- Pharmaceuticals

- Injectable Drug Delivery Market

Injectable Drug Delivery Market Size, Share, and Growth Forecast, 2026 - 2033

Injectable Drug Delivery Market by Device Type (Conventional Injection Devices, Prefilled Syringes, Auto-Injectors, Others), Route of Administration (Intravenous, Intramuscular, Subcutaneous), End-user (Hospitals & Clinics, Home Care Settings, Others), and Regional Analysis for 2026 - 2033

Injectable Drug Delivery Market Share and Trends Analysis

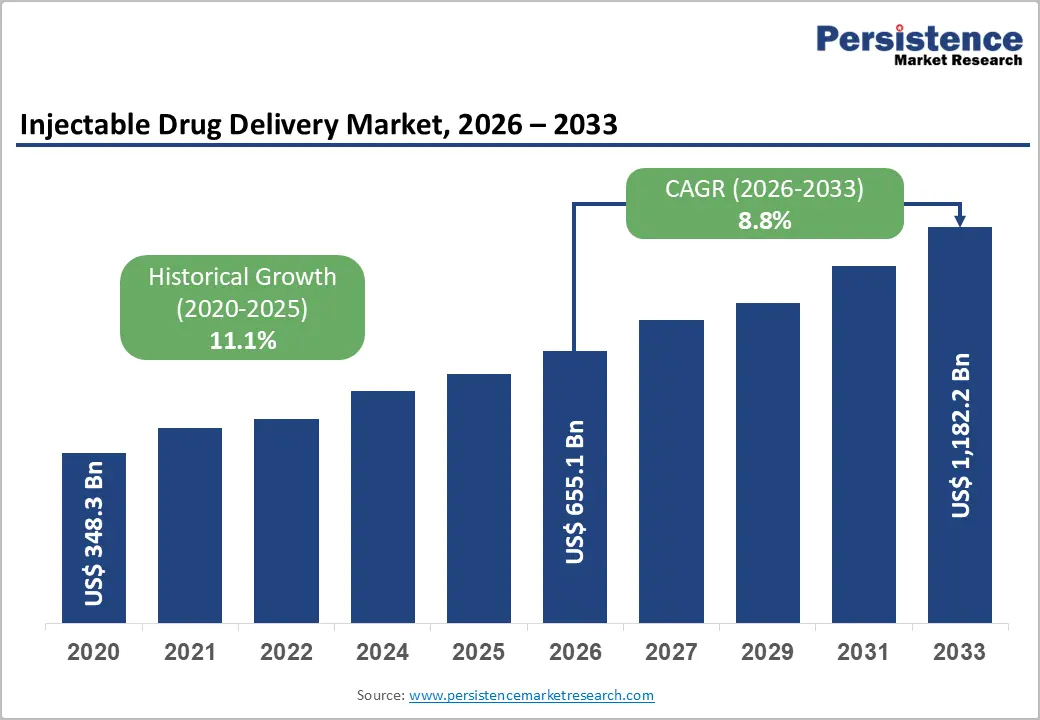

The global injectable drug delivery market size is likely to be valued at US$655.1 billion in 2026 and is estimated to reach US$1182.2 billion by 2033, growing at a CAGR of 8.8% during the forecast period 2026 - 2033, driven by a convergence of aging demographics, accelerating biologics adoption, regulatory modernization, and expanding healthcare infrastructure across emerging economies.

The rising global burden of chronic diseases, including diabetes, oncology, and autoimmune conditions, as documented by the World Health Organization and the U.S. Centers for Disease Control and Prevention, is structurally expanding demand for parenteral drug administration routes that deliver faster therapeutic onset compared to oral alternatives.

Key Industry Highlights:

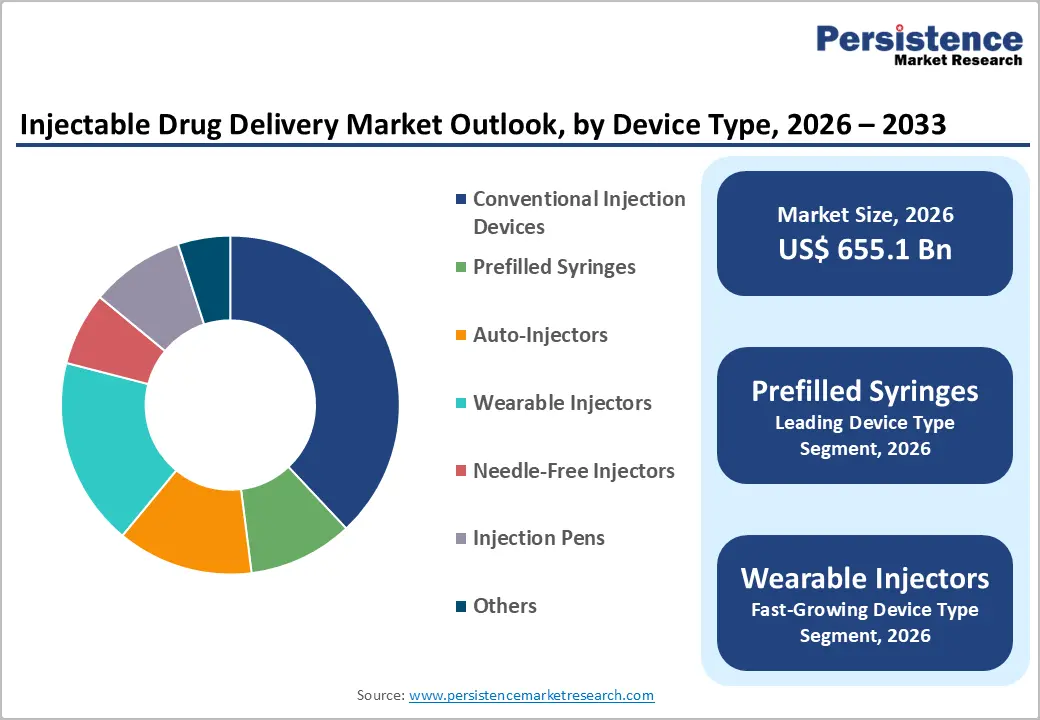

- Leading Device Type: Prefilled syringes are set to hold around 38% revenue share in 2026, driven by broad biologic fill finish adoption across hospital and home care channels.

- Fastest-growing Device Type: Wearable injectors are projected as the fastest-growing segment, supported by the accelerating shift of large volume biologic therapies to home administration settings.

- Leading End-user: Hospitals and clinics are estimated to hold roughly 52% revenue share in 2026, due to their role as the primary institutional site for complex parenteral therapy initiation.

- Fastest-Growing End-user: Home care settings are forecast to record the fastest growth, driven by auto-injector and wearable device proliferation, enabling safe self-administration of chronic disease biologics.

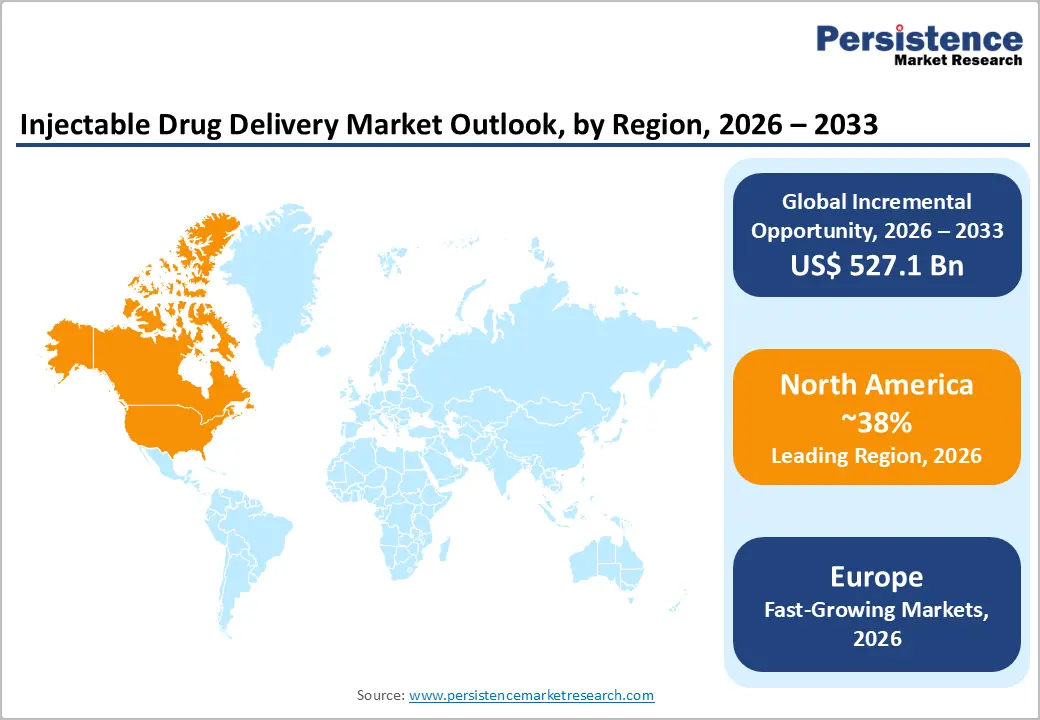

- Regional Leadership: North America is projected to capture roughly 38% of the injectable drug delivery market share in 2026, while Europe is forecast to record the fastest growth due to harmonized regulatory approval frameworks.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Becton Dickinson and West Pharmaceutical Services leveraging scale, co-development partnerships, and platform integration to maintain competitive positioning.

DRO Analysis

Driver - Growing Burden of Chronic Diseases Driving Injectable Therapy Demand

The structural rise in chronic disease incidence is the primary demand catalyst for injectable drug delivery. According to the International Diabetes Federation, approximately 537 million adults globally were living with diabetes in 2021, a figure projected to rise to 783 million by 2045, generating an enormous base of patients requiring insulin and GLP-1 receptor agonist injections on a daily or weekly basis. This demographic reality creates a non-discretionary, recurring demand base for injection devices and drug formulation platforms that grows independently of economic cycles.

Oncology and immunology are generating parallel structural demand. The National Cancer Institute documented over 2,041,910 new cancer diagnoses in the United States alone in 2025, the majority of which involve chemotherapy or biologics administered via intravenous or subcutaneous injection. The clinical efficacy advantages of parenteral administration over oral routes for high molecular weight biologics make substitution unlikely, locking in long-term demand for sophisticated delivery platforms across hospital, ambulatory, and home care settings.

Restraint - Needle-Related Safety Concerns and Regulatory Compliance Burden

Needle-stick injuries and contamination risks remain significant operational concerns across hospitals, clinics, and home healthcare environments. Healthcare institutions are required to comply with stringent regulatory standards covering sterility assurance, disposal management, and device safety validation. Complex approval pathways for combination products are extending commercialization timelines for advanced injectable delivery systems.

Manufacturers face high compliance costs associated with quality assurance, clinical validation, and post-market surveillance requirements. Product recalls related to contamination or device malfunction can damage brand credibility and increase financial liabilities. Limited patient acceptance of needle-based therapies in specific demographics is also constraining adoption rates for certain injectable treatment categories.

Opportunity - Wearable Injector Adoption Enabling Large Volume Subcutaneous Drug Delivery

Wearable injectors represent a transformative delivery innovation enabling subcutaneous administration of large volume biologics that previously required intravenous infusion in clinical settings. The migration of these therapies to the home setting reduces healthcare system cost burden while improving patient quality of life, creating a policy-aligned growth pathway that is gaining support from payers and national health authorities. The U.S. Centers for Medicare and Medicaid Services has been progressively expanding reimbursement frameworks for home-administered biologics, creating a regulatory tailwind for wearable injector platform adoption.

Pharmaceutical manufacturers are actively partnering with device companies to develop drug-device combination products built around wearable injector platforms, embedding delivery technology into branded therapy differentiation strategies. Companies such as Becton Dickinson, Enable Injections, and West Pharmaceutical Services are receiving increased development partnership inquiries, signaling accelerating pipeline activity. The convergence of digital connectivity features, such as Bluetooth-enabled adherence monitoring, into next-generation wearable injectors is further differentiating the platform and expanding its appeal across specialty therapy categories.

Category-wise Analysis

Device Type Insights

Prefilled syringes are anticipated to secure around 38% of the injectable drug delivery market share in 2026, reflecting the segment's critical role in enabling safe, accurate, and ready-to-use drug administration across hospital and home care settings. Manufacturers such as Gerresheimer and Schott have expanded capacity to meet biologic fill finish demand, illustrating the segment's centrality. The elimination of reconstitution steps reduces medication errors and supports regulatory compliance in high acuity care environments.

Wearable injectors are expected to be the fastest-growing segment, propelled by the accelerating shift of large volume biologic therapies from infusion centers to patient home settings. Amgen and Halozyme Therapeutics have integrated wearable delivery into their biologic commercialization strategies, exemplifying adoption momentum. Regulatory endorsement of home-administered combination products and payer incentives favoring outpatient therapy are reinforcing the structural demand trajectory for this segment.

Route of Administration Insights

Intravenous routes are poised to dominate with a forecast market share of over 45% in 2026, powered by their indispensability in oncology, critical care, and anti-infective therapy, where rapid systemic drug distribution is clinically required. Hospital-based IV therapy protocols for sepsis management, as standardized by the Surviving Sepsis Campaign guidelines, demonstrate the non-discretionary nature of this route. The intravenous segment's dominance is reinforced by the irreplaceability of rapid-onset delivery in acute care scenarios.

Subcutaneous is estimated to be the fastest-growing segment, fueled by the proliferating approval of subcutaneous formulations for therapies historically requiring intravenous administration. Roche's FDA-approved subcutaneous formulation of Herceptin illustrates how reformulation investments are enabling outpatient and self-administration of complex oncology therapies. Patient preference for less invasive, self-managed injection experiences combined with payer pressure to reduce infusion center utilization is driving rapid adoption.

End-user Insights

Hospitals and clinics are likely to be the leading segment with a projected 52% of the injectable drug delivery market share in 2026 due to their role as the primary site of complex parenteral therapy initiation, including chemotherapy, immunosuppressants, and acute care regimens. Cleveland Clinic and Mayo Clinic exemplify integrated health systems that standardize injectable protocols across oncology and critical care service lines. The concentration of high acuity patient populations and physician oversight requirements sustains the institutional dominance of this segment.

Home care settings are anticipated to be the fastest-growing segment, fueled by the structural migration of chronic disease management from institutional to patient-centric environments enabled by auto-injectors, prefilled pens, and wearable devices. Fresenius Kabi's expansion of home infusion services across North America illustrates the commercial investment in this channel. Reimbursement policy evolution and digital health integration are accelerating the safe transfer of complex injectable therapies to the home environment.

Regional Insights

North America Injectable Drug Delivery Market Trends

North America is expected to lead with an estimated 38% of the injectable drug delivery market share in 2026, supported by early technology adoption and a high concentration of established biopharmaceutical enterprises. The regional market exhibits high healthcare expenditure and rapid integration of smart, connected therapeutic devices into commercial health insurance reimbursement models. High rates of diagnosed metabolic and cardiovascular diseases necessitate advanced self-injection technologies.

U.S. Injectable Drug Delivery Market Insights

The U.S. market is projected to see sustained capital inflows driven by private biotechnology investments and ongoing FDA approvals for novel combination products. The implementation of strict safe-needle legislation across domestic clinical systems mandates continuous procurement of passive sharps protection mechanisms. Rising demand for localized specialty pharmacy services accelerates home-based biologic delivery integration.

Canada Injectable Drug Delivery Market Insights

The Canada market is forecast to expand due to increasing provincial healthcare funding aimed at optimizing home-based care for seniors. Public procurement frameworks focus on long-term cost reduction, favoring reusable auto-injector platforms over completely disposable alternatives. Collaborative efforts between regional university research laboratories and medical device producers support localized engineering innovations.

Europe Injectable Drug Delivery Market Trends

Europe is forecast to be the fastest-growing market for injectable drug delivery, stimulated by harmonized regulatory approval frameworks and widespread public health support for self-administered chronic therapies. The implementation of unified European Medical Device Regulations demands strict human factors validation, pushing manufacturers to innovate ergonomic design and safety. National health programs integrate advanced delivery systems to lower hospital re-admission expenditures.

Germany Injectable Drug Delivery Market Insights

The Germany market is likely to lead regional growth owing to advanced industrial manufacturing infrastructure and specialized polymer injection molding expertise. Domestic production facilities expand capacity to meet global contract manufacturing demands for prefilled syringe sub-assemblies. German statutory health insurance funds provide comprehensive reimbursement coverage for digital health applications tied to smart injectors.

U.K. Injectable Drug Delivery Market Insights

The U.K. market is expected to focus heavily on cost-efficient biosimilar deployment, which requires compatible, low-cost parenteral delivery systems. The National Health Service implements strategic purchasing initiatives to move chronic disease therapies out of centralized clinics into community-based care models. This strategy drives continuous bulk procurement of auto-injectors.

Asia Pacific Injectable Drug Delivery Market Trends

The Asia Pacific market is likely to expand due to rapid healthcare infrastructure modernization and expanding public immunization programs. Local healthcare ministries focus on improving rural access to essential therapeutics, driving high volume consumption of conventional injection technologies. Rising disposable income across urban centers increases private market demand for advanced diabetes care platforms.

China Injectable Drug Delivery Market Insights

The China market is anticipated to experience high volume growth as domestic biopharmaceutical companies expand clinical pipelines for monoclonal antibodies. Government mandates focused on domestic healthcare equipment manufacturing drive regional production facility upgrades. Expanding clinical hospital networks across secondary cities accelerates the bulk acquisition of automated infusion technologies.

Japan Injectable Drug Delivery Market Insights

The Japanese market is forecast to prioritize specialized delivery systems tailored for an advanced geriatric demographic with physical limitations. Medical device developers focus on engineering low-force activation mechanisms and highly visible dosage indicators to overcome age-related visual and dexterity challenges. Strict national quality standards ensure a preference for premium, high-precision component manufacturing.

Competitive Landscape

The global injectable drug delivery market is moderately consolidated, with a small number of large-scale multinational manufacturers controlling significant shares of device production, primary packaging, and drug-device combination product development. Key industries include Becton Dickinson, West Pharmaceutical Services, Gerresheimer, Baxter International, and Terumo Corporation.

Mid-tier and regional participants compete through specialization in niche device categories, geographic focus, or contract manufacturing services for emerging biotech firms whose pipeline products require customized delivery solutions.

Key Industry Developments:

- In May 2026, Roche Pharma launched India’s first 7-minute injectable immunotherapy, Tecentriq SC, for lung cancer treatment, strengthening innovation in rapid subcutaneous drug delivery solutions for oncology care.

- In December 2025, Intas Pharmaceuticals partnered with IntegriMedical to launch India’s first needle-free injection system for IVF and gynecology, reinforcing innovation in patient-centric injectable drug delivery technologies.

- In October 2025, Lupin Limited launched a strategic partnership program to expand its PrecisionSphere long-acting injectable platform, reinforcing innovation in sustained-release injectable drug delivery technologies.

Companies Covered in Injectable Drug Delivery Market

- Becton, Dickinson and Company

- West Pharmaceutical Services, Inc.

- Gerresheimer AG

- Ypsomed Holding AG

- SHL Medical AG

- Stevanato Group S.p.A.

- Schott AG

- Terumo Corporation

- Owen Mumford Ltd.

- Nemera France SAS

- Haselmeier GmbH

- Bespak

- AptarGroup, Inc.

- Nipro Corporation

- Medtronic plc

Frequently Asked Questions

The global injectable drug delivery market is projected to reach US$655.1 billion in 2026.

The rising prevalence of chronic diseases and increasing adoption of biologics are driving demand for advanced injectable drug delivery systems.

The injectable drug delivery market is poised to witness a CAGR of 8.8% from 2026 to 2033.

Expansion of self-administration technologies and growing adoption of wearable injectors are creating significant opportunities in the injectable drug delivery market.

Some of the key market players include Becton Dickinson, West Pharmaceutical Services, Gerresheimer, Baxter International, and Terumo Corporation.