- Food Ingredients & Additives

- Seaweed Cultivation Market

Seaweed Cultivation Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Seaweed Cultivation Market By Species Type (Red Seaweed, Brown Seaweed), Cultivation Technique (Nearshore, Offshore), Form, Application, and Regional Analysis for 2025 - 2032

Seaweed Cultivation Market Size and Trends Analysis

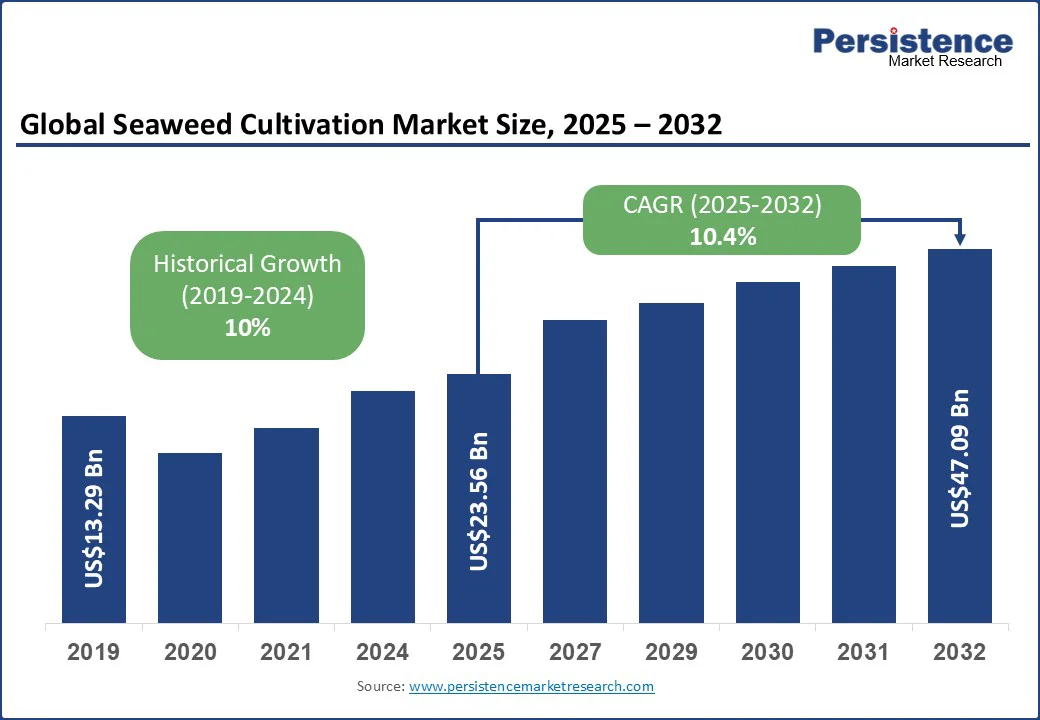

The global seaweed cultivation market size is likely to be valued at US$23.56 Bn in 2025 and is expected to reach US$47.09 Bn by 2032, growing at a CAGR of 10.4% during the forecast period from 2025 to 2032.

The seaweed cultivation market growth is driven by the rising consumer demand for plant-based nutrition, increasing use of seaweed extracts in biostimulants and animal feed, and supportive government initiatives for sustainable aquaculture.

Seaweed is emerging as a key segment within the aquaculture and sustainable food industries, driven by its diverse applications across food, pharmaceuticals, agriculture, cosmetics, and biofuel production. With Asia Pacific leading production and new offshore farming technologies expanding capacity, the market is set to benefit from both environmental advantages and growing investments in seaweed-based value chains.

Key Industry Highlights

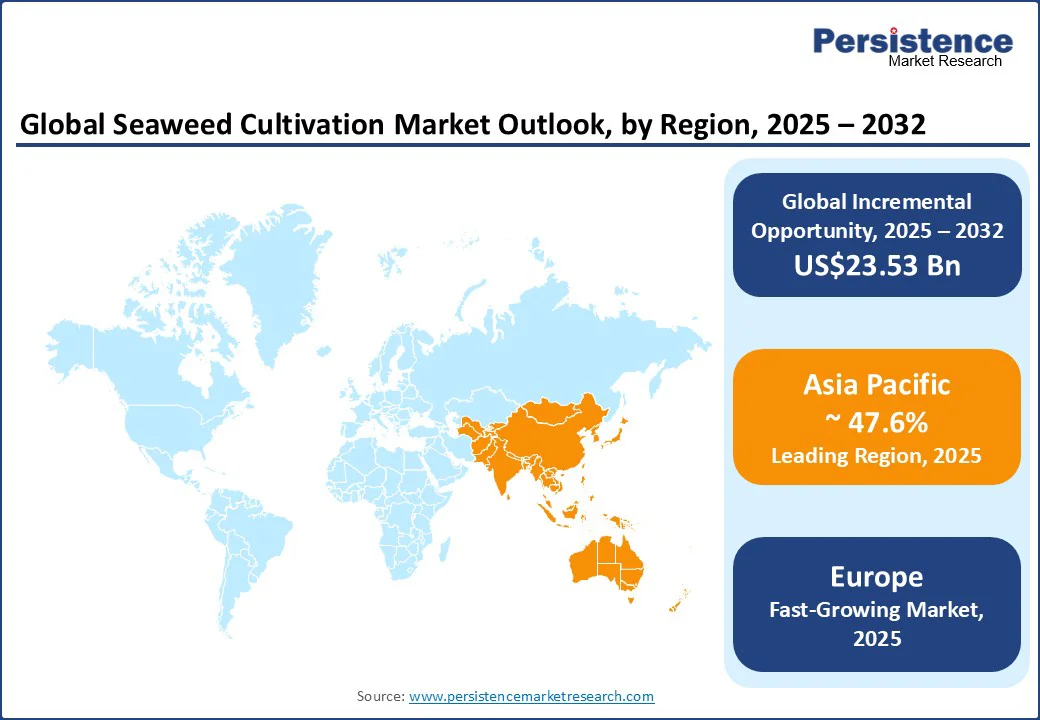

- Leading Region: Asia Pacific is anticipated to dominate the market in 2025, accounting for over 70% share, driven by large-scale production in China, Indonesia, and South Korea.

- Fastest Growing Region: Europe is projected to emerge as the fastest growing region with strong government support, strict environmental regulations, and a growing demand for vegan, clean-label, and bio-based products.

- Dominant Species Type: Red seaweed is expected to lead the market with more than 49% of the market share in 2025, largely due to its use in carrageenan and agar for food and pharmaceutical applications.

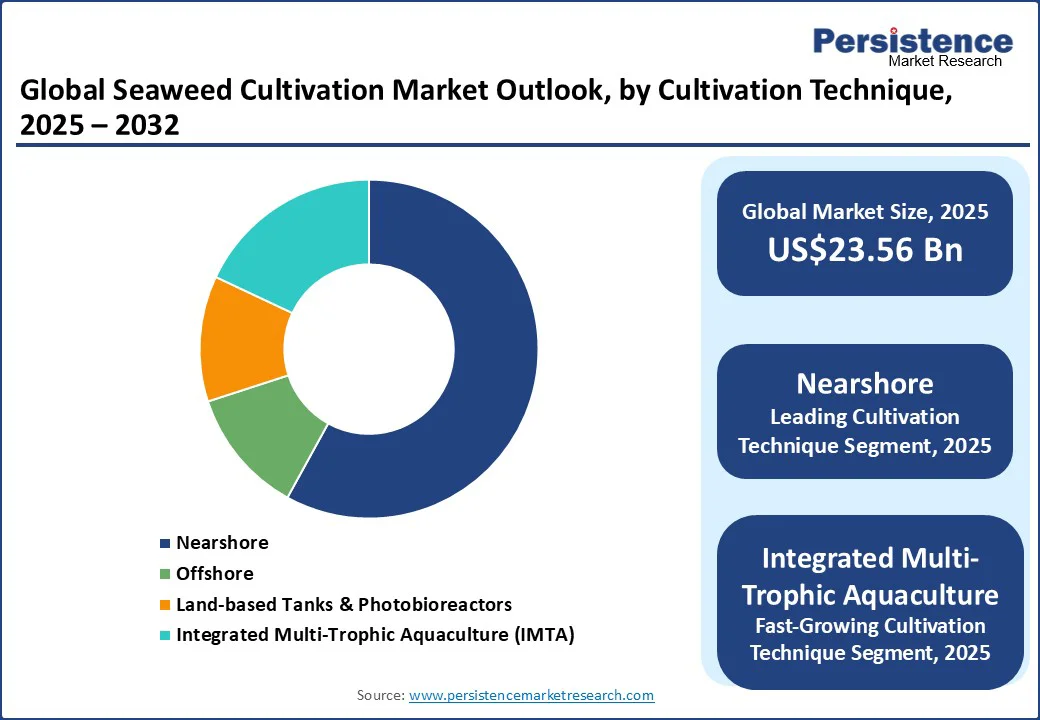

- Leading Cultivation Technique: Nearshore cultivation is expected to lead the market in 2025 with a 58% share, dominating production volume and geographic reach due to its cost-efficiency, accessibility, and scalability.

|

Global Market Attribute |

Key Insights |

|

Seaweed Cultivation Market Size (2025E) |

US$23.56 Bn |

|

Market Value Forecast (2032F) |

US$47.09 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10% |

Market Dynamics

Driver - Climate-Driven Demand for Methane Reduction and Sustainable Bioproducts

The primary growth driver for the seaweed cultivation market is the rising demand for Asparagopsis taxiformis as a livestock feed additive to cut methane emissions from cattle. Scientific trials have shown that including just 0.2% of this red algae in ruminant feed can reduce methane emissions by up to 99%.

This breakthrough is driving dairy and meat producers to secure reliable supplies of farmed Asparagopsis, as it helps reduce their environmental footprint. As climate regulations tighten and sustainability reporting becomes mandatory across agri-food chains, large-scale cultivation of this premium species is gaining strong commercial interest.

Another driver is the expanding use of seaweed-based extracts in agriculture and packaging applications. Seaweed biostimulants, rich in polysaccharides and natural hormones, are being adopted to improve soil health, boost crop resilience against drought and salinity, and reduce dependence on chemical fertilizers.

Hydrocolloid-rich seaweed is emerging as a sustainable raw material for biodegradable plastics, particularly in food packaging films. Its rapid growth in marine environments, combined with its carbon-sequestering ability, makes it one of the most promising natural feedstocks for replacing single-use plastics.

Restraint - Biological Risks and Infrastructure Limitations Impeding Expansion

One of the biggest restraints is the growing impact of disease outbreaks such as ice-ice syndrome and epiphytic filamentous algae (EFA). These conditions particularly affect red algae such as Kappaphycus, which are widely farmed for carrageenan production.

Outbreaks are triggered by rising sea temperatures, fluctuating salinity, and nutrient imbalances, often causing large portions of seaweed biomass to detach and die. Regions such as Tanzania and Madagascar have already witnessed dramatic production collapses due to these challenges, forcing many smallholder farmers to scale back or abandon their farms.

Another major challenge comes from post-harvest losses and limited hatchery infrastructure. Freshly harvested seaweed begins to degrade within 12-15 hours if not processed quickly, which forces farmers to either operate near processing facilities or invest in expensive preservation techniques.

This short shelf-life makes it difficult to expand farming into new coastal regions where processing infrastructure is limited. The lack of advanced hatchery systems for selective breeding has slowed progress in developing stronger, climate-resilient seaweed strains. Technical hurdles, such as ensuring spore survival and controlling reproduction cycles, limit the availability of high-yield, disease-resistant varieties.

Opportunity - High-Value Functional Ingredients and Blue Carbon Potential

Seaweed cultivation presents strong opportunities in the development of functional food ingredients and nutraceutical applications. Seaweed is rich in bioactive compounds such as fucoidans, laminarins, and carrageenans, which have shown potential benefits for gut health, immune support, and anti-inflammatory properties.

With rising consumer interest in plant-based and clean-label products, there is a growing demand for natural ingredients that can replace synthetic additives in food and beverages. Cultivators specializing in species rich in these bioactive compounds are uniquely positioned to establish strategic partnerships with health food manufacturers, dietary supplement brands, and wellness-focused product developers.

Another promising opportunity lies in the use of seaweed for blue carbon credits and ecosystem restoration projects. Large-scale seaweed farms not only act as a renewable biomass source but also play a role in carbon sequestration, nitrogen absorption, and ocean de-acidification.

Offshore farming initiatives that integrate seaweed with shellfish or fish cultivation are being explored as sustainable solutions for both food production and environmental management. This dual value, commercial output and ecological services, positions seaweed cultivation as a strategic sector in the transition to a low-carbon, regenerative economy.

Category-wise Analysis

Species Type Insights

The largest segment in seaweed cultivation is expected to be red seaweed, which accounts for over 49% of the global market share. Red seaweeds such as Kappaphycus, Eucheuma, Gracilaria, and Asparagopsis are in high demand for their hydrocolloid content, including agar, carrageenan, and agarose.

These compounds are essential in food processing, pharmaceuticals, and cosmetics, making red seaweed the backbone of commercial seaweed farming. A notable example is Asparagopsis taxiformis, which is increasingly cultivated as a livestock feed additive to reduce methane emissions, demonstrating both environmental and commercial value.

The fastest-growing segment is green seaweed, driven by rising interest in its nutritional and industrial applications. Species such as Ulva (sea lettuce), Caulerpa, and Cladophora are gaining attention for their high protein content, use in functional foods, biofertilizers, and potential in biofuel production due to rapid growth and carbohydrate richness. While green seaweed currently has a smaller market share compared to red seaweed, its growth trajectory is strong, fueled by innovation in the food and renewable energy sectors.

Cultivation Technique Insights

Nearshore cultivation is likely to be the leading segment in 2025 with 58% share. It dominates in both production volume and geographic spread due to its cost-efficiency, accessibility, and scalability. Nearshore systems are typically set up within a few hundred meters from the coastline, where water depth, salinity, and wave conditions are suitable for seaweed growth without requiring advanced technology or heavy infrastructure. Techniques such as rope lines, rafts, off-bottom grids, and nets are commonly used. These systems are simple to install and manage, making them ideal for smallholder farmers and larger cooperatives.

Maintenance and harvesting are relatively easy, and the setup minimizes disruption to marine ecosystems. Nearshore farms benefit from lower operational costs compared to offshore systems, which require vessels, moorings, and automation for deep-water deployment. For example, in Zanzibar, farmers cultivate Eucheuma denticulatum using off-bottom rope systems in nearshore waters, achieving high yields with minimal infrastructure.

Integrated multi-trophic aquaculture (IMTA) is expected to be the fastest-growing segment in 2025. IMTA combines seaweed farming with other aquaculture species, such as fish or shellfish, creating a sustainable ecosystem that improves water quality and provides multiple revenue streams.

IMTA systems are gaining traction in Europe, North America, and Asia, as they address environmental concerns while increasing profitability. This approach allows farmers to produce high-quality seaweed while supporting overall ecosystem health, making it an attractive growth area for the industry.

Regional Insights

Asia Pacific Seaweed Cultivation Market Trends - Expanding Aquaculture Innovation and Sustainable Food Applications

Asia Pacific is projected to be the global epicenter of seaweed cultivation in 2025, with a share of 47.6%, producing the vast majority of the world’s supply due to its long coastlines, favorable growing conditions, and deep-rooted cultural integration of seaweed in food and agriculture. Countries such as China, Indonesia, the Philippines, and South Korea dominate the market through both traditional and industrial-scale cultivation.

The region is not only the leader in volume, but it is also advancing rapidly in innovation. There is a strong push toward offshore systems, selective breeding for climate-resilient species, and the commercialization of seaweed in biofuels, pharmaceuticals, and biodegradable materials. National policies in many Asia Pacific countries actively support aquaculture development through subsidies, R&D funding, and export promotion.

South Korea leads the region in both production and scientific advancement. Seaweed, particularly gim (nori), makes up about 76% of the country’s total aquaculture output. The industry is highly structured, with government-backed programs such as the Golden Seed Project investing in selective breeding for disease resistance, faster growth, and better nutritional profiles.

In 2024, South Korea made headlines by becoming the first country to achieve dual MSC-ASC certification for sustainable seaweed production, earned by the Sinan Bada Fishery Corporation. South Korea is experimenting with early IMTA systems and is investing in turning seaweed waste into bioenergy.

Europe Seaweed Cultivation Market Trends - Advancing Algae Biotech Research and Growing Focus on Climate-Resilient Marine Industries

Europe is currently the fastest-growing regional market, holding a projected high CAGR, due to strong government support, strict environmental regulations, and a growing demand for vegan, clean-label, and bio-based products. While Europe historically relied on imports, especially from Asia, it is now building domestic capacity across coastal nations, particularly through offshore cultivation and vertical farming.

Seaweed is being explored not just as a food source but also as a key input for biodegradable plastics, pharmaceuticals, animal feed, and carbon sequestration strategies. The European Union has provided funding and policy direction to promote seaweed as a component of the circular economy and the Blue Bioeconomy Strategy, including pilot projects that align seaweed cultivation with offshore wind infrastructure.

In the Netherlands, innovation is thriving through projects such as AlgaeDemo, which has developed advanced offshore seaweed farms using textile-based substrates and autonomous underwater vehicles for efficient seeding, monitoring, and harvesting.

The country is planning to allocate over 400 km² of North Sea space specifically for seaweed farming, often in multi-use zones near wind farms. In 2024, the Dutch government also trialed a mechanical offshore harvester, a key step toward industrial-scale production.

North America Seaweed Cultivation Market Trends - Seaweed-Based Functional Foods and Expanding Sustainable Farming Practice

North America is steadily emerging as a hub for sustainable seaweed innovation, driven by rising consumer awareness of plant-based nutrition, climate-conscious agriculture, and the blue economy. It is carving out a niche in regenerative ocean farming and methane-reducing feed applications.

IMTA, which co-cultivates seaweed alongside shellfish or finfish, is gaining significant momentum as both an ecological and economic model. Venture-backed startups and academic research are driving new technologies for carbon sequestration, sustainable packaging, and biofertilizer development.

In the U.S., Maine is leading by example in integrated seaweed and shellfish farming. Bangs Island Mussels has successfully deployed IMTA systems that cultivate kelp alongside mussels and oysters, using the seaweed to absorb excess carbon and nitrogen from the water, thus improving shellfish quality and growth. In Hawaii, red algae species such as Asparagopsis taxiformis are being trialed as methane-reducing cattle feed.

A notable initiative is Symbrosia’s pilot with Parker Ranch, one of the largest cattle ranches in the U.S., which demonstrated up to 77% methane reduction in cattle. The project received over USD$2.2 Mn in federal grants to scale operations. Organizations such as GreenWave are championing 3D ocean farming vertical farms that grow seaweed and shellfish together for ecological restoration and local food systems.

Competitive Landscape

The global seaweed cultivation market is highly fragmented, with dominance from Asia Pacific producers and growing participation from Western innovators. In countries, including China, Indonesia, and South Korea, production is primarily driven by large-scale farming cooperatives and community-based aquaculture, supplying raw materials for food, feed, and hydrocolloid industries. These markets benefit from favorable coastal resources, established farming practices, and strong government support, making Asia Pacific the clear global leader.

North America and Europe are witnessing a surge in start-ups and mid-sized companies focusing on high-value applications such as bio-packaging, nutraceuticals, and methane-reducing animal feed. Companies such as Atlantic Sea Farms (U.S.), Symbrosia (Hawaii), and Algaia (France) are examples of innovators leveraging technology, sustainability credentials, and strategic partnerships to capture niche markets.

Key Industry Development

- In August 2025, Finland’s Origin by Ocean secured US$7.5 Mn in seed funding to process sargassum into high-quality alginate and fucoidan for textiles and cosmetics. The target is a production facility in Finland producing 4,000 tonnes of sargassum annually by 2028, with plans to expand into the Caribbean by 2032.

- In March 2025, the startup Marine Biologics is advancing a novel “Seaweed Slurry” fermentation process, creating ingredient streams for food emulsifiers, cosmetics, and biomaterials. Termed SuperCrudes, these are benchmarked similarly to petroleum grades, offering a modular, sustainable platform with early-stage demonstrations slated for a Future Food Tech event.

Companies Covered in Seaweed Cultivation Market

- Cargill, Incorporated

- Algaia SA

- Acadian Seaplants Limited

- Indo Alginate

- Seasol International Pty Ltd.

- Ocean Rainforest Sp/F

- Atlantic Sea Farms

- Mara Seaweed

- Symbrosia

- Sea6 Energy Pvt. Ltd.

- Gelymar SA

- China National Agricultural Development Group

- Rongcheng Yandunjiao Aquatic Co., Ltd.

- DuPont Nutrition & Biosciences

- Kelpak

- Irish Seaweeds

- AlgAran Ltd.

- FMC Corporation

- Ocean Harvest Technology

- Umami Bioworks

Frequently Asked Questions

The seaweed cultivation market is estimated to reach US$23.56 Bn in 2025.

By 2032, the market is projected to be valued at US$47.09 Bn.

Key trends include the expansion of integrated multi-trophic aquaculture (IMTA), the adoption of offshore seaweed farming technologies, and the development of seaweed-based bioplastics and textiles.

By species type, red seaweed dominates the market with over 49% share, largely due to its use in carrageenan, agar, and food applications. By cultivation technique, nearshore farming holds the largest share of 58%.

The market is expected to grow at a CAGR of 10.4% from 2025 to 2032, fueled by rising demand in food, feed, pharmaceuticals, and sustainable packaging industries.

The leading companies include Cargill, Incorporated, Algaia SA, Acadian Seaplants Limited, Indo Alginate, and Seasol International.