- Pharmaceuticals

- Injectable Suspensions Market

Injectable Suspensions Market Size, Share, and Growth Forecast, 2025 - 2032

Injectable Suspensions Market by Product Type (Steroid Injectable Suspensions, Non-Steroid Injectable Suspensions), Application (Oncology, Cardiovascular Diseases, Autoimmune Diseases, Infectious Diseases, Others), End-use (Hospitals, Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis for 2025 - 2032

Injectable Suspensions Market Size and Trend Analysis

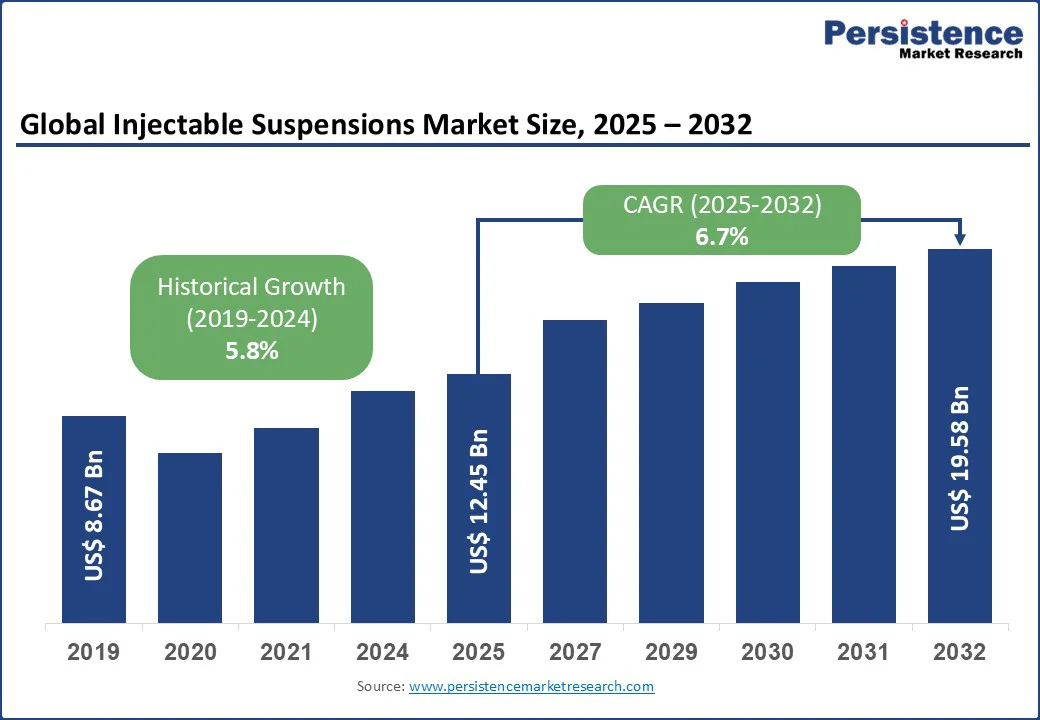

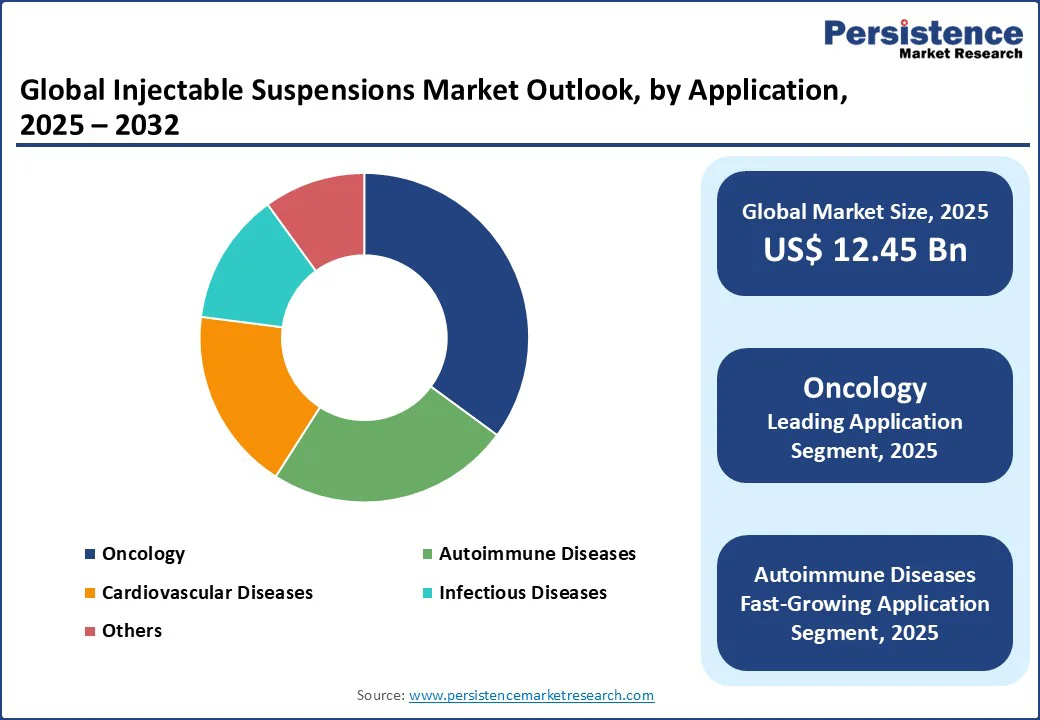

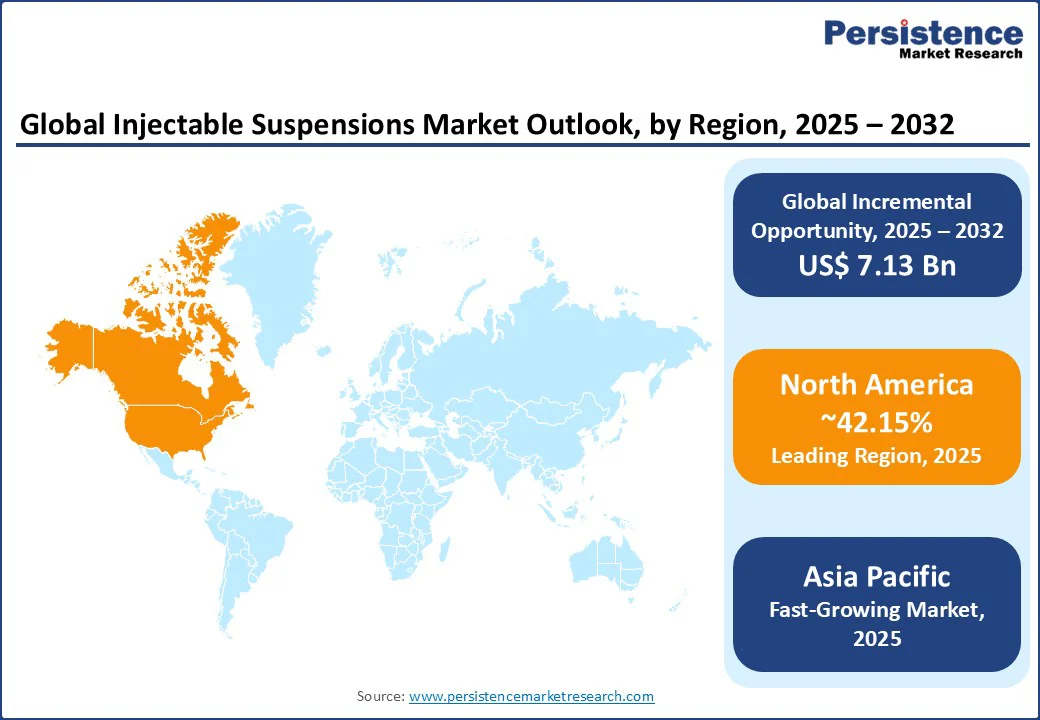

The global injectable suspensions market size is likely to be valued at US$12.45 Bn in 2025 and reach US$19.58 Bn by 2032, growing at a CAGR of 6.7% during the forecast period from 2025 to 2032.

Key Industry Highlights:

- Leading Region: North America holds a 42.15% share in 2025, driven by advanced healthcare infrastructure, high R&D investments, and a strong presence of key pharmaceutical companies in the U.S. and Canada.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, propelled by increasing healthcare expenditure, rising prevalence of chronic diseases, and growing biopharmaceutical production in China and India.

- Investment Plans: The U.S. National Institutes of Health (NIH) allocated $41.7 billion for medical research in 2024, boosting innovation in injectable advanced drug delivery systems for oncology and autoimmune diseases.

- Dominant Product Type: Non-Steroid Injectable Suspensions account for 58.6% of the market share, attributed to their widespread use in chronic disease management and cost-effectiveness.

- Leading Application: Oncology contributes over 35.12% of market revenue, driven by the rising global cancer burden and demand for targeted therapies.

| Global Market Attribute | Key Insights |

|---|---|

| Injectable Suspensions Market Size (2025E) | US$ 12.45Bn |

| Market Value Forecast (2032F) | US$ 19.58Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

The injectable suspensions market is experiencing robust growth, driven by increasing demand for advanced drug delivery systems in critical healthcare sectors such as oncology, cardiovascular diseases, and autoimmune disorders.

Injectable suspensions, known for their ability to deliver precise dosages and sustained drug release, are essential for treating complex medical conditions. Moreover, the rise in chronic diseases, coupled with innovations in biopharmaceutical manufacturing, supports market expansion.

Rising Prevalence of Chronic Diseases and Demand for Targeted Therapies

The global injectable suspensions market is experiencing significant growth due to the increasing prevalence of chronic diseases such as cancer, cardiovascular diseases, and autoimmune disorders. According to the World Health Organization (WHO), cancer accounted for nearly 9.7 million deaths globally in 2022, driving demand for targeted therapies delivered via injectable suspensions.

These formulations offer precise drug delivery and sustained release, improving treatment outcomes for complex conditions. According to the Centers for Disease Control and Prevention (CDC), approximately 6 in 10 adults in the United States have at least one chronic disease, fueling demand for advanced therapeutics.

The Asia Pacific region, particularly China and India, is witnessing a surge in chronic disease cases due to aging populations and lifestyle changes. Companies such asPfizer and Novartis are investing heavily in R&D to develop innovative injectable suspensions, with Pfizer reporting an increase in biologics sales in 2024. Government healthcare initiatives and rising patient awareness further ensure sustained market growth through 2032.

Challenges of High Development Costs and Regulatory Landscape

The injectable suspensions market faces challenges due to high development costs and stringent regulatory requirements. These costs limit smaller players’ ability to compete in the injectable suspensions market. Additionally, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose rigorous standards for product safety and efficacy, delaying market entry.

Compliance with Good Manufacturing Practices (GMP) and addressing concerns over product stability further increase costs. Competition from oral and topical drug delivery systems, which are less invasive, also poses a challenge, particularly in cost-sensitive markets, restraining overall market growth.

Injectable suspensions must maintain consistent stability over their shelf life, which is often complicated by the presence of suspended particles that can settle, aggregate, or degrade. Formulating stable suspensions requires careful selection of excipients, advanced technology, and thorough testing, all of which add layers of complexity and cost. Manufacturing such products under sterile conditions adds to challenges, requiring specialized equipment and rigorous contamination control measures.

Opportunity: Advancements in Biologics and Personalized Medicine

The injectable suspensions market is poised for significant growth, driven by advancements in biologics and personalized medicine. Biologics, including monoclonal antibodies, vaccines, and gene therapies, are increasingly dependent on injectable suspensions for precise and effective drug delivery. These therapies target complex diseases such as cancer, autoimmune disorders, and rare genetic conditions, where personalized treatment is crucial.

Leading pharmaceutical companies such as Roche and Amgen are at the forefront of innovating targeted injectable therapies that improve patient outcomes. For instance, Roche’s oncology portfolio includes multiple injectable biologics designed for tailored cancer treatments. Similarly, Amgen’s biologics pipeline focuses on autoimmune diseases with injectable suspensions as a key delivery method.

Government support further fuels market expansion. The EU’s Horizon Europe program, allocating €95.5 billion for health research between 2021 and 2027, fosters innovation in biologics and drug delivery technologies. As drug delivery technologies evolve, manufacturers have increasing opportunities to develop high-efficacy, stable, and affordable injectable suspensions, positioning the market for robust growth through 2032.

Category-wise Analysis

By Product Type

- Non-steroid injectable suspensions hold the largest market share, approximately 58.6% in 2025, due to their widespread use in managing chronic diseases such as diabetes, oncology, and cardiovascular conditions. Their cost-effectiveness and versatility in delivering biologics and small-molecule drugs make them a preferred choice. Companies such as Sanofi and Eli Lilly lead with extensive portfolios, catering to demand in hospitals and clinics across North America and Europe.

- Steroid injectable suspensions are the fastest-growing segment, driven by increasing demand for treatments in autoimmune diseases and inflammatory conditions. Their adoption is rising in specialized applications, such as rheumatoid arthritis and lupus, with brands such as Pfizer and Merck expanding offerings in the Asia Pacific and North America, supported by growing healthcare investments.

By Application

- The oncology segment accounts for over 35.12% of revenue in 2025, driven by the global rise in cancer cases and demand for targeted therapies. Injectable suspensions are critical for delivering chemotherapy drugs and biologics, with major players such as Roche and Bristol-Myers Squibb supplying advanced formulations for cancer treatment in the U.S. and Europe.

- Autoimmune Diseases are the fastest-growing application, propelled by the increasing prevalence of conditions such as rheumatoid arthritis and multiple sclerosis. Injectable suspensions offer sustained drug release for biologics, with companies such as AbbVie and Novartis innovating for high-efficacy treatments. Growth in Asia Pacific and North America supports this segment’s rapid expansion.

By End-use

- The hospitals segment holds the largest share, contributing 38% in 2025, driven by the high volume of injectable suspension administration in inpatient settings. Hospitals rely on these formulations for critical care in oncology and cardiovascular treatments, with players such as Johnson & Johnson and Pfizer dominating supply chains in North America and Europe.

- Ambulatory surgical centers (ASCs) are the fastest-growing end-use segment, fueled by the rise in outpatient procedures and cost-effective care models. ASCs are increasingly adopting injectable suspensions for pain management and post-surgical treatments, with growth in the U.S. and Asia Pacific driven by healthcare infrastructure expansion.

Regional Insights

North America Injectable Suspensions Market Trends

North America dominates the injectable suspensions market, accounting for 42.15% in 2025, driven by advanced healthcare infrastructure and high R&D investments in the U.S. and Canada. According to the Centers for Medicare & Medicaid Services (CMS), the U.S. healthcare industry reached a total expenditure of $4.9 trillion in 2023, accounting for 17.6% of the nation's Gross Domestic Product (GDP). The industry relies heavily on injectable suspensions for oncology and cardiovascular treatments.

Canada’s growing biopharmaceutical sector drives demand for advanced formulations, per the Canadian Life Sciences Industry Report. Major players such as Pfizer and Merck dominate with extensive distribution networks, catering to hospital and clinic demands. Consumer preference for high-efficacy biologics further strengthens North America’s market position.

Asia Pacific Injectable Suspensions Market Trends

The Asia Pacific is the fastest-growing region, fueled by rising healthcare expenditure, increasing prevalence of chronic diseases, and robust biopharmaceutical production in China and India. China, a global leader in pharmaceutical manufacturing, contributes significantly to the supply of injectable suspensions, per the China National Medical Products Administration. India’s healthcare sector, supported by initiatives such as Ayushman Bharat, boosts demand for cost-effective formulations.

The region’s oncology and autoimmune disease treatment markets also contribute, with companies such as Novartis and Roche expanding their presence. Rising medical tourism and government-led healthcare reforms ensure the Asia Pacific’s rapid market growth through 2032.

Europe Injectable Suspensions Market Trends

Europe is the second fastest-growing region, driven by stringent regulatory standards, rising demand in oncology and autoimmune disease treatments, and healthcare infrastructure development in Germany and France. The European pharmaceutical market supports demand for injectable suspensions in hospital settings.

Biosimilars are gaining traction in Europe as cost-effective alternatives to branded biologics. The increasing acceptance and approval of biosimilars are expanding the injectable suspensions market, making treatments more accessible to a broader patient population.

Germany’s biopharmaceutical sector, a key consumer of biologics, benefits from players such as Roche and Sanofi. The EU’s health policies, including the EU4Health program, promote innovation in drug delivery systems, increasing demand for advanced formulations. Europe’s focus on quality and sustainability drives market growth through 2032.

Competitive Landscape

The global injectable suspensions market is highly competitive, characterized by a fragmented landscape with numerous global and regional players. Leading companies such as Pfizer, Novartis, and Roche dominate through extensive product portfolios and global distribution networks.

Regional players focus on localized offerings, particularly in the Asia Pacific. Companies are investing in advanced biopharmaceutical manufacturing and novel drug delivery systems to enhance market share, driven by demand for high-efficacy treatments in oncology and autoimmune diseases.

Key Industry Developments

- June 2025: Hikma Pharmaceuticals released a 40?mg/mL triamcinolone acetonide injectable suspension in the U.S. It's a corticosteroid used for a variety of inflammatory and autoimmune conditions and marks Hikma’s expansion into complex injectable offerings. Hikma is a top-three supplier of generic injectable medicines by volume in the US1, with a growing portfolio of more than 170 products.

- April 2025: NHS England became the first health system in Europe to offer the injectable form of nivolumab for cancer patients. The subcutaneous injection cuts administration time dramatically from about an hour to just 3-5 minutes-and is expected to benefit up to 15,000 patients annually, improving hospital capacity and patient convenience. This new method, approved by the Medicines and Healthcare products Regulatory Agency (MHRA), is available for patients with various cancers, including lung, bowel, and skin cancers, aiming to improve patient convenience and free up hospital capacity.

Companies Covered in Injectable Suspensions Market

- Pfizer Inc.

- GlaxoSmithKline plc

- Sanofi S.A.

- AstraZeneca plc

- Merck & Co., Inc.

- Johnson & Johnson

- Novartis AG

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- AbbVie Inc.

- Roche Facetiousness

- Roche Holding AG

- Others

Frequently Asked Questions

The Injectable Suspensions market is projected to reach US$12.45 Bn in 2025.

Rising prevalence of chronic diseases and demand for targeted therapies are the key market drivers.

The Injectable Suspensions market is poised to witness a CAGR of 6.7% from 2025 to 2032.

Advancements in biologics and personalized medicine are the key market opportunities.

Pfizer Inc., Novartis AG, Roche Holding AG, and Sanofi S.A. are key market players.