- Medical Devices

- Ophthalmic Injectable Market

Ophthalmic Injectable Market Size, Share, and Growth Forecast, 2026 – 2033

Ophthalmic Injectable Market by Drug Class (Anti-VEGF Agents, Corticosteroids, Antibiotics, Antivirals, Antifungals), Indication (Age-Related Macular Degeneration (AMD), Diabetic Retinopathy, Retinal Vein Occlusion, Endophthalmitis, Others), End-User (Hospitals, Ophthalmology Clinics, Ambulatory Surgical Centers, Specialty Eye Centers), and Regional Analysis for 2026-2033

Ophthalmic Injectable Market Share and Trends Analysis

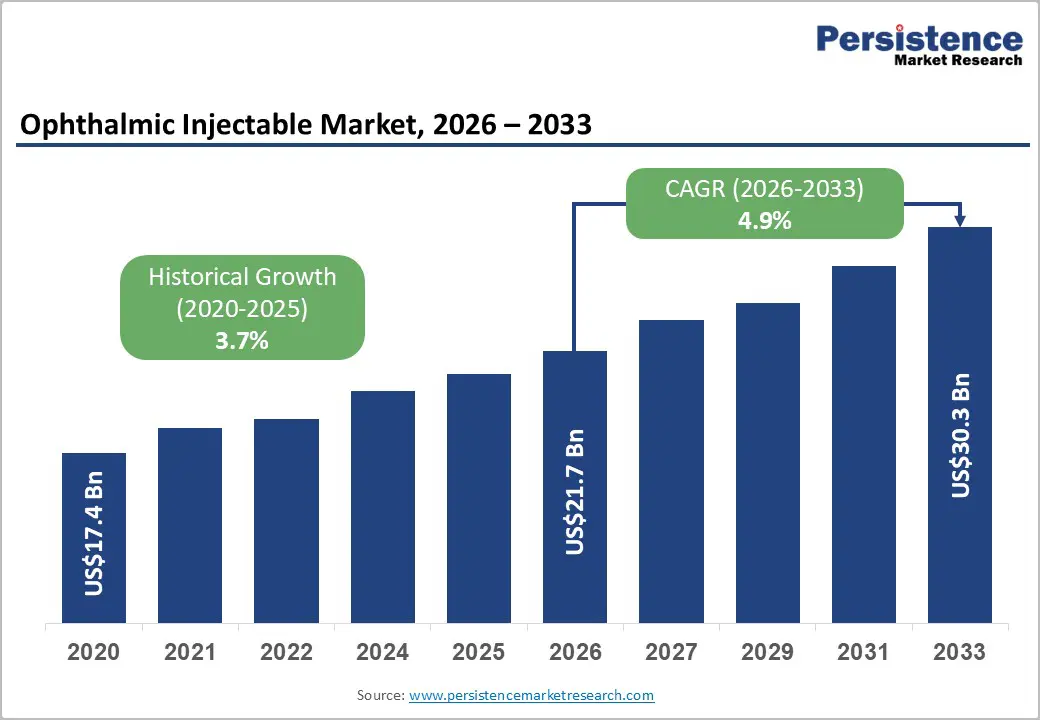

The global ophthalmic injectable market size is likely to be valued at US$ 21.7 billion in 2026, and is projected to reach US$ 30.3 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026−2033. Sustained expansion of injectable ophthalmic therapies reflects rising prevalence of retinal diseases combined with increasing clinical reliance on targeted intraocular drug delivery.

Population aging represents a major structural factor shaping demand, as retinal degeneration and microvascular ocular disorders demonstrate strong correlation with advanced age groups. Health authorities such as the World Health Organization (WHO) identify retinal diseases and diabetic eye complications as growing contributors to visual impairment globally, encouraging earlier diagnosis and structured treatment pathways.

Clinical awareness initiatives and screening programs increasingly detect retinal disorders at treatable stages, expanding the patient population eligible for injectable therapy. The U.S. Centers for Disease Control and Prevention (CDC) reports expanding surveillance programs for diabetic eye disease and retinal degeneration, which strengthens early therapeutic intervention

Key Industry Highlights

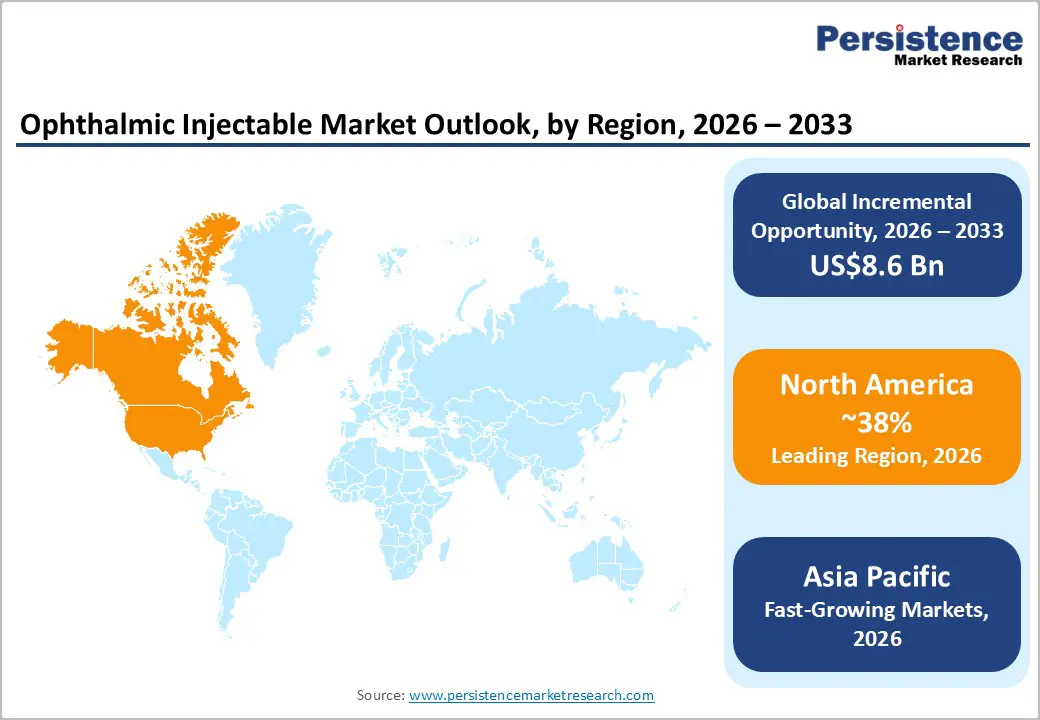

- Dominant Region: North America is expected to hold a market share of about 38% in 2026, driven by strong healthcare infrastructure in the United States and Canada.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market between 2026 and 2033, driven by expanding ophthalmology treatment in China and India.

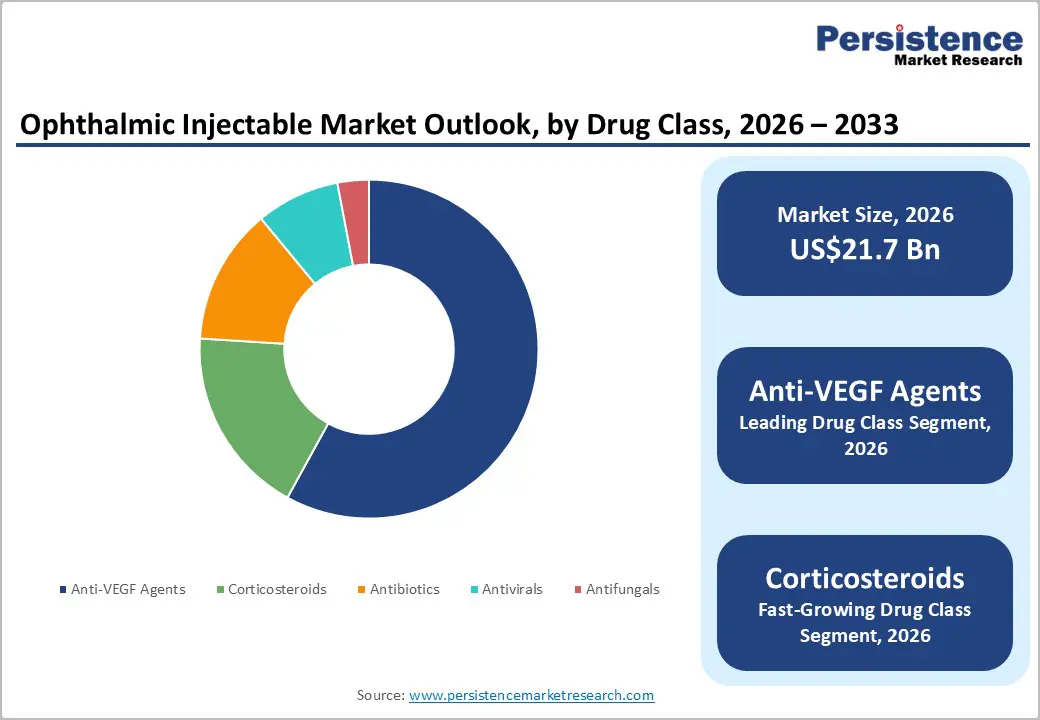

- Leading Drug Class: Anti-vascular endothelial growth factor (VEGF) agents are expected to hold about 58% revenue share in 2026, owing to the widening adoption of diabetic retinopathy treatment.

- Fastest-growing Drug Class: Corticosteroids are projected to be the fastest-growing segment during 2026–2033, on account of their increasing use in managing retinal inflammation and macular edema.

| Key Insights | Details |

|---|---|

| Ophthalmic Injectable Market Size (2026E) | US$ 21.7 Bn |

| Market Value Forecast (2033F) | US$ 30.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Retinal Disorders and Age-Related Vision Impairment

Escalating incidence of retinal diseases across aging populations creates sustained demand for targeted ocular therapeutics delivered through intravitreal administration. Degenerative retinal conditions such as age-related macular degeneration, diabetic retinopathy, and retinal vein occlusion involve progressive damage to retinal microvasculature and photoreceptor cells. Such disorders frequently require localized drug delivery directly into the vitreous cavity to achieve therapeutic concentration within retinal tissues. Epidemiological surveillance conducted by the Vision and Eye Health Surveillance System of the U.S. CDC estimated that about 19.8 million adults aged 40 years and above in the United States were living with age-related macular degeneration, a major retinal disorder linked with severe vision impairment.

Demographic transition toward older population cohorts strengthens clinical demand for therapies capable of preserving visual function during later life stages. Age-associated decline in retinal pigment epithelium performance, accumulation of drusen deposits, and chronic inflammatory signaling accelerate structural damage within macular tissue. Vision impairment originating from these mechanisms produces substantial functional limitations, including reduced reading ability, impaired mobility, and diminished productivity among older adults. Healthcare systems therefore prioritize therapeutic approaches that stabilize retinal architecture and delay disease progression.

Technological Advancement in Biologic Therapies and Intravitreal Drug Delivery

Advanced biologic drug platforms and precision injection systems support strong clinical adoption across retinal disease treatment pathways. Biologic therapies such as anti-VEGF monoclonal antibodies directly regulate pathological angiogenesis and vascular leakage in retinal tissues, enabling targeted disease control in conditions such as diabetic retinopathy, retinal vein occlusion, and age-related macular degeneration. Direct intravitreal administration allows the therapeutic molecule to reach the vitreous cavity with high ocular bioavailability and minimal systemic exposure, which improves treatment precision and safety in ophthalmic care.

Technological progress in intravitreal delivery systems strengthens clinical efficiency and procedural safety, supporting large-scale utilization across ophthalmology practices. Innovations such as micro-needle injection systems, optimized syringe design, and sustained-release ocular implants improve dosing accuracy and patient tolerance during administration. Advanced delivery platforms enable consistent drug deposition within the vitreous body, reducing variability in therapeutic exposure and supporting predictable treatment outcomes.

Prohibitive Treatment Cost and Repeated Injection Burden

Elevated therapy expenditure and continuous procedural requirements create a structural barrier for patient adherence and healthcare accessibility in retinal disease management. Biologic agents delivered through intravitreal administration involve high manufacturing complexity, cold-chain distribution, and specialized clinical infrastructure, which collectively increase treatment pricing. Each procedure requires sterile ophthalmic equipment, trained retina specialists, and monitoring of ocular parameters such as intraocular pressure and retinal thickness, generating significant clinical service costs.

Frequent intravitreal administration further intensifies treatment burden through operational and behavioral barriers. Standard regimens often require injections every four to eight weeks, leading to repeated hospital visits, procedural discomfort, and dependence on caregiver support for elderly patients. Continuous follow-up imaging and clinical evaluation increase logistical pressure on ophthalmology clinics and extend waiting periods in public healthcare facilities. Long-term therapy schedules generate psychological fatigue among patients, reducing willingness to maintain strict treatment intervals and resulting in therapy interruption or delayed dosing.

Risk of Injection-Related Complications and Clinical Procedure Requirements

Intravitreal therapy involves direct delivery of medication into the vitreous cavity through a needle-based ocular procedure. Such administration demands strict sterile technique, specialized ophthalmic equipment, and trained retinal specialists, which raises operational complexity within clinical settings. Surgical precision remains essential since the eye represents a highly sensitive organ where minor deviation during needle placement may affect retinal tissue, intraocular pressure, or lens integrity. Reported adverse events include retinal detachment, intraocular inflammation, vitreous hemorrhage, and lens damage, each requiring prompt medical management and follow-up monitoring.

Procedural requirements further introduce logistical and healthcare system constraints. Intravitreal administration occurs within sterile operating rooms or controlled ophthalmic procedure suites, involving antiseptic preparation, anesthetic administration, and post-injection monitoring. Such workflow extends procedure time and increases clinical resource utilization across hospitals and specialty eye centers. Patient perception of ocular injections may also influence treatment adherence, particularly among elderly populations managing chronic retinal disorders requiring repeated injections over multiple treatment cycles.

Development of Long-Acting Biologic Therapies and Sustained Delivery Platforms

Rising prevalence of chronic retinal disorders such as age-related macular degeneration and diabetic macular edema increases demand for therapies capable of maintaining therapeutic drug levels over extended periods. Conventional biologic injections often require administration every four to eight weeks, creating a significant treatment burden for elderly patients and overstretched ophthalmology clinics. Clinical practice data indicate a clear adherence gap when frequent dosing schedules dominate treatment pathways. For example, a 2025 clinical analysis reported that around 28.5% of patients discontinued anti-VEGF therapy during treatment, reflecting adherence limitations linked to repeated injection visits and procedural discomfort.

Technological progress in biologic engineering and intraocular delivery platforms further strengthens this opportunity. Long-acting formulations integrate high-affinity antibodies, polymer-based drug reservoirs, or refillable ocular implants that provide controlled release for several months. Continuous delivery systems demonstrate the potential to transform treatment logistics in ophthalmology clinics by minimizing repeated intravitreal procedures. A 2025 clinical program evaluating a refillable ocular implant delivering ranibizumab reported that approximately 95% of treated patients required refilling only every six months while maintaining retinal stability, demonstrating the clinical durability achieved through sustained delivery platforms.

Expansion of Ophthalmology Infrastructure in Emerging Healthcare Systems

Strengthening ophthalmology infrastructure across emerging healthcare systems creates favorable conditions for advanced ocular treatment adoption, particularly for injectable therapeutics used in retinal disorders. Government investment in specialized eye hospitals, diagnostic imaging systems, and surgical units improves clinical capacity for intravitreal drug administration and follow-up monitoring. Such therapies require sterile operating environments, trained ophthalmologists, optical coherence tomography imaging, and post-procedure surveillance. Infrastructure development directly enables these requirements. Public health initiatives aimed at blindness prevention and diabetic retinopathy screening further expand patient identification within hospital networks and specialty clinics.

Healthcare infrastructure expansion across Asia, Latin America, and parts of Africa supports the transition from basic vision correction services toward specialized retinal care and minimally invasive ophthalmic procedures. New eye clinics, ambulatory surgical units, and tertiary ophthalmology departments increase access to vitreoretinal diagnostics, angiography imaging, and injection-based pharmacologic therapies. Expanded infrastructure also supports workforce development through ophthalmology residency programs and subspecialty training in retina and glaucoma. Stronger clinical networks improve patient referral flows from primary screening centers to tertiary treatment facilities, increasing treatment initiation rates for chronic retinal disorders.

Category-wise Analysis

Drug Class Insights

Anti-VEGF agents are anticipated to secure around 58% of the ophthalmic injectable market revenue share in 2026, reflecting widespread clinical adoption for treatment of retinal vascular disorders. Anti-vascular endothelial growth factor therapies directly inhibit abnormal angiogenesis associated with macular degeneration, diabetic retinopathy, and retinal vein occlusion. Ophthalmology specialists increasingly rely on targeted anti-angiogenic drugs to prevent retinal vascular leakage and preserve visual acuity. Regulatory approvals from authorities including the U.S. Food and Drug Administration and the European Medicines Agency strengthen physician confidence in biologic anti-angiogenic therapies.

Corticosteroids are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by increasing utilization for inflammatory retinal disorders. Corticosteroid injectables provide anti-inflammatory and immunomodulatory effects that help control macular edema and inflammatory ocular diseases. Intravitreal corticosteroid implants deliver sustained drug release, enabling prolonged therapeutic activity within retinal tissues. Healthcare authorities including the National Eye Institute highlight inflammatory processes as important contributors to retinal disease progression.

Corticosteroid therapy addresses these pathways through suppression of inflammatory cytokines and vascular permeability.

Indication Insights

Age-related macular degeneration (AMD) extracts are poised to dominate with a forecasted market share of nearly 41% in 2026, powered by increasing prevalence among aging populations and established treatment protocols using injectable therapies. Macular degeneration represents a leading cause of vision impairment within elderly populations worldwide. Public health institutions, including the World Health Organization recognize age-related retinal degeneration as a significant contributor to visual disability.

Clinical management of AMD relies heavily on intravitreal injection of anti-angiogenic drugs capable of suppressing abnormal retinal blood vessel formation. Ophthalmologists routinely implement injection-based therapy to prevent disease progression and preserve visual acuity.

Diabetic retinopathy is estimated to be the fastest-growing segment from 2026 to 2033, fueled by rising diabetes prevalence and expanding retinal screening initiatives. Global health organizations including the International Diabetes Federation highlight rapid growth in diabetes prevalence across both developed and emerging economies. Prolonged hyperglycemia can damage retinal microvasculature, resulting in progressive vision impairment when untreated. Healthcare providers increasingly implement retinal screening programs for individuals diagnosed with diabetes. Early detection enables physicians to initiate treatment before irreversible retinal damage occurs.

Regional Insights

North America Ophthalmic Injectable Market Trends

North America is expected to lead with an estimated 38% of the ophthalmic injectable market share in 2026, supported by strong retinal disease diagnosis capacity and advanced treatment infrastructure across the United States and Canada. A dense network of ophthalmology clinics, retina specialty centers, and ambulatory surgical facilities enables large-scale administration of intravitreal therapies for conditions such as age-related macular degeneration, diabetic retinopathy, and retinal vein occlusion. High clinical adoption of anti-VEGF therapeutics supports consistent treatment volumes within tertiary hospitals and specialty eye institutes.

Strong biopharmaceutical innovation ecosystems across the United States and Canada further reinforce regional leadership through continuous development and commercialization of ophthalmic biologics. Major pharmaceutical and biotechnology organizations maintain research pipelines focused on retinal therapeutics, including long-acting anti-VEGF molecules, corticosteroid implants, and gene-based ophthalmic treatments. Robust regulatory pathways and accelerated drug approval mechanisms encourage rapid introduction of new injectable therapies into clinical practice.

Europe Ophthalmic Injectable Market Trends

Europe represents a mature and technologically advanced environment for ophthalmic injectable therapies, supported by strong clinical research activity and highly structured healthcare delivery systems. Countries such as Germany, France, Italy, Spain, and the United Kingdom maintain extensive ophthalmology hospital networks equipped with advanced retinal diagnostic technologies including optical coherence tomography, fundus imaging, and angiography systems. These capabilities enable early detection of retinal diseases such as age-related macular degeneration, diabetic macular edema, and retinal vein occlusion, conditions frequently treated through intravitreal pharmacologic therapy.

Advanced regulatory frameworks and coordinated pharmacovigilance systems support safe and structured introduction of innovative ophthalmic drugs across healthcare systems. The European Medicines Agency (EMA) regulatory pathway encourages multi-country clinical trials and cross-border research collaboration, accelerating development of novel biologic agents and long-acting injectable formulations. Pharmaceutical manufacturers frequently conduct retinal therapy trials through collaborative networks involving hospitals and ophthalmology research institutes in countries such as Switzerland, the Netherlands, and Sweden, strengthening regional innovation capacity.

Asia Pacific Ophthalmic Injectable Market Trends

Asia Pacific is forecasted to be the fastest-growing market for ophthalmic injectable treatments between 2026 and 2033, stimulated by rapid expansion of retinal disease diagnosis programs and increasing availability of specialized ophthalmic treatment infrastructure. Healthcare modernization across China and India strengthens hospital capacity for retinal imaging, intravitreal drug administration, and long-term patient monitoring. Large diabetic populations in these countries create substantial clinical demand for therapies addressing diabetic retinopathy and macular edema, conditions frequently treated through injectable pharmacologic intervention.

Public healthcare expansion programs focus on blindness prevention, vision screening, and ophthalmology service integration within tertiary hospitals, increasing detection of treatable retinal conditions.

Clinical adoption growth is further supported by healthcare system strengthening across Japan and South Korea, where advanced diagnostic infrastructure and aging population demographics generate sustained demand for retinal disease management. High prevalence of age-related macular degeneration and retinal vascular disorders encourages early clinical intervention through intravitreal pharmacologic therapy. Hospitals in these countries operate advanced retinal imaging platforms, including optical coherence tomography and fluorescein angiography, enabling accurate disease staging and repeated monitoring required for injection-based treatment protocols.

Competitive Landscape

The global ophthalmic injectable market structure demonstrates moderate concentration, characterized by the presence of several multinational pharmaceutical organizations that maintain strong influence over biologic retinal drug commercialization and clinical adoption. Key participants such as Novartis, F. Hoffmann-La Roche, Regeneron Pharmaceuticals, and Bristol-Myers Squibb contribute significantly to therapeutic development targeting retinal disorders including age-related macular degeneration, diabetic macular edema, and retinal vein occlusion.

Competitive differentiation increasingly relies on development of long-acting injectable formulations and next-generation retinal therapeutics that extend treatment intervals while maintaining visual acuity outcomes. Research strategies focus on sustained-release biologic agents, antibody-based drugs, and novel therapeutic pathways that target inflammation and vascular permeability within retinal tissue. Global commercialization networks enable efficient distribution of injectable ophthalmic drugs through hospital pharmacies, ophthalmology clinics, and specialty treatment centers. Strong collaboration between pharmaceutical developers and ophthalmology specialists further supports physician training in advanced retinal pharmacotherapy and injection protocols.

Key Industry Developments

- In December 2025, Amneal Pharmaceuticals announced that the U.S. Food and Drug Administration (FDA) approved cyclosporine ophthalmic emulsion 0.05%, a sterile preservative-free formulation supplied in single-use vials and developed as a generic equivalent to the dry eye treatment RESTASIS.

- In December 2025, Sagent Pharmaceuticals announced the launch of Bludigo® (indigotindisulfonate sodium injection) through a strategic partnership with Provepharm to expand the injectable diagnostic dye portfolio and strengthen visualization capabilities in surgical and ophthalmic procedures.

- In July 2025, Torrent Pharmaceuticals announced plans to launch oral and injectable semaglutide formulations by 2026 following patent expiry of the originator drug, aiming to expand access to injectable metabolic therapies and strengthen presence in the global diabetes treatment segment.

Companies Covered in Ophthalmic Injectable Market

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Regeneron Pharmaceuticals, Inc.

- Bristol-Myers Squibb Company

- Alcon Pharmaceuticals

- Allergan

- Valeant Pharmaceuticals International, Inc.

- Alimera Sciences

- ThromboGenics, Inc.

- Regeneron Pharmaceuticals

Frequently Asked Questions

The global ophthalmic injectable market is projected to reach US$ 21.7 billion in 2026.

Rising prevalence of retinal disorders such as AMD and diabetic retinopathy, growing adoption of intravitreal biologic therapies, and expansion of advanced ophthalmology treatment infrastructure, are driving the market.

The market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Expansion of ophthalmology infrastructure in emerging healthcare systems and growing adoption of long-acting biologic therapies for retinal diseases such as AMD are unlocking key market opportunities.

Some of the key market players include Novartis AG, F. Hoffmann-La Roche Ltd, Regeneron Pharmaceuticals, Inc., and Bristol-Myers Squibb Company.