- Industrial Goods & Service

- Power Hand Tools Market

Power Hand Tools Market Size, Share, and Growth Forecast, 2025 - 2032

Power Hand Tools Market by Mode of Operation (Electric Tools, Pneumatic Tools, Others), Application (Industrial, Residential), Product Type (Drills, Saws, Wrenches, Grinders, Sanders, Others), and Regional Analysis for 2025 - 2032

Power Hand Tools Market Forecast and Trends Analysis

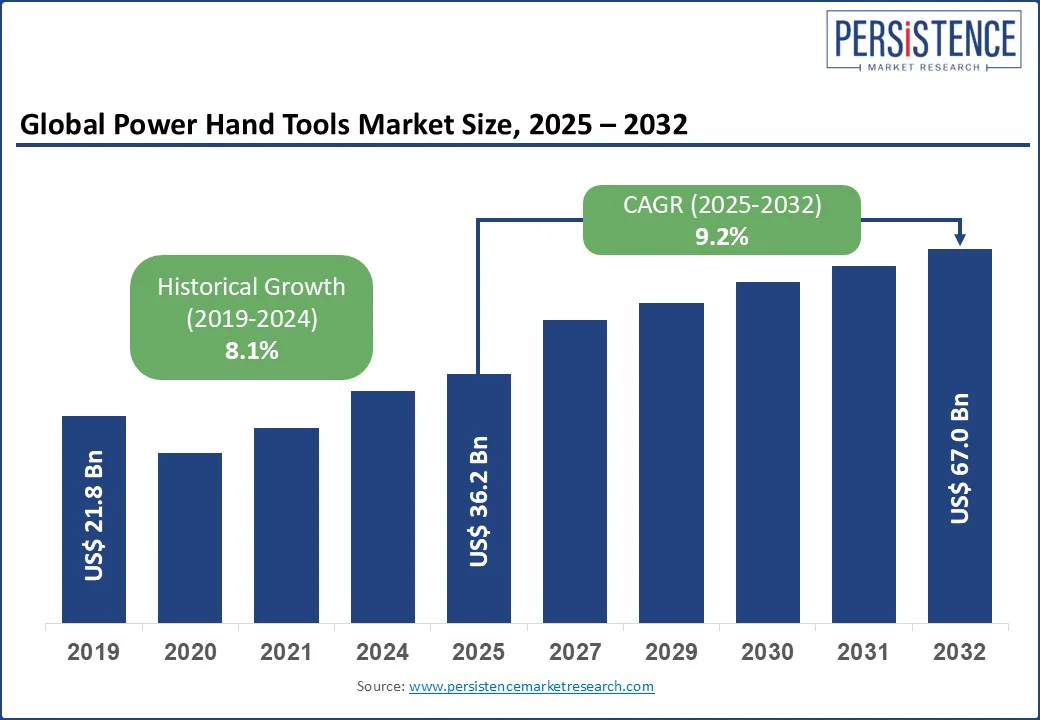

The global Power Hand Tools Market size is likely to value at US$ 36.2 Bn in 2025 to US$ 67.0 Bn by 2032, registering a CAGR of 9.2% during the forecast period 2025 - 2032.

The Power Hand Tools industry has experienced robust growth, driven by increasing DIY activities, rising construction and manufacturing sectors, and advancements in cordless technology. Power hand tools, including drills, saws, and grinders, offer portability and efficiency for industrial and residential applications.

Key Power Hand Tools Industry Highlights:

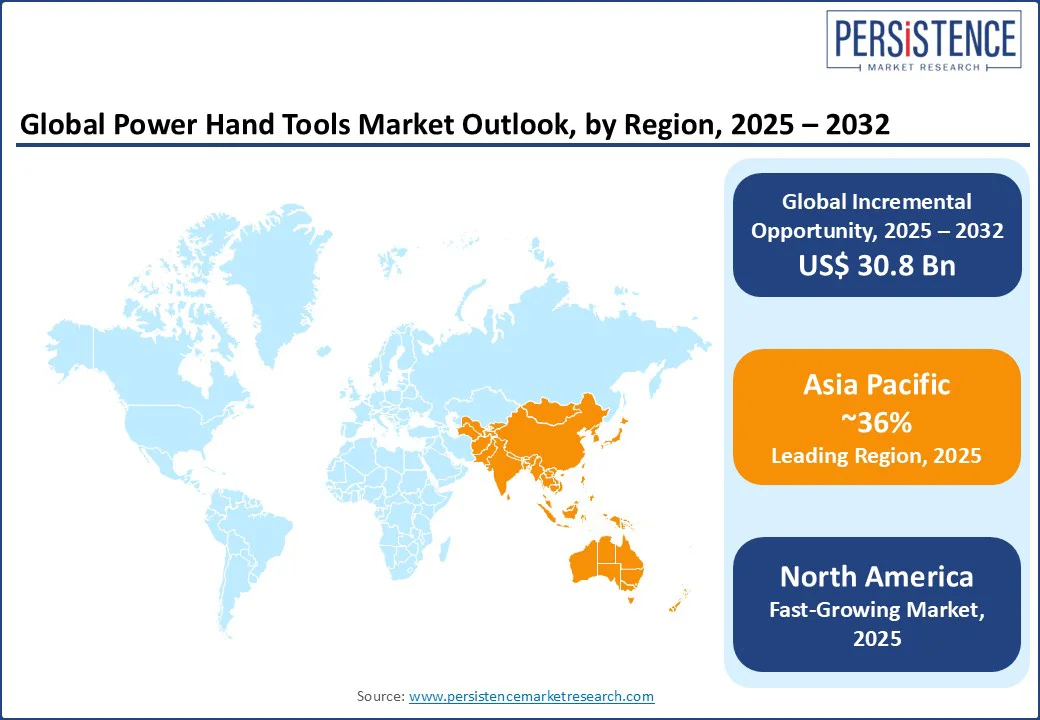

- Leading Region: Asia Pacific holds a 36% market share in 2025, supported by robust manufacturing infrastructure, rapid urbanization, and high demand for power tools in countries like China and India.

- Fastest-growing Region: North America, driven by a strong DIY culture, technological innovations in cordless tools, and increasing construction activities.

- Investment Trends: Europe is focusing on sustainable and ergonomic tools, backed by regulatory frameworks like the EU’s Green Deal and consumer demand for eco-friendly products.

- Dominant Mode of Operation: Electric tools account for nearly 65% of the global Power Hand Tools market share, driven by advancements in lithium-ion batteries for cordless operation.

- Leading Application: Industrial applications lead with a 63% share, reflecting high demand in manufacturing and construction.

- Consumer Trend: Cordless and smart tools are gaining traction, driven by demand for portability, efficiency, and integration with IoT for professional and DIY users.

|

Global Market Attribute |

Key Insights |

|

Power Hand Tools Market Size (2025E) |

US$ 36.2 Bn |

|

Market Value Forecast (2032F) |

US$ 67.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.1% |

Power Hand Tools Market Dynamics

Driver- Rising DIY Activities and Construction Boom Push Demand

The global increase in DIY activities and home improvement projects is a key driver of the power hand tools market. With urbanization and rising disposable incomes, consumers are increasingly taking on DIY tasks, leading to higher demand for cordless drills, saws, and other versatile tools. In the U.S., a growing number of homeowners are engaging in home improvement projects, while in Europe, there is a clear preference for user-friendly electric tools that cater to both professionals and hobbyists.

The expansion of the construction and manufacturing sectors is also fueling market growth. Rising global construction activity is increasing the demand for pneumatic and electric tools in industrial applications. In the Asia Pacific, large-scale infrastructure projects, such as China’s Belt and Road Initiative, are further driving the use of equipment like pneumatic wrenches and grinders.

Government initiatives aimed at strengthening the manufacturing and construction sectors are providing a significant boost to the power hand tools market. In India, programs promoting industrial automation are encouraging industries to adopt advanced tools to enhance productivity, reduce labour dependency, and improve precision in operations.

This is fostering demand across sectors such as automotive, metalworking, and furniture manufacturing. For instance, India has seen an exponential increase in infrastructure spending, with budgetary allotments reaching INR 10 lakh crore in 2023-2024. In the U.S., large-scale infrastructure development programs are driving the need for high-performance, durable tools capable of handling heavy-duty applications. These policies not only stimulate market growth but also encourage innovation, leading to the development of more efficient, ergonomic, and technologically advanced power tools.

Restraint- High Costs and Safety Concerns Restrict Adoption

High initial costs of advanced power hand tools remain a significant barrier to market growth, particularly for residential users and small enterprises. Cordless tools with lithium-ion batteries, such as Makita’s 18V series, can be expensive, and the cost of replacement batteries further adds to overall expenses. These price factors limit adoption in cost-sensitive markets, especially in rural areas of Asia Pacific and Latin America.

Safety concerns and regulatory compliance also act as obstacles to market expansion. Power tools can cause injuries if misused, prompting strict safety regulations such as the EU’s Machinery Directive, which requires the integration of protective features. For instance, in the European Union, the Machinery Directive (2006/42/EC) establishes essential health and safety requirements for machinery sold or placed on the Power Hand Tools market, mandating features like guarding, emergency stops, and CE marking to ensure compliance. While these measures enhance user safety, they also increase production costs, creating additional challenges for innovation and adoption in developing regions.

Opportunity- Innovation in Cordless Technology and E-commerce Boosts Consumption

The advancement of cordless technology and battery innovations presents significant opportunities for the power hand tools market. With lithium-ion batteries delivering longer runtimes and improved performance, brands are developing high-voltage tools aimed at professional users. For example, Bosch recently introduced a cordless drill in Europe with enhanced battery life, appealing to construction workers seeking greater efficiency. In North America, companies such as Stanley Black & Decker are exploring solid-state battery technology to further reduce charging times and improve durability.

E-commerce and direct-to-consumer sales channels offer another promising growth avenue. Online platforms like Amazon and Home Depot have expanded access to tools for both professionals and DIY users, creating opportunities for brands to introduce subscription models for batteries and accessories.

The growing focus on sustainability also fuels market opportunities. Eco-friendly tools made with recyclable materials and low-emission motors are increasingly popular among environmentally conscious consumers. For instance, manufacturing businesses in Singapore can receive significant assistance from the Energy Efficiency Fund (E2F) to invest in energy-efficient technologies and implement low-carbon practices. In the Asia Pacific, government initiatives such as India’s PLI scheme for electronics encourage green manufacturing practices, further boosting demand for sustainable power tools.

Category-wise Analysis

By Mode of Operation

The power hand tools market is segmented into Electric Tools, Pneumatic Tools, and Others. Electric tools dominate, holding approximately 65% of the global Power Hand Tools industry share in 2025, due to their versatility, portability, and advancements in cordless technology. Brands like Makita and Bosch have solidified their position with lithium-ion powered drills and saws for both industrial and residential use.

Pneumatic tools are the fastest-growing segment, fueled by their high power-to-weight ratio and suitability for heavy-duty industrial applications. Tools like Ingersoll Rand’s pneumatic wrenches are gaining traction in automotive and construction sectors.

By Application Type

By application, the global Power Hand Tools market is divided into Industrial and Residential. Industrial applications lead, accounting for 63% of the Power Hand Tools market share in 2025, driven by demand in manufacturing, construction, and automotive sectors. High-performance tools like grinders and wrenches are essential for precision tasks.

Residential applications are the fastest-growing segment, fueled by the rise in DIY and home improvement projects. Cordless drills and sanders from Stanley Black & Decker are popular among homeowners for renovation activities.

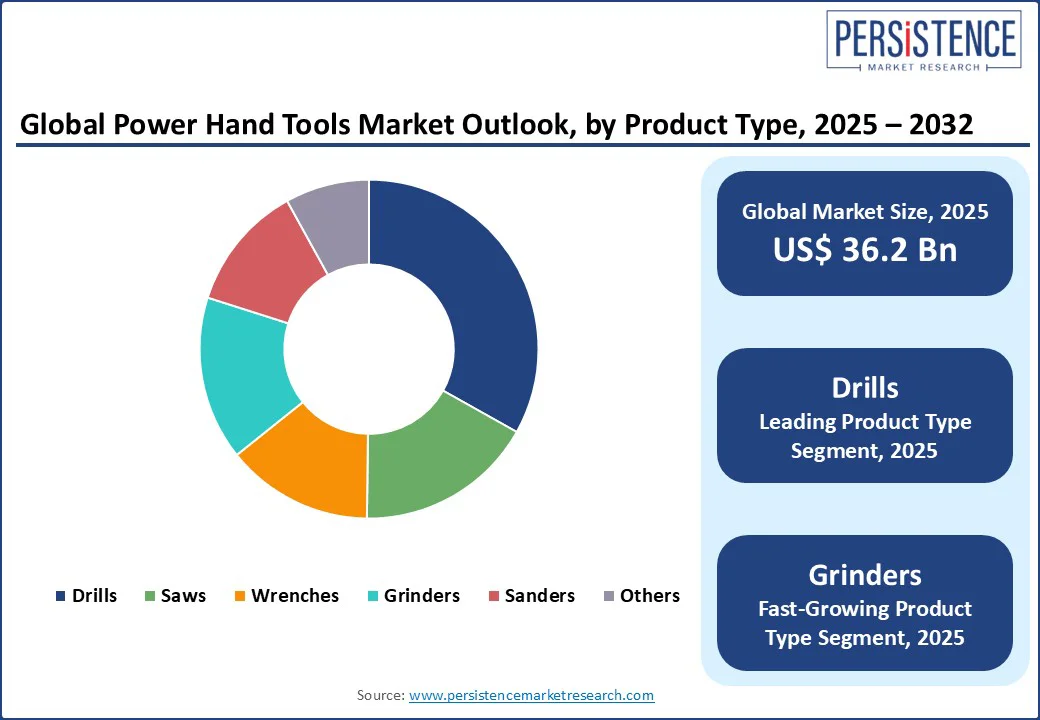

By Product Type

The Power Hand Tools market is segmented into Drills, Saws, Wrenches, Grinders, Sanders, and Others. Drills dominate with a 33.2% share in 2025, due to their versatility in drilling and fastening tasks across industries. Cordless drills from Techtronic Industries are widely used for their efficiency. Grinders are the fastest-growing segment, driven by demand in metalworking and construction. Angle grinders from Hilti offer high-speed performance for cutting and polishing.

Regional Insights

North America Power Hand Tools Market Trends

In North America, the U.S. stands out as the fastest-growing market for power hand tools, driven by a strong do-it-yourself (DIY) culture and a resilient construction industry. The growing adoption of electric cordless tools is being fueled by continuous advancements in lithium-ion battery technology, offering longer runtimes, faster charging, and improved durability. The surge in home renovation activities, spanning everything from small interior upgrades to large-scale remodeling projects, is creating strong demand for versatile tools such as drills, saws, and sanders.

Consumer preferences are evolving toward smart, connected, and ergonomically designed tools that improve efficiency while reducing user fatigue. Leading brands like Stanley Black & Decker are increasingly focusing on IoT-integrated devices that allow for enhanced precision, real-time monitoring, and predictive maintenance. Sustainability is also emerging as a key priority, with companies like Emerson Electric developing low-emission pneumatic tools to reduce environmental impact. Additionally, regulatory incentives promoting green building practices and major infrastructure investments are providing a favorable environment for continued innovation, adoption, and market growth across both professional and residential segments.

Europe Power Hand Tools Market Trends

Europe’s power hand tools market is led by Germany, the U.K., and France, supported by strong regulatory frameworks and rising industrial demand. Germany commands a prominent position, driven by the presence of global brands such as Robert Bosch and Hilti. The European Union’s Green Deal is encouraging the development and adoption of energy-efficient tools, accelerating the shift toward advanced electric and pneumatic models in manufacturing and assembly lines.

In the U.K., demand is fueled by a thriving home renovation culture, where cordless tools dominate the do-it-yourself (DIY) segment due to their convenience, portability, and versatility. France is seeing growth in industrial applications, particularly in the automotive sector, where pneumatic wrenches from companies like Atlas Copco are gaining greater adoption for precision and efficiency.

Regulatory incentives promoting sustainable manufacturing practices are shaping product development strategies across the region. At the same time, rising consumer interest in ergonomically designed tools that reduce fatigue and improve productivity is influencing purchasing decisions, creating favorable conditions for continued market expansion in both professional and residential sectors.

Asia Pacific Power Hand Tools Market Trends

Asia Pacific holds a 36% market share in 2025. In India, rapid urbanization and rising disposable incomes are fueling demand for affordable and efficient electric tools. The country’s expanding construction sector, supported by large-scale government infrastructure initiatives, is creating strong opportunities for both domestic and international tool manufacturers, with companies such as Hitachi Koki playing a prominent role.

China’s market benefits from its position as a global manufacturing hub, with sustained demand for power tools across industrial and commercial applications. Brands like Makita maintain a strong presence, particularly in the cordless drill segment, which is favored for its portability and efficiency. Japan’s market is characterized by its focus on precision-engineered tools, especially for electronics and high-tech industries, with players like Apex Tool Group gaining increased traction.

Competitive Landscape

The power hand tools market is highly competitive, with global players vying for share through innovation, pricing, and distribution. The rise of cordless and smart tools intensifies competition, as consumers demand efficiency and sustainability. Strategic acquisitions and R&D investments are key differentiators.

Key Players

- Makita Corporation

- Robert Bosch Group

- Stanley Black & Decker

- Techtronic Industries Co., Ltd.

- Emerson Electric Co.

- Atlas Copco

- Hilti Corporation

- Ingersoll Rand, Inc.

- Hitachi Koki Co., Ltd.

- Apex Tool Group, LLC

Key Developments

- In September 2024, Milwaukee Tool unveiled next-generation band saws and deep cuts, offering improved user-cutting capabilities. Compared to older models, the new band saws cut 4-inch black iron pipes 20% faster.

- In October 2024, Bosch Power Tools added several new items to its lineup of 18V cordless tools. A palm router, an angle grinder, new-generation interior leveling layers, brand-new first-hand tools, and 18V press tool kits with ergonomic designs, strong brushless motors, and long-lasting durability are among the new tools.

Companies Covered in Power Hand Tools Market

- Makita Corporation

- Robert Bosch Group

- Stanley Black & Decker

- Techtronic Industries Co., Ltd.

- Emerson Electric Co.

- Atlas Copco

- Hilti Corporation

- Ingersoll Rand, Inc.

- Hitachi Koki Co., Ltd.

- Apex Tool Group, LLC

- Others

Frequently Asked Questions

The Power Hand Tools market is projected to reach US$ 36.2 Bn in 2025.

Rising DIY activities, construction boom, and government initiatives are the key market drivers.

The Power Hand Tools market is poised to witness a CAGR of 9.2% from 2025 to 2032.

Innovation in cordless technology and e-commerce expansion are the key market opportunities.

Makita Corporation, Robert Bosch Group, and Stanley Black & Decker are among the key market players.