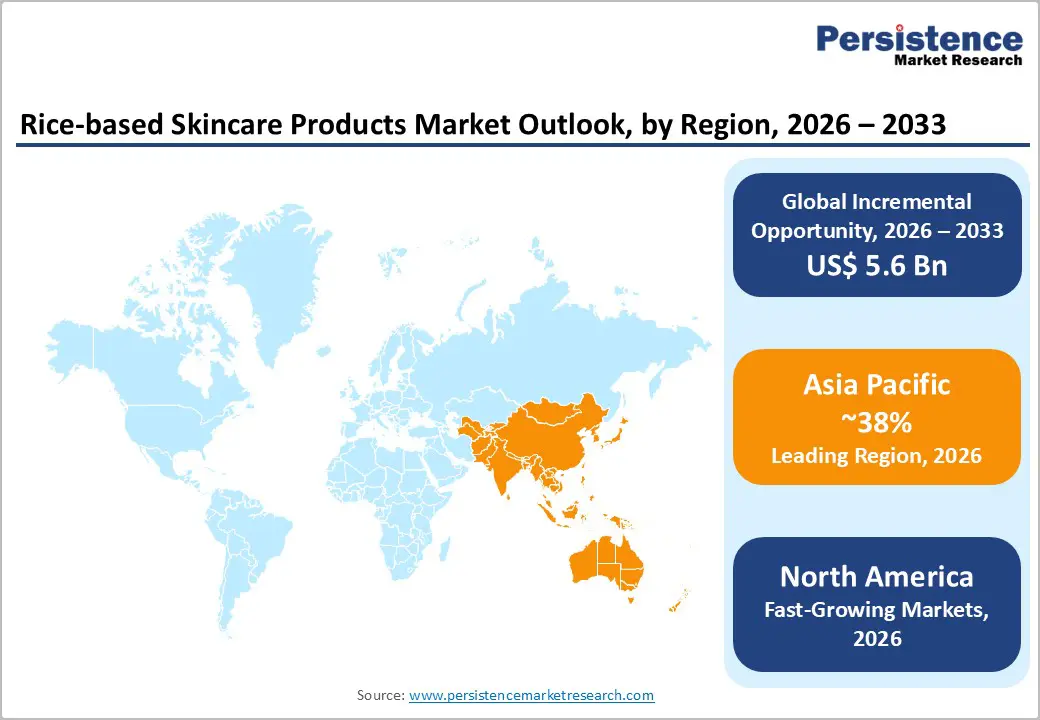

- Leading Region: Asia Pacific leads the Rice-based Skincare Products Market with around 38% share, leveraging deep cultural heritage in rice-based beauty rituals and strong manufacturing bases in Japan, South Korea, China, and India, which collectively drive innovation and global exports.

- Fastest Growing Region: North America, led by the United States, is a fast-growing market where rice-based skincare is riding the broader wave of clean, science-backed beauty.

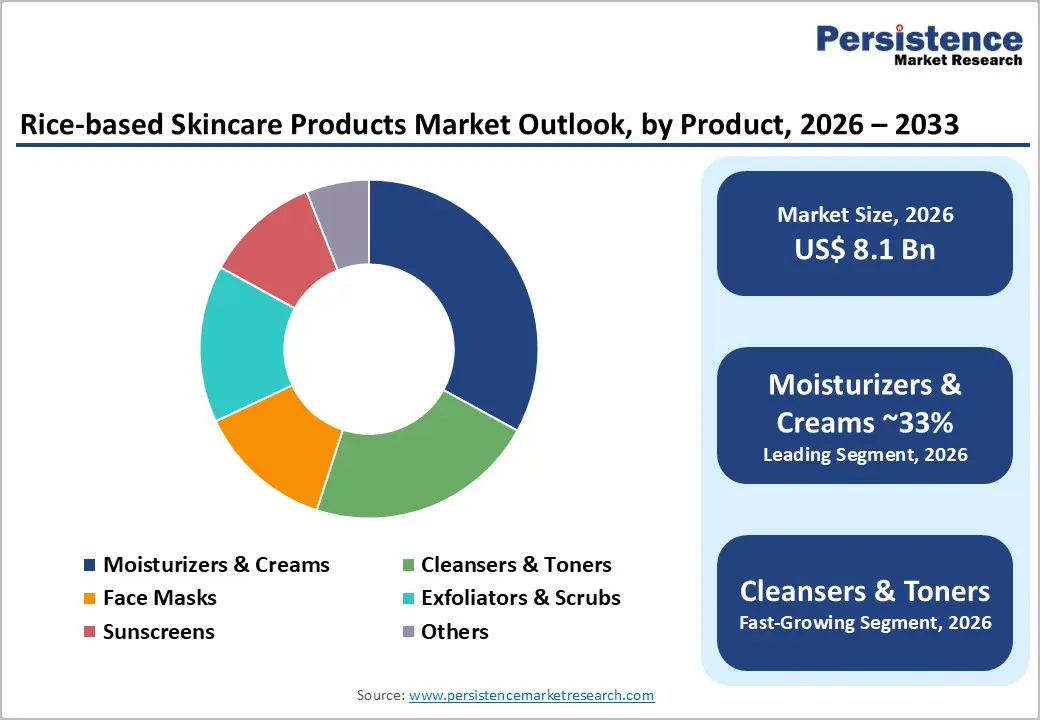

- Dominant Segment: Moisturizers & Creams hold the largest product-type share at about 33%, as rice-based actives align perfectly with hydration, brightening and barrier-support claims sought in everyday cream usage across age groups and skin types.

- Fastest Growing Segment: Within product types, Face Masks are expanding the fastest, riding global enthusiasm for K-beauty-inspired sheet masks and wash-off treatments that promise visible radiance and “glass skin” with rice-based brightening complexes.

- Key Market Opportunity: The Men’s Grooming space, with men’s facial skincare at USD 19.6 Bn in 2024 and set to reach USD 31.7 Bn by 2034 at 4.9% annual growth, offers high-margin upside for rice-based, hypoallergenic, low-fragrance formulations tailored specifically to male skin concerns.

| Key Insights | Details |

|---|---|

| Rice-based Skincare Products Market Size (2026E) | US$ 8.1 Bn |

| Market Value Forecast (2033F) | US$ 13.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Dynamics

Drivers - Scientific Validation and Clean Beauty Movement Accelerating Consumer Adoption

The clean beauty movement is now firmly mainstream, and rice-based formulations sit at the intersection of “natural” positioning and scientific validation. A peer-reviewed study in the Journal of Cosmetic Dermatology reported that individual rice components, including phenolic compounds, betaine, squalene, tricin, and rice bran, demonstrate antiaging, anti-inflammatory, whitening, photoprotective and moisturizing benefits, and are safe, non-irritating, and hypoallergenic. This evidence is complemented by laboratory research on fermented red rice extracts, which show antioxidative, moisturizing, and brightening effects, creating a strong rationale for using fermented rice in premium serums and creams. As consumers increasingly scrutinize INCI lists and seek clinically supported botanical actives, rice-derived ingredients provide a credible bridge between traditional Asian beauty practices and modern dermatological science, encouraging the adoption of rice-based cleansers, toners, and moisturizers in daily routines.

K-beauty and J-beauty Global Influence Driving Cross-Border Demand

K-beauty and J-beauty have transformed the global skincare landscape, and rice-based products are among the biggest beneficiaries. The global K-beauty market is estimated at about USD 12.39 Bn in 2024, projected to grow at around 8.4% CAGR through 2034, underscoring the structural nature of demand for Korean skincare formats and ingredients. Korean and Japanese brands such as Beauty of Joseon, Innisfree, and Tony Moly have heroed rice water and rice extract across essences, serums, and creams, with many products going viral on TikTok and Instagram. The BBC highlighted in January 2026 that K-beauty has evolved from a trend into an economic powerhouse, reflecting long-term consumer engagement rather than short-lived hype. As these brands scale through cross-border e-commerce, multi-brand retailers, and duty-free channels, they effectively educate global consumers about the benefits of rice-based skincare, directly supporting growth in the rice-based skincare products market.

Restraints - Raw Material Price Volatility and Supply Chain Uncertainty

The rice-based skincare value chain is exposed to agricultural volatility and trade policy risk, both of which can impact raw material availability and pricing. In 2023, India, the world’s largest rice exporter, imposed curbs on exports of certain non-basmati rice categories to stabilize domestic availability and prices, tightening global supply. Climate-related disruptions, such as irregular monsoons and flooding in major producers like India, Vietnam, and Thailand, further exacerbate price swings and quality variability. For cosmetic formulators relying on specific rice varieties or organic-certified rice, this volatility can raise input costs and complicate secure sourcing, particularly for smaller and indie brands with limited supplier diversification. These cost pressures make it harder to maintain stable pricing and margins in price-sensitive markets, slowing expansion in the lower and mid-price skincare segments.

Regulatory Complexity Across Key Markets

Rice-based skincare brands must navigate a tightening web of cosmetic regulations, especially in Europe, where compliance burdens are high. Under Regulation (EC) No. 1223/2009, cosmetic products must undergo rigorous safety assessment, maintain a Cosmetic Product Safety Report, and comply with strict labeling rules. In 2023, Regulation (EU) 2023/1545 added more than 60 substances to restricted or banned lists, reflecting the EU’s ongoing vigilance over potential allergens and hazardous chemicals in cosmetics. In parallel, the EU Deforestation Regulation (EUDR) (EU) 2023/1115 imposes new due-diligence obligations for agricultural commodities, pushing brands to prove traceability and low-deforestation risk for plant-derived inputs. While rice is not currently the primary focus of all these rules, the broader compliance environment demands more documentation, testing, and supply-chain transparency, raising time-to-market and compliance costs for smaller players in the Rice-based Skincare Products Market.

Market Opportunities

Men’s Grooming Segment Emerging as a High-Value Growth Frontier

The men’s grooming market is undergoing a structural shift toward skincare, and natural formulations are at the center of this transition. According to NATRUE, the global men’s facial skincare market reached USD 19.6 Bn in 2024 and is expected to grow to USD 31.7 Bn by 2034, at an average annual growth rate of 4.9%. Men’s use of facial skincare products has increased sharply in both the U.S. and major European markets, supported by changing norms and rising emphasis on wellbeing and appearance. Within this context, certified natural and plant-based formulations are gaining traction as male consumers increasingly associate “clean” ingredients with safety, sustainability, and authenticity. Rice-based skincare, being gentle, non-irritating and suitable for shaven, thicker male skin, is well-positioned to capture this opportunity via targeted SKUs such as soothing post-shave moisturizers, oil-control rice water toners, and minimalist, fragrance-light creams marketed specifically to men.

Expanding E-commerce and Social Commerce Channels Creating New Market Access Points

The rapid expansion of e-commerce and social commerce is structurally favorable for ingredient-led niche categories such as rice-based skincare. Global online beauty sales are estimated at USD 65,111 Bn by 2025, with skincare accounting for roughly 39,400% of beauty e-commerce revenue. In China and South Korea, online penetration of beauty purchases is approaching or exceeding 50%, while in India, beauty e-commerce sales rose 39% year-on-year between June and November 2024, compared with 3% growth in offline channels. This shift particularly benefits rice-based brands, which rely on education and storytelling about heritage, fermentation technologies, and clinical benefits; formats such as long-form product pages, influencer videos, and social “before-and-after” content work far better online than on crowded shelves.

Category-wise Analysis

Product Type Insights

Among product types, moisturizers & creams represent the leading segment in the Rice-based Skincare Products Market, with an estimated share of around 33% of global revenue. This is consistent with their central role in daily skincare regimens and with the multi-functional nature of rice-based actives, which combine hydration, barrier reinforcement, brightening, and soothing properties in a single product. Rice bran oil and rice water are rich in antioxidants, vitamins, and lipids that support the skin barrier and address dullness, making them ideal for day and night creams that target both short-term radiance and long-term anti-aging. Premium brands such as Tatcha (with products like The Dewy Skin Cream) and high-end Korean and Japanese labels have used rice-based moisturizers as anchor SKUs in their ranges, fueling awareness and encouraging mass brands to follow with affordable rice-infused creams.

End-user Insights

The Women segment is the dominant end-user group, accounting for roughly 72% of revenues in the Rice-based Skincare Products Market. Historically, women have been the primary purchasers and users of skincare, and rice-based rituals are deeply embedded in Asian feminine beauty heritage, from Japanese “nuka-bukuro” rice-bran bags to Korean rice-water rinses. Contemporary female consumers, especially in East Asia, North America and Europe, are increasingly willing to pay for ingredient-transparent, clinically supported products, a trend that aligns strongly with the evidence-based benefits of rice-derived actives. Women also over-index on multi-step routines (cleansing, toning, essence, serum, cream, mask), creating more touchpoints for rice-based SKUs within a single regimen.

The Men segment is the fastest-growing end-user group, supported by data showing sharp increases in male facial skincare usage and higher openness to natural, low-irritation formulas, pointing to meaningful upside for rice-based launches tailored to men’s needs.

Distribution Channel Insights

The online distribution channel has emerged as the leading route to market for rice-based skincare, with an estimated 57% share of global sales and a clear upward trajectory. Several structural trends are pushing this: the growth of digital-native K-beauty brands, the role of social media and influencers in product discovery, and the ability of cross-border marketplaces to bring Korean and Japanese rice-based products to Western and emerging-market consumers. E-commerce allows brands to communicate detailed ingredient benefits, showcase user reviews and clinical data, and offer bundles or subscriptions that encourage trial and repeat purchases, which is especially valuable for a category like rice-based skincare that depends on education. Offline channels remain important for sensory trial and premium positioning in department stores and specialty chains, but the strongest incremental growth momentum in the Rice-based Skincare Products Market is clearly concentrated in online and social commerce ecosystems.

Regional Insights

North America Rice-Based Skincare Products Market Trends

North America, led by the United States, is a fast-growing market where rice-based skincare is riding the broader wave of clean, science-backed beauty. Consumers are highly engaged with ingredient-level claims, and there is a strong overlap between interest in non-irritating, fragrance-light formulations and the properties documented for rice-derived actives in dermatology literature.

Large multinationals are validating and scaling the category in North America. Tatcha, although inspired by Japanese rituals, is headquartered in the U.S. and has achieved strong double-digit growth through retailers such as Sephora, with signature rice-based products like The Rice Wash and The Dewy Skin Cream regularly featured in editorial and influencer lists. Global CPG leaders such as Procter & Gamble and Unilever have launched rice water-based cleansers and moisturizers in recent years, signaling confidence in consumer demand for rice-derived actives.

Europe Rice-based Skincare Products Market Trends

In Europe, demand for rice-based skincare is underpinned by strong interest in natural, organic and ethically sourced cosmetics. Markets such as Germany, France, the U.K. and Spain exhibit high penetration of certified natural and organic labels, and frameworks like COSMOS and NATRUE help structure the segment. Rice-based formulations, particularly those that are minimally processed and free from controversial preservatives and fragrances, fit well within this regulatory and consumer context.

European specialty retailers and e-commerce platforms have expanded their Korean and Japanese brand assortments, making rice-based essences, creams and masks widely accessible. At the same time, local European brands are increasingly experimenting with rice extract as a gentle alternative in brightening or barrier-support formulas, often pairing it with oat, ceramides, or niacinamide. Sustainability narratives around rice as a renewable agricultural resource, plus heightened focus on packaging recyclability and ethical sourcing, are differentiators for rice-based products in European markets, contributing to steady growth from a relatively smaller base compared to Asia.

Asia Pacific

Asia Pacific is the largest and most mature region in the Rice-based Skincare Products Market, accounting for an estimated 38% share of global revenues. This leadership is rooted in both cultural heritage and industrial capability. Historical use of rice water for hair and skin care in Japan and Korea, as well as grain-based beauty rituals in China and India, has created deep familiarity and trust in rice as a cosmetic ingredient. Beauty consumers in South Korea and Japan are among the most sophisticated globally, encouraging rapid innovation in fermented rice technologies, encapsulation and combination of rice actives with other botanicals or actives, which then diffuse internationally via K-beauty and J-beauty exports.

The region also benefits from structural manufacturing advantages: it includes the top rice producers, such as China, India, Vietnam, Thailand, and Indonesia, enabling tight integration of agricultural sourcing and cosmetic production. Korean brand MIDHA’s launch of a line based on “MIDHA Rice 8 Complex” in 2024, and other launches using patented fermented rice complexes, illustrate the ongoing move toward IP-protected rice technologies. At the same time, rapid growth in beauty e-commerce, especially India’s 39% rise in online beauty sales in 2024, is expanding reach to younger and more rural consumers.

Competitive Landscape

The Rice-based Skincare Products Market is semi-fragmented, with a blend of multinational corporations, large regional champions, and a long tail of indie and niche brands. Major Asian and Japanese brands such as Shiseido, Sulwhasoo, Innisfree, The Face Shop, and Kose Corporation compete alongside premium global brands like Tatcha and indie labels that emphasize heritage and minimalism. Key strategic levers include proprietary fermentation or extraction technologies, the use of specific regional rice varieties as a branding story, strong clinical or consumer-use evidence, and sustainability (organic rice, traceable sourcing, eco-packaging).

Key Developments:

- In February 2025, Zen Dew introduced the Violet Aura 2% BHA Rice Toner, combining Korean rice extract, azulene, niacinamide, and salicylic acid. This leave-on toner aims to brighten, hydrate, and smooth the skin while reducing inflammation and minimizing pores. It's suitable for all skin types and has received positive reviews for its gentle formulation.

- In February 2024, Cécred, a haircare brand launched by Beyoncé, debuted the Fermented Rice & Rose Protein Ritual. This product harnesses fermented rice water and rose protein to nourish and repair hair, drawing inspiration from global hair rituals. It has been recognized for its innovative approach to hair health.

Companies Covered in Rice-based Skincare Products Market

- Tatcha

- The Face Shop

- Skinfood

- Innisfree

- Shiseido

- JUARA Skincare

- MIRABELLE COSMETICS Pvt. Ltd

- GLAMVEDA

- Kose Corporation

- Etude House

- Beauty of Joseon

- TonyMoly

- Sulwhasoo

- Neogen Dermalogy

- Skin Inc.

- Other Key Players

Frequently Asked Questions

The global Rice-based Skincare Products Market is supposed to be valued at US$ 8.1 Bn in 2026 and is projected to reach US$ 13.9 Bn by 2033, expanding at a CAGR of 8.1% over 2026 - 2033.

Key growth drivers include the clean beauty movement, increasing dermatological evidence of rice-derived actives’ antiaging, anti-inflammatory and moisturizing benefits, and the global influence of K-beauty and J-beauty brands that popularize rice water and fermented rice extracts.

The Moisturizers & Creams segment leads the market with roughly 33% share, leveraging rice bran oil, rice water and fermented rice actives to deliver hydration, brightening, and barrier-strengthening benefits aligned with daily skincare needs.

Asia Pacific dominates the market with about 38% share, driven by deep-rooted cultural usage of rice in beauty rituals, leading innovation ecosystems in Japan and South Korea, and large, fast-growing consumer bases in China and India.

Key players include Tatcha, Shiseido Co., Ltd., Sulwhasoo (Amorepacific Group), Innisfree, The Face Shop, Skinfood, Beauty of Joseon, TonyMoly, Kose Corporation, Etude House, JUARA Skincare, MIRABELLE COSMETICS Pvt. Ltd., GLAMVEDA, Neogen Dermalogy and Skin Inc., among others.