- Processed Food

- Potato Processing Market

Potato Processing Market Size, Share, and Growth Forecast, 2026 - 2033

Potato Processing Market by Product Type (Frozen Potato, Dehydrated Potato, Fresh Potatoes), Application (Potato Wedges, Potato Flakes, Potato Granules, Potato Powder, Snacks), End-user (Supermarkets/Hypermarkets, Others), and Regional Analysis for 2026 - 2033

Potato Processing Market Size and Trends Analysis

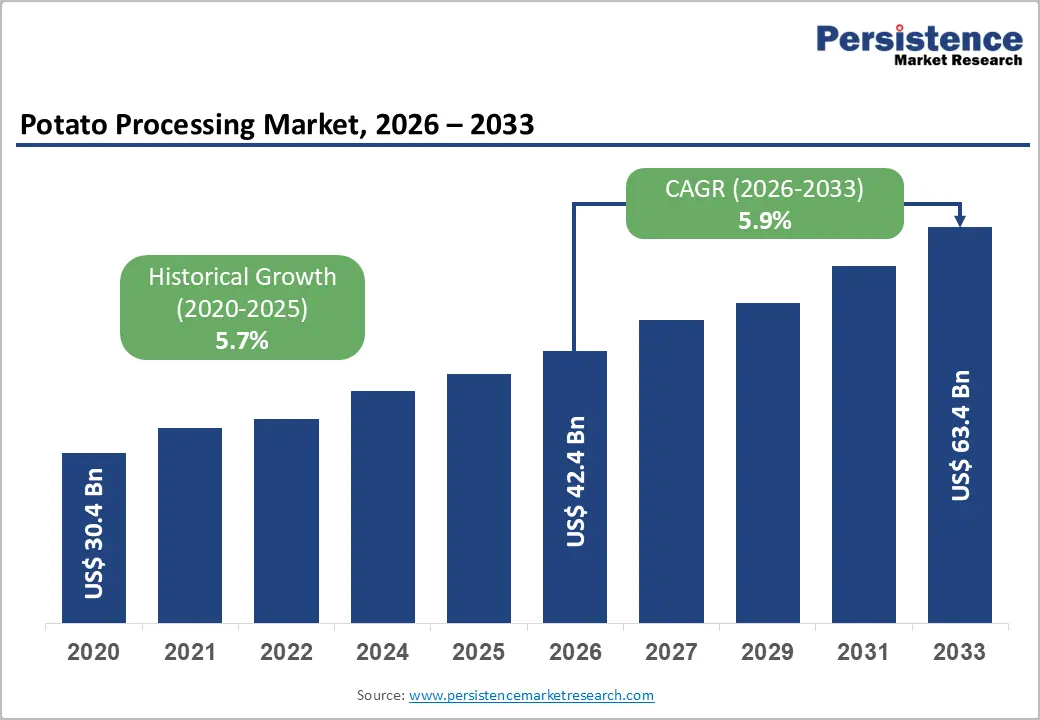

The global potato processing market size is likely to be valued at US$42.4 billion in 2026 and is expected to reach US$63.4 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by growing demand for value-added potato products across both developed and emerging regions. Consumer preference for convenient and ready-to-eat foods continues to rise, fueling the growth of frozen, dehydrated, and snack-based potato offerings. Quick-service restaurants (QSRs) and other foodservice outlets increasingly rely on processed potato products, creating a stable demand channel for processors.

Technological advancements in freezing, dehydration, and packaging methods have improved product shelf life, quality, and operational efficiency, enabling manufacturers to cater to modern lifestyles that favor ready-to-cook and easy-to-prepare meal solutions. Urbanization, busier schedules, and changing dietary habits support market growth, as consumers opt for time-saving food formats. The market also benefits from diverse applications in retail, foodservice, and industrial segments, ensuring resilience against supply chain fluctuations. Favorable macroeconomic factors such as rising disposable incomes, supportive food processing policies, and investments in cold storage and infrastructure provide a strong foundation for sustained expansion.

Key Industry Highlights:

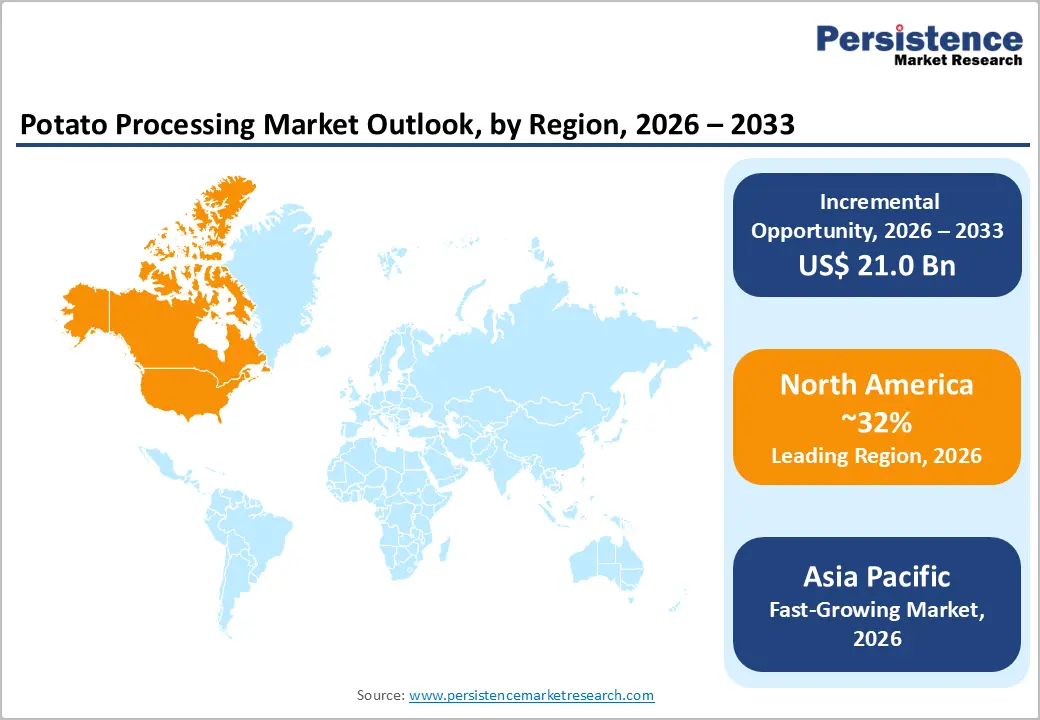

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 32% in 2026, driven by strong foodservice demand, advanced processing infrastructure, and high per-capita consumption of frozen products.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid urbanization, rising disposable incomes, and growing demand for convenient and processed potato products.

- Leading Product Type: Frozen potatoes are projected to represent the leading product type in 2026, accounting for 40% of the revenue share, driven by their long shelf life, widespread use in QSRs, and popularity in French fries and wedges.

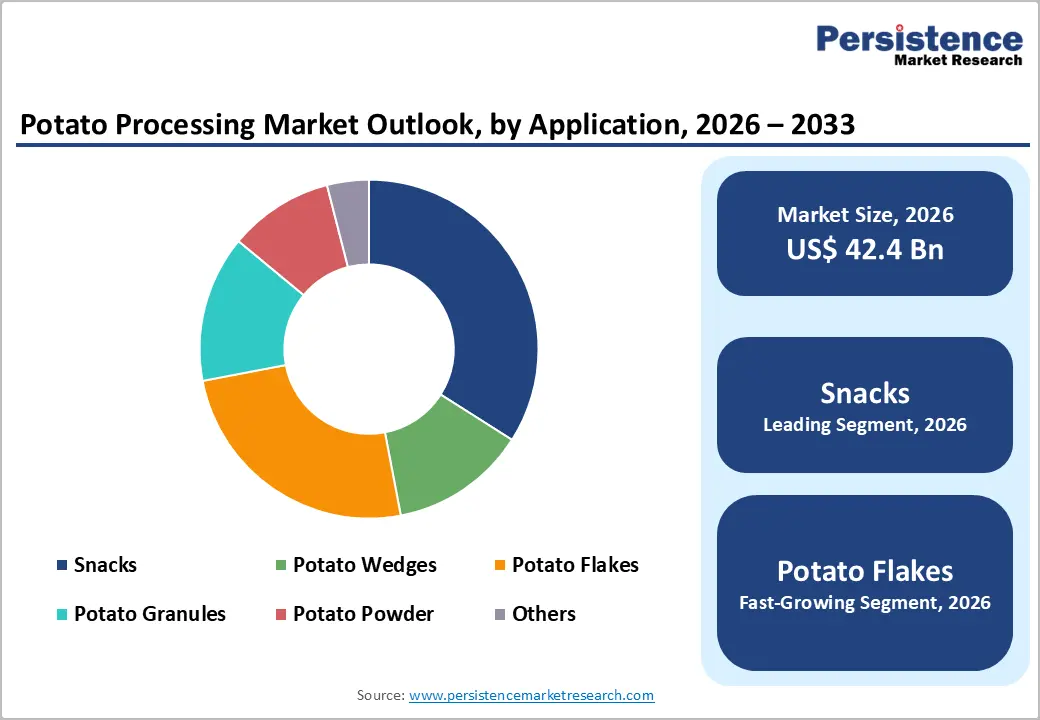

- Leading Application: Snacks are anticipated to be the leading application, accounting for over 45% of the revenue share in 2026, supported by strong retail penetration, impulse-buy appeal, and continuous flavor and texture innovations.

| Key Insights | Details |

|---|---|

|

Potato Processing Market Size (2026E) |

US$42.4 Bn |

|

Market Value Forecast (2033F) |

US$63.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Rising Demand for Convenience and Ready-to-Eat Foods

Consumer lifestyles are increasingly fast-paced, leading to higher demand for convenient, ready-to-eat, and ready-to-cook products. Frozen French fries, wedges, and snack chips provide time-saving solutions, especially for households with working professionals. Retail expansion of pre-packaged and frozen potato items enhances accessibility, while innovation in packaging and portion sizes improves convenience. Supermarkets, online grocery channels, and urban retail formats facilitate consumption. Manufacturers are responding with new formats, flavors, and healthier options to meet evolving consumer preferences.

Rising consumer adoption of snacking habits and on-the-go meals has expanded the processed potato market across age groups. Meal kits, frozen snacks, and quick-prep products are increasingly incorporated into daily routines, creating recurring purchase patterns. Urban households prefer ready-to-cook potato options that reduce preparation time, supporting higher turnover for retail and foodservice channels. Convenience-driven innovations such as microwaveable fries, pre-seasoned wedges, and portion-controlled snacks enhance consumer appeal. Combined with marketing campaigns emphasizing ease of use, these offerings sustain strong demand.

Expansion of Quick-Service Restaurants and the Foodservice Sector

The quick-service restaurants (QSRs) and foodservice sector have expanded significantly, driving high-volume consumption of processed potato products. French fries, wedges, and snack items remain core menu offerings, leading to steady procurement from frozen potato processors. Growth in QSR chains, both international and regional, ensures consistent demand across multiple regions. Investment in modern kitchens, frozen storage, and automated preparation enhances operational efficiency, making processed potatoes an essential input.

Foodservice expansion also encourages innovation in product variety and portion formats. Premium, health-focused, and flavored potato products gain attention in casual dining and fast-casual chains. Partnerships between processors and foodservice operators ensure customized solutions, including portion-controlled fries, wedges, and snack pellets. Seasonal menu offerings, limited-time promotions, and localized flavors increase product turnover. Cold-chain logistics and reliable supply networks allow processors to maintain consistent quality.

Restraint Analysis - Seasonality and Climatic Volatility in Potato Supply

Potato production is highly sensitive to seasonal patterns and climatic conditions, creating supply variability that affects processing operations. Droughts, excessive rainfall, or unexpected temperature fluctuations can impact yield, quality, and tuber size, forcing processors to adjust sourcing strategies. Regional production hubs may experience uneven supply, leading to price volatility and inventory challenges. Dependence on specific cultivation areas, such as Idaho in the U.S. or major potato-growing regions in India and China, exposes the market to localized climatic risks.

Fluctuations in raw potato availability can disrupt production planning, leading to underutilized processing capacity or higher procurement costs. Processors must invest in buffer stocks, cold storage, and supply agreements to mitigate seasonal risks. Variations in tuber quality may affect product consistency, particularly for French fries, wedges, or dehydrated flakes, impacting brand reputation. Crop diseases and pest infestations exacerbate supply instability. Reliance on favorable weather conditions can limit scalability in emerging regions.

Limited Shelf Life and Cold Chain Dependency

Processed potato products, especially frozen and ready-to-cook formats, require strict cold-chain logistics to maintain quality and safety. Inadequate storage, transportation, or handling can lead to spoilage, textural degradation, or microbial contamination. Retailers and foodservice operators rely heavily on uninterrupted freezing and refrigeration infrastructure, which adds to operational costs and complexity. Regions with underdeveloped cold-chain facilities face constraints in market expansion, limiting accessibility for remote consumers.

Cold chain management directly impacts profitability and efficiency for processors. Power outages, transportation delays, or storage inefficiencies can cause financial losses and product recalls. Maintaining product integrity across multiple stages from processing plants to distributors, retailers, or QSRs requires investment in temperature-controlled vehicles, warehouses, and monitoring systems. Shelf-life constraints also affect marketing strategies and packaging innovations, as products must remain fresh until consumption.

Opportunity Analysis - Health-Oriented and Value-Added Potato Products

Increasing health awareness among consumers presents opportunities for fortified, low-fat, and minimally processed potato products. Innovations include baked fries, reduced-sodium chips, air-fried snacks, and products enriched with fiber or protein. Health-oriented products also align with the growing demand for clean-label and organic offerings, creating premium market segments. Processors can differentiate through nutrient-enriched potato snacks, flavored wedges with natural seasonings, or low-calorie frozen items, addressing lifestyle-conscious buyers while expanding product portfolios.

Consumer preference for convenient yet nutritious options drives product development in snacks, ready-to-cook, and meal solutions. Partnerships with QSRs and retail chains enable co-branded health-focused offerings, enhancing market visibility. Emerging markets with rising disposable incomes also show increasing adoption of fortified or value-added products. Sustainability initiatives, including reduced processing waste and eco-friendly packaging, complement health-oriented positioning, allowing manufacturers to strengthen brand equity while tapping into evolving consumer priorities in processed potato consumption.

Dehydrated and Ingredient-Grade Potato Products for Industrial Use

Dehydrated potatoes, including flakes, granules, and powders, offer flexibility for industrial applications in bakery, snacks, convenience foods, and ready-to-eat meals. These ingredient-grade products enable precise formulation, longer shelf life, and lower transportation costs, supporting bulk processing and export potential. Industrial clients favor consistency in texture, moisture, and reconstitution properties, making dehydrated potato products essential inputs for large-scale manufacturers.

Dehydrated products also create opportunities for innovation in instant foods, convenience meals, and blended mixes. By providing stable, easy-to-handle ingredients, processors can cater to QSR chains, retail private labels, and industrial food producers. Expansion of industrial processing infrastructure, technology transfer, and packaging innovation supports market penetration. Emerging economies investing in food processing plants increase the adoption of dehydrated potato products. Trade in powdered or flaked potatoes enables access to distant markets, enhancing revenue streams.

Category-wise Analysis

Product Type Insights

Frozen potatoes are expected to lead the potato processing market, accounting for approximately 40% of revenue in 2026, driven by their long shelf life, consistent quality, and widespread adoption across QSRs and retail channels. French fries, wedges, and other frozen formats are staples in fast food chains and supermarkets due to their convenience and ease of preparation. For example, McCain Foods supplies frozen French fries, catering to large QSR chains and grocery stores, illustrating the segment’s critical role in supporting high-volume demand. Investments in freezing technology, automated processing lines, and cold storage infrastructure have enabled processors to maintain quality while scaling production efficiently.

Dehydrated potatoes are likely to represent the fastest-growing segment in 2026, supported by their advantages in storage, transportation, and industrial reconstitution, often used in flakes, granules, and powders. This category is increasingly adopted in bakery, snacks, and ready-to-cook meals, providing flexibility for industrial applications. For example, Aviko B.V. produces dehydrated potato flakes for instant mashed potatoes, bakery formulations, and snack mixes, showcasing its industrial utility. The segment benefits from lower logistics costs compared to frozen products and longer shelf stability without dependence on continuous cold-chain management.

Application Insights

Snacks are projected to lead the market, capturing around 45% of the revenue share in 2026, supported by strong retail penetration, impulse-buy appeal, and brand loyalty. For example, Burts Potato Chips has established a strong presence in premium snack markets in the U.K., demonstrating how branding and flavor innovation can drive consumer preference. Retail chains, supermarkets, and convenience stores favor snacks due to their long shelf life, attractive packaging, and ready-to-eat format. Flavor diversity, such as baked, air-fried, and seasoned options, appeals to both health-conscious and traditional consumers.

Potato flakes are likely to be the fastest-growing application, driven by their utility in mashed products, bakery items, extruded snacks, and ready-to-cook meals. They enable convenience in industrial and foodservice formulations, allowing precise dosing and consistent quality. For example, Idahoan Foods supplies potato flakes to restaurants and packaged food manufacturers for mashed potato mixes and snack applications, illustrating their versatile usage. The segment is gaining traction due to rising demand for processed, ingredient-grade potatoes in QSRs, bakeries, and packaged foods.

Regional Insights

North America Potato Processing Market Trends

North America is anticipated to be the leading region, accounting for a market share of 32% in 2026, driven by high consumer demand for convenience foods, strong QSR penetration, and advanced processing infrastructure. Frozen potato products, especially French fries and wedges, dominate retail and foodservice channels due to their long shelf life and consistent quality. For example, J.R. Simplot Company invests in state-of-the-art freezing and dehydration facilities to supply major QSR chains, reflecting the importance of technological advancements and vertical integration in maintaining supply chain efficiency.

North American trends also show increasing adoption of value-added and flavored frozen potato products, reflecting evolving consumer tastes. Retailers and QSRs focus on differentiated offerings, including snack-sized fries, wedges, and seasoned potato bites, to attract younger demographics. Expansion of online grocery channels and e-commerce delivery supports wider accessibility of frozen potato products. Innovation in packaging, portion control, and ready-to-cook formats enhances convenience.

Europe Potato Processing Market Trends

Europe is likely to be a significant market for potato processing in 2026, due to high demand for frozen, dehydrated, and snack-based products, driven by mature retail chains, health-conscious consumers, and extensive QSR networks. Consumers increasingly prefer baked, air-fried, or low-fat potato snacks, encouraging processors to innovate in healthier offerings. For example, Aviko B.V. in the Netherlands has expanded its product portfolio with ready-to-cook frozen fries and dehydrated potato flakes to meet industrial and retail demand.

Growth in frozen wedges, snack bites, and portion-controlled fries reflects consumer demand for ready-to-eat and customizable options. Investment in automation, cold-chain infrastructure, and logistics ensures operational efficiency and supports exports to emerging markets. Innovation ecosystems, including partnerships with food technology providers, enhance product differentiation.

Asia Pacific Potato Processing Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by increasing urbanization, rising disposable incomes, and expanding QSR and retail sectors. Emerging economies such as China, India, and ASEAN countries contribute significantly to market growth, leveraging lower production costs and expanding domestic potato cultivation. For example, McCain Foods Limited has scaled production in India and China, supplying frozen fries to major QSR chains and retail outlets, demonstrating strategic market expansion and localization.

Trends in Asia Pacific highlight increasing adoption of dehydrated potato products and ingredient-grade flakes for bakery, snack, and convenience food applications. QSR growth, urban household adoption, and evolving lifestyles drive demand for frozen, instant, and snack-ready potato formats. Regional players collaborate with multinational processors to introduce premium, health-oriented, and value-added products tailored to local tastes. Expansion of retail modern trade, e-commerce grocery channels, and organized foodservice chains ensures wider distribution and accessibility.

Competitive Landscape

The global potato processing market exhibits a moderately fragmented structure, driven by a mix of multinational corporations and strong regional players leveraging extensive distribution networks, diverse product portfolios, and continuous innovation to maintain competitive advantage. Large companies such as McCain Foods Limited dominate with broad frozen and dehydrated product lines across major markets, while others focus on niche segments and regional tastes, fostering healthy competition.

With key leaders including Lamb Weston Holdings, Inc., The Kraft Heinz Company, J.R. Simplot Company, Aviko B.V., and Farm Frites International B.V., the market’s competitive dynamics revolve around expanding geographic reach and enhancing product portfolios. These players compete through technological upgrades, strategic partnerships with foodservice chains and retail distributors, and sustainability initiatives that address modern consumer preferences.

Key Industry Developments:

- In March 2026, Belgian potato growers launched a direct sales campaign to address a significant surplus of unsold potatoes and support local communities. Sector organizations, including Boerenbond, ABS, Belgapom, and Belpotato.Viaverda and VLAM organized an event allowing consumers to buy potatoes directly from growers at a subsidized price, with a portion of sales donated to Food Banks.

- In February 2025, Krishak Bharati Cooperative Ltd (KRIBHCO) and Netherlands-based Farm Frites signed a joint venture agreement to establish a state-of-the-art potato processing unit in Shahjahanpur, Uttar Pradesh, aimed at increasing farmer incomes and creating employment opportunities.

- In August 2025, Ukrainian potato processor Potato-Agro began construction of a major new processing facility in the Cherkasy region to produce both frozen French fries and potato flour, targeting a gap in the country’s value-added potato sector. The plant, with equipment already being delivered and construction underway, is designed to process a significant volume of potatoes annually into value-added formats, marking one of Ukraine’s largest domestic investments in potato processing.

Companies Covered in Potato Processing Market

- Lamb Weston Holdings, Inc.

- McCain Foods Limited

- The Kraft Heinz Company

- J.R. Simplot Company

- Idahoan Foods, LLC

- Agristo NV

- Farm Frites International B.V.

- Aviko B.V.

- AGRANA Beteiligungs-AG

- Burts Potato Chips Ltd.

- Intersnack Group GmbH & Co. KG

- J.R. Short Milling Company

- The Little Potato Company Ltd.

- HyFun Foods

- Cavendish Farms

Frequently Asked Questions

The global potato processing market is projected to reach US$42.4 billion in 2026.

The potato processing market is driven by rising demand for convenience foods, ready-to-eat products, and growth in QSR and retail channels.

The potato processing market is expected to grow at a CAGR of 5.9% from 2026 to 2033.

Key market opportunities lie in health-oriented, value-added, and dehydrated potato products for retail, foodservice, and industrial applications.

Lamb Weston Holdings, Inc., McCain Foods Limited, The Kraft Heinz Company, J.R. Simplot Company, and Idahoan Foods are the leading players.