- Beauty & Personal Care

- Facial Injectable Market

Facial Injectable Market Size, Share, and Growth Forecast, 2025 - 2032

Facial Injectable Market By Product Type (Collagen, Hyaluronic Acid, Botulinum Toxin Type A), Generation (Gen X, Boomer, Millennials), Application (Aesthetics, Therapeutics), by End-user (Hospitals, Specialty Clinics), and Regional Analysis for 2025 - 2032

Facial Injectable Market Size and Trends Analysis

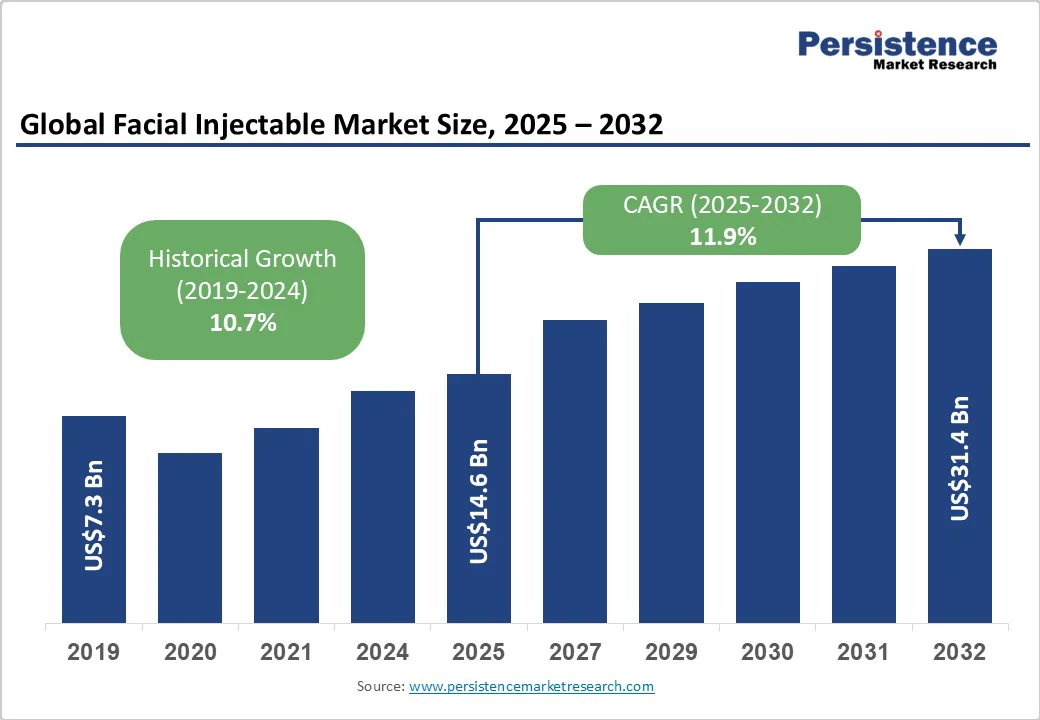

The global facial injectable market size is likely to be valued at US$14.6 Bn in 2025 and is estimated to reach US$31.4 Bn in 2032, growing at a CAGR of 11.9% during the forecast period 2025 - 2032, driven by rising consumer demand for minimally invasive, quick, and customizable treatments. In addition, the ongoing development of long-lasting neuromodulators and hybrid fillers influences growth.

Key Industry Highlights

- Marketing Campaign: Allergan Aesthetics introduced the Naturally You with Injectable Hyaluronic Acid Fillers campaign in September 2025. It aims to provide clear and factual education about HA injectable fillers.

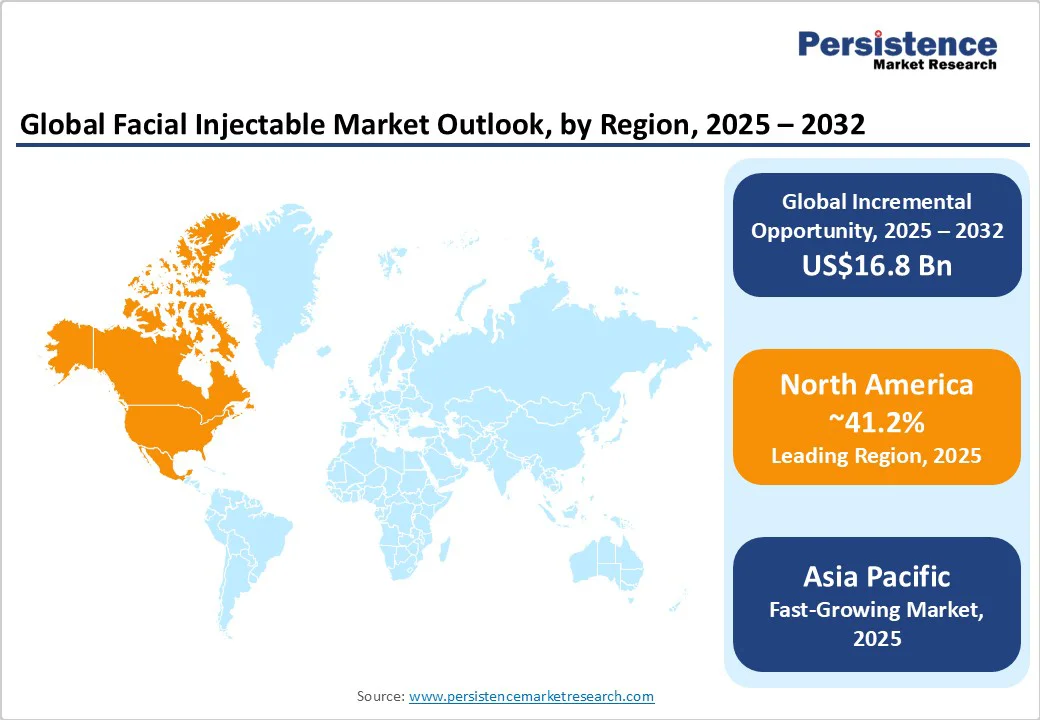

- Leading Region: North America, with about 41.2% share in 2025, due to early adoption of unique neuromodulators and fillers.

- Fastest-growing Region: Asia Pacific, owing to the influence of K- and J-beauty trends as well as increasing medical tourism for aesthetic treatments.

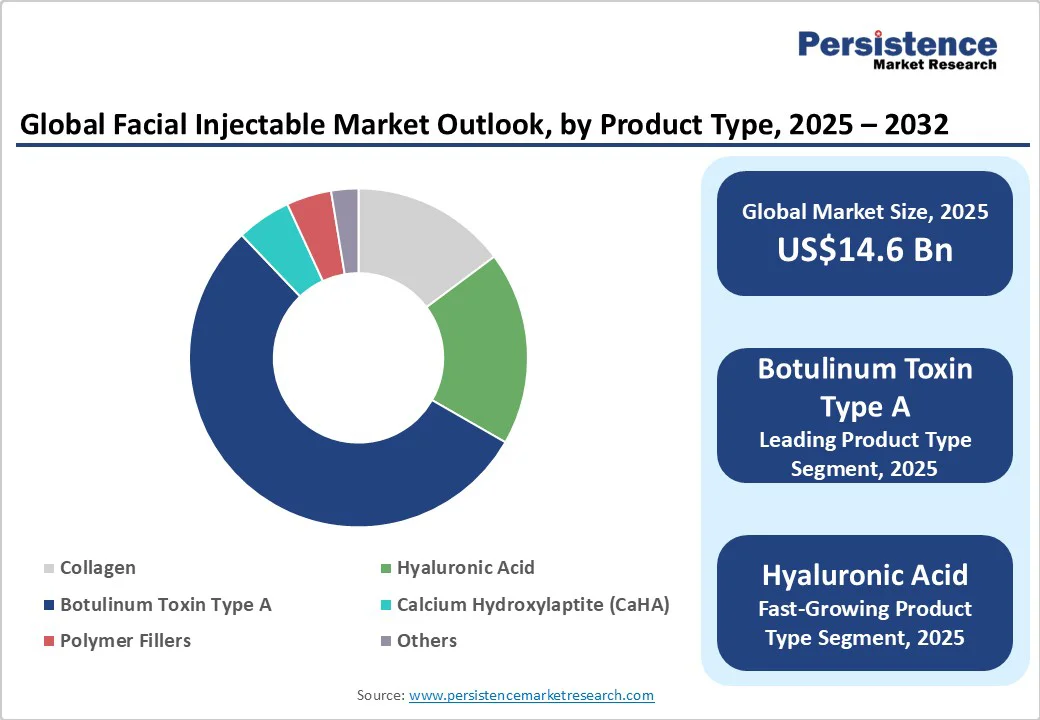

- Leading Product Type: Botulinum toxin type A is anticipated to hold nearly 54.6% share in 2025, backed by predictable results, minimal downtime, and expanded indications.

- Dominant Application: Aesthetics, approximately 59.3% of the facial injectable market share in 2025, owing to the rising demand for non-surgical, quick, and customizable treatments.

- Key End-user: Spa and beauty clinics are anticipated to record about 48.2% market share in 2025, owing to convenient access and the influence of social media marketing.

| Key Insights | Details |

|---|---|

| Facial Injectable Market Size (2025E) | US$14.6 Bn |

| Market Value Forecast (2032F) | US$31.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 11.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Popularity of Non-surgical Cosmetic Solutions

Consumers are now opting for minimally invasive procedures over surgical interventions due to faster recovery, lower risk, and surging accessibility. Awareness campaigns by medspas, influencers, and beauty brands have demystified injectables, showing results through social media before-and-after content.

For instance, Evolus’s Jeuveau campaigns in North America target millennials with relatable messaging, emphasizing subtle improvements rather than dramatic changes. Such campaigns educate consumers about treatment options, safety, and convenience, encouraging first-time users to explore facial injectables and expanding market growth.

Developments Transforming Facial Treatments

Continuous developments in aesthetic medicine are making injectables highly effective, long-lasting, and customizable. New formulations such as Allergan’s Daxxify, which lasts up to six months, and hybrid fillers such as HArmonyCa (combining hyaluronic acid with calcium hydroxyapatite) provide both volumizing and collagen-stimulating benefits.

Additionally, digital tools such as Galderma’s FACE simulation platform allow patients to visualize outcomes before treatment, increasing confidence in procedures. These technological developments help improve precision, comfort, and patient satisfaction, encouraging repeat treatments and raising adoption in both cosmetic and therapeutic applications.

Shifting Cultural and Social Beauty Preferences

Modern beauty ideals emphasize natural-looking results, skin quality, and individualized improvements rather than exaggerated changes. Young generations, especially in Asia Pacific and Europe, are adopting preventive or subtle injectables to maintain a youthful appearance and skin health.

Social media trends and celebrity influence play a key role as visible transformations are now anticipated to look smooth. Products such as Belotero Revive, which focus on hydration and skin glow rather than volume, comply with these evolving standards, propelling high consumer acceptance and fueling demand across diverse demographic groups.

Temporary Discomfort and Minor Adverse Effects Challenges Buying Decision

Despite being minimally invasive, facial injectables can cause short-term side effects such as bruising, swelling, redness, or mild pain at the injection site. These reactions, though usually transient, can deter first-time users or those with sensitive skin from opting for treatments. For example, some patients undergoing masseter reduction with botulinum toxin report swelling that lasts a few days, affecting social or professional commitments.

Clinics are now emphasizing post-treatment care and using techniques such as microcannulas to reduce bruising. However, concerns about even minor discomfort continue to act as a restraint on rapid adoption, especially among cautious consumers.

Ongoing Maintenance and Treatment Commitment

The temporary nature of various facial injectables requires regular repeat sessions to maintain results. Neuromodulators require re-administration every few months, and hyaluronic acid fillers gradually dissolve over time. This necessity for repeated visits tends to be a financial and logistical burden for consumers, leading some to avoid or delay treatments.

For instance, patients using skin boosters or volumizing fillers in Europe often schedule maintenance every six to nine months, which can affect long-term commitment. The requirement for consistent upkeep acts as a barrier to market expansion, specifically in price-sensitive or time-constrained segments.

Shift from Targeted Wrinkle Treatment to Holistic Facial Rejuvenation To Fuel More Opportunities

The market is moving beyond simple wrinkle correction toward holistic facial improvement. Patients now seek facial harmony, including volume restoration, skin texture improvement, and contour refinement. Hybrid fillers that combine hyaluronic acid with calcium hydroxyapatite allow simultaneous volumization and collagen stimulation, addressing multiple concerns in one session.

Clinics in Europe and North America are adopting multi-area treatment plans that treat the forehead, cheeks, and jawline together for natural-looking symmetry. This shift creates opportunities for new product development and treatment protocols. They help attract clients who prefer more comprehensive, long-term aesthetic solutions rather than isolated line reduction.

Precision Techniques through Micro-dosing and Strategic Placement

Micro-dosing, i.e., using small amounts of product in carefully chosen locations, has gained traction for subtle, preventative, or corrective outcomes. This approach reduces the risk of overfilling and creates natural results, appealing to young clients seeking early interventions. For example, the use of micro-Botox in the upper face and neck has become popular in South Korea to soften fine lines without restricting facial expression.

Strategic placement also allows practitioners to personalize treatments for individual facial anatomy, increasing patient satisfaction and repeat visits. The rising adoption of these techniques encourages development in low-dose formulations and specialized injectables.

Improved Practitioner Training and Certification Programs

As demand surges for complex and precise treatments, proper training for practitioners is becoming a key growth opportunity. New courses on anatomy, injection techniques, and unique formulations enable dermatologists and aesthetic clinicians to deliver safe and effective results.

Programs such as Galderma’s FACE simulator in Europe provide hands-on learning and outcome visualization, improving confidence for practitioners and patients. Expanding access to such training, mainly in emerging markets, tends to increase adoption, reduce adverse events, and build consumer trust. This creates a more sustainable market for facial injectables worldwide.

Category-wise Analysis

Product Type Insights

Botulinum toxin type A is poised to account for nearly 54.6% of the market share in 2025, as it delivers predictable results with minimal downtime, making it suitable for busy patients seeking subtle improvements. Its applications have expanded beyond forehead lines to include jawline slimming, masseter reduction, and even neck bands.

The 2023 U.S. launch of Daxxify, a longer-lasting alternative to Botox, has further increased interest in botulinum toxin treatments as they reduce the frequency of clinic visits.

Cosmetic-grade hyaluronic acid is seeing steady demand as it delivers versatility, working as both a volumizer and a skin-quality enhancer. Unlike permanent fillers, it is reversible, giving patients confidence in trying aesthetic treatments.

New formulations such as Skinvive in the U.S. focus on hydration and glow rather than just volume, complying with global trends toward natural and radiant results. This dual role of correction and skin health support keeps hyaluronic acid in consistent demand.

Application Insights

The aesthetics segment will likely hold a share of around 59.3% in 2025, as consumer preferences are shifting toward non-surgical and minimally invasive procedures that deliver quick results with little downtime. Rising interest in preventive treatments among young adults, combined with social media influence and the popularity of subtle enhancements, is broadening the market. New product launches are also attracting patients looking for natural-looking results, boosting adoption in clinics and medspas.

The therapeutics application is witnessing decent growth as botulinum toxin type A and other injectables are extensively used to treat medical conditions beyond aesthetics, such as chronic migraines, hyperhidrosis, and muscle spasticity.

Regulatory approvals expanding these indications, including Botox’s approval for cervical dystonia and platysma band treatment, are supporting steady adoption among healthcare providers, creating a rising demand alongside cosmetic uses.

End-user Insights

Spa and beauty clinics are expected to account for approximately 48.2% in 2025, as they provide convenient and accessible locations for non-surgical aesthetic treatments that appeal to young and first-time patients. These clinics often combine injectables with skincare services, creating a holistic beauty experience. For example, several U.S. medspas now bundle skin boosters such as Skinvive with facial treatments, attracting clients who prioritize hydration and glow alongside subtle improvements.

Specialty clinics are anticipated to grow rapidly in 2025, as they offer access to highly trained medical professionals who can perform complex or corrective procedures, including treating asymmetry, post-traumatic scarring, or medical conditions (hyperhidrosis using botulinum toxin).

Clinics in Europe and Asia Pacific, including dermatology-focused centers in Germany and South Korea, are embracing novel injectables such as hybrid HA-calcium fillers (HArmonyCa) to target both aesthetic and therapeutic requirements, ensuring safety and precision for high-risk treatments.

Regional Insights

North America Facial Injectable Market Trends

In 2025, North America is predicted to account for approximately 41.2% of the market share. It is attributed to rapid regulatory approvals and a push toward niche treatments. The U.S. Food and Drug Administration (FDA) is expanding indications such as approving Juvéderm Voluma XC for temple hollowing and Botox for neck platysma bands. These approvals are broadening the appeal of injectables beyond just wrinkle reduction.

Consumer preferences are also changing. Many people now seek natural-looking results, moving away from the overfilled ‘pillow-face’ look that dominated in the past. Celebrities dissolving fillers have reinforced this trend. Young adults in their 20s and 30s are turning to light-dose neuromodulators and subtle fillers for preventative care, seeing injectables as part of routine skincare.

Asia Pacific Facial Injectable Market Trends

In Asia Pacific, facial injectables are mainly shaped by cultural beauty ideals that focus on subtlety and skin quality rather than dramatic changes. Treatments such as skin boosters, which improve hydration and radiance, are highly popular, especially in South Korea and Southeast Asia. These comply with K-beauty and J-beauty trends that favor glowing, natural-looking skin.

Young consumers are propelling much of the demand, often using injectables for prevention rather than correction. Medical tourism also plays a key role, with countries such as South Korea and Thailand attracting international clients due to their unique techniques, new products, and competitive pricing. However, while South Korea and Japan have superior practitioner standards, other markets face challenges with uneven regulation.

Europe Facial Injectable Market Trends

In Europe, the market is influenced by cultural preferences for subtle and natural-looking results. Patients are now choosing skin boosters that improve hydration and texture rather than heavy fillers that change facial structure. Products such as Belotero Revive and Allergan’s HArmonyCa are gaining popularity for combining rejuvenation with collagen stimulation.

Regulation is stricter than in many other regions, with CE-mark standards and country-level rules that emphasize practitioner training and patient safety. This has slowed the rollout of some products but also built high trust among consumers, who are more conscious about product quality and side effects. Innovation is visible through hybrid fillers and the use of digital tools to help patients visualize outcomes before treatment.

Competitive Landscape

The global facial injectable market is highly fragmented, with established pharmaceutical giants competing alongside specialized aesthetic medicine companies and emerging biotech start-ups. Leading players are not only strengthening their portfolios with botulinum toxins and dermal fillers but are also investing in long-lasting and natural-looking formulations to maintain an edge. Partnerships and acquisitions are shaping competition as well. Small players are competing by introducing niche products focusing on safety and customization.

Business Strategies

Business strategies in facial injectables center on innovation through long-lasting neuromodulators and biostimulatory fillers, cost leadership with biosimilar toxins from Asia Pacific, and market expansion into medspas and emerging economies. Market leaders differentiate via safety data, physician training, and branding, while emerging models emphasize subscription-based aesthetic plans and digital-first patient engagement.

Key Industry Developments

- In February 2025, Evolus, Inc. bagged FDA approval for Evolysse Form and Evolysse Smooth injectable hyaluronic acid gels, the first two products in the Evolysse collection. This approval marked the company’s entry into the U.S. HA dermal filler market.

- In May 2024, Galderma introduced its hyaluronic acid injectable filler, Restylane VOLYME, in China. It also launched the complementary Shape Up Holistic Individualized Treatment (HIT) in the country.

Companies Covered in Facial Injectable Market

- Lumenis

- Johnson & Johnson

- Syneron Candela

- Hologic, Inc.

- Alma Lasers

- Solta Medical

- Novartis AG

- Becton, Dickinson and Company

- Galderma SA

- Antares Pharma Inc.

Frequently Asked Questions

The facial injectable market is projected to reach US$14.6 Bn in 2025.

Rising demand for minimally invasive treatments and increased awareness through beauty campaigns are the key market drivers.

The facial injectable market is poised to witness a CAGR of 11.9% from 2025 to 2032.

Key market opportunities include advanced practitioner training and expansion of preventive aesthetic care.

Lumenis, Johnson & Johnson, and Syneron Candela are a few key market players.