- Automation & Robotics

- North America Warehouse Automation Market

North America Warehouse Automation Market Size, Share, and Growth Forecast, 2026 - 2033

North America Warehouse Automation Market by Warehouse Automation (Automated Storage and Retrieval Systems (AS/RS), Conveyor Systems, Automated Sortation Systems, Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Goods-to-Person (GTP) Systems, and Misc.), Warehouse Function (Storage, Order Picking, Material Movement/Transportation, Sorting & Consolidation, and Packing & Palletizing.), Industry and Regional Analysis for 2026 - 2033

North America Warehouse Automation Market Size and Trends Analysis

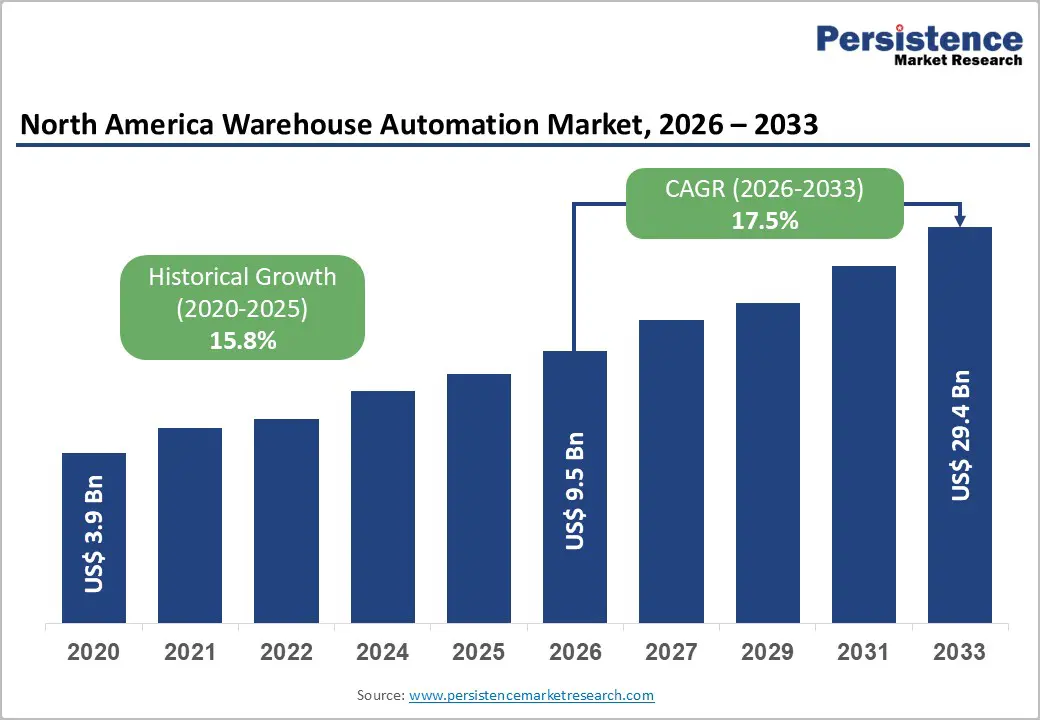

The North America warehouse automation market size is likely to reach US$9.5 billion in 2026 and is projected to reach US$29.4 billion by 2033, growing at a CAGR of 17.5% between 2026 and 2033.

The primary catalysts include the sustained acceleration of e-commerce fulfilment volumes, acute warehouse labor shortfalls, and rapid deployment of AI-integrated robotics platforms across North American supply chains. According to the U.S. Census Bureau, retail e-commerce sales in the United States reached approximately US$ 310.3 billion in Q3 2025, representing 16.4% of total retail sales on a seasonally adjusted basis, a foundational demand signal for automated fulfilment infrastructure.

Key Industry Highlights:

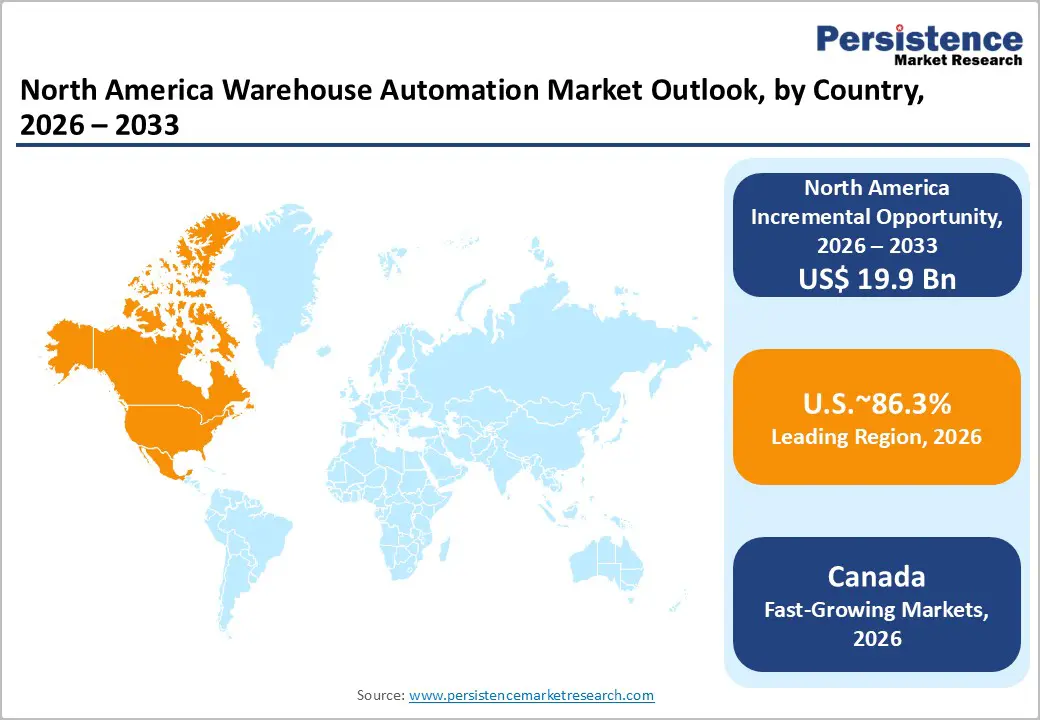

- Leading Regional Market: The U.S. dominates the North America warehouse automation market, with California, Texas, and New York driving significant adoption through high-volume e-commerce, retail, and food & beverage distribution centres.

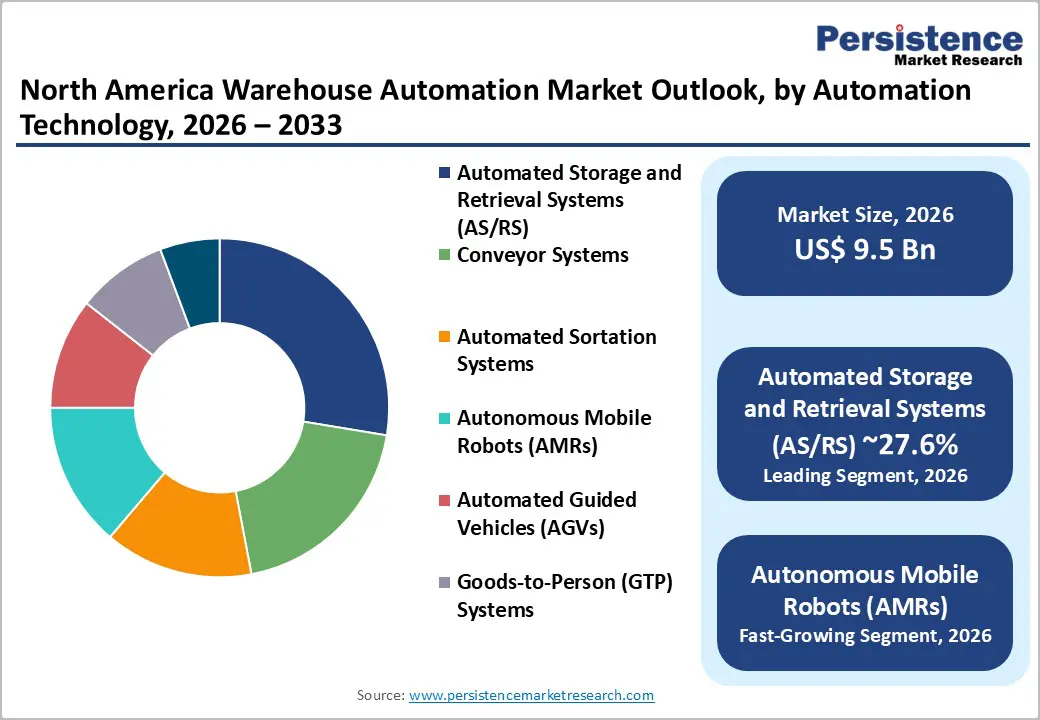

- High-Value Leading Technology: Automated Storage and Retrieval Systems (AS/RS) hold the largest market share at 27.6%, driven by high-density storage requirements, 24/7 operations, and precision inventory management in CPG, pharmaceutical, and food & beverage warehouses.

- Fastest-Growing Technology: Autonomous Mobile Robots (AMRs) are the fastest-growing segment, enabled by AI-driven navigation, operational flexibility, and rapid deployment in multi-SKU, dynamic fulfillment environments.

- Leading End-user: Retail & E-Commerce emerges as the largest end-use segment with 41.8% market share, supported by same-day and next-day delivery expectations and structural shifts toward online shopping.

- Fastest-Growing End-user: Third-party logistics (3PL) providers are the fastest-growing end-user, accounting for 42% of total U.S. warehouse take-up in Q2 2025, driven by shippers outsourcing fulfillment amid rising omnichannel complexity.

- Key Growth Indicators: AI integration and subscription-based automation models (RaaS/SaaS) are expanding market access to SMEs, enabling advanced robotics deployment with lower upfront costs and operational scalability.

| Key Insights | Details |

|---|---|

| Warehouse Automation Market Size (2026E) | US$ 9.5 Bn |

| Market Value Forecast (2033F) | US$ 29.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.8 |

Market Dynamics

Structural Acceleration of E-Commerce Fulfilment Volumes

The fundamental shift of consumer purchasing behaviour toward digital channels has created an unprecedented requirement for high-throughput, precision-oriented warehouse operations across North America. As fulfillment speed expectations have compressed to same-day and next-day delivery windows, conventional manual operations are structurally incapable of sustaining the throughput and accuracy standards required.

According to the U.S. Census Bureau, retail e-commerce sales in Q3 2025 reached approximately US$ 310.3 billion (seasonally adjusted), reflecting a 5.1% year-over-year increase and accounting for 16.4% of total retail sales. In Canada, the e-commerce sector achieved approximately US$ 89.4 billion in gross merchandise value (GMV) in 2024, with revenues projected to reach US$ 104 billion by 2029, led by fashion, hobby and leisure and electronics as top-performing categories. This structural demand shift directly fuels capital deployment into the North America warehouse automation market, compelling operators to invest in AS/RS, conveyor systems, and sortation technologies to enable faster, more accurate order processing at scale.

AI Integration and Subscription-Based Automation Models Broadening Market Access

The convergence of artificial intelligence, machine learning, and scalable software-delivery business models is fundamentally reshaping who can access warehouse automation across North America, extending the market from enterprise-scale operators down to small and midsized enterprises (SMEs). Robotics-as-a-Service (RaaS) and Software-as-a-Service (SaaS) subscription platforms have structurally reduced the capital barrier to automation adoption, enabling companies with annual revenues under US$ 50 million to deploy sophisticated robotics infrastructure at operating expense levels.

As confirmed by March 2026 industry data, these subscription-based platforms are driving rapid democratization of AI-driven automation across North American logistics, e-commerce, and manufacturing sectors. CMES Robotics, in January 2026, secured multi-year robotic palletizing and depalletizing contracts with a premium U.S. food ingredient manufacturer, deploying AI-Vision technologies for mixed-case palletizing, random bag/box depalletizing, and intelligent piece-picking in high-variability environments. This technological convergence is a critical structural enabler that is expanding the total addressable base of the North America warehouse automation market well beyond traditional Fortune 500 operators.

Restraint - Prohibitive Capital Expenditure and System Integration Complexity

The substantial upfront investment required for warehouse automation implementation remains a material adoption barrier, particularly for mid-market operators and regional logistics providers. Full-scale AS/RS installations, AMR fleets, and integrated WMS platforms demand multi-million-dollar capital commitments with multi-year payback horizons.

Kraft Heinz's US$ 400 million automated distribution centre in DeKalb, Illinois, a 775,000-sq-ft facility, illustrates the capital intensity required at enterprise scale for a single automated facility deployment. Beyond procurement, integration complexity across legacy WMS platforms, real-time data infrastructure, and multi-vendor robotics ecosystems introduces significant project risk, timeline extensions, and budget overruns, deterring smaller operators with constrained capital budgets from committing to full automation transformation programs.

Opportunity - Food & Beverage Sector as an Underpenetrated Automation Frontier

The food and beverage manufacturing sector represents a strategically significant and structurally underpenetrated opportunity for warehouse automation adoption across North America. Food and beverage establishments accounted for 16.8% of total U.S. manufacturing sales in 2021, employing approximately 1.7 million workers and contributing 15.0% of total manufacturing value added. The sector is distributed across more than 42,700 establishments nationwide, led by California, Texas, and New York (USDA Economic Research Service). Meat processing alone contributed 26.2% of sector sales and employed 30.6% of the workforce, underscoring the high-volume, high-complexity nature of operations that are prime candidates for automation investment.

Concrete deployments validate the sector's automation trajectory and signal significant latent opportunity for the North America warehouse automation market. JBS Foods Canada partnered with Scott Technology on a US$ 71 million fully automated warehousing system at its Brooks, Alberta beef production facility capable of handling 85,000 boxes and 600 SKUs, picking 3,000 cartons per hour, shipping 40,300 cartons daily, and palletising over 120 pallets per hour, replacing fully manual operations with AI-driven, high-speed fulfilment infrastructure.

ABB Robotics Canada's 2021 strategic alliance with Cam Industrial and Remtech Systems to implement automated mixed-load palletising, depalletising, and AS/RS systems across Alberta and British Columbia distribution centres confirms the geographic breadth of this sector's automation opportunity.

Third-Party Logistics Outsourcing Driving Automated Warehouse Infrastructure Demand

Third-party logistics (3PL) providers are emerging as one of the most strategically actionable demand channels for the North America warehouse automation market, driven by shipper outsourcing momentum, the complexity of omnichannel fulfilment, and the increasing need for technology-enabled warehousing services that meet stringent delivery SLAs. In Q2 2025, 3PLs accounted for 42% of total warehouse take-up in the United States, a 12% year-on-year increase (Savills), reflecting the accelerating shift toward outsourced fulfilment amid supply chain uncertainty and tariff disruptions.

KNAPP AG's strategic establishment of a new Canadian subsidiary in August 2025, appointing Michael Sudjian as Managing Director to deliver tailored warehouse automation solutions with local project management and after-sales support for healthcare, retail, and food distribution sectors, exemplifies how automation vendors are proactively positioning to capture 3PL sector growth.

The January 2026 SSI SCHAEFER–Moffett Automation strategic partnership, integrating free-roaming pallet shuttle systems with WMS software and high-density pallet storage, directly targets the throughput and layout optimisation demands of high-volume 3PL warehouse environments. As regulated sectors, including pharmaceuticals, increasingly outsource fulfilment, the 3PL segment's technology requirements are broadening the North American warehouse automation market's addressable revenue pool across more complex use cases.

Category-wise Analysis

Automation Technology Insights

Automated Storage and Retrieval Systems (AS/RS) command the largest share of the North America Warehouse Automation Market at 27.6% in 2026, driven by their unparalleled capacity to maximise vertical storage density, minimise inventory retrieval time, and support continuous 24/7 unattended operations in high-SKU, high-volume environments. AS/RS technology is particularly dominant in food & beverage, pharmaceutical, and CPG distribution applications that require precise inventory management at scale.

Technology’s market leadership is evidenced by landmark capital deployments: Kraft Heinz's US$ 400 million automated distribution centre in DeKalb, Illinois, features a 24/7 AS/RS system across 775,000 sq ft for high-volume foodservice distribution. TK Elevator's smart warehouse in Olive Branch, Mississippi, integrates mini-load AS/RS retrieval technology, enabling 24/7 parts availability with the potential to reduce logistics processing time by 30% and customer waiting time by up to 20% through AI-driven automatic replenishment and QR-coded inventory tracking. Hai Robotics' March 2026 upgraded HaiPick Climb system, delivering up to 4,000 tote deliveries per hour and increasing storage density, confirms continuous performance advancements within this leading segment.

Autonomous Mobile Robots (AMRs) are the fastest-growing automation technology within the North American Warehouse Automation Market, propelled by their operational flexibility, rapid deployment, and compatibility with dynamic, multi-SKU fulfilment environments that cannot support rigid, fixed-infrastructure systems. AMRs navigate using AI-powered sensors and real-time spatial mapping, enabling rapid reconfiguration without costly facility redesign, a critical advantage in e-commerce and 3PL environments subject to seasonal volume fluctuation.

End-user Insights

Retail & e-commerce holds the dominant position in the North America Warehouse Automation Market, with 41.8% market share in 2026, underpinned by the structural and sustained shift of consumer spending toward online channels, which require high-speed, high-accuracy order fulfilment infrastructure capable of operating at unprecedented SKU breadth and order volume. U.S. e-commerce sales reached approximately US$ 310.3 billion (seasonally adjusted) in Q3 2025, up 5.1% year-over-year, representing 16.4% of total retail sales (U.S. Census Bureau).

Third-Party Logistics (3PL) providers represent the fastest-growing end-use industry in the North America warehouse automation market, as shippers across retail, manufacturing, healthcare, and food sectors increasingly outsource fulfilment to technology-enabled 3PL partners capable of delivering automation-backed SLA performance at variable cost structures. In Q2 2025, 3PLs accounted for 42% of total U.S. warehouse take-up, a year-on-year increase of 12% (Savills), confirming the accelerating momentum of outsourcing amid supply chain uncertainty and tariff disruptions.

Competitive Landscape

The North America warehouse automation market is moderately consolidated, dominated by global leaders such as Dematic, Daifuku Co., Swisslog Holding AG, Honeywell International, KNAPP AG, and SSI Schaefer AG. These companies offer comprehensive solutions, including automated storage and retrieval systems, autonomous mobile robots, and warehouse execution software, enabling large-scale, efficient, and integrated operations.

While the top players control a significant share, emerging specialists like GreyOrange, InVia Robotics, and TGW Logistics Group drive innovation with modular and flexible solutions for e-commerce, CPG, and food & beverage sectors. The market combines the scale and integration capabilities of large vendors with the agility and customisation of smaller players, creating a dynamic competitive environment. Adoption of AI, robotics, and IoT-enabled systems continues to fuel growth, making North America a key region for advanced warehouse automation solutions.

Key Industry Developments:

- In January 2026, CMES Robotics secured multi-year robotic palletizing and depalletizing projects with a U.S. food ingredient manufacturer. The deployment leverages AI-Vision technologies for mixed-case palletizing, random bag/box depalletizing, and intelligent piece-picking, improving labor efficiency, operational flexibility, and scalability. This reflects the growing adoption of AI-powered, adaptable warehouse automation platforms across North American logistics, e-commerce, and manufacturing sectors.

- In August 2025, KNAPP AG opened a new subsidiary in Canada, appointing Michael Sudjian as Managing Director, to provide tailored warehouse automation solutions, local project management, and after-sales support. This move strengthens KNAPP’s ability to deliver intelligent intralogistics and automated warehouse systems to Canadian customers, highlighting the increasing investment in North American warehouse automation infrastructure.

Companies Covered in North America Warehouse Automation Market

- Dematic

- Daifuku Co., Ltd.

- Swisslog Holding AG

- Honeywell International Inc.

- KNAPP AG

- SSI Schaefer AG

- TGW Logistics Group

- Kardex Holding AG

- Murata Machinery, Ltd.

- GreyOrange

- InVia Robotics Inc.

Frequently Asked Questions

The North America Warehouse Automation Market is projected to be valued at US$ 9.5 Bn in 2026.

The Automated Storage and Retrieval Systems (AS/RS) segment is expected to account for approximately 27.6% of the North America Warehouse Automation Market by Automation Technology in 2026.

The market is expected to witness a CAGR of 17.5% from 2026 to 2033.

The North America Warehouse Automation Market is driven by the structural acceleration of e-commerce fulfillment volumes and the adoption of AI-enabled, subscription-based automation models that broaden access for SMEs.

Key market opportunities in the North America Warehouse Automation Market lie in the underpenetrated food & beverage sector and the rapidly growing third-party logistics (3PL) outsourcing segment.

Key players in the Warehouse Automation Market include Dematic, Daifuku Co., Swisslog Holding AG, Honeywell International, KNAPP AG, and SSI Schaefer AG.