- Medical Devices

- IV Tubing Sets and Accessories Market

IV Tubing Sets and Accessories Market Size, Share, and Growth Forecast, 2026 - 2033

IV Tubing Sets and Accessories Market by Product (Primary IV Tubing Sets, Secondary IV Tubing Sets, Others) Application (Central Venous Catheter Placement, Peripheral Intravenous Catheter Insertion, PICC Line Insertion), and Regional Analysis for 2026 - 2033

IV Tubing Sets and Accessories Market Size and Trends Analysis

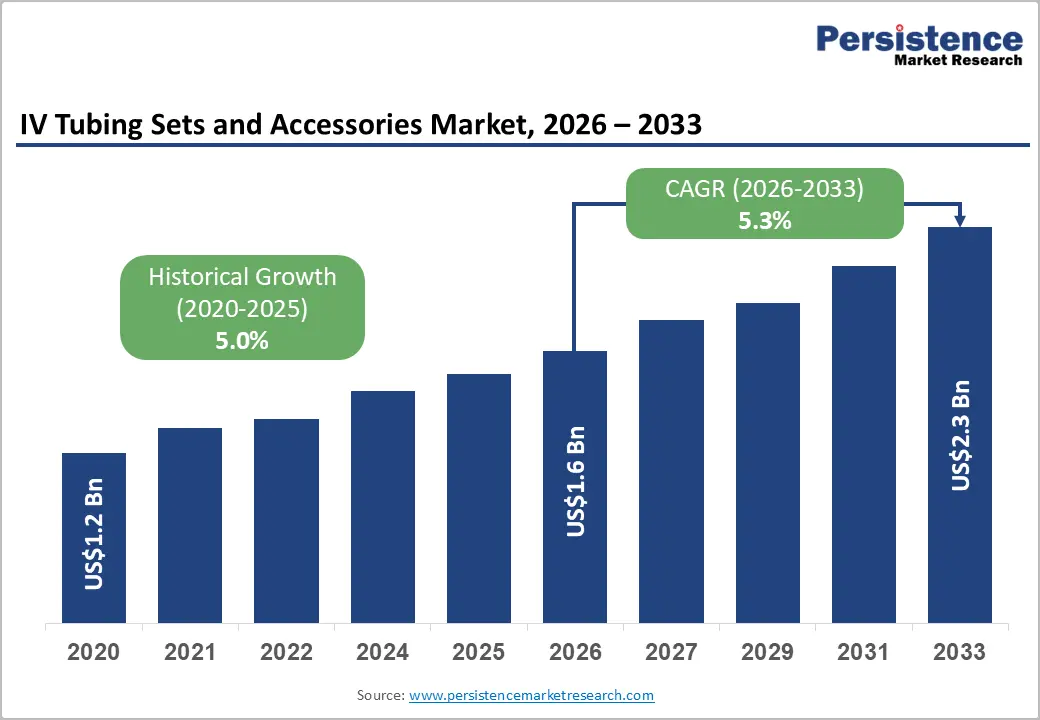

The global IV tubing sets and accessories market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by increasing reliance on intravenous therapy across hospitals, ambulatory surgical centers, and home healthcare settings. Rising cases of chronic diseases and higher surgical volumes continue to drive demand for safe and efficient infusion systems.

According to healthcare burden insights from the World Health Organization (WHO, 2024), non-communicable diseases account for nearly 74% of global deaths, indirectly supporting long-term infusion therapy utilization. Growth is supported by the shift toward closed-system and needle-free IV solutions to reduce catheter-related infections.

Key Industry Highlights:

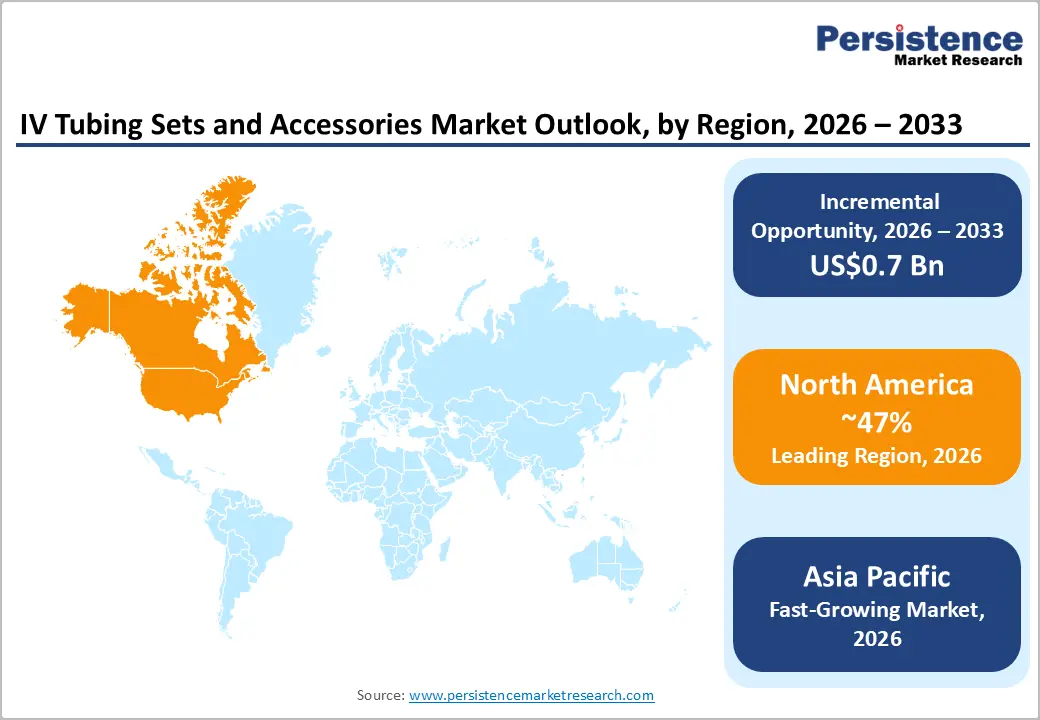

- Leading Region: North America is anticipated to be the leading region, accounting for 47% market share in 2026, driven by high prevalence of chronic diseases, stringent regulatory standards, and strong adoption of closed-system and home infusion therapies.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region for IV tubing sets and accessories in 2026, supported by a rising chronic disease burden, increasing surgical volumes, and strong manufacturing capabilities.

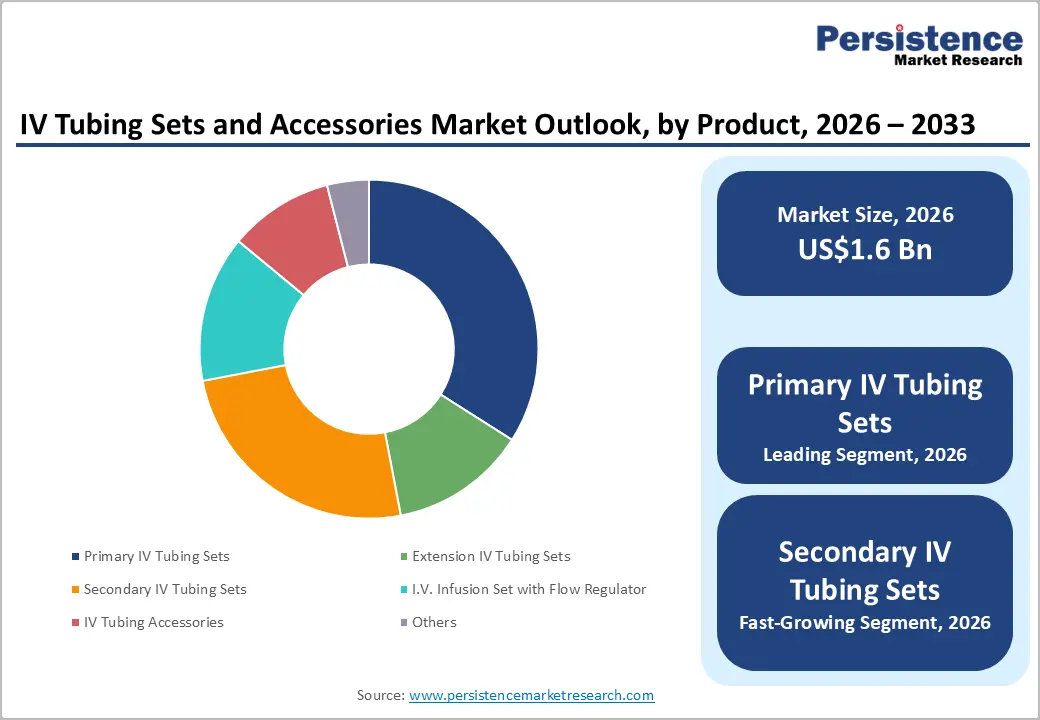

- Leading Product Type: Primary IV tubing sets are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, due to their high usage in routine infusion therapies and standardized hospital procurement.

- Leading Application: Peripheral intravenous catheter insertion is anticipated to be the leading application, accounting for over 41% of the revenue share in 2026, supported by its widespread use in routine hospital care.

- Key Opportunity: The key market opportunity in the IV tubing sets and accessories market lies in the growing integration of smart infusion technologies with needle-free closed IV systems to support safer, home-based, and digitally connected intravenous therapy worldwide.

DRO Analysis

Driver - Shift toward Needle-Free Closed IV Systems

Healthcare facilities are increasingly adopting these systems to reduce the risk of catheter-related bloodstream infections (CRBSIs) and needle-stick injuries among healthcare workers. Hospitals and ambulatory care centers are standardizing closed IV setups as part of infection prevention protocols. Rising awareness about hospital-acquired infections and stricter clinical safety guidelines are accelerating the replacement of conventional open systems.

The adoption of needle-free closed IV systems is also being driven by regulatory emphasis on patient safety and quality care outcomes. Healthcare providers are prioritizing devices that minimize contamination risk and improve workflow efficiency. Advanced IV tubing sets with integrated valves, anti-reflux mechanisms, and sealed connectors are becoming standard in modern hospitals.

Manufacturers are investing in product innovation to meet evolving clinical needs and compatibility with infusion pumps. As home healthcare expands, closed systems are increasingly preferred for long-term therapies, ensuring safer administration outside hospital environments and supporting broader market growth across developed and emerging healthcare systems.

Restraint - Supply Chain Fragility for Medical-Grade Resins

These resins are essential for producing high-quality, biocompatible tubing used in intravenous therapy. Disruptions, geopolitical tensions, and raw material shortages often lead to inconsistent supply and price volatility. Manufacturing delays directly impact production timelines for IV consumables, creating procurement challenges for hospitals and distributors. The dependency on a limited number of certified resin suppliers intensifies supply risk, particularly during periods of high healthcare demand, such as pandemics or seasonal disease surges.

This fragility also affects product availability and cost stability across regions, especially in price-sensitive markets. Medical device manufacturers face challenges in maintaining consistent quality standards while managing fluctuating input costs. Regulatory requirements for medical-grade materials limit alternative sourcing options, increasing dependency on established supply chains.

Opportunity - Technological Convergence with Smart Infusion Systems

Technological convergence with smart infusion systems presents a strong growth opportunity in the IV tubing sets and accessories market. Integration of IV tubing with smart pumps, sensors, and digital monitoring platforms is transforming traditional infusion therapy into a more controlled and data-driven process. These advancements improve dosage accuracy, reduce medication errors, and enhance patient safety in hospitals and critical care units.

Increasing adoption of electronic health systems and connected medical devices is supporting the transition toward intelligent infusion ecosystems. This creates demand for compatible tubing sets designed to work seamlessly with advanced infusion technologies. The opportunity is strengthened by rising investment in digital healthcare infrastructure and remote patient monitoring.

Smart IV systems enable real-time tracking of infusion rates and alerts for blockages or air detection, improving clinical efficiency. Manufacturers are developing next-generation tubing with embedded compatibility features for IoT-based healthcare platforms. This convergence is also expanding into home healthcare, where remote monitoring ensures safe long-term therapy management.

Category-wise Analysis

Product Type Insights

Primary IV tubing sets are expected to lead, accounting for 45% of revenue in 2026. Its extensive use in routine clinical procedures such as hydration therapy, antibiotic administration, and standard intravenous infusions. Their dominance is supported by high-volume procurement in hospitals and standardized treatment protocols that favor cost-effective and reliable infusion delivery systems. For example, B. Braun Melsungen AG supplies primary IV infusion systems that are widely used in large hospital networks.

Secondary IV tubing sets are likely to represent the fastest-growing segment, supported by increasing adoption of multi-drug infusion therapies and complex treatment regimens. These sets are essential for parallel drug administration, chemotherapy, and critical care treatments, where multiple medications must be delivered simultaneously without risk of contamination. A notable example is ICU Medical Inc., which offers advanced secondary infusion systems widely used in oncology and intensive care units to ensure precise drug delivery and reduced medication errors.

Application Insights

Peripheral intravenous catheter insertion is projected to lead the market, capturing around 41% of the revenue share in 2026, supported by its widespread use in routine hospital care and short-term therapy administration. It is the most commonly used vascular access method for delivering fluids, antibiotics, and pain management drugs in emergency rooms, inpatient wards, and outpatient settings. For instance, Fresenius Kabi provides peripheral IV infusion solutions widely adopted in hospital systems across Asia and Europe, supporting efficient bedside care delivery.

Central venous catheter placement is likely to be the fastest-growing application, due to rising demand for long-term and complex intravenous therapies. This method is increasingly used in critical care, oncology, and intensive treatment settings where multiple drug administration and hemodynamic monitoring are required. For example, BD (Becton Dickinson) offers advanced central venous catheter systems widely used in ICUs for high-risk patients requiring continuous infusion therapy.

Regional Insights

North America IV Tubing Sets and Accessories Market Trends

North America is anticipated to be the leading region, accounting for a market share of 47% in 2026, supported by advanced healthcare infrastructure, high surgical volumes, and strict infection-control regulations. Hospitals are rapidly adopting needle-free and closed IV systems to reduce catheter-related bloodstream infections and improve patient safety outcomes. A notable example includes Baxter International, which offers advanced IV therapy and infusion solutions widely used in critical care settings across North America.

U.S. IV Tubing Sets and Accessories Market Trends

The U.S. dominates the regional market, driven by high hospitalization rates, advanced ICU infrastructure, and strong adoption of digital healthcare systems. Hospitals are increasingly using smart infusion pumps and connected devices to improve medication accuracy and reduce errors. FDA-driven safety regulations are accelerating the shift toward closed IV systems. Rising cancer treatments, surgeries, and emergency care cases are increasing the demand for IV consumables.

Canada IV Tubing Sets and Accessories Market Trends

Canada is a significant market for IV tubing sets and accessories supported by government-funded healthcare modernization programs and increasing chronic disease burden. The aging population is driving higher demand for long-term intravenous therapy. Expansion of home healthcare and outpatient infusion services is reducing hospital dependency and improving patient accessibility to IV treatments. Investments in hospital infrastructure upgrades are also supporting market growth.

Europe IV Tubing Sets and Accessories Market Trends

Europe is likely to be a significant market for IV tubing sets and accessories in 2026, due to strict regulatory frameworks, an aging population, and a rising focus on infection control. Hospitals are increasingly adopting closed IV systems and needle-free connectors to minimize hospital-acquired infections. Healthcare systems are investing in advanced disposable devices and smart infusion technologies to improve safety and efficiency. For instance, Fresenius Kabi provides widely used IV infusion systems across European hospitals, supporting safe and precise drug delivery in critical care environments.

U.K. IV Tubing Sets and Accessories Market Trends

The U.K. is a significant market for IV tubing sets and accessories, supported by NHS modernization programs, rising surgical procedures, and increasing pressure on hospital capacity. Expansion of home healthcare services is supporting outpatient infusion growth. An aging population and rising chronic disease incidence are significantly increasing demand for IV consumables across healthcare facilities. Investments in hospital efficiency and patient safety are supporting market expansion.

Germany IV Tubing Sets and Accessories Market Trends

Germany dominates the regional market due to its highly advanced hospital infrastructure, strong medical device manufacturing capabilities, and increasing adoption of precision infusion systems. Hospitals are investing in ICU modernization and digital healthcare transformation, increasing demand for smart IV technologies. Strict infection-control regulations are accelerating the adoption of closed IV systems. Rising chronic disease burden is increasing long-term infusion therapy demand.

Asia Pacific IV Tubing Sets and Accessories Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by its rapid healthcare infrastructure expansion, increasing surgical volumes, and rising chronic disease burden. Hospitals are expanding capacity in urban and semi-urban regions, driving higher demand for IV consumables. For example, B. Braun Melsungen AG is strengthening its presence across Asia Pacific by supplying advanced IV therapy solutions to major hospital networks.

China IV Tubing Sets and Accessories Market Trends

China dominates the regional market, supported by increasing ICU capacity and the rising prevalence of chronic diseases. Government healthcare reforms and investments in tertiary hospitals are improving access to advanced infusion therapies. China is also focusing on domestic medical device manufacturing to reduce import dependency. Adoption of smart hospital systems and digital healthcare technologies is improving infusion efficiency and safety.

India IV Tubing Sets and Accessories Market Trends

India is a significant market for IV tubing sets and accessories, due to expanding healthcare infrastructure, rising surgical volumes, and increasing hospital admissions. Government initiatives such as Ayushman Bharat are improving healthcare access for a large population base. The growth of private hospitals and home healthcare services is increasing the demand for IV consumables. Increasing awareness of infection control and affordable infusion solutions is accelerating market adoption.

Competitive Landscape

The global IV tubing sets and accessories market exhibits a moderately fragmented structure, driven by the presence of multinational medical device manufacturers, regional infusion therapy suppliers, and specialized IV consumable providers. Market competition is influenced by increasing demand for infection-prevention technologies, smart infusion compatibility, and high-performance disposable tubing systems across hospitals and ambulatory care settings.

With key leaders including Baxter International, BD, ICU Medical, Inc., and Fresenius Kabi, the market continues to witness strong investment in advanced infusion technologies and safety-focused IV administration solutions. These players compete through product innovation, strategic partnerships, hospital supply agreements, regulatory compliance, and expansion of integrated infusion therapy portfolios.

Key Industry Developments:

- In January 2026, ICU Medical received Health Canada clearance for its Plum Solo™ and Plum Duo™ precision IV pumps with LifeShield™ infusion safety software, expanding its advanced infusion therapy platform in the Canadian market. The launch strengthens ICU Medical’s position in smart infusion systems and supports improved IV medication accuracy, safety, and workflow efficiency across healthcare facilities.

- In March 2026, Baxter International introduced the IV Verify Line Labeling System, an automated IV labeling solution designed to improve medication safety and streamline nursing workflows in healthcare settings. The system uses barcode scanning and color-coded adhesive labels to replace handwritten IV labels, helping reduce medication administration errors and improve line-tracing accuracy in critical care environments.

Companies Covered in IV Tubing Sets and Accessories Market

- Ips BD

- Focus Technology Co., Ltd

- Baxter

- ICU Medical, Inc.

- Perfect Medical Ind. Co., Ltd.

- Dynarex Corporation

- TrueCare Biomedix

- Fresenius Kabi USA

- Healthline Medical Products

- Nipro Medical Corporation

- Polymedicure

- Amsino International, Inc.

Frequently Asked Questions

The global IV tubing sets and accessories market is projected to reach US$1.6 billion in 2026.

The IV tubing sets and accessories market is driven by rising surgical procedures, increasing chronic disease prevalence, growing demand for intravenous therapies, and expanding adoption of infection-prevention and smart infusion technologies.

The IV tubing sets and accessories market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Key market opportunities in the IV tubing sets and accessories market include expanding home infusion therapy, increasing adoption of smart infusion systems, rising demand for needle-free closed IV solutions, and healthcare infrastructure growth in emerging economies.

BD (Becton, Dickinson and Company), Focus Technology Co., Ltd, Baxter, and Perfect Medical Ind. Co., Ltd. are the leading players.