- Retail

- India Insurance Market

India Insurance Market Size, Share, and Growth Forecast, 2026 - 2033

India Insurance Market by Insurance Type (Life Insurance, General Insurance, Health Insurance), Customer Type (New Subscriptions, Others), Distribution Channel (Brokers & Agents, Bancassurance, Digital Channels), and Analysis 2026 - 2033

India Insurance Market Size and Trends Analysis

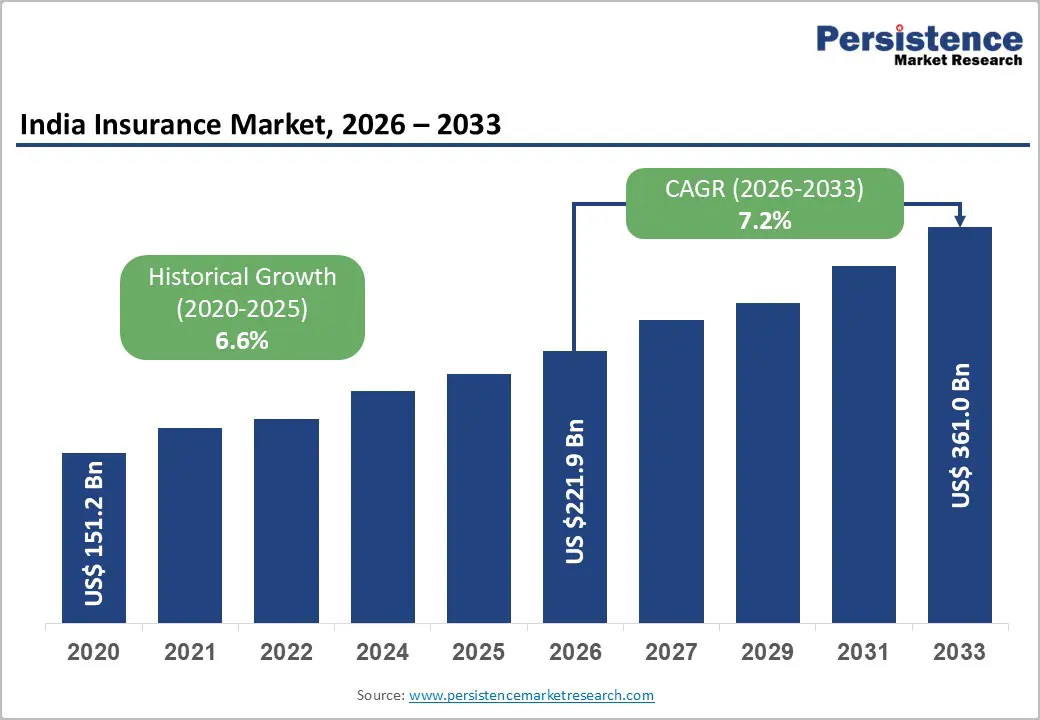

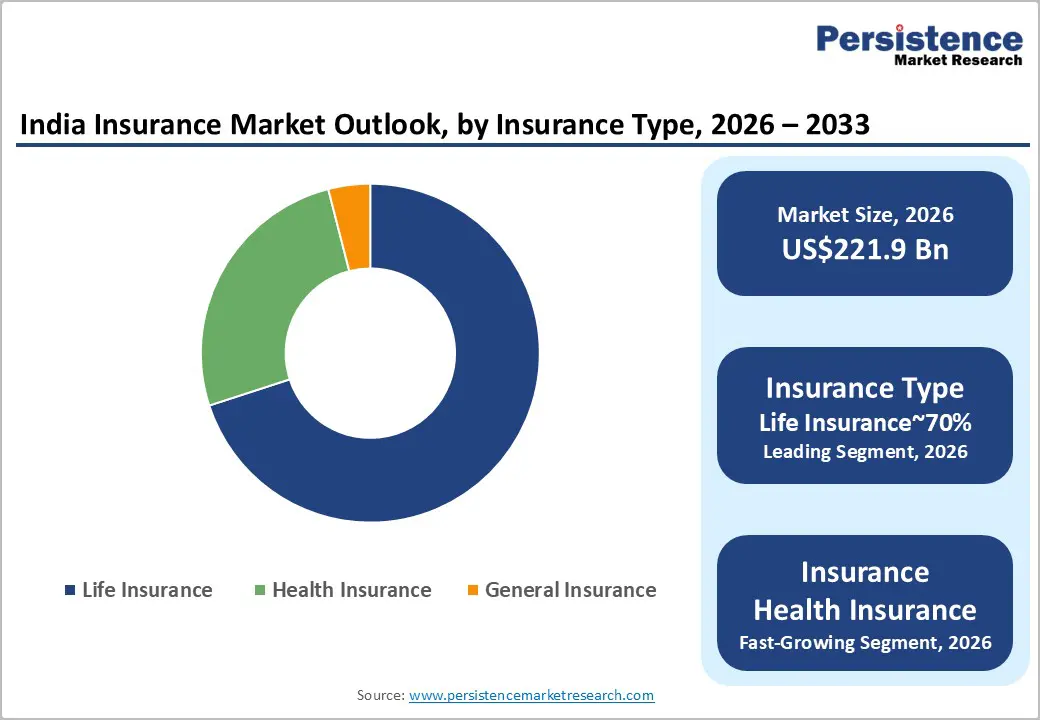

The India insurance market size is likely to be valued at US$221.9 billion in 2026 and is expected to reach US$361.0 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by rising domestic income levels, which are increasing the demand for financial protection across the country.

The expansion of digital distribution channels is accelerating policy adoption among diverse population segments, while digital platforms are lowering entry barriers for new customers. Continuous technological integration is further supporting steady uptake, particularly among urban and semi-urban consumers. Additionally, evolving regulatory frameworks aimed at expanding consumer coverage are reinforcing long-term market growth, ensuring sustained expansion over the coming years.

Key Industry Highlights:

- Leading Insurance Type: Life insurance is expected to lead, accounting for approximately 71% share in 2026 through widespread adoption, long-term savings preferences, and high-value risk coverage applications.

- Fastest-growing Insurance Type: Health insurance is expected to grow the fastest due to on-demand coverage, integration with preventive healthcare, hybrid digital-physical distribution workflows, and enterprise adoption through corporate health mandates.

- Leading Distribution Channel: Bancassurance is projected to dominate for simplicity, cost-efficiency, adoption, and functional integration across key financial sectors, holding approximately 52% share in 2026.

- Fastest-growing Distribution Channel: Digital channels are expected to grow fastest for complex, tech-driven, on-demand policy applications targeting younger, digitally-savvy cohorts with high personalization requirements.

| Key Insights | Details |

|---|---|

| India Insurance Market Size (2026E) | US$221.9 Bn |

| Market Value Forecast (2033F) | US$361.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Digital Underwriting Infrastructure

Advanced data analytics models are fundamentally restructuring risk assessment today. This technological advancement is expected to streamline policy issuance. Carriers actively utilize algorithms to eliminate manual processing bottlenecks effectively. Instantaneous evaluation capabilities directly improve corporate operational margin profiles worldwide. Such efficiency gains enable broader coverage across varied targeted demographics. Underwriters strategically redirect human expertise toward exceptionally complex anomalous portfolios. Machine learning frameworks constantly adapt alongside emerging behavioral consumer patterns. The resulting friction reduction consistently stimulates mass retail market adoption.

Seamless digital interfaces are projected to dominate modern distribution networks. Aggregators instantly simplify complex product comparisons for retail demographic segments. Policybazaar with PB Partners exemplifies this transparent marketplace architecture perfectly. Brokers use these integrated dashboards to optimize daily client interactions. Accelerated quoting mechanisms directly increase monthly sales conversion volumes significantly. Mobile applications empower agents working within remote provincial territories constantly. Real-time backend synchronization prevents embarrassing duplicate form submission errors entirely. Consequently, technology investment remains on track to boost overall profitability.

Preventive Healthcare Integration

Escalating medical treatment costs compel consumers toward proactive clinical wellness. This behavioral transition is forecast to fundamentally reshape traditional underwriting. Insurers actively incentivize healthy lifestyle choices through dynamic pricing models. Wearable device synchronization provides verifiable metrics for precise risk adjustment. Such continuous monitoring reduces aggregate claim frequency significantly over time. Preventive diagnostics catch potential severe illnesses during highly treatable stages. Data streams validate actual physical activity against self-reported health benchmarks. The resulting mutual benefit establishes highly resilient long-term customer relationships.

Ecosystem partnerships seamlessly connect clinical providers with broad coverage frameworks. Subscribers can easily access subsidized routine diagnostic testing facilities. Aditya Birla Health Insurance, in partnership with Activ Health, embodies this convergence. Rewards programs directly lower renewal costs for compliant, proactive individuals. This value proposition is poised to accelerate specialized category expansion. Gym memberships are often included in premium holistic wellbeing policy tiers today. Nutritionist consultations add tangible, immediate value beyond theoretical indemnification promises. Overall portfolio morbidity improves alongside enhanced consumer physical conditioning naturally.

Restraint Analysis - Rural Distribution Costs

Geographic population dispersion significantly increases physical customer acquisition expenditures. Fragmented transportation networks complicate consistent agent deployment across vast hinterlands. Low average premium sizes struggle to offset heavy logistical operational overhead. These structural constraints are anticipated to limit geographical expansion efforts. Limited, localized health facilities further dampen the regional appeal of medical products. Cash collections pose significant physical security risks during remote transit. Irregular rural internet connectivity completely sabotages real-time uploads to digital applications. Operators consequently hesitate to deploy extensive resources into isolated provincial territories.

Establishing permanent branch infrastructure requires massive, ongoing upfront capital commitments. Recruiting qualified local intermediaries proves exceptionally difficult outside metropolitan clusters. SBI Life with Smart Care struggles against these distinct hurdles. Maintaining continuous policyholder engagement demands innovative hybrid communication channels constantly. Without digital intervention, physical scaling remains on track to stall. Training scattered personnel imposes severe logistical coordination challenges across regions. High turnover among rural agents destroys carefully cultivated grassroots relationships. Profitability targets dictate concentrating efforts within denser urban agglomerations strategically.

Fraud Detection Complexity

Sophisticated, organized syndicates continually exploit vulnerabilities in claims processing workflows. Fabricated medical documentation forces investigators into prolonged manual verification procedures. These malicious activities are projected to inflate aggregate loss ratios. Manual auditing techniques frequently miss subtle cross-institutional historical criminal patterns. Resource-intensive reviews inherently delay legitimate reimbursements for honest affected individuals. Phony clinics invent phantom patients to extract illicit financial capital. Coordinated motor collision scams drain vast capital resources from carriers. Trust deficits, therefore, emerge between cautious providers and legitimate consumers.

Deploying advanced analytical countermeasures requires the acquisition of scarce specialized talent. Systemic data sharing among competitors is constrained by strict government privacy regulations. ICICI Lombard with AI Fraud Detection illustrates defensive technology investments. Predictive modeling algorithms require vast historical datasets to ensure proper training. This defensive operational necessity is positioned to drain internal resources. False positives occasionally penalize entirely legitimate complex medical compensation requests. Regulatory audits scrutinize automated denial mechanisms with extreme legal prejudice. Criminal adaptation continually forces expensive reactive security protocol updates.

Opportunity Analysis - Parametric Climate Protection

Increasingly volatile weather events severely threaten traditional agricultural livelihoods. Conventional indemnity assessments often delay critical post-disaster community recovery efforts. Parametric triggers are poised to revolutionize rural economic safeguards entirely. Pre-agreed payout thresholds automatically execute upon specific meteorological measurements instantly. This objective methodology consistently eliminates subjective damage evaluation disputes. Soil moisture sensors seamlessly communicate directly with centralized actuarial databases. Temperature spikes trigger automatic financial relief for vulnerable livestock populations. Swift capital injection stabilizes vulnerable communities during catastrophic environmental shocks.

Satellite imagery algorithms provide indisputable verification regarding localized rainfall deficiencies. Agri-tech collaborations distribute these specialized contracts directly to rural farmers. Reliance General, in partnership with Weather Protect, showcases this automated compensation model. Immediate liquidity allows immediate replanting following adverse seasonal weather conditions. Such predictable loss modeling is likely to attract global reinsurers. Cooperatives strategically bundle this vital protection with subsidized fertilizer disbursements. Blockchain smart contracts execute these transfers without human intervention seamlessly. Climate adaptation mechanisms subsequently become an indispensable agricultural input requirement permanently.

Embedded Ecosystem Platforms

Digital commerce platforms generate vast transactional contextual data streams continuously. Integrating coverage directly within consumer purchasing journeys drives conversion seamlessly. This invisible protection layer is anticipated to expand rapidly everywhere. Context-aware algorithms instantly suggest relevant policies during standard checkout procedures. Seamless bundling drastically reduces conventional standalone customer acquisition costs. Micro-durations align perfectly with temporary rental or spontaneous travel experiences. Personalized pricing reflects real-time behavioral insights captured via mobile apps. Embedded architectures, therefore, redefine traditional distribution boundary lines entirely today.

Travel portals routinely add flight cancellation protections at the time of booking. E-commerce marketplaces secure expensive electronic devices against accidental physical damage. Acko with Ride Insurance demonstrates contextual integration via digital networks. API connectivity allows instantaneous backend policy generation without consumer friction. These contextual deployments continue to normalize widespread automated insurance consumption. Food delivery applications offer instant micro-health coverage for freelance couriers. Payment gateways leverage transaction histories to seamlessly target pre-approved credit protection. Platform synergies thereby generate highly predictable recurring corporate revenue streams.

Category-wise Analysis

Insurance Type Insights

Life insurance is expected to dominate the market, accounting for approximately 71.0% of the total share in 2026. Cultural emphasis on familial financial security underpins widespread ongoing adoption. Tax-saving government incentives simultaneously compel systematic annual premium investments continually. Long-term savings objectives dictate dominant preferences across middle-class households everywhere. Max Life with Smart Term exemplifies these foundational protective offerings. Retirement planning requirements further sustain consistent portfolio expansion trajectories. Institutional stability successfully reinforces consumer confidence during turbulent macroeconomic cycles successfully. Agents actively leverage community relationships, maximizing provincial rural penetration effectively. Educational endowments secure future academic funding against parental mortality risks. This enduring trust mechanism continues to anchor overall sector growth. Such structural alignment ensures continuous dominance throughout the coming decade.

Health insurance is anticipated to be the fastest-growing segment, driven by rising private medical treatment expenses that necessitate robust financial buffers. Post-pandemic awareness permanently shifted priorities toward comprehensive clinical protection globally. Corporate employers increasingly mandate baseline coverage for modern productive workforces. Star Health with Comprehensive Insurance addresses these complex hospitalization costs. Outpatient diagnostic inclusions strongly appeal to preventive care advocates by nature. Specialized critical illness modules provide vital supplemental disease safeguards continually. Cashless facility networks drastically reduce patients' out-of-pocket costs during emergencies. Telemedicine consultations are standard features in premium, modern tiered packages. This convergence of necessity and accessibility is positioned to accelerate.

Distribution Channel Insights

Bancassurance is anticipated to lead, accounting for approximately 52% share through institutional synergy in 2026. Established retail banking relationships provide inherent advantages in consumer trust. Financial institutions possess comprehensive visibility into individual household cash flows. Such data access enables highly targeted protective product recommendations natively. Kotak Mahindra Life with Kotak Assured highlights seamless, integrated distribution. Branch personnel effortlessly bundle policies alongside traditional mortgage loan disbursals. Vast physical branch networks effectively penetrate geographically isolated provincial districts. Joint ventures between insurers and banks optimize shared infrastructure costs. Wealth managers integrate life coverage into holistic retirement planning blueprints. This operational alignment is expected to maintain market dominance securely. Enduring financial ecosystems thus anchor long-term, predictable premium accumulations successfully.

Digital channels are anticipated to be the fastest-growing segment, driven by smartphone proliferation, which democratizes access to sophisticated financial planning tools. Self-directed consumers demand autonomous, transparent product comparison environments constantly today. Eliminating intermediary commissions allows providers to offer highly competitive premium pricing. Digit General, with Go Digit, exemplifies this agile, direct-to-consumer philosophy. Intuitive mobile applications transform complex purchasing journeys into gamified experiences. Artificial intelligence chatbots deliver continuous, instantaneous, personalized advisory services globally. Younger cohorts explicitly reject traditional high-pressure face-to-face field sales tactics. Direct engagement pathways, therefore, rapidly secure increasingly larger operational footprints. Future growth remains intrinsically linked to continuous refinements of the digital interface.

Competitive Landscape

The India insurance market is highly consolidated, with leadership concentrated among major incumbents such as LIC, HDFC Life, and ICICI Prudential, whose scale, actuarial capabilities, and national distribution networks shape industry norms. These players exert significant functional influence through underwriting standards, digital platform integration, and regulatory engagement, establishing benchmarks for pricing, policy structures, and consumer trust across both life and health segments.

Competitive positioning reflects a bifurcation between legacy institutions pursuing vertically integrated wealth advisory and holistic insurance solutions, and insurtech entrants like Go Digit focusing on horizontal niche disruption through API-enabled digital distribution and embedded ecosystems. Industry dynamics are characterized by platform convergence, strategic partnerships with banks and e-commerce portals, and technology-driven operational efficiency, reinforcing structural consolidation while expanding access via digital channels and preventive health integration.

Key Industry Developments:

- In January 2026, Bajaj FinServ completed the acquisition of Allianz SE’s 23% stake in their life and general insurance joint ventures for approximately INR 21,390 crore (US$2.26 billion). This gives Bajaj FinServ complete control, allowing for more agile decision-making and a unified brand strategy in the competitive private space.

- In December 2025, IRDAI imposed an INR 1 crore (US$105,500) penalty on Reliance General Insurance for routing unauthorized payouts as disguised commissions. The action underscores a tightening regulatory stance on expense management, aiming to curb mis-selling and improve overall industry governance.

Companies Covered in India Insurance Market

- Life Insurance Corporation of India (LIC)

- HDFC Life Insurance Company

- ICICI Prudential Life Insurance

- SBI Life Insurance

- Max Life Insurance

- Tata AIA Life Insurance

- Kotak Mahindra Life Insurance

- Bajaj Allianz General Insurance

- ICICI Lombard General Insurance

- New India Assurance

- Star Health and Allied Insurance

- Aditya Birla Health Insurance

- Digit Insurance

- Acko General Insurance

- Policybazaar (PB Fintech)

- Go Digit

Frequently Asked Questions

The India insurance market is projected to be valued at US$221.9 billion in 2026 and is expected to reach US$361.0 billion by 2033, driven by rising domestic income, digital distribution adoption, and expanding financial protection demand across urban and semi-urban populations.

Digital underwriting and ecosystem integration are key market drivers because they streamline policy issuance, reduce operational inefficiencies, and support integration with preventive healthcare services. These advancements allow insurers to expand distribution more efficiently, deliver personalized products, and build stronger, long-term customer relationships across both retail and corporate segments.

The India insurance market is forecast to grow at a CAGR of 7.2% from 2026 to 2033, reflecting consistent adoption of life and health insurance, digital channel expansion, and increasing penetration of preventive healthcare-linked policies.

Health insurance is anticipated to grow the fastest due to rising demand for preventive care, corporate coverage mandates, and integration with digital health monitoring and wellness programs.

The India insurance market is relatively consolidated, with major players such as Life Insurance Corporation of India, HDFC Life Insurance, ICICI Prudential Life Insurance, SBI Life Insurance, and Max Life Insurance leading the market. These incumbents maintain their dominance through scale, regulatory trust, extensive distribution networks, and technology-driven operations. Meanwhile, insurtech companies such as Go Digit General Insurance are driving niche disruption through digital channels and embedded ecosystem models.