- Processed Food

- Potato Starch Market

Potato Starch Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Potato Starch Market by Product Type (Modified Potato Starch, Native Potato Starch), Nature (Organic, Conventional), End-user (Food and Beverages, Paper & Packaging, Chemical, Cosmetics & Personal Care, Animal Feed), Distribution Channel (B2B, B2C), and Regional Analysis, 2026 - 2033

Potato Starch Market Share and Trends Analysis

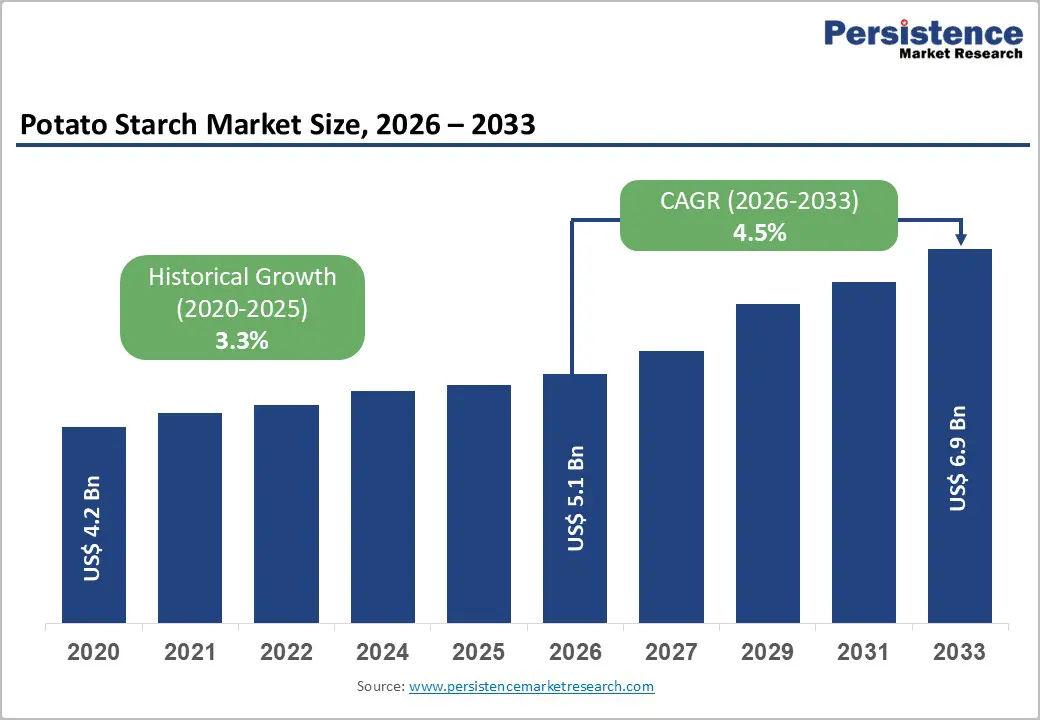

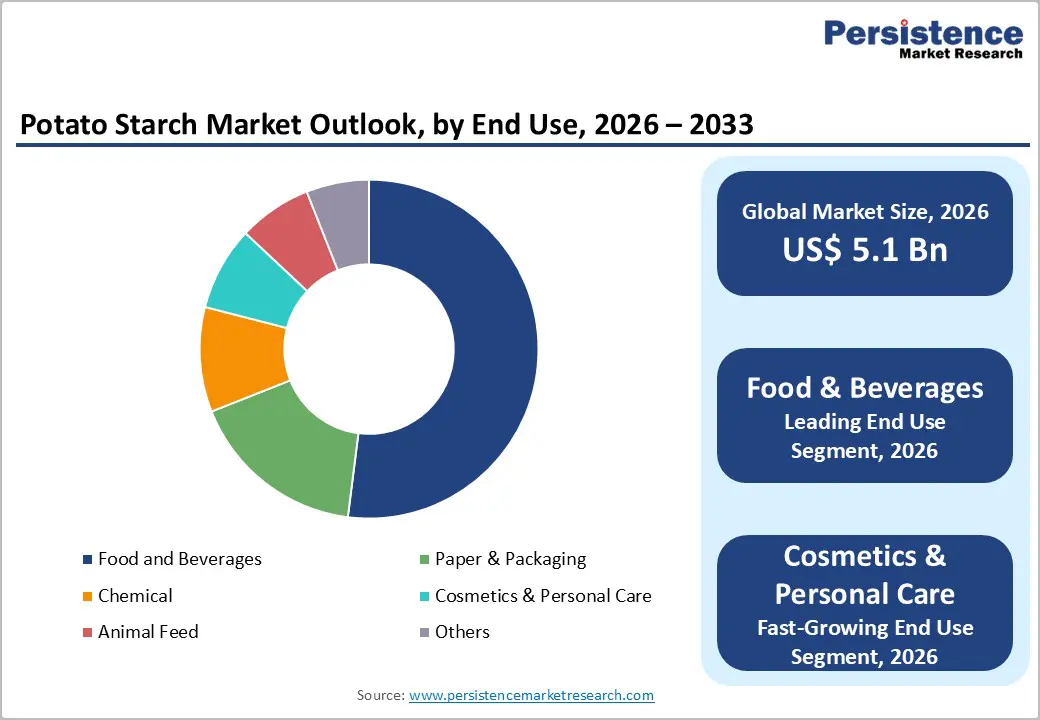

The global potato starch market size is expected to be valued at US$ 5.1 billion in 2026 and projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

The global market is evolving into a high-impact ingredient ecosystem shaped by functionality, cost efficiency, and clean-label demand. Once limited to traditional food thickening roles, potato starch is now gaining strategic importance across processed foods, pharmaceuticals, paper, and even personal care. Rapid industrialization, combined with shifting consumer expectations toward transparency and plant-based formulations, is accelerating innovation. At the same time, competition from alternative starches and pricing pressures are forcing manufacturers to differentiate through performance and sustainability. This dynamic landscape is pushing companies to rethink product development, supply chains, and end-use diversification.

Key Industry Highlights

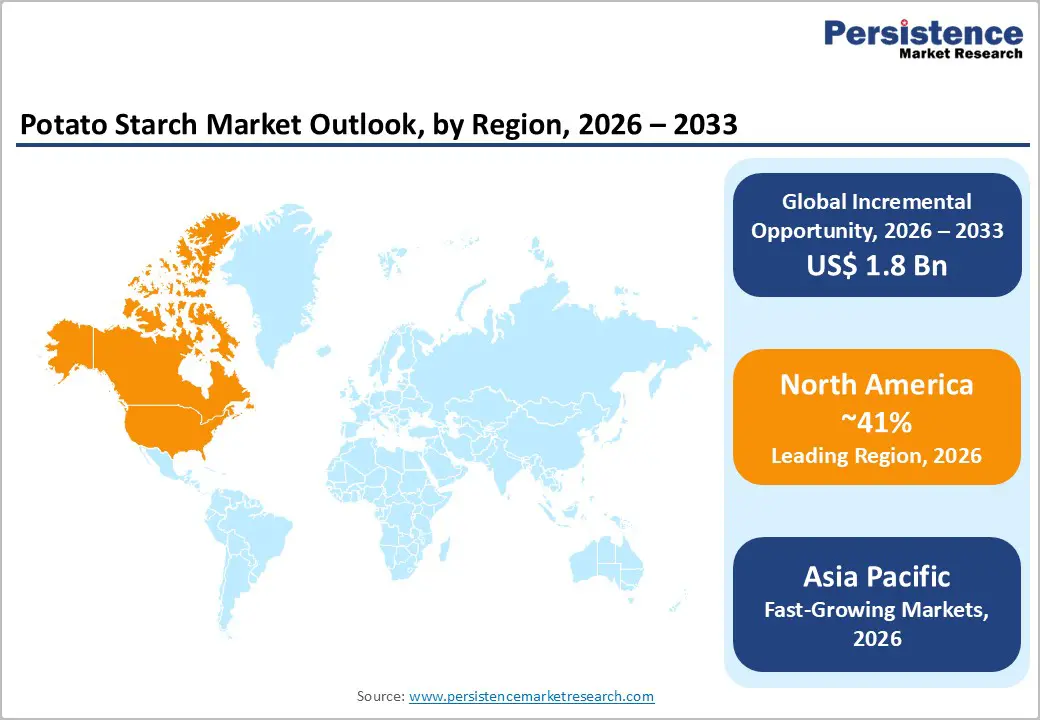

- Leading Region: North America, holding around 41% market share, driven by strong processed food demand, advanced industrial applications, and regulatory support from the U.S. Food and Drug Administration

- Fastest-Growing Region: Asia Pacific, fueled by rapid urbanization, rising disposable incomes, expanding food processing industries, and increasing demand for functional ingredients in China, India, and ASEAN

- Leading Product Type Segment: Modified Potato Starch, driven by superior functionality, high stability in processed and frozen foods, and widespread use across food, pharmaceutical, textile, and paper industries

- Growth Indicators: Increasing consumption of processed and convenience foods, supported by urban lifestyles, clean-label demand, and growing global trade as highlighted by the United States Department of Agriculture

- Consumer Trends: Rising preference for gluten-free, plant-based, and clean-label ingredients is accelerating adoption of potato starch in ready meals, snacks, and functional food products

- Opportunities: Expanding applications in cosmetics and personal care as a natural, plant-based alternative to synthetic additives, with companies like AGRANA Beteiligungs-AG and Tate & Lyle investing in high-purity starch solutions

- Key Developments: In March 2026, Pendulum Therapeutics launched Superfood Gut Fuel Powder incorporating resistant potato starch and plant-based fibers for gut health support.

| Key Insights | Details |

|---|---|

| Global Potato Starch Market Size (2026E) | US$ 5.1 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.3% |

Market Dynamics

Driver - Growing Consumption of Processed and Convenience Foods

Growing consumption of processed and convenience foods is significantly strengthening demand for potato starch, driven by its multifunctional performance as a thickener, binder, and stabilizer. Increasing urbanization, time-constrained lifestyles, and the proliferation of ready-to-eat and ready-to-cook formats are reshaping global food consumption patterns. Potato starch stands out due to its clean-label positioning, gluten-free nature, and neutral taste, making it highly suitable for soups, sauces, processed meats, instant meals, and bakery products. Its superior water-binding capacity and viscosity enhancement improve texture, consistency, and shelf stability in industrial food formulations.

Beyond conventional uses, manufacturers are leveraging potato starch in frozen and microwaveable foods due to its stability under heat and freeze-thaw cycles. According to the United States Department of Agriculture, U.S. processed food exports reached US$38.8 billion in 2024, underscoring robust global demand. This trend is creating strong growth avenues for functional, plant-based ingredient solutions.

Beyond health considerations, sustainability concerns are further strengthening Potato Starch demand, as plant-based proteins generally require fewer natural resources compared to animal farming. Food manufacturers are also integrating Potato Starch into clean-label and fortified products to meet evolving consumer expectations. The continuous rise in global soy production reflects its growing importance in addressing protein requirements, particularly as innovation in plant-based food formulations accelerates across both developed and emerging markets.

Restraint - Competition from Cost-Effective Starch Alternatives

The global potato starch market faces notable constraints due to strong competition from substitute starches such as corn, tapioca, rice, and wheat-based variants. These alternatives are widely adopted across food and industrial applications due to their lower cost, broader availability, and adaptability in high-temperature processing. In large-scale manufacturing, especially in emerging markets, cost efficiency often outweighs functional advantages, leading producers to favor corn starch. According to the United States Department of Agriculture, corn-based starches benefit from extensive production scale and supply chain efficiencies. Additionally, tapioca and rice starches are gaining traction in gluten-free and clean-label formulations. This growing substitution trend limits the penetration of potato starch, particularly in price-sensitive and high-volume application segments.

Opportunity - Surging Demand for Plant-Based Additives in Cosmetics and Personal Care

There is a burgeoning opportunity for market participants to tap into the high-growth Cosmetics & Personal Care segment, which is identified as the fastest-growing end-use category. Potato starch is increasingly utilized as a natural talc substitute in powders, a texturizer in lotions, and an oil-absorbent agent in dry shampoos. As the Clean Beauty movement gains momentum, major cosmetic brands are seeking bio-derived ingredients to replace synthetic silicones and parabens. Opportunities exist for companies to develop specialized, high-purity Modified Potato Starch tailored for topical applications. By positioning potato starch as a sustainable, skin-friendly alternative, producers like AGRANA Beteiligungs-AG and Tate & Lyle can capture high-margin revenue streams and diversify their portfolios away from the volatile food commodity market.

Category-wise Analysis

Product Type Insights

Modified starch is increasingly preferred across industries due to its superior functionality and versatility. In the food sector, it acts as an effective thickener, stabilizer, and emulsifier in products such as sauces, soups, baked goods, and ready-to-eat meals, with strong performance in frozen and processed applications due to its resistance to freeze-thaw cycles. In pharmaceuticals, modified starch serves as a binder and disintegrant in tablet formulations, ensuring consistent drug delivery. Its adaptability also supports applications in textiles, where it is used for warp sizing and fabric finishing, improving smoothness and strength. In the paper industry, it enhances paper strength, printability, and surface quality, making it essential for high-performance uses. In contrast, native potato starch is valued for its natural origin and clean-label appeal, offering effective thickening and water-binding properties for minimally processed and organic food products.

Nature Insights

The conventional segment continues to dominate the potato starch market, supported by well-established agricultural supply chains, large-scale production, and cost advantages for industrial applications. It remains the primary choice across high-volume sectors such as animal feed and paper manufacturing. However, the organic segment is emerging as a high-growth niche, particularly in North America and Western Europe, driven by increasing consumer preference for clean-label, non-GMO, and chemical-free ingredients. Brands like Bob's Red Mill Natural Foods are effectively targeting retail consumers with organic offerings aligned with farm-to-fork and sustainability trends.

Rising health awareness and demand for transparency are accelerating the shift toward organic potato starch in processed foods, snacks, and ready-to-eat products. Its absence of synthetic additives and pesticides enhances its appeal, while growing scrutiny around conventional starch is further strengthening organic adoption.

Regional Insights

North America Potato Starch Market Trends and Insights

North America is expected to account for nearly 41% of the global potato starch market in 2025, driven by a well-established food processing industry and strong consumer demand for convenient, safe, and functional foods. In the United States, increasing use of potato starch as a clean-label thickener and texturizing agent in ready-to-eat meals, snacks, and bakery products is accelerating market growth. Regulatory clarity from the U.S. Food and Drug Administration has strengthened consumer confidence and supported widespread adoption. Innovation trends such as snackification, plant-based meat alternatives, and starch-based sustainable packaging are further enhancing market expansion.

Canada is witnessing steady growth, supported by rising demand for gluten-free and plant-based food products. Increasing imports of potato starch reflect expanding applications in packaged foods and specialty diets. Additionally, growing focus on clean-label ingredients and sustainable consumption is reinforcing market development across both retail and industrial sectors.

Asia Pacific Potato Starch Market Trends and Insights

Asia Pacific is projected to be the fastest-growing potato starch market through 2033, driven by rapid urbanization, rising disposable incomes, and evolving dietary patterns across China, India, and ASEAN countries. Increasing adoption of convenience foods and gradual shifts away from traditional staples in urban areas are accelerating demand for functional starch ingredients. China plays a dual role as a major consumer and emerging producer, supported by government-led agricultural modernization initiatives to enhance starch yield and processing efficiency. The region’s cost advantages and expanding industrial base further strengthen its growth trajectory.

India is witnessing rising demand from food processing, paper, and pharmaceutical sectors, supported by infrastructure development and foreign investments. Companies such as Angel Starch and Food Pvt Ltd are scaling production of modified starches for diverse applications. Additionally, the rapid expansion of e-commerce platforms like Alibaba Group and BigBasket is improving accessibility to premium starch products, supporting regional market expansion.

Competitive Landscape

The global potato starch market is highly competitive, with a mix of multinational corporations and regional players focusing on innovation, efficiency, and product differentiation. Companies are investing in advanced processing technologies, capacity expansion, and R&D to develop modified and specialty starches with enhanced functionality and stability. Collaborations with food scientists and ingredient specialists are enabling tailored solutions for diverse applications. Strategic mergers and acquisitions are further strengthening supply chains and expanding global footprints, while improvements in extraction and drying technologies are optimizing production efficiency and cost structures.

The market remains moderately consolidated, led by key players such as Ingredion Incorporated, Roquette Frères, and Royal Avebe, which leverage vertical integration and technological expertise. At the same time, niche players are addressing specialized industrial and premium food segments. Competitive differentiation is increasingly driven by starch purity, viscosity performance, sustainability certifications, and traceability initiatives.

Key Developments:

- In March 2026, Pendulum Therapeutics launched Superfood Gut Fuel Powder, a functional nutrition product formulated to support gut health. The formulation includes resistant potato starch, baobab, acacia fiber, oat beta-glucan, and grape seed extract

- In March 2025, KMC announced a €40 million investment to expand its existing granule factory in Brande, Denmark. The expansion project includes upgrading production equipment and facilities to boost capacity and future-proof operations.

Companies Covered in Potato Starch Market

- Ingredion

- Cargill, Incorporated

- Roquette Frères

- AGRANA Beteiligungs-AG

- Tate & Lyle

- Emsland-Stärke GmbH

- Avebe

- Südstärke GmbH

- Tereos SA

- KMC

- AKV AmbA

- Angel Starch

- Meelunie B.V.

- Bob's Red Mill Natural Foods

- Others

Frequently Asked Questions

The global potato starch market is projected to be valued at US$ 5.1 Bn in 2026.

Growing consumption of processed and convenience foods is a major factor driving the global Potato Starch market.

The global potato starch market is poised to witness a CAGR of 4.5% between 2026 and 2033.

Surging Demand for Plant-Based Additives in Cosmetics and Personal Care is a significant opportunity in the Potato Starch market.

Major players in the global potato starch market include Ingredion, Cargill, Incorporated, Roquette Frères, AGRANA Beteiligungs-AG, Tate & Lyle, Emsland-Stärke GmbH, Avebe, and others.